Labor Market

Various indicators of Eurozone wage growth have cooled off in recent months. Notably, the labor costs index eased sharply from a downwardly revised 5.2% y/y to 3.4% y/y in 2023Q4 – the slowest pace of increase since Q3 2022. Alternative measures such as…

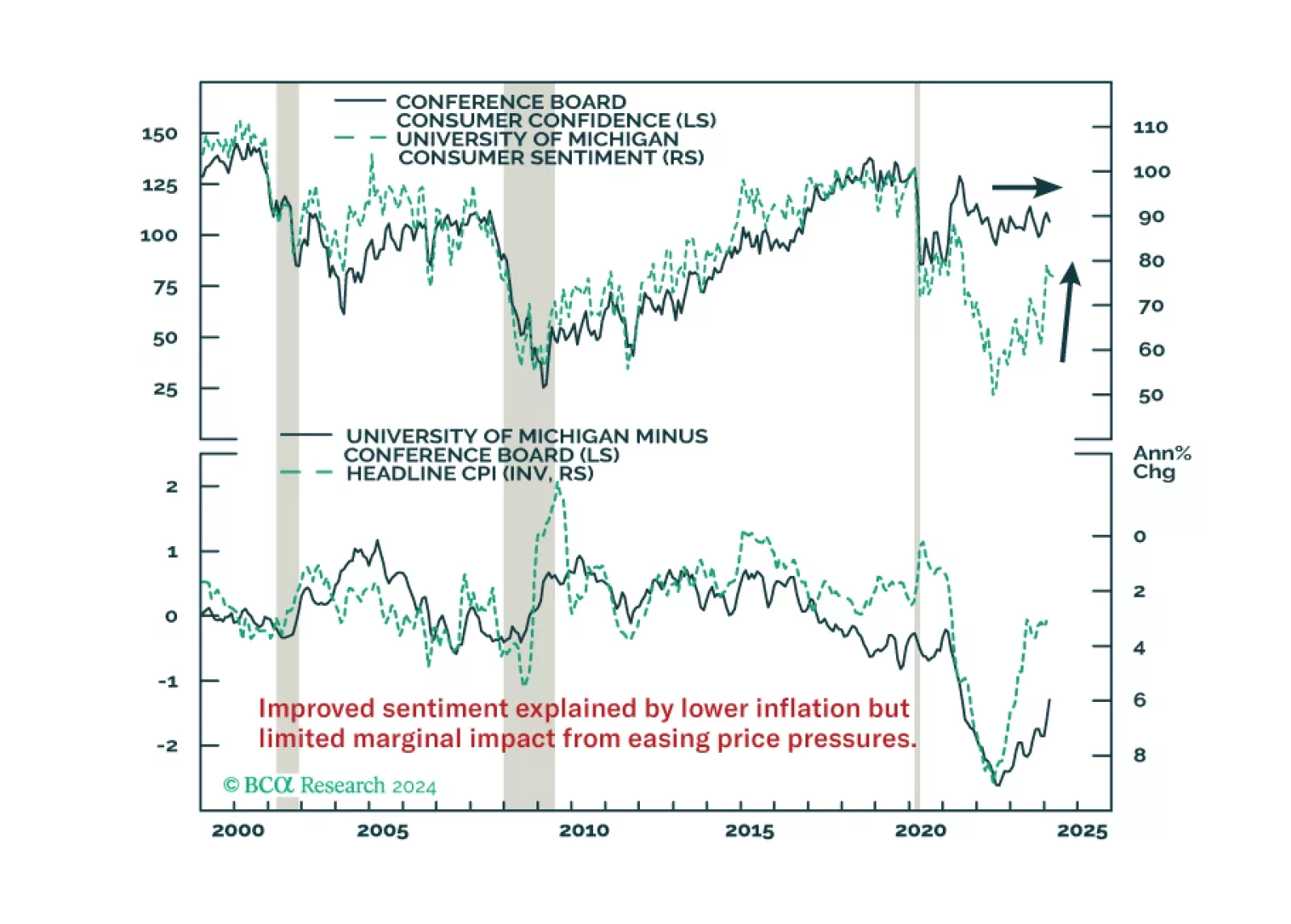

Improved consumer morale will not compensate for the fading tailwinds to consumption. Neither will the wealth effects from higher stocks and home prices.

