Oil

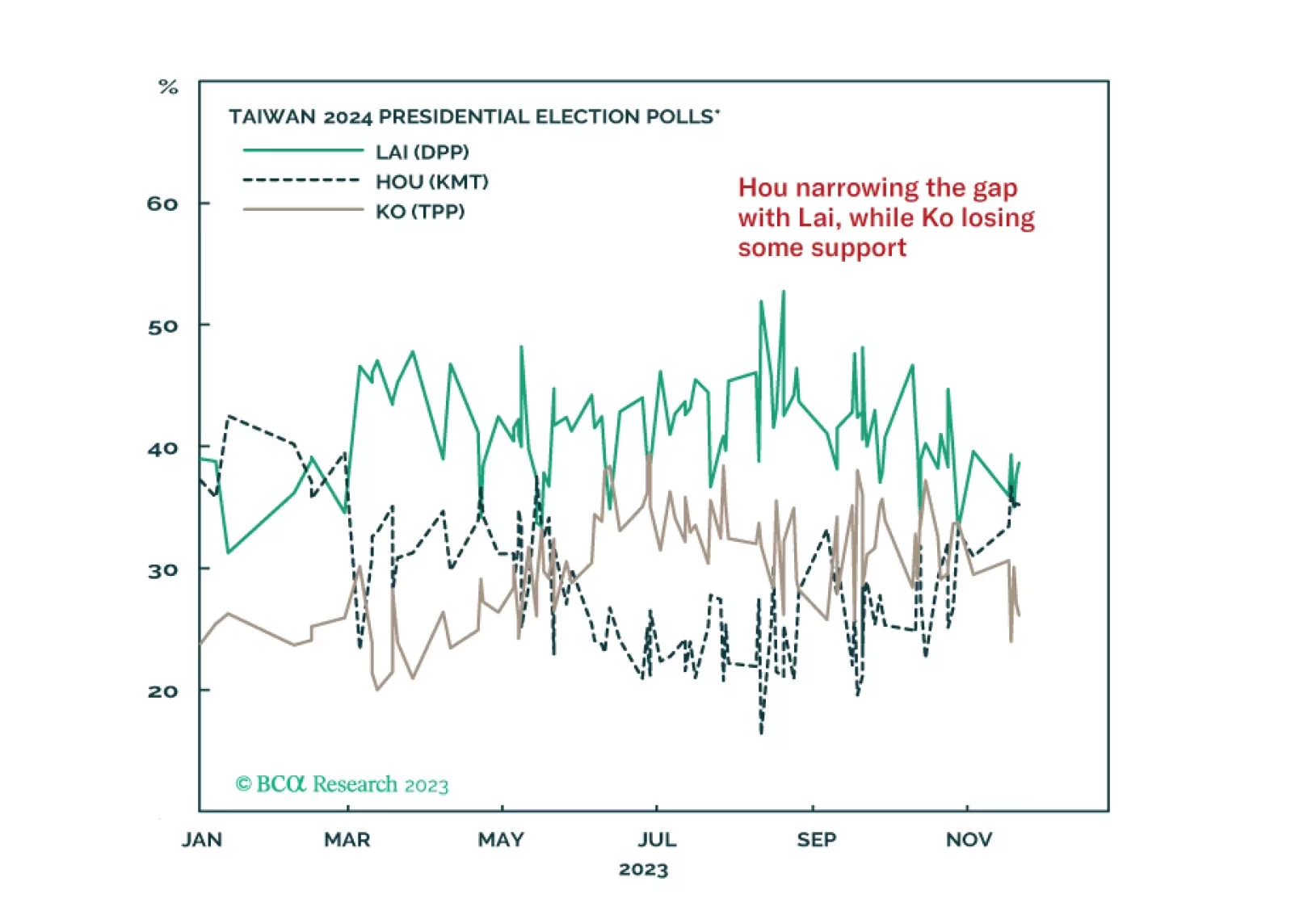

A series of notable events took place over the Thanksgiving holiday but none of them force us to change our fundamental assessments. The conflict in the Middle East is likely to escalate rather than de-escalate, while the Taiwan Strait has at least a 50/50 chance of seeing tensions escalate next year.

