Inflation/Deflation

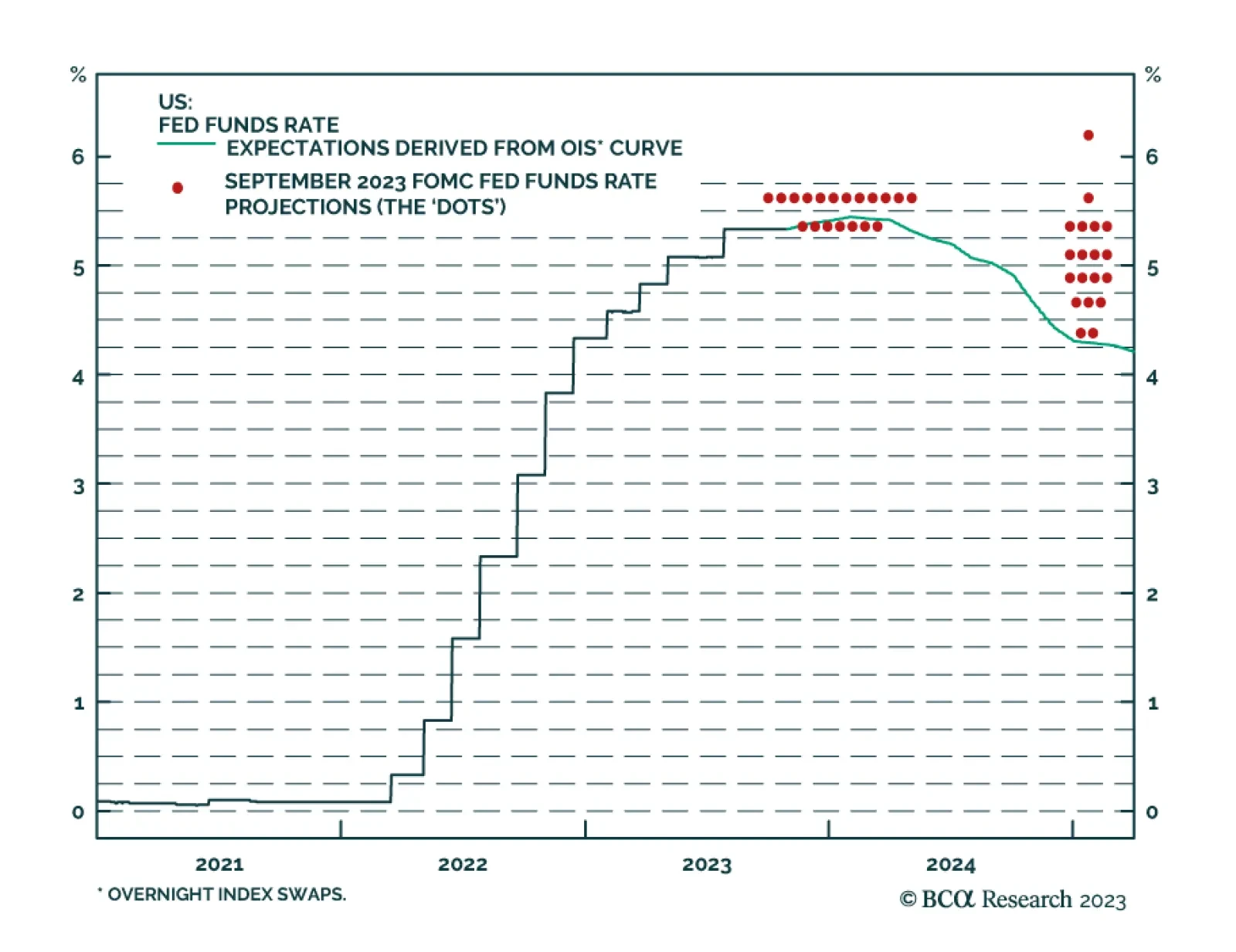

As expected, the Fed stood pat at its Wednesday meeting, maintaining the target for the fed funds rate at 5.25-5.50%. The minimal changes made to the Fed Statement were to emphasize the strong pace of economic activity in Q3, to characterize job gains as…

Our reaction to today’s FOMC meeting and the Treasury’s Quarterly Refunding Announcement.

