Monetary Policy

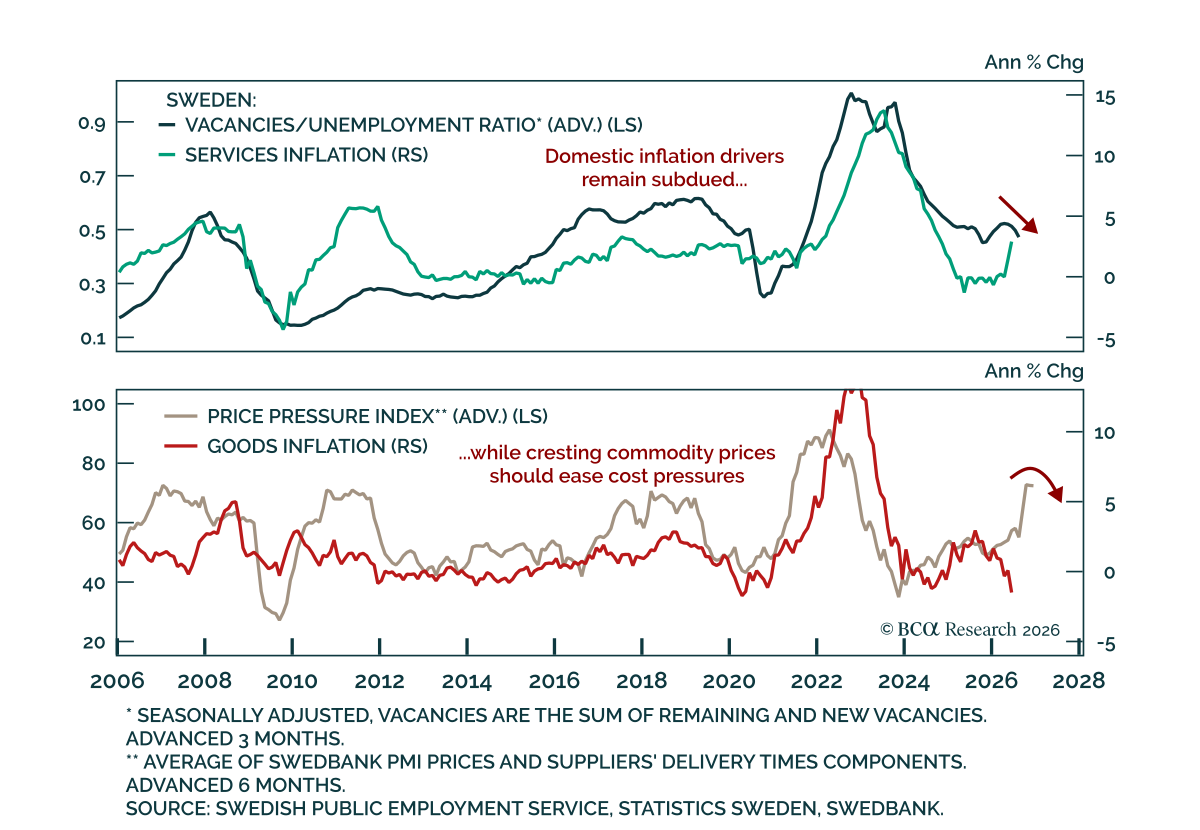

Subdued Swedish inflation should keep the Riksbank on hold. June headline CPIF eased to 1.3% y/y (0.3% m/m) from 1.5% (0.9%), and CPIF excluding energy slowed to 0.4% y/y (0.6% m/m) from 0.5% (0.7%). Both were marginally above estimates, but disinflation has…

