Inflation/Deflation

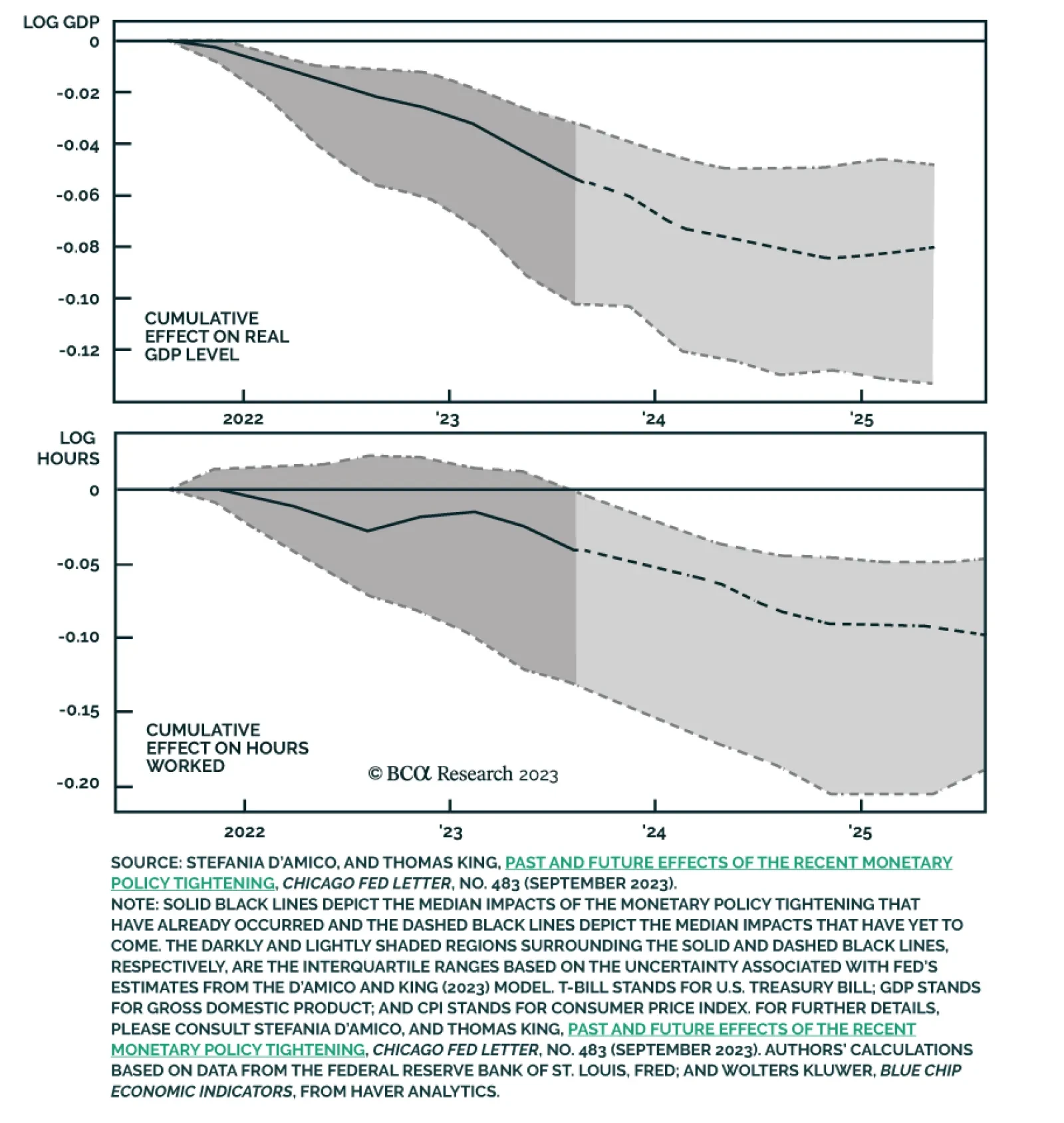

According to BCA Research's Global Investment Strategy service, the global economy will stay buoyant over the next few quarters but will then sour as the lagged effects of higher interest rates and tighter bank lending standards work their way through the…