High interest rates will eventually cause growth to slow. Signs of stress are already starting to show. Stay cautiously positioned.

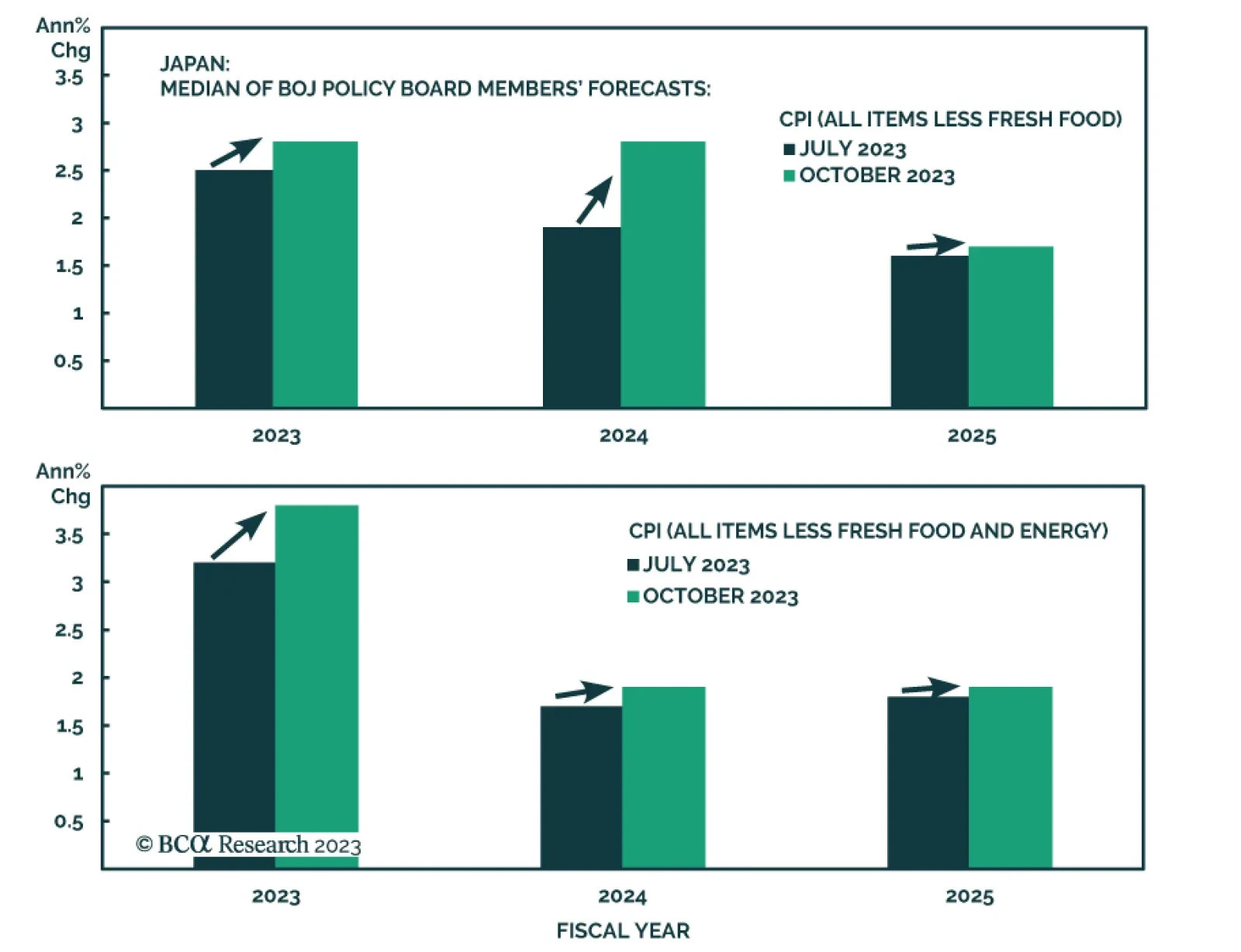

The Bank of Japan adjusted the language of its Monetary Policy Statement on Tuesday to indicate that it will allow greater flexibility it its yield curve control policy (YCC). It indicated that although the target level of 10-year JGB yields remains unchanged…

