Oil

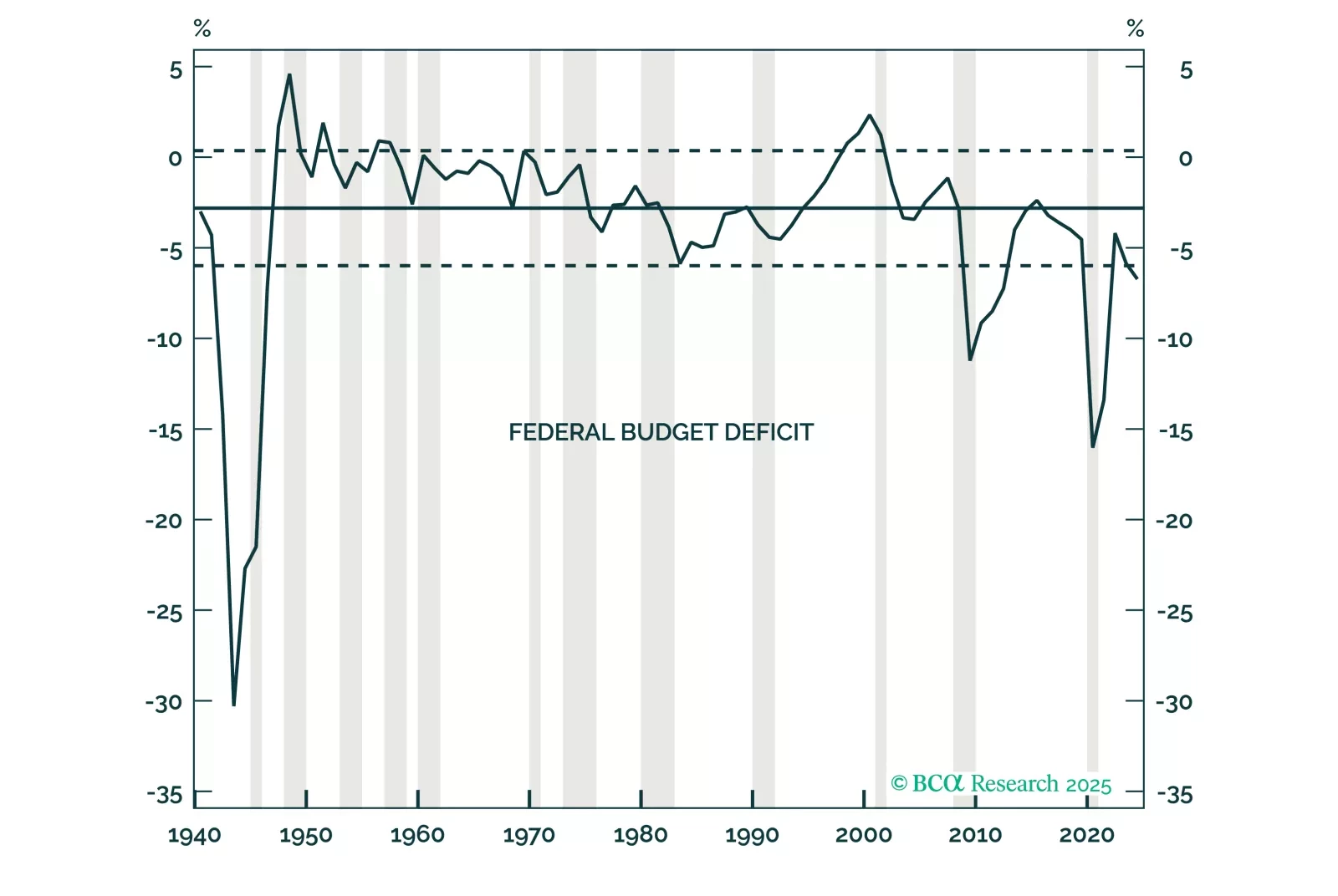

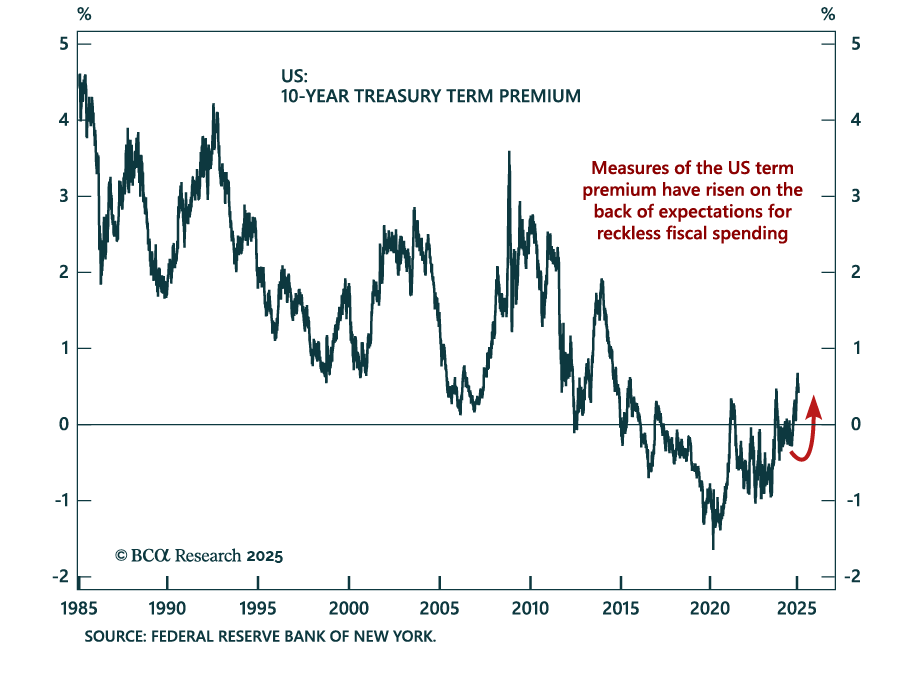

The 3-3-3 plan pitched by Treasury Secretary Scott Bessent will need several improbabilities to break its way if it is to meet its goals. We think it is much more likely that the plan will disappoint. Defensive asset allocations will outperform once it becomes clear that 3-3-3 will fall short, but we are currently neutral across the board because the disappointment may be months away.