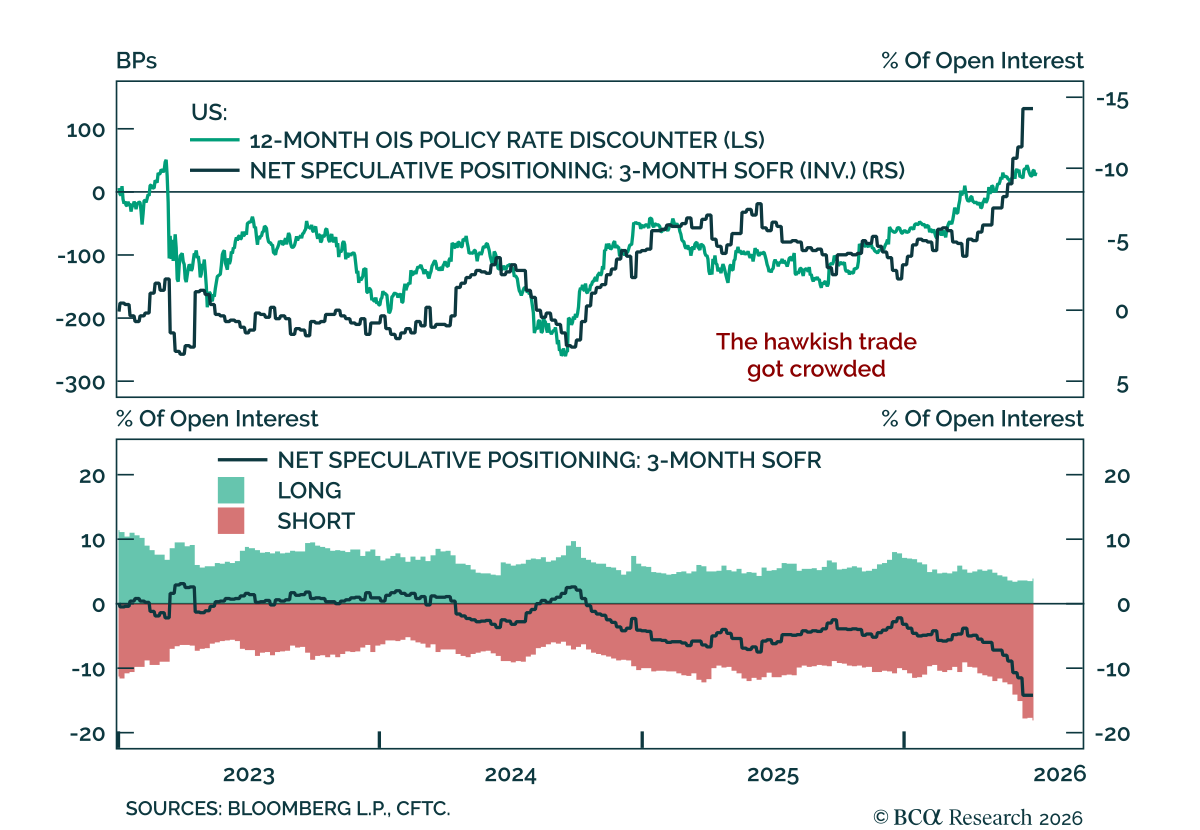

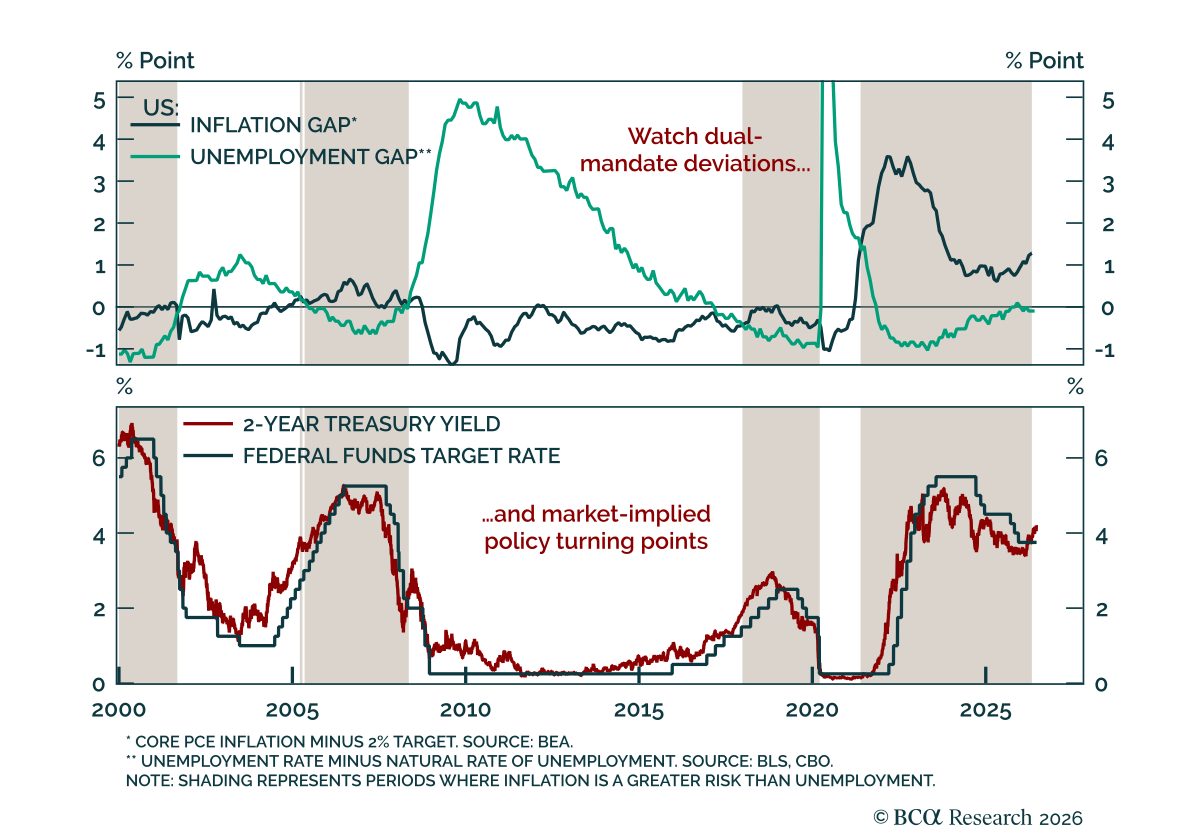

Peak hawkishness is likely behind us, supporting carry trades and risk assets. Despite a hawkish June Fed meeting, Treasury yields have now roughly returned to where they were before Chairman Warsh’s first meeting. The 2-year has tested and rejected new…