BCA Research’s Global Fixed Income Strategy service is maintaining a tactical neutral duration stance to begin Q4. The team believes the risk/reward on US Treasuries has improved substantially after latest backup in yields, with the market now discounting…

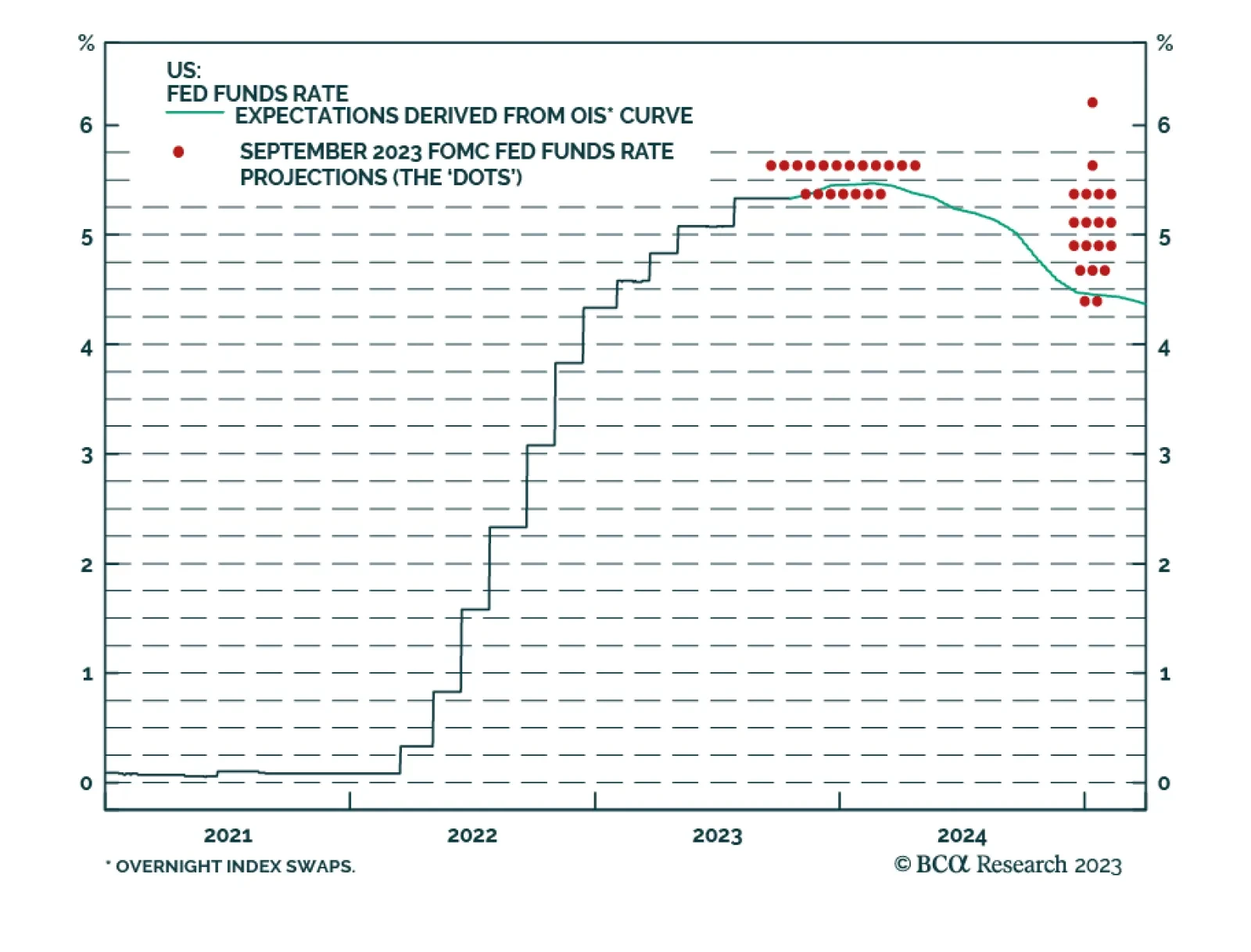

Fed Chair Jay Powell's speech at the Economic Club of New York on Thursday corroborates the signal from other recent Fedspeak that policymakers may not need to hike rates again. He highlighted that although inflation is still too high, price pressures are…