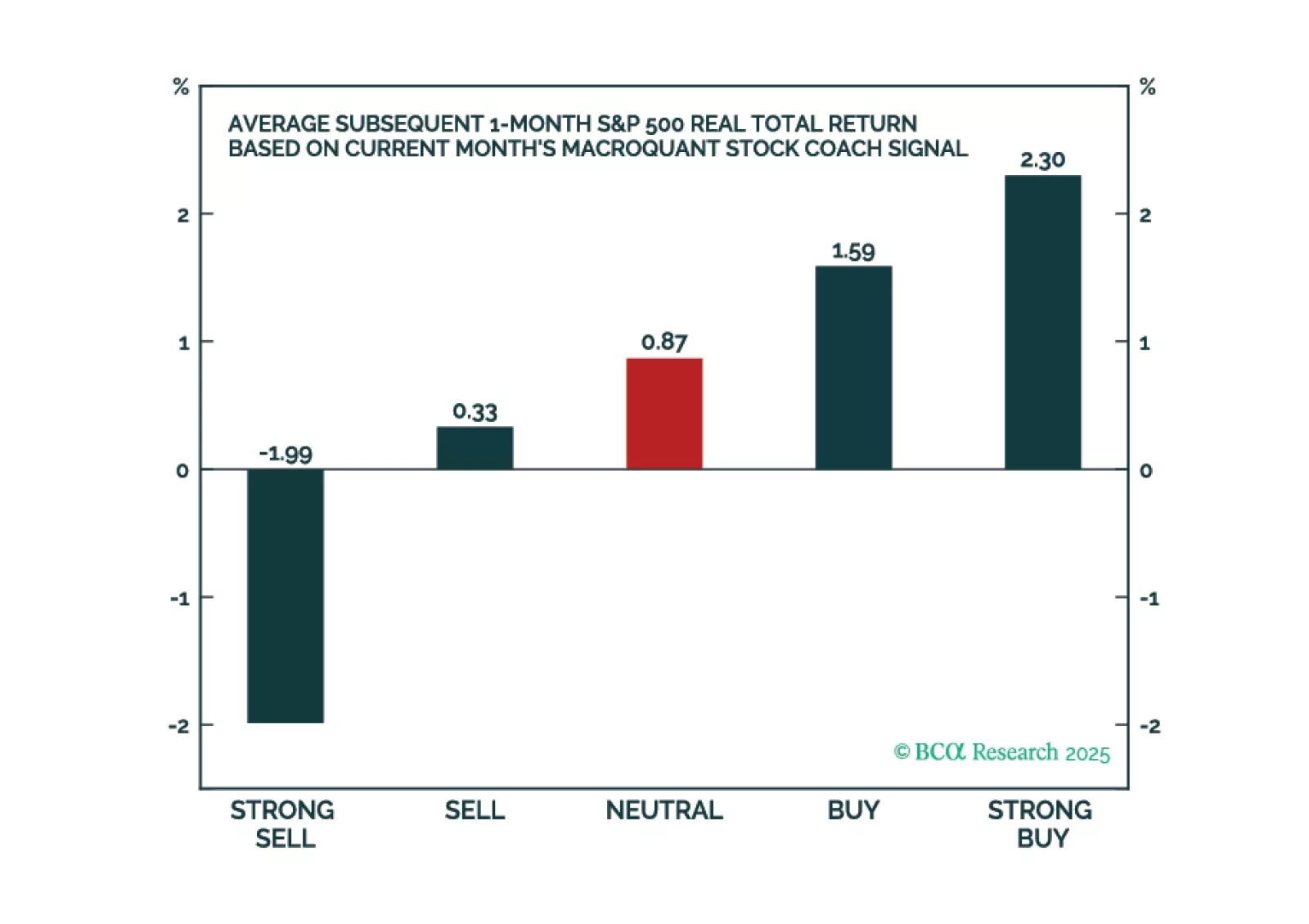

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.