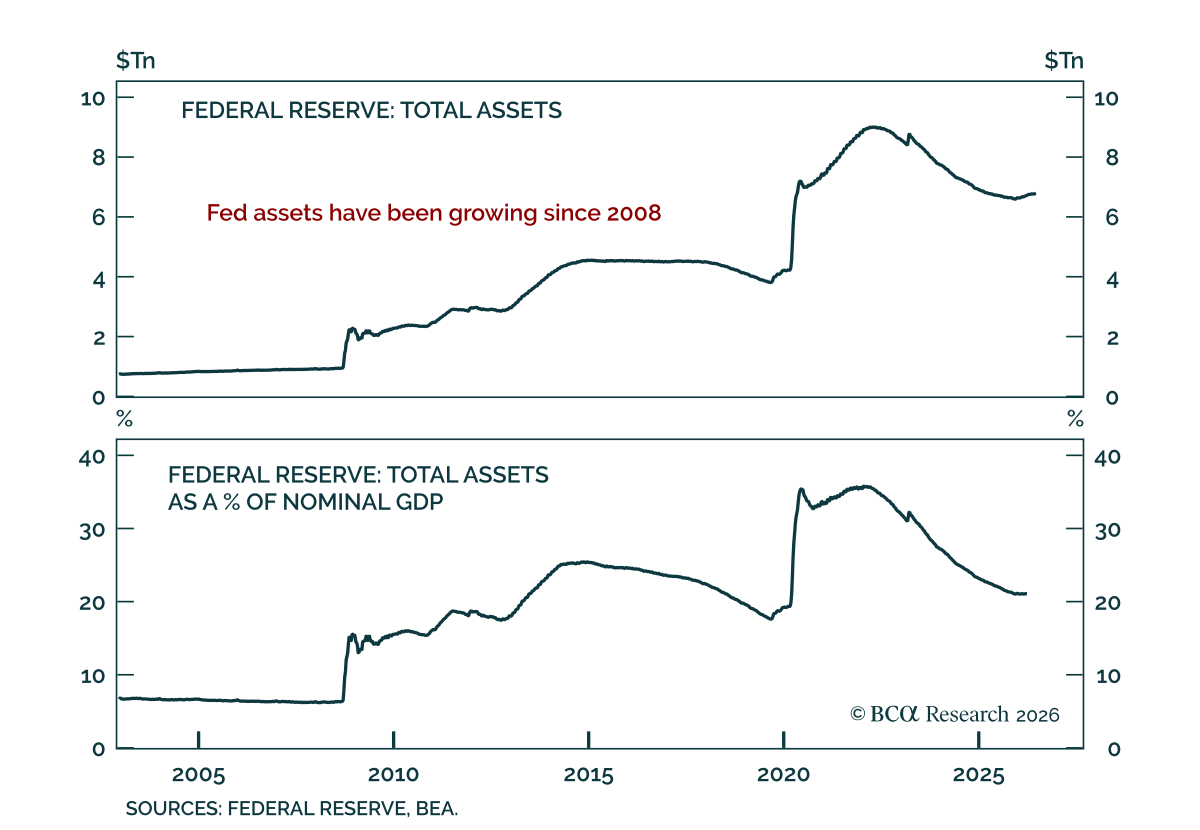

Our US Bond strategists expect the Fed to begin shrinking its balance sheet in 2027, but assets will remain well above pre-2008 levels even once that program concludes. Chairman Warsh has launched a task force to review balance sheet policy, and given his…