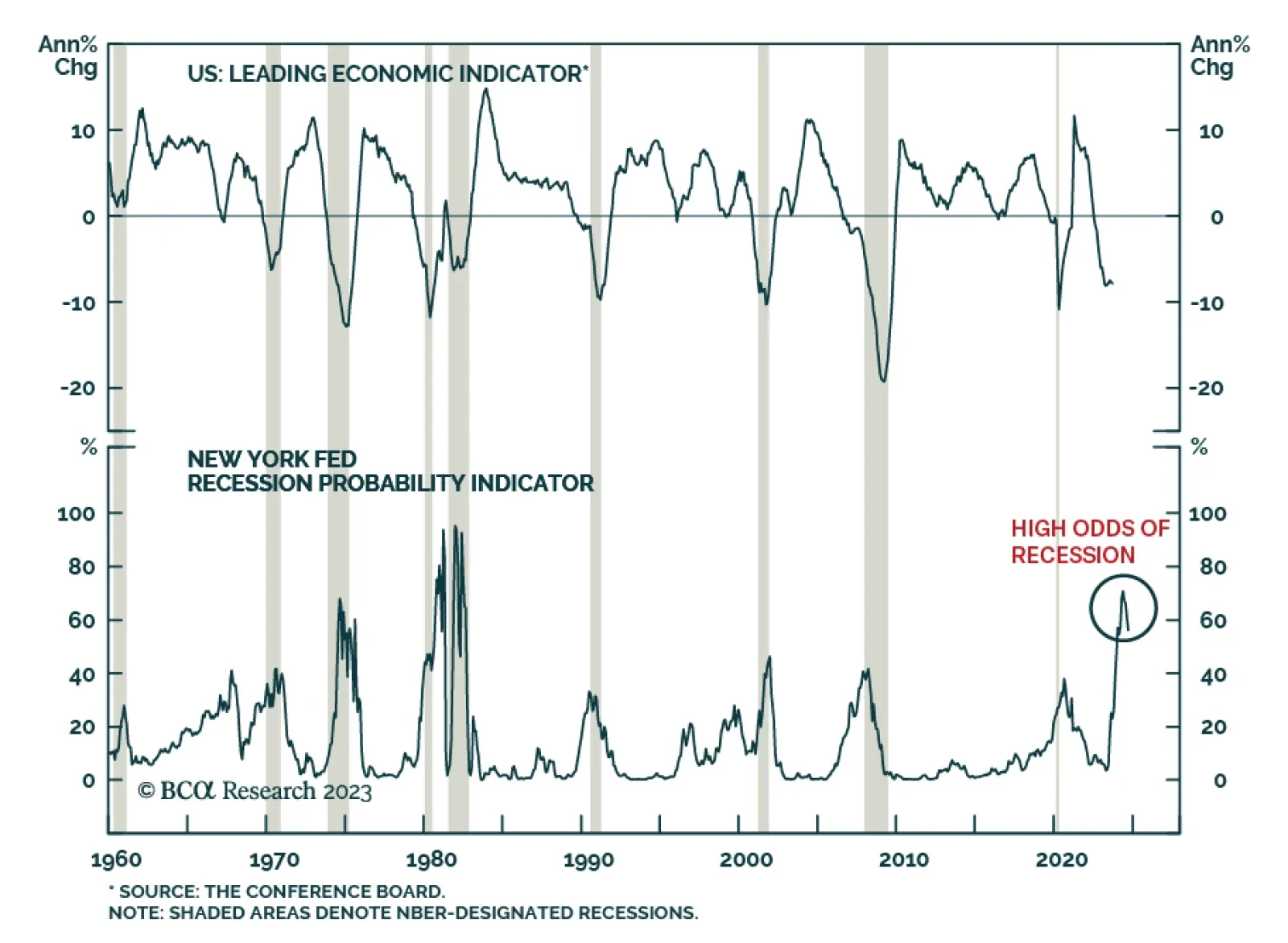

The Conference Board's Leading Economic Index's 0.7% m/m decline in September sent a weaker-than-anticipated signal about the outlook for the US economy. It fell below anticipations that the pace of decline would remain unchanged at -0.4% m/m and marks the…