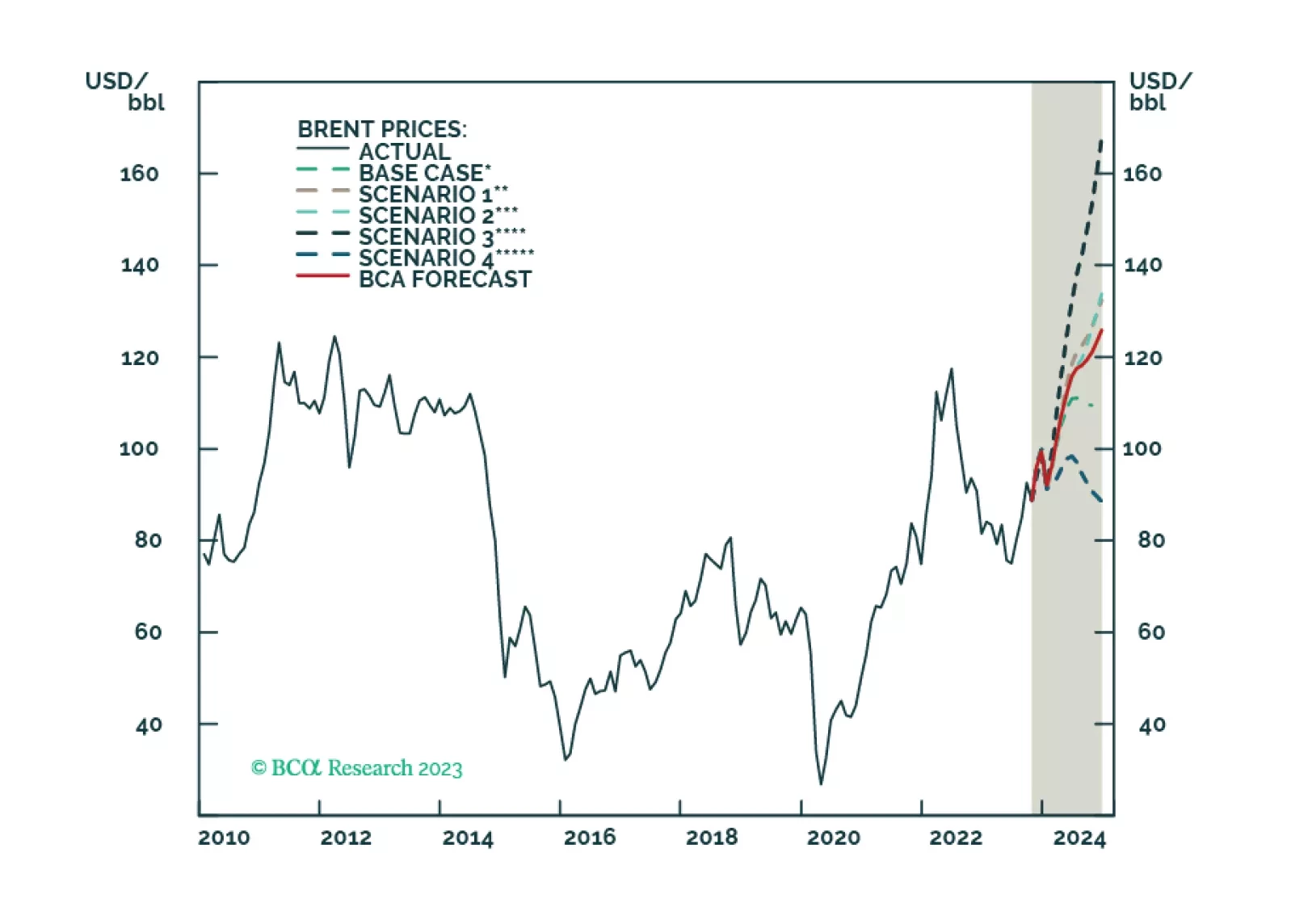

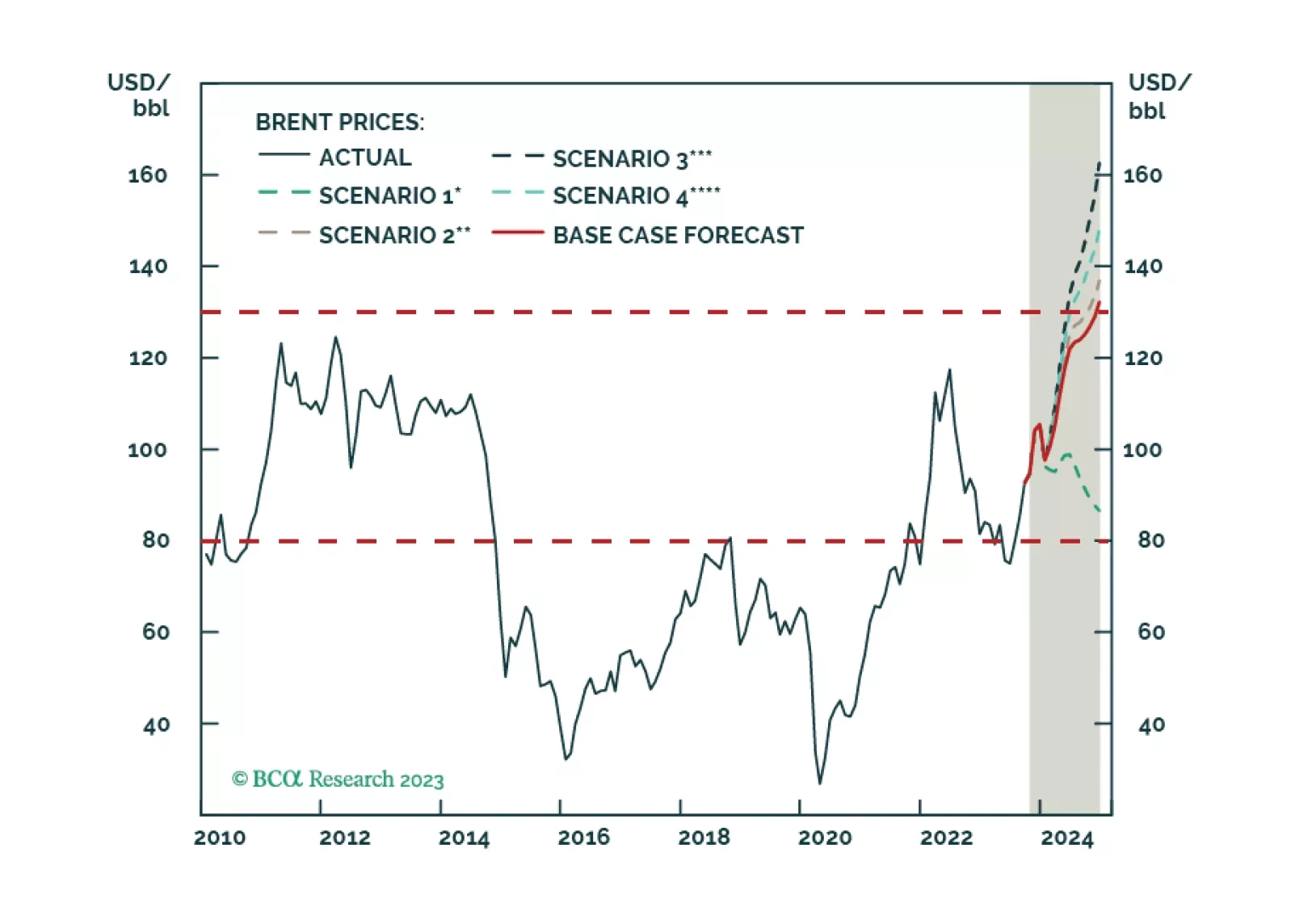

US and Chinese oil-demand strength will offset EU weakness next year. Incremental supply growth from non-OPEC 2.0 producers, coupled with a lower risk of the US enforcing its sanctions on Iranian oil exports, reduces our 2024 Brent price forecast by $6/bbl, and takes it to $112/bbl.