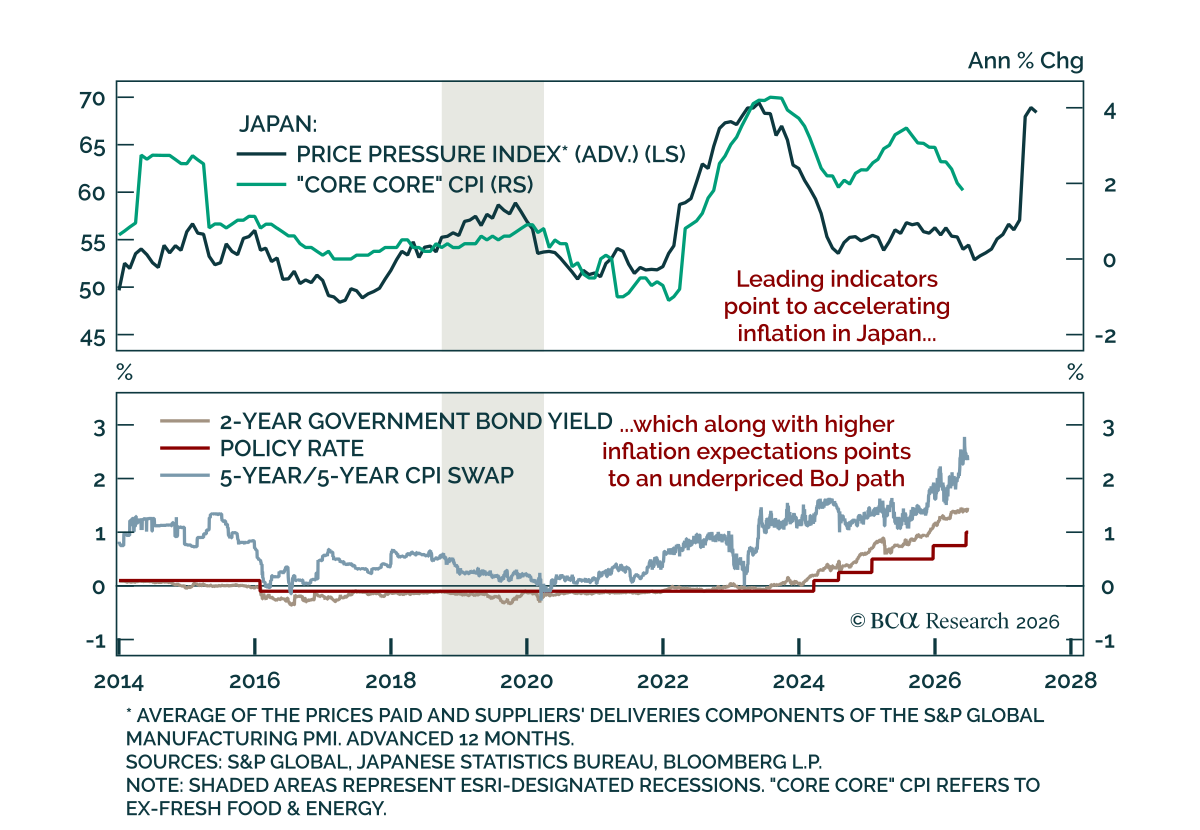

The June Tokyo CPI came in hotter than consensus, pointing to rising price pressures and further policy tightening. The headline index rose to 1.7% y/y from 1.4%. Core measures were also hot, with CPI ex-fresh food rising to 1.6% from 1.3%, and “core core”…