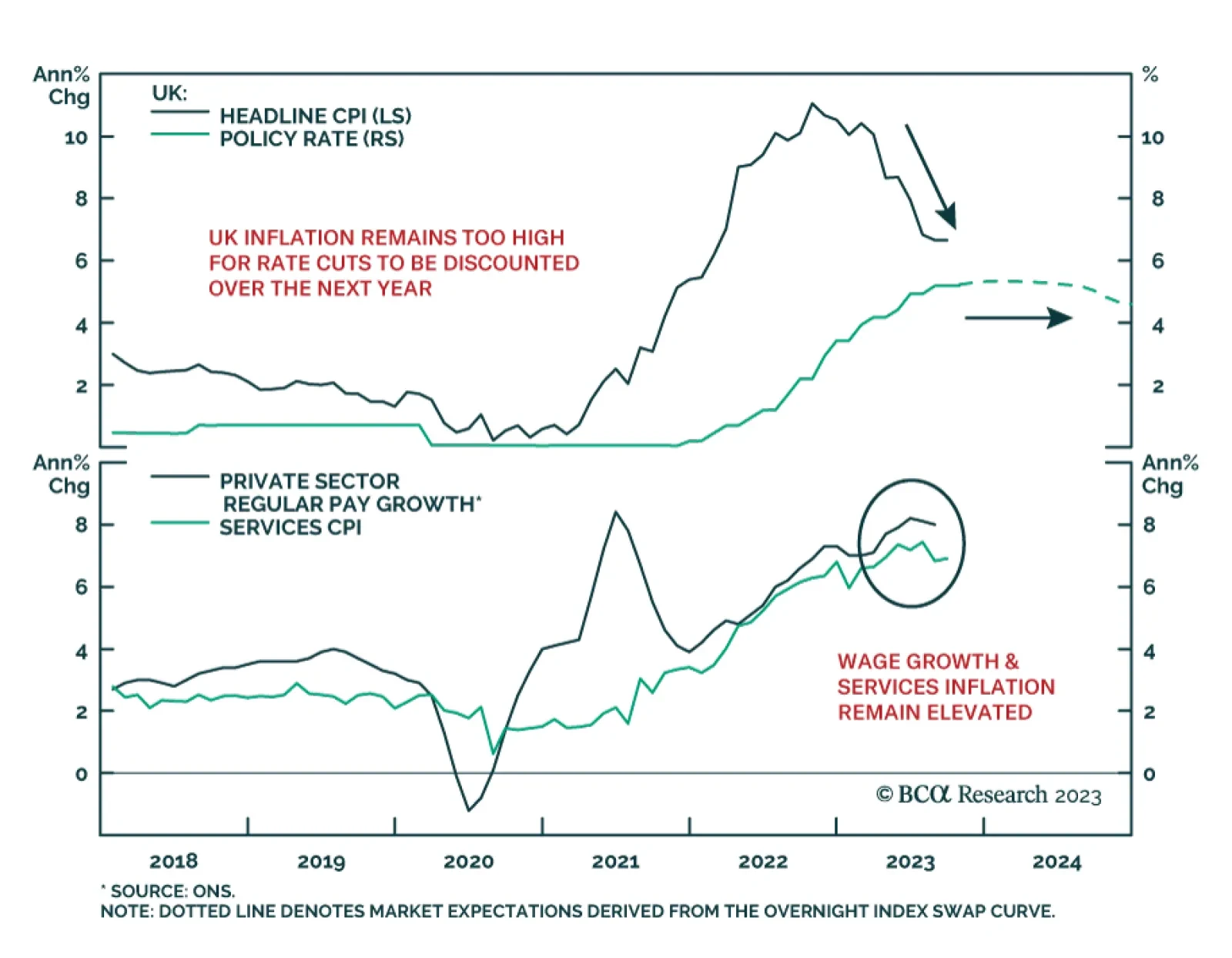

The data releases this week in the UK were disappointing for those that have been looking for a major downshift in UK inflation – most importantly, the Bank of England (BoE). The CPI report for September came in above expectations at 0.5% month-on-month…