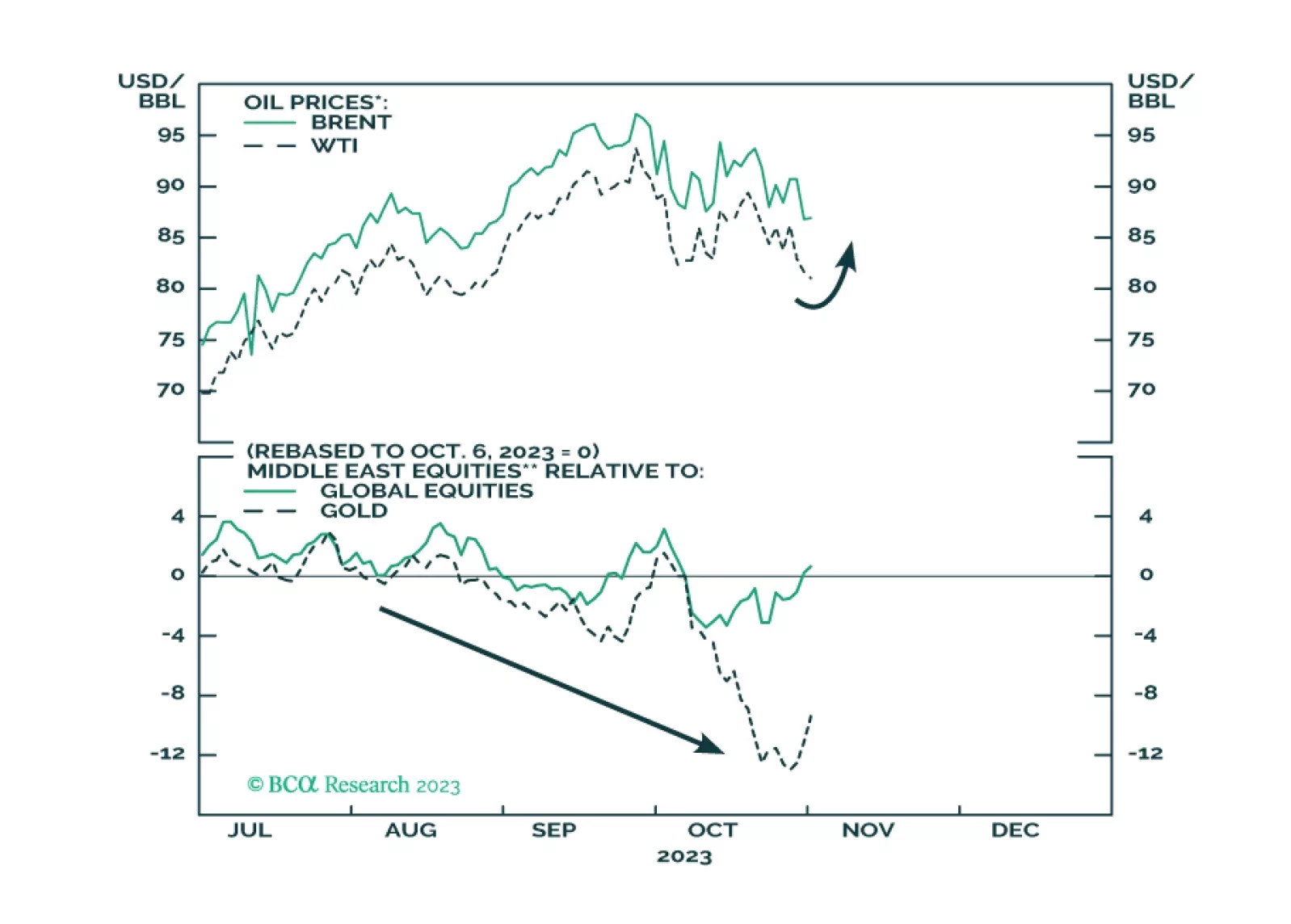

Investors should reduce risk, increase allocation to safe havens, and brace for oil price volatility and supply disruptions stemming from the Middle East over the next zero-to-12 months.

Economic fragmentation will accelerate in the wake of the Israel-Hamas and Russia-Ukraine wars. China’s fis-cal support for its economy; a still-strong US economy, and the preparation for a wider war in the Middle East involving Iran will elevate volatility and bias oil prices upward. We remain long equity and commodity exposure via the XOP, XME and COMT ETFs.