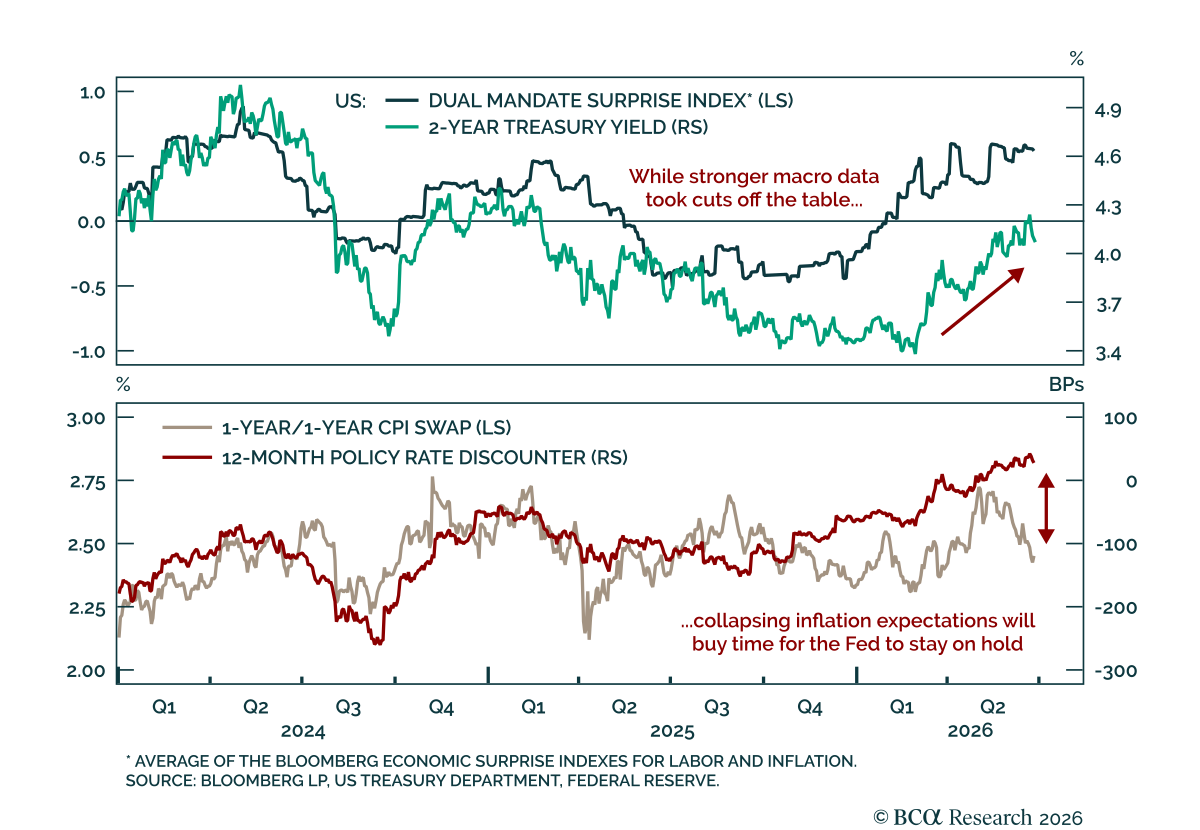

Mixed labor and inflation data should create a window for the Warsh Fed to keep rates on hold. We recently highlighted an important nuance to the communication changes so far: explicit guidance is removed, yet implicit guidance remains. The Warsh Fed will…