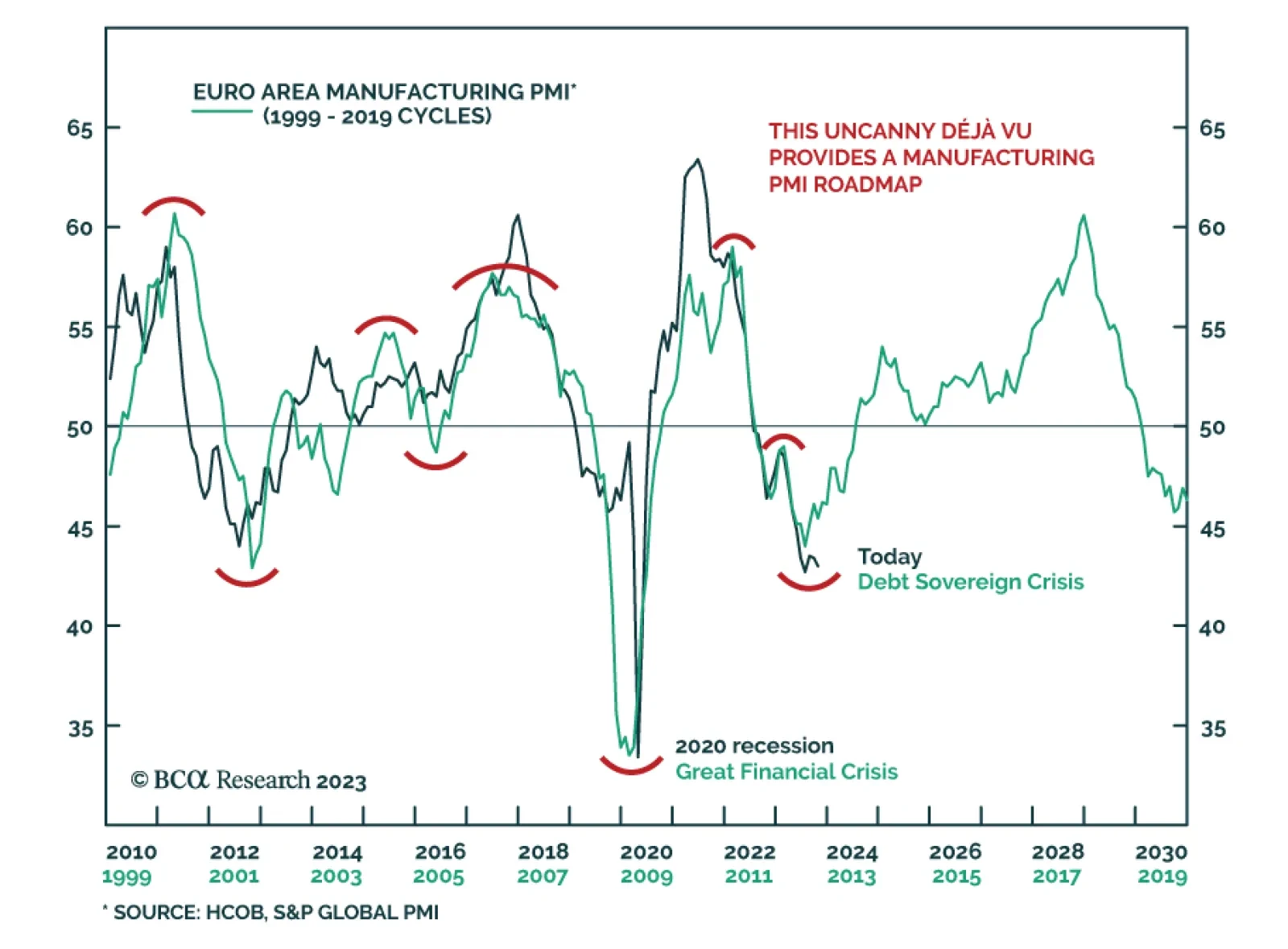

According to BCA Research’s European Investment Strategy service, 2012 provides a tentative roadmap of the next Eurozone manufacturing cycle. The resemblance between today and 2012 is uncanny. The overlap matches the current cycle down to a couple of…