According to BCA Research’s Counterpoint service, a fundamental question for investors is, will central banks fail to exorcise the pandemic’s lingering inflationary shock, just as they failed to exorcise the inflationary shock that came from the collapse of…

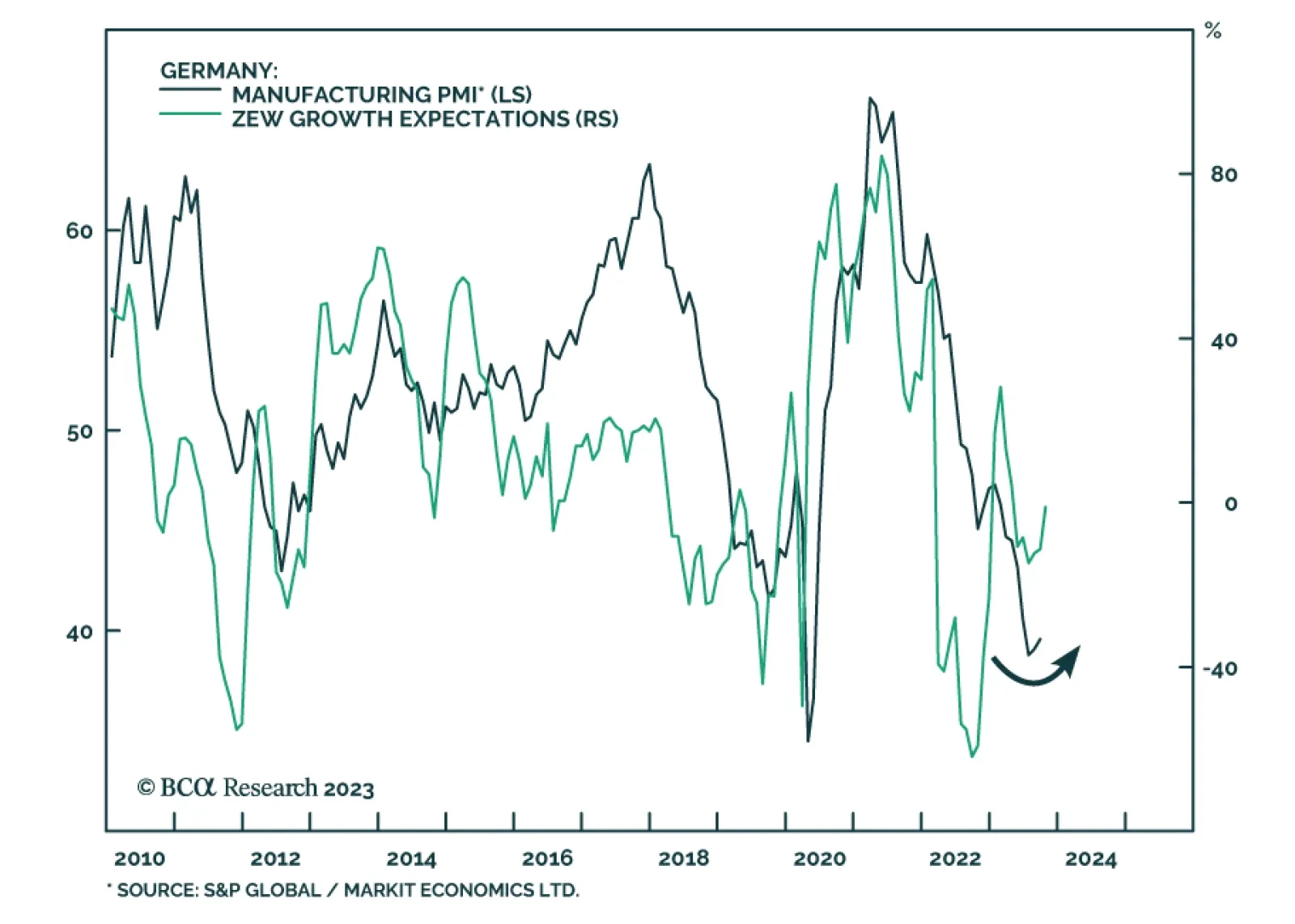

The ZEW survey of investor sentiment sent an optimistic signal on Tuesday. German sentiment rebounded sharply from -11.4 to -1.1 in October – its highest level since April. Lower inflation expectations and a sharp increase in the share of respondents…