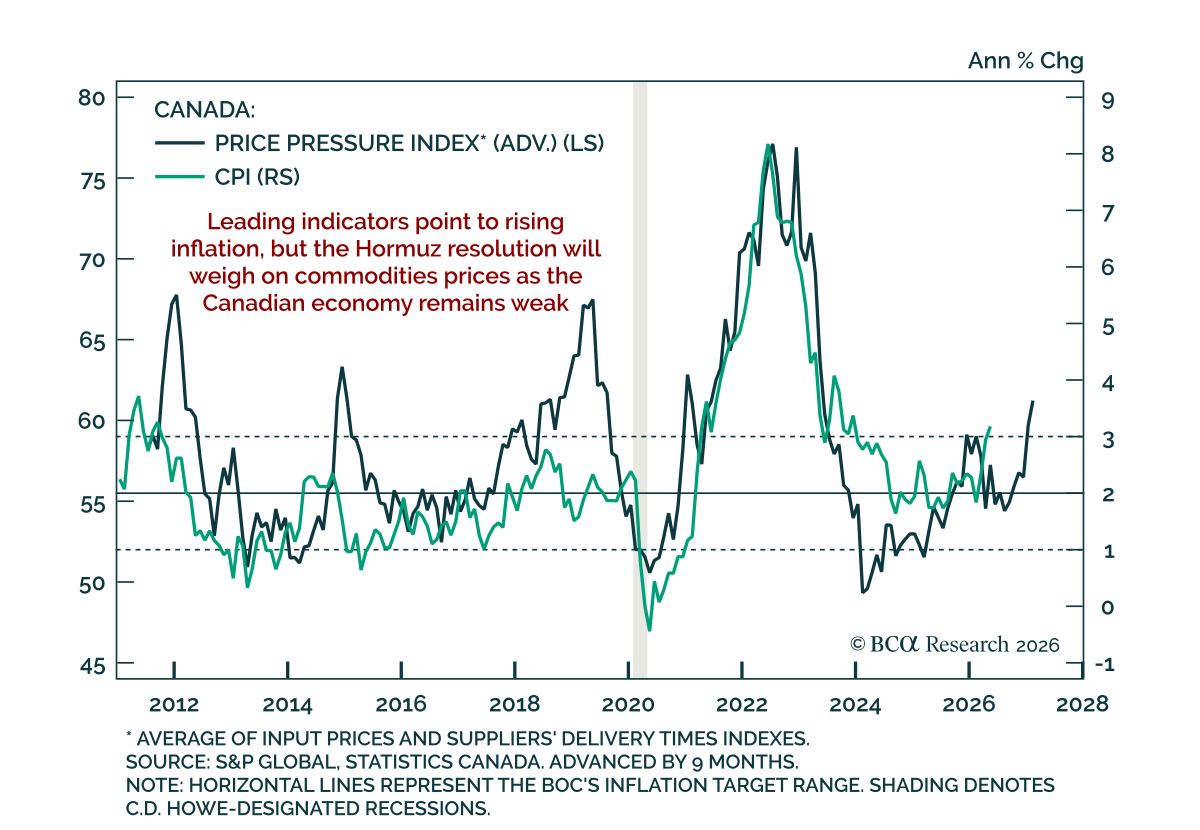

Canadian May inflation was hotter than estimates, but the underlying inflation picture remains much more muted. Headline CPI rose to 3.2% from 2.8%, moving above the Bank of Canada’s 1%-to-3% target range. The increase, however, was driven by energy, which…

New Fed Chair Kevin Warsh wants to make Fed-watching great again. The Warsh Fed will speak less and guide less. There is, however, an important nuance to the communication changes so far. While explicit guidance was removed, some implicit guidance remains, as…