There is a general consensus among BCA Research strategists that a US recession is highly likely over the next two years. While last month our Global Investment strategists reduced the probability that a recession will materialize in H1 2024 and raised the…

According to BCA Research’s Counterpoint service, ‘bad unemployment’ is on the rise in the US, despite resilient growth. There are two ways that you can become unemployed. Either by losing your job. Or by entering the labour force to look for a job. The…

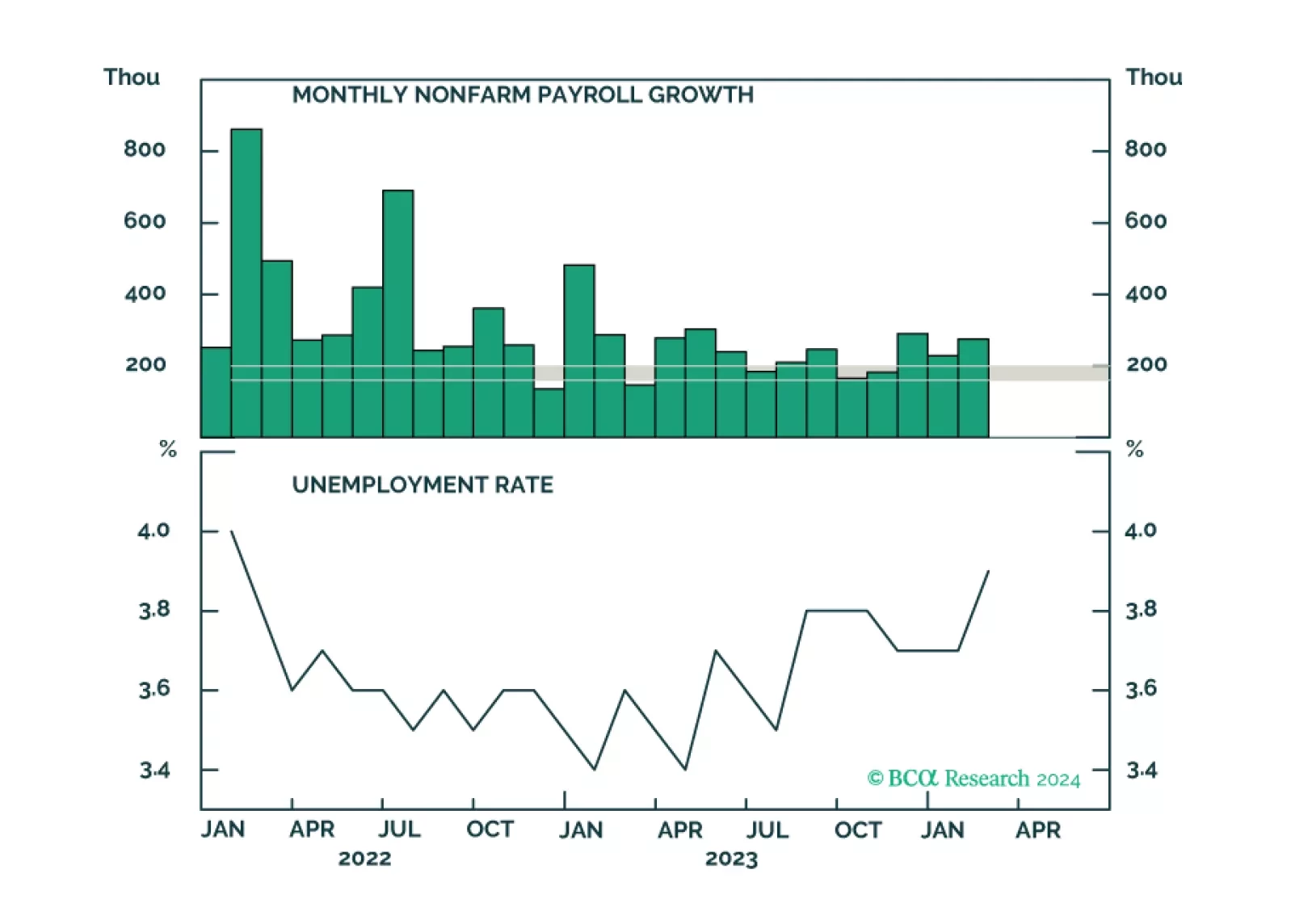

For the past year, relatively large downward revisions have been key features of the monthly US nonfarm payrolls reports. Friday’s release was no exception. Although it showed the magnitude of job gains beat expectations in February, estimates for December…

According to BCA Research’s European Investment Strategy service, last week’s ECB meeting confirmed their long-held view that the most likely date for the first ECB rate cut would be June. The ECB continues to acknowledge that the European economy is soft…

The US employment situation report sent a mixed signal on Friday. While total nonfarm payrolls rose by 275 thousand jobs in February, exceeding the 200 thousand expected, the previous two months’ numbers were revised lower by 167 thousand jobs (see Indicator…

Japanese equities and government bonds sold off on Monday and the yen strengthened following the release of the revised Q4 GDP report showing the economy expanded by an annualized 0.4% q/q in Q4 2023 versus earlier estimates of a 0.4% contraction. A…

According to Factset, analysts are forecasting S&P 500 earnings and revenues to grow by 11.0% y/y and 5.0% y/y respectively in 2024 (an acceleration from 0.9% and 2.8% in 2023). Information technology and communications services (broadly-defined tech) are…

We update the indicators in our duration checklist following this morning’s employment report.