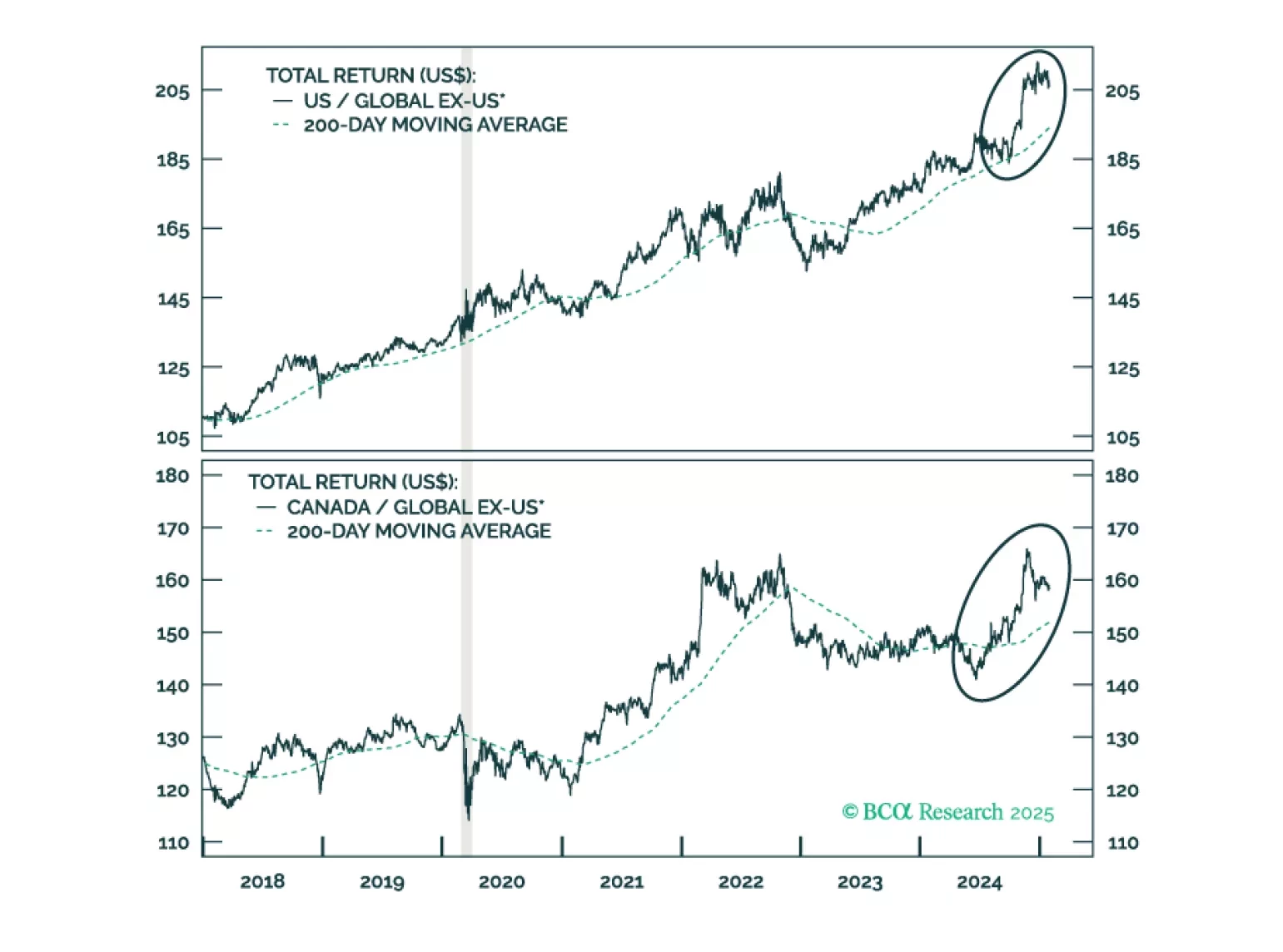

Jonathan provides an update on Canada following strong performance from Canadian stocks last year. On a tactical basis, underweight Canada versus global ex-US on the expectation of tariffs targeting Canada and Mexico. Following a sell off, or if a trade war is avoided, investors should place Canadian stocks on upgrade watch with the goal of moving to a modest overweight versus global ex-US.