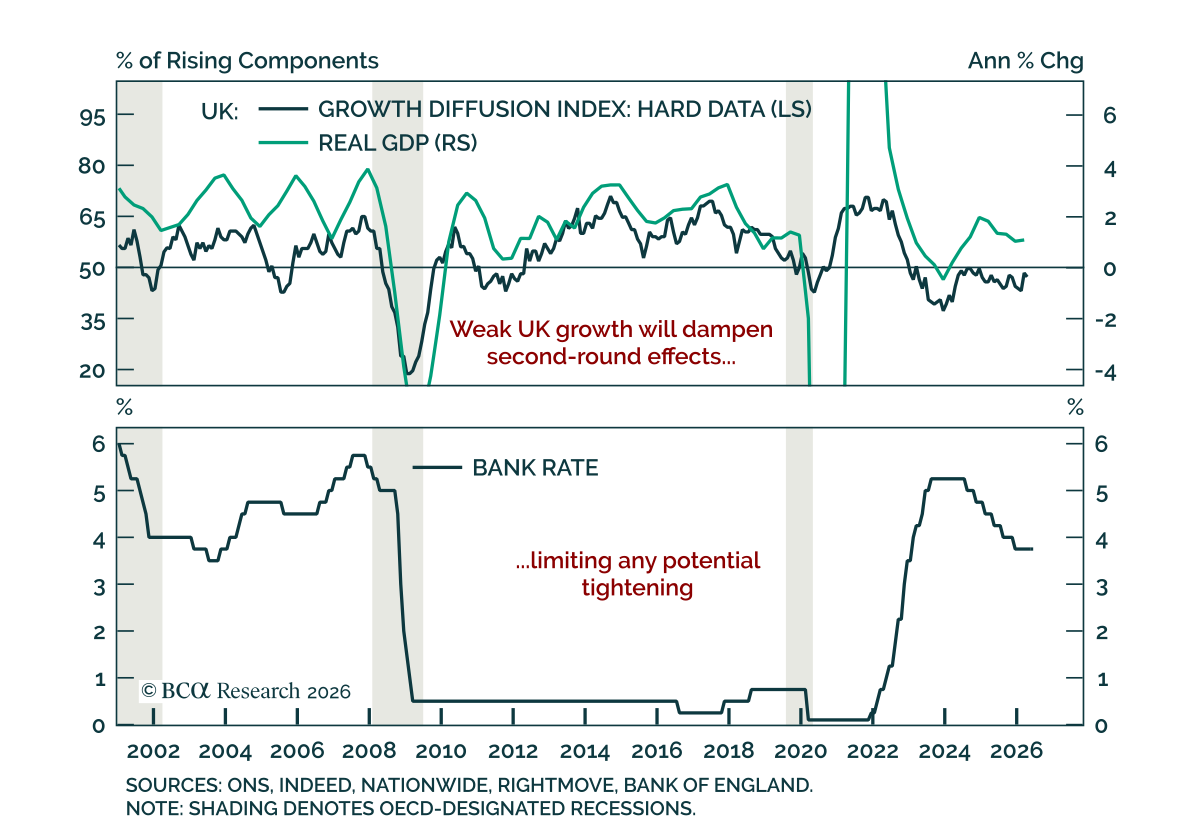

The Bank of England held rates at 3.75%, as expected; we remain overweight UK gilts on a 12-month horizon. The hold was a 7-2 decision, with the two dissenters favoring a hike. Those MPC members were concerned about second-round effects and pointed to…

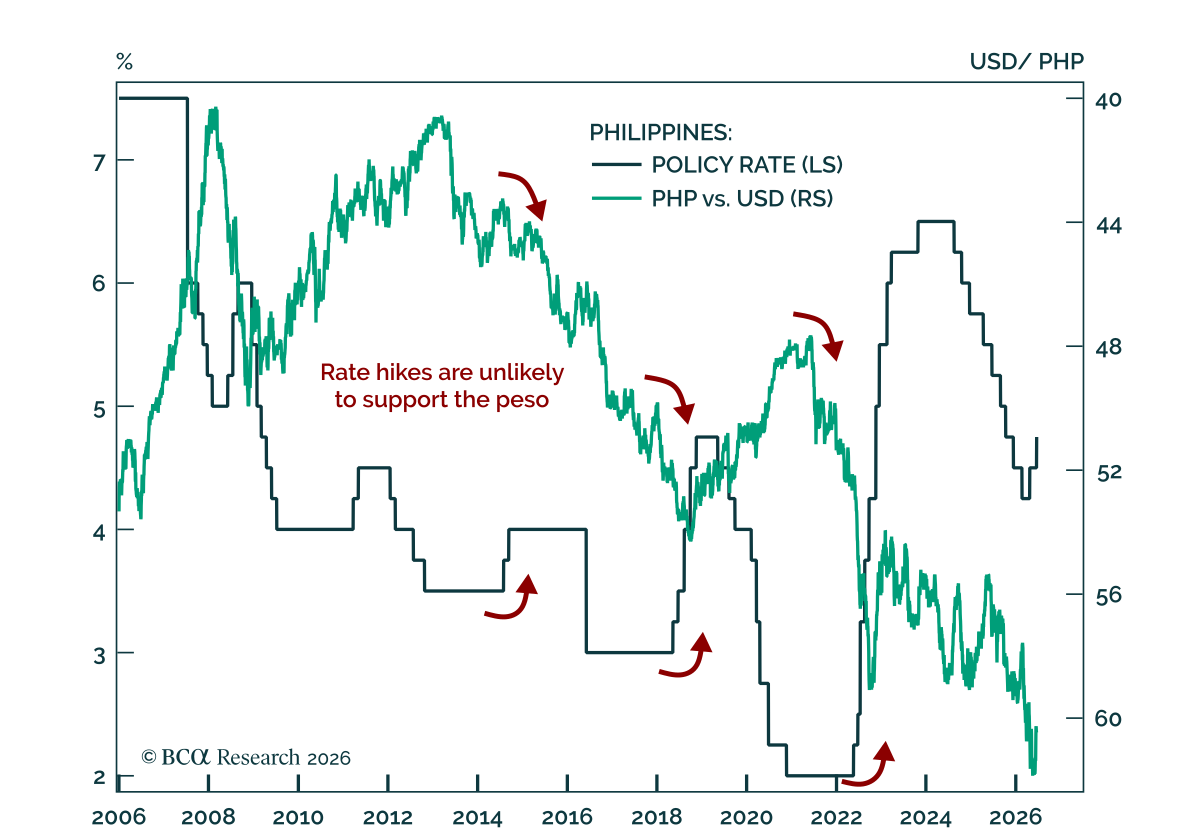

The Philippines’ central bank raised rates to 4.75%, but higher policy rates are unlikely to provide much support to the peso or local assets. The central bank hiked by 25 bps, citing rising energy and food inflation. With headline CPI already well above…