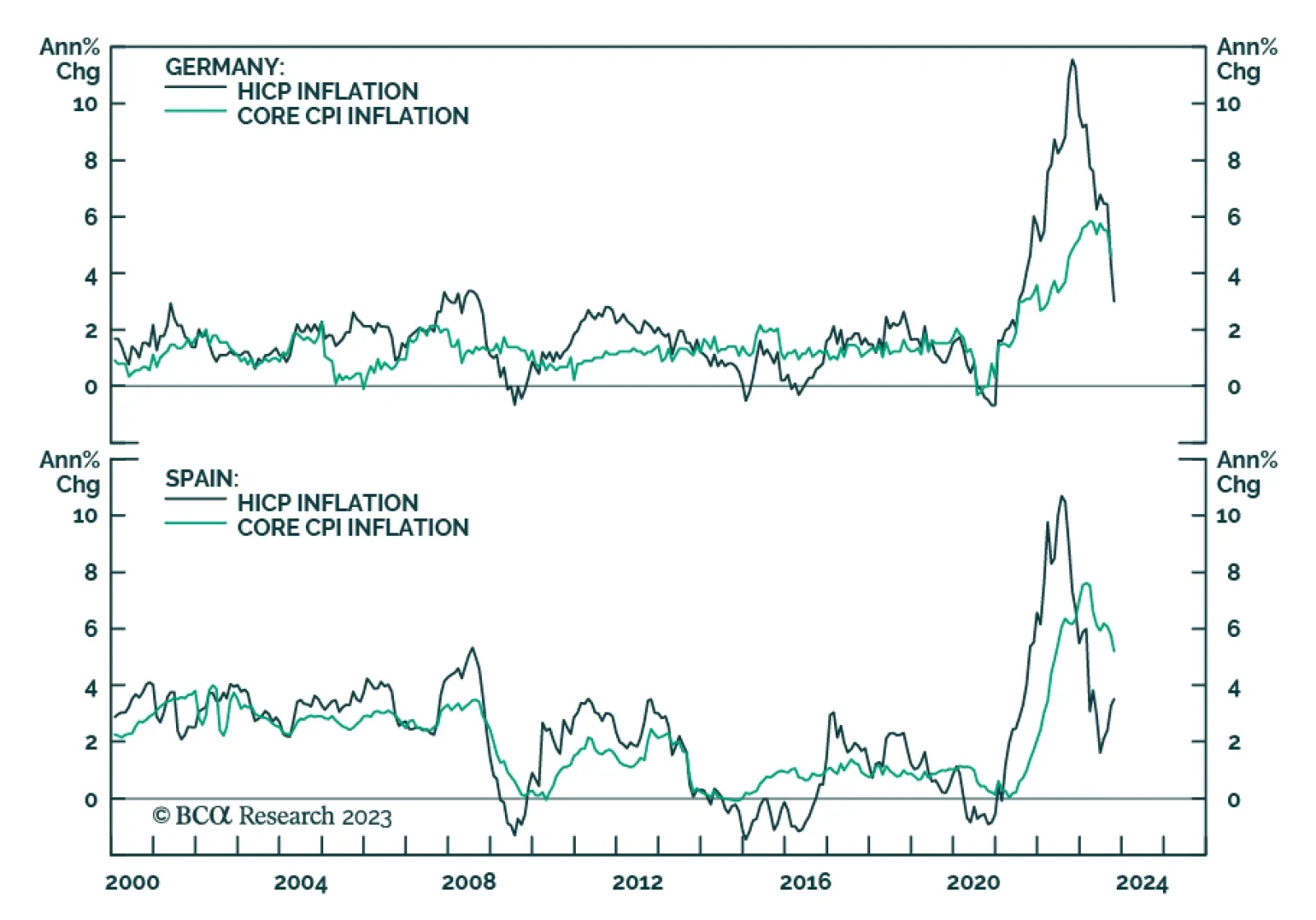

Eurozone economic data sent a positive signal on Monday. Preliminary CPI releases from Germany and Spain show price pressures continue to moderate. In Germany, the harmonized index declined by 0.2% m/m while the annual rate of change eased from 4.3% y/y to…