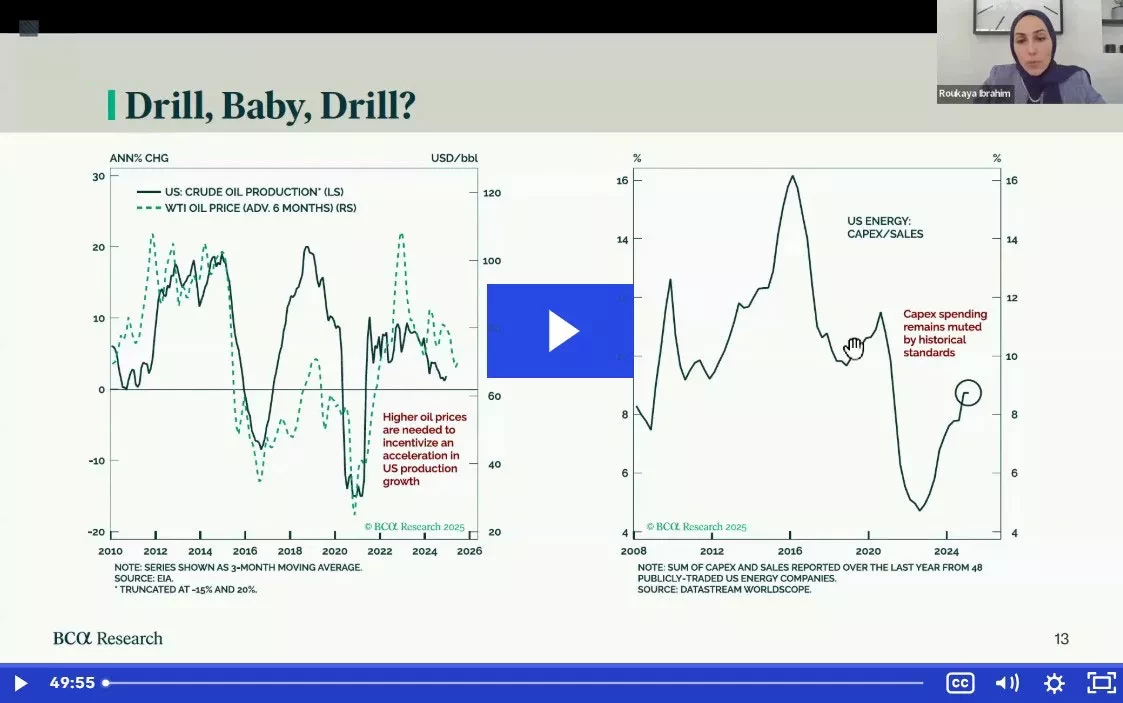

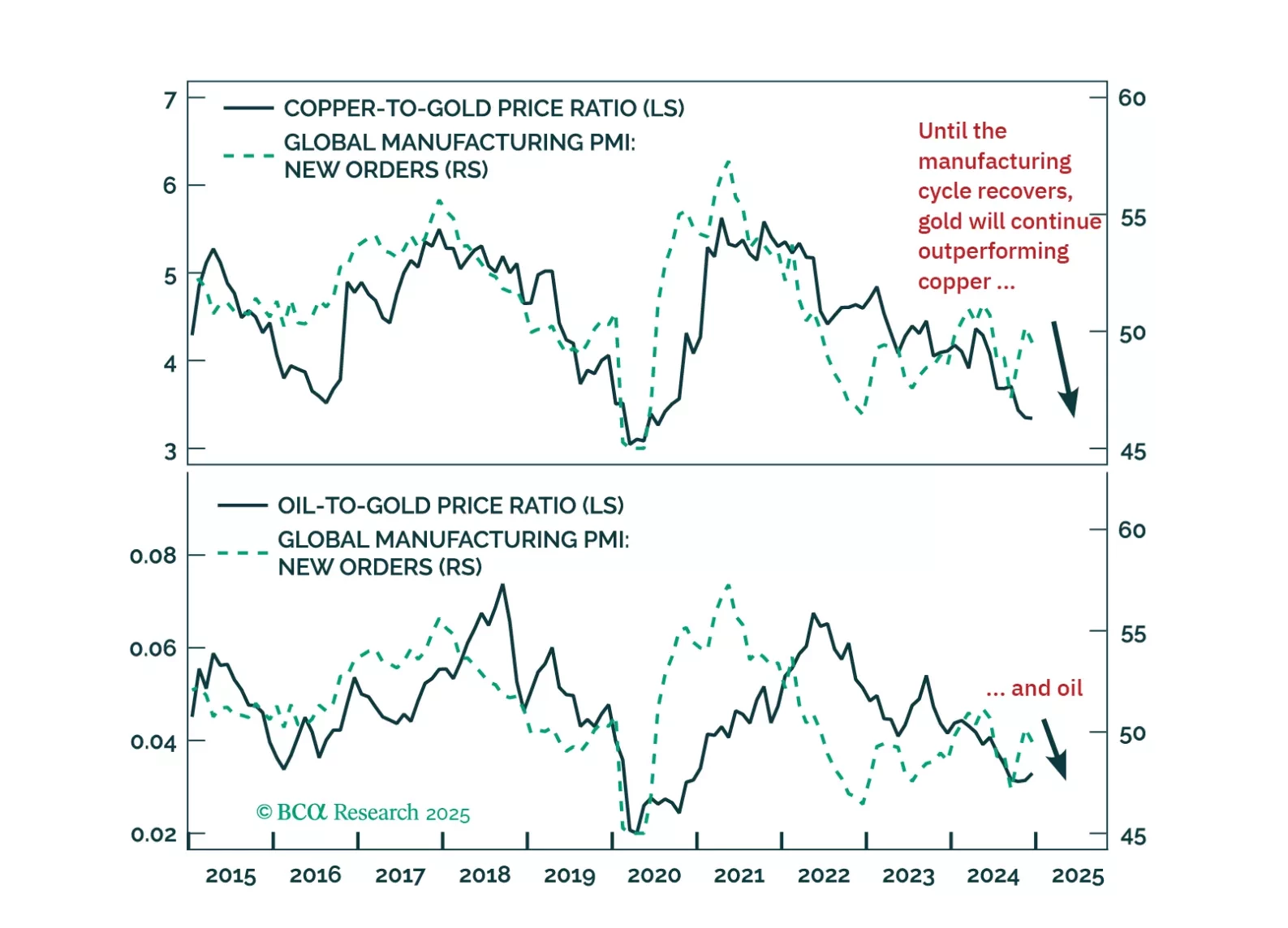

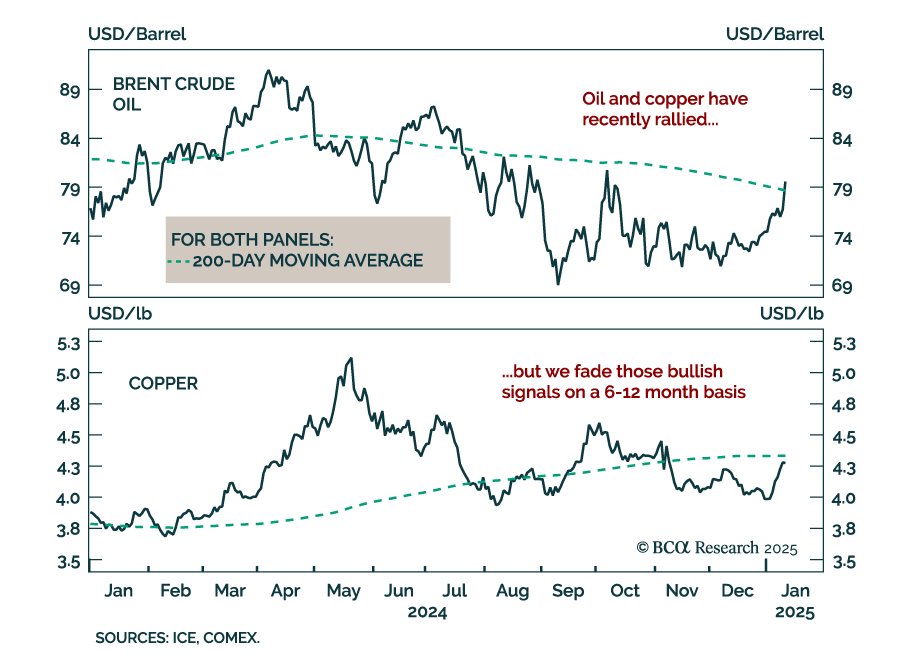

In this Special Report, we outline the three themes that we believe will drive commodity markets this year: (1) demand growth will remain sluggish across cyclical commodities (2) supply-side developments will ultimately be bearish for oil prices, and (3) traditional relationships between commodity prices and financial variables may not hold.

The outgoing Biden administration has launched a slew of macro-relevant executive orders and regulatory actions. The one with immediate macro implications are the sanctions against Russian oil traders and its “dark fleet” of oil tankers.