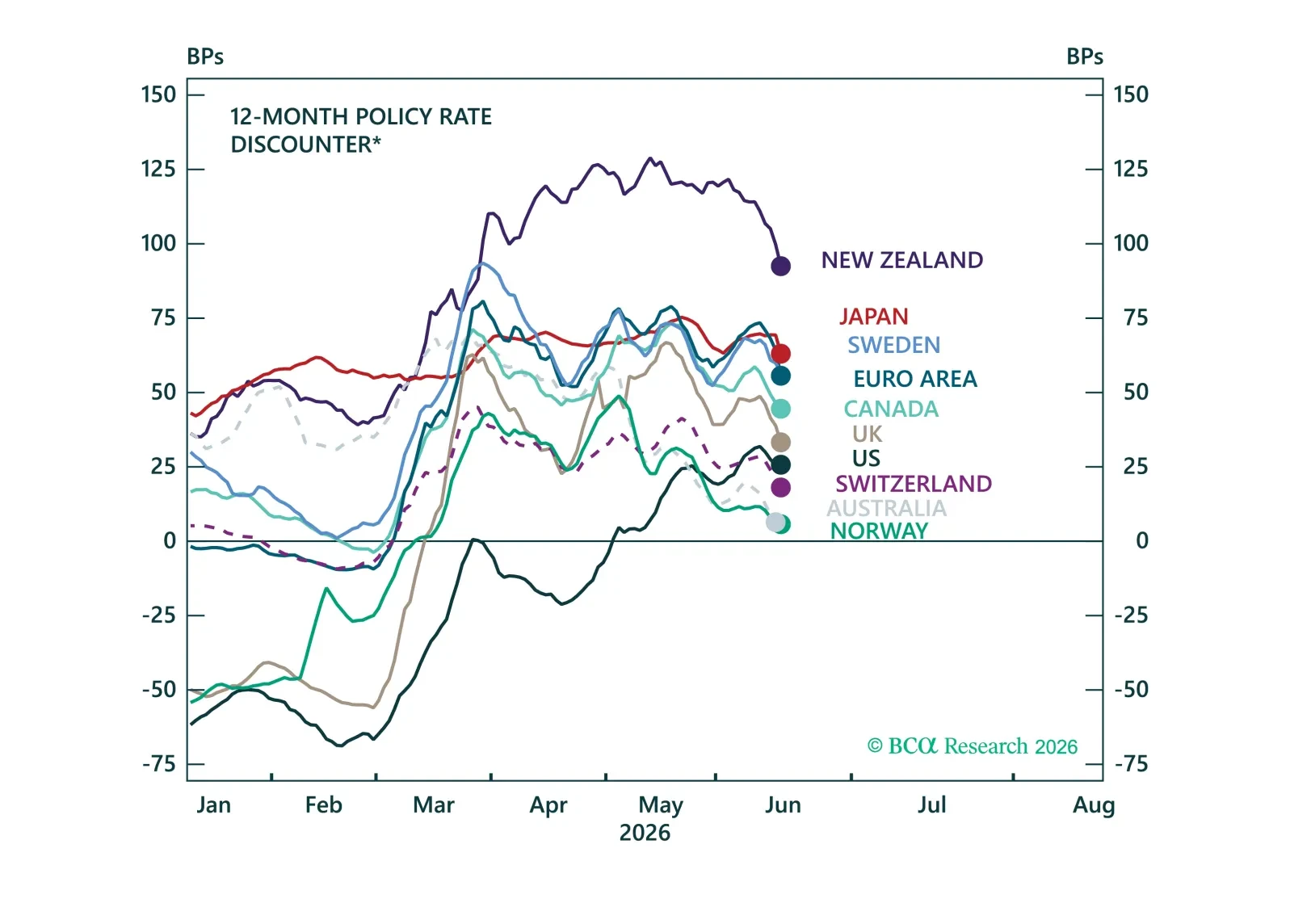

We react to DM central bank meetings this week and highlight the opportunities emerging across global fixed income and currency markets.