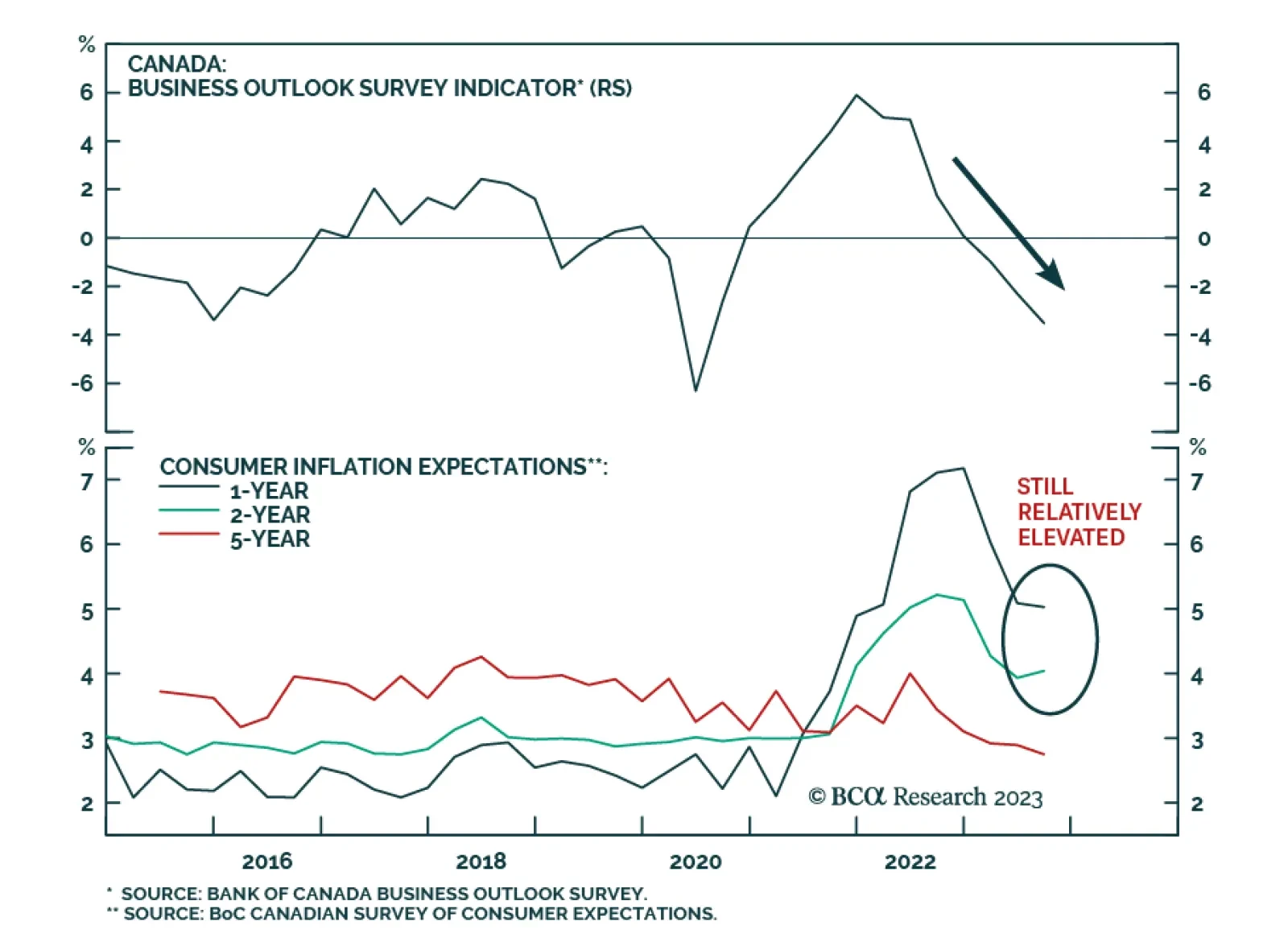

Results of the Banks of Canada’s Q3 business and consumer surveys reveal that the aggressive tightening cycle is dampening economic agents’ sentiment. Putting aside the sharp decline at the onset of the pandemic in Q2 2020, the Business Outlook Survey (BOS)…