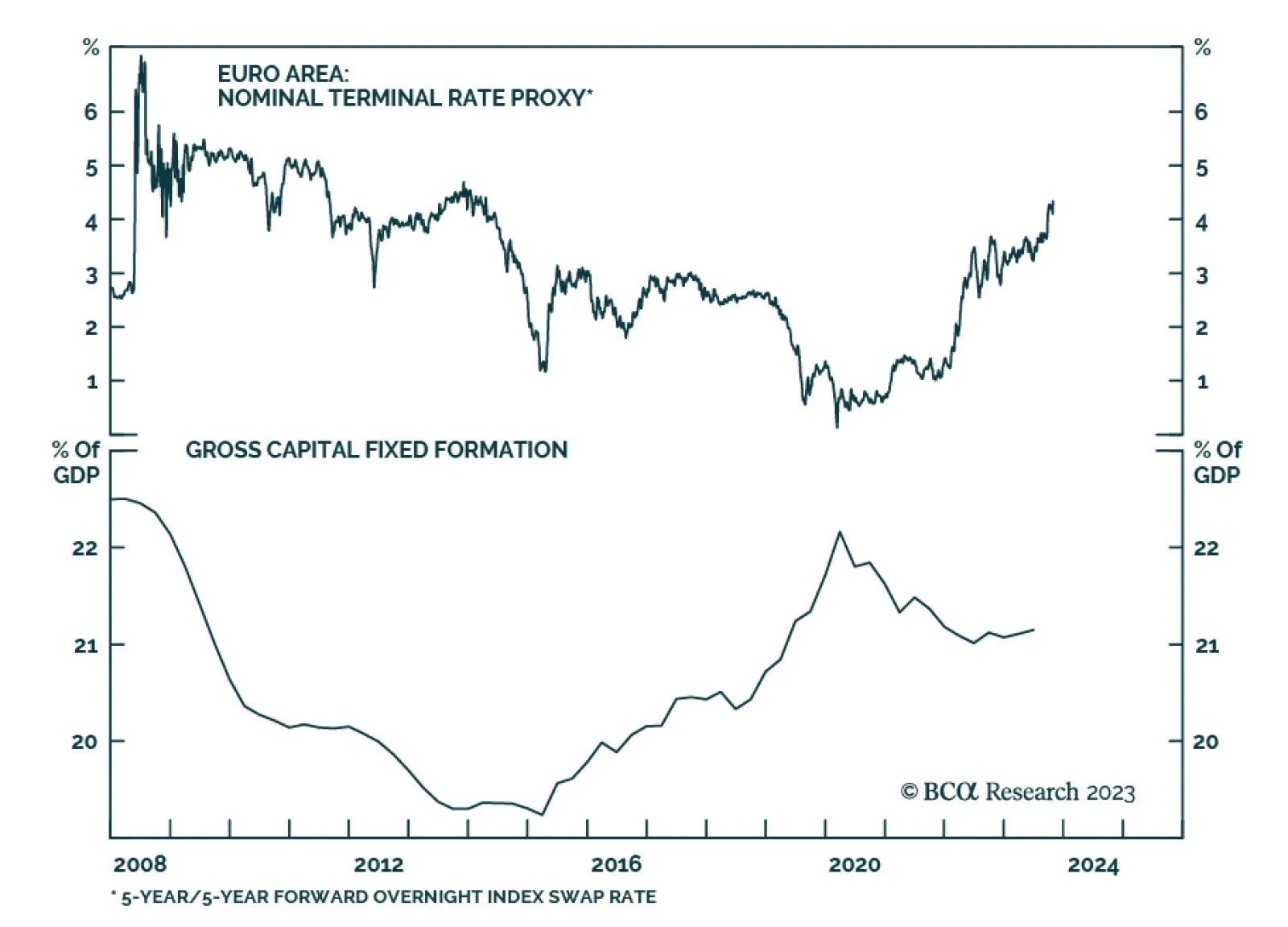

The European money market curve anticipates three rate cuts by October 2024. This pricing is appropriate considering the outlook for European growth next year. BCA’s Europe strategist expect a recession in the second half of the year, which will force the ECB…