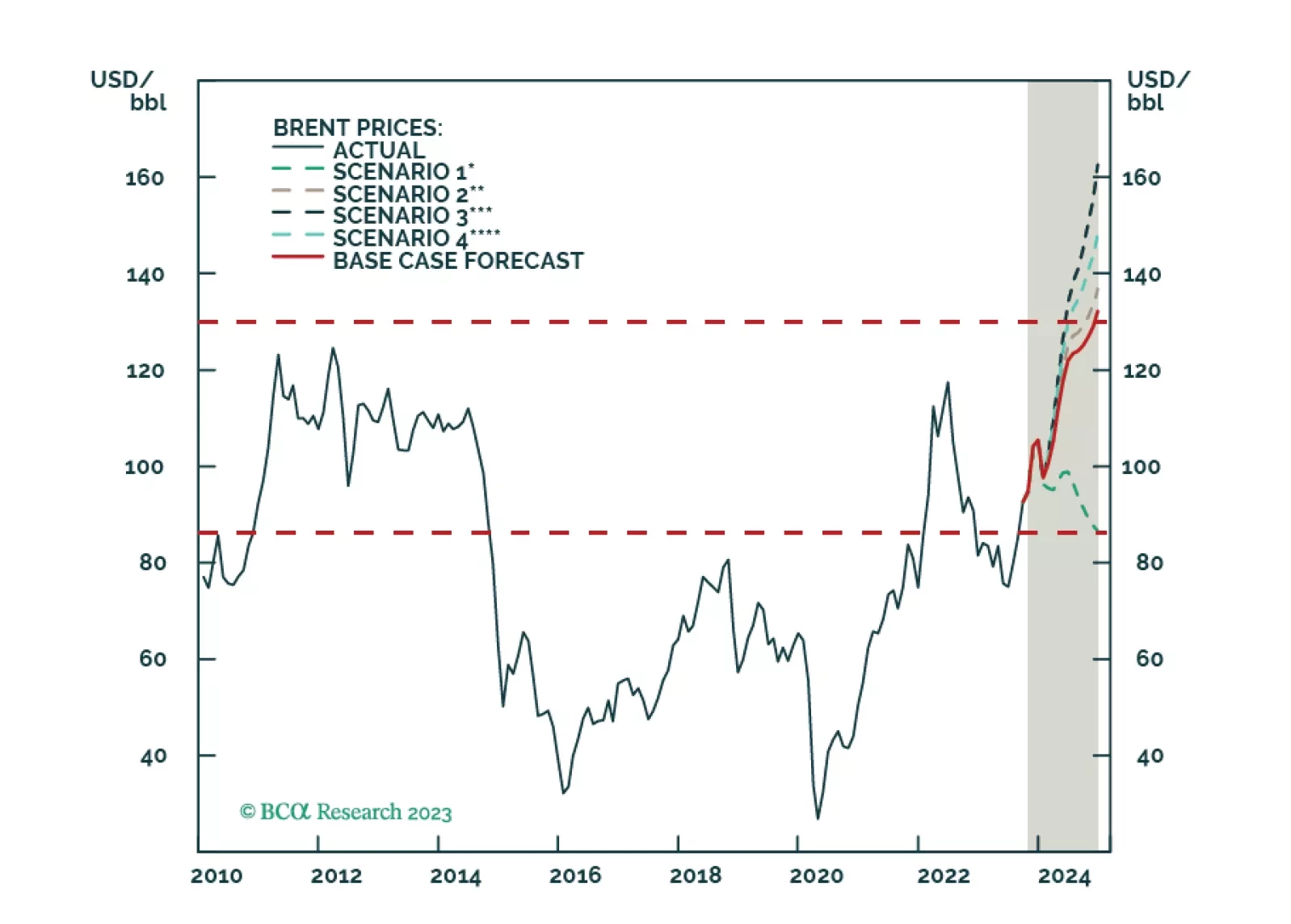

The US and core OPEC 2.0 are – wittingly or not – laying the groundwork for a price band with a floor and cap on oil prices – at $79/bbl and $130/bbl, respectively – “at least” to May 2024. This accommodates multiple goals for both. To meaningfully support policy, the US would need to scale up purchases to refill its SPR. We remain long the XOP and COMT ETFs for direct exposure to energy E+P equities and commodities.