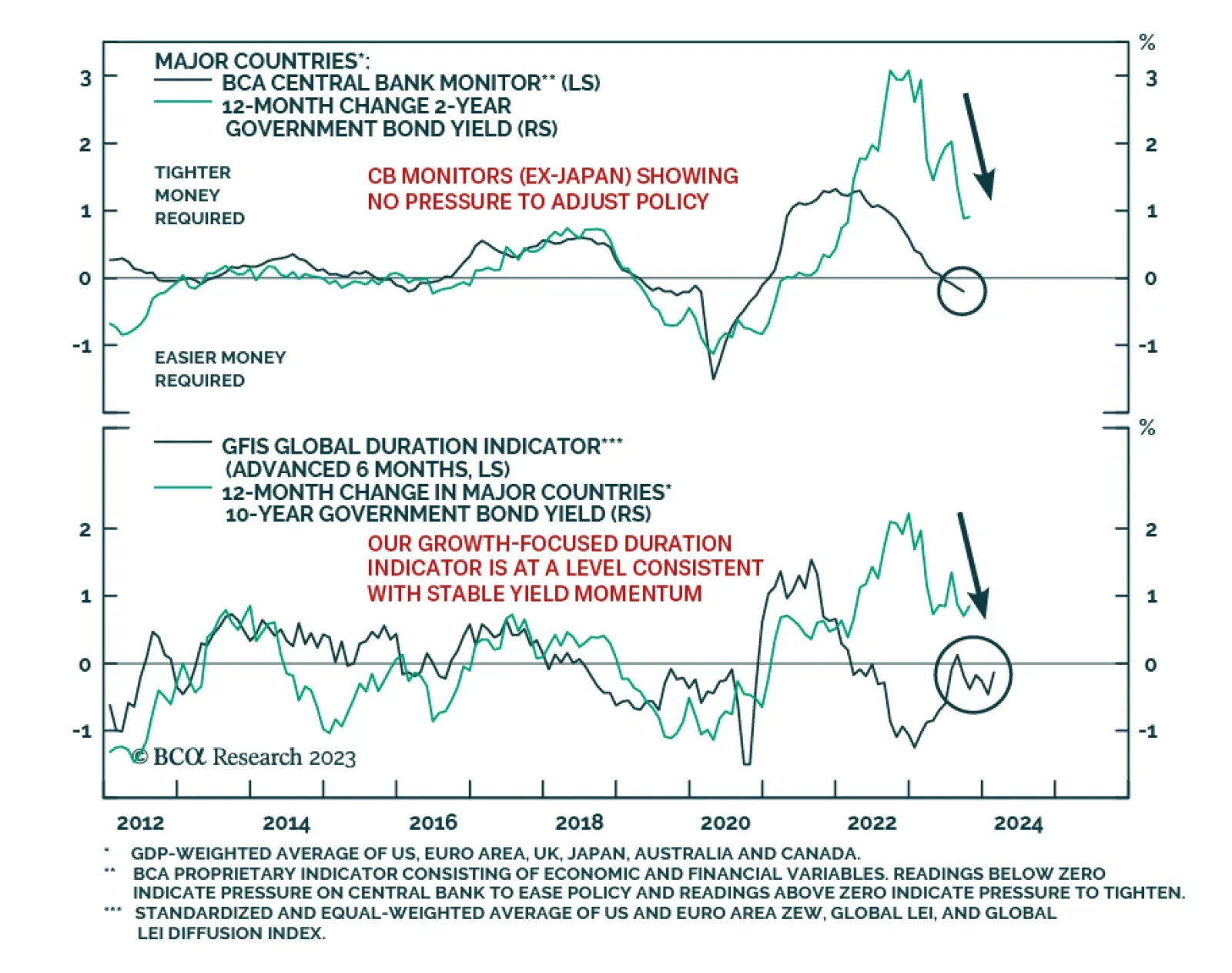

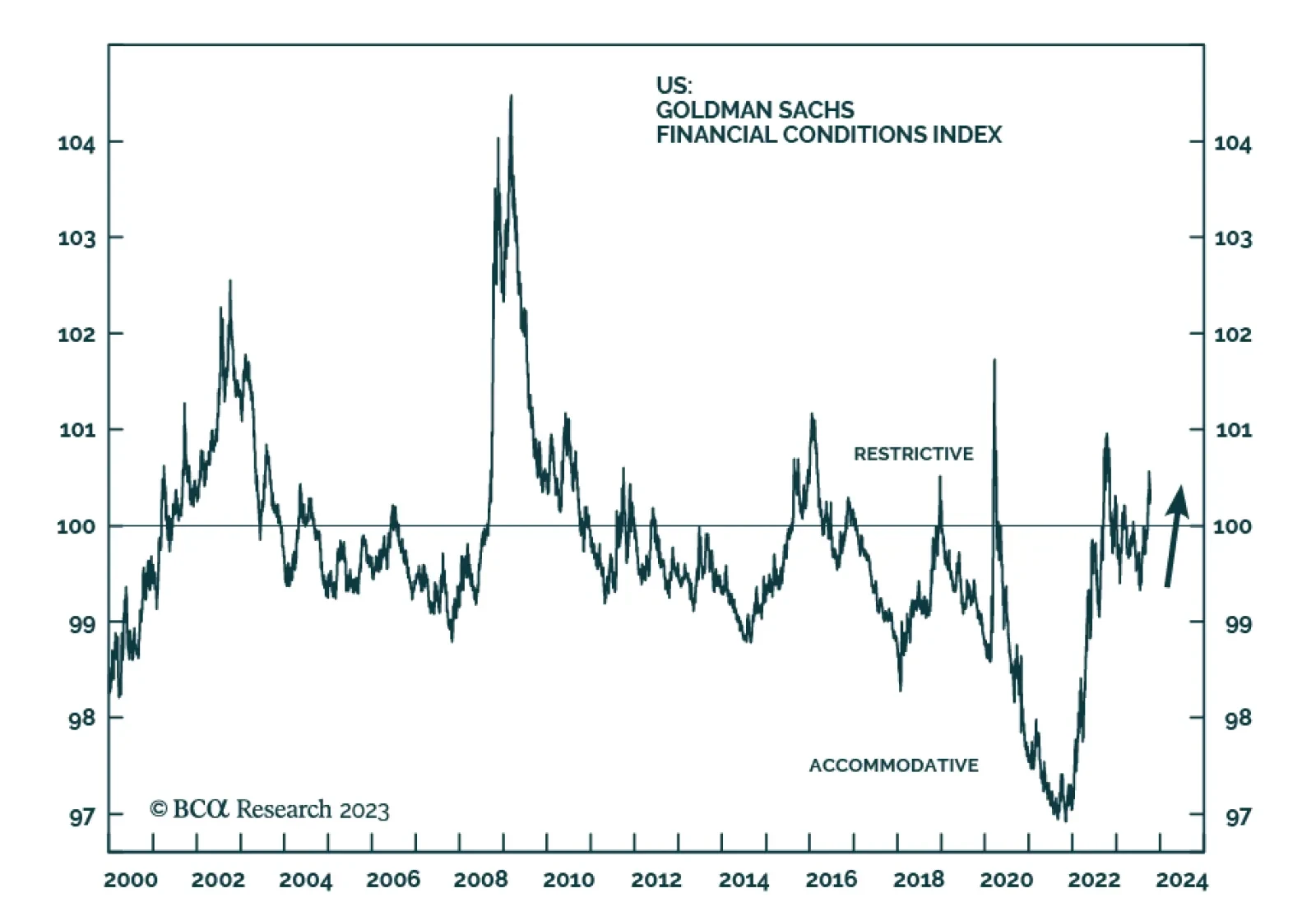

US financial conditions have tightened meaningfully in Q3. While the Goldman Sachs index remains below where it was a year ago, it crossed above the 100 line in late September into restrictive levels after spending most of the year in accommodative territory.…

More equity volatility is coming in the short run. Trump’s nomination looks to be smooth, which marginally reduces the incumbent party advantage and increases policy uncertainty.