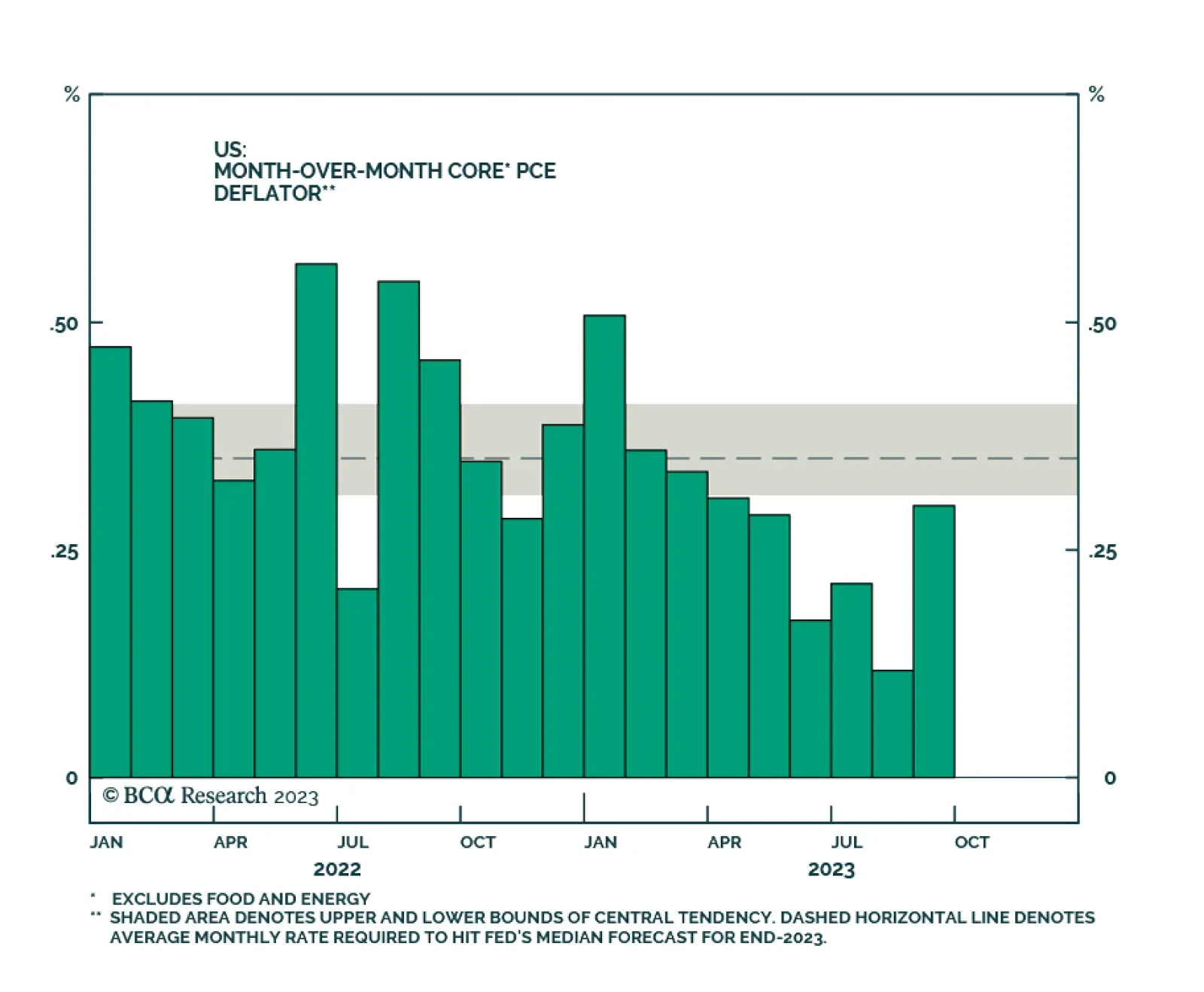