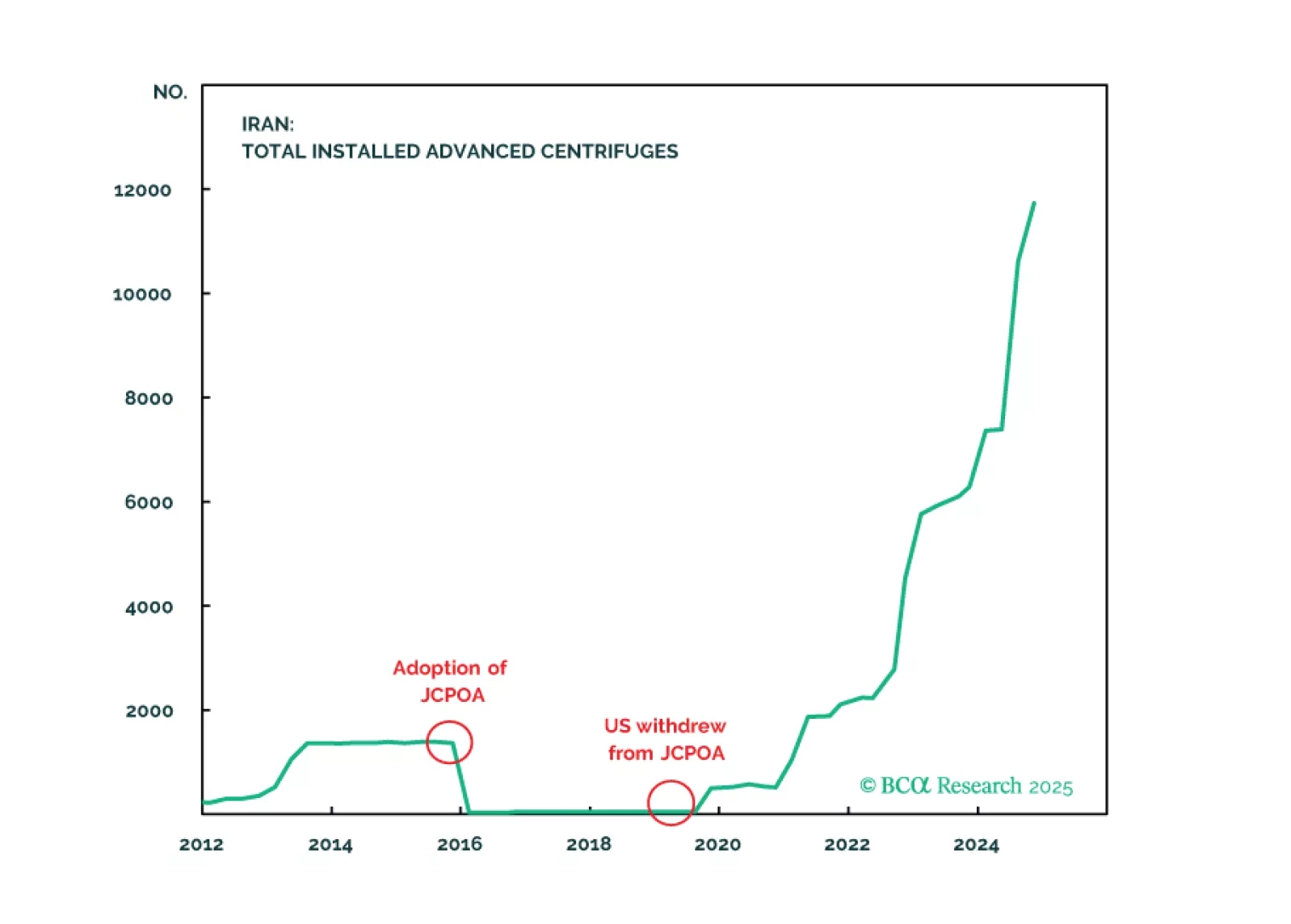

Every year we highlight five low-odds scenarios that would have a major impact on global financial markets if they happened. This year we contemplate a total reversal of Chinese policy, a US-Iran nuclear deal, a breakdown of NATO, US military action across the Americas, and an internationally coordinated FX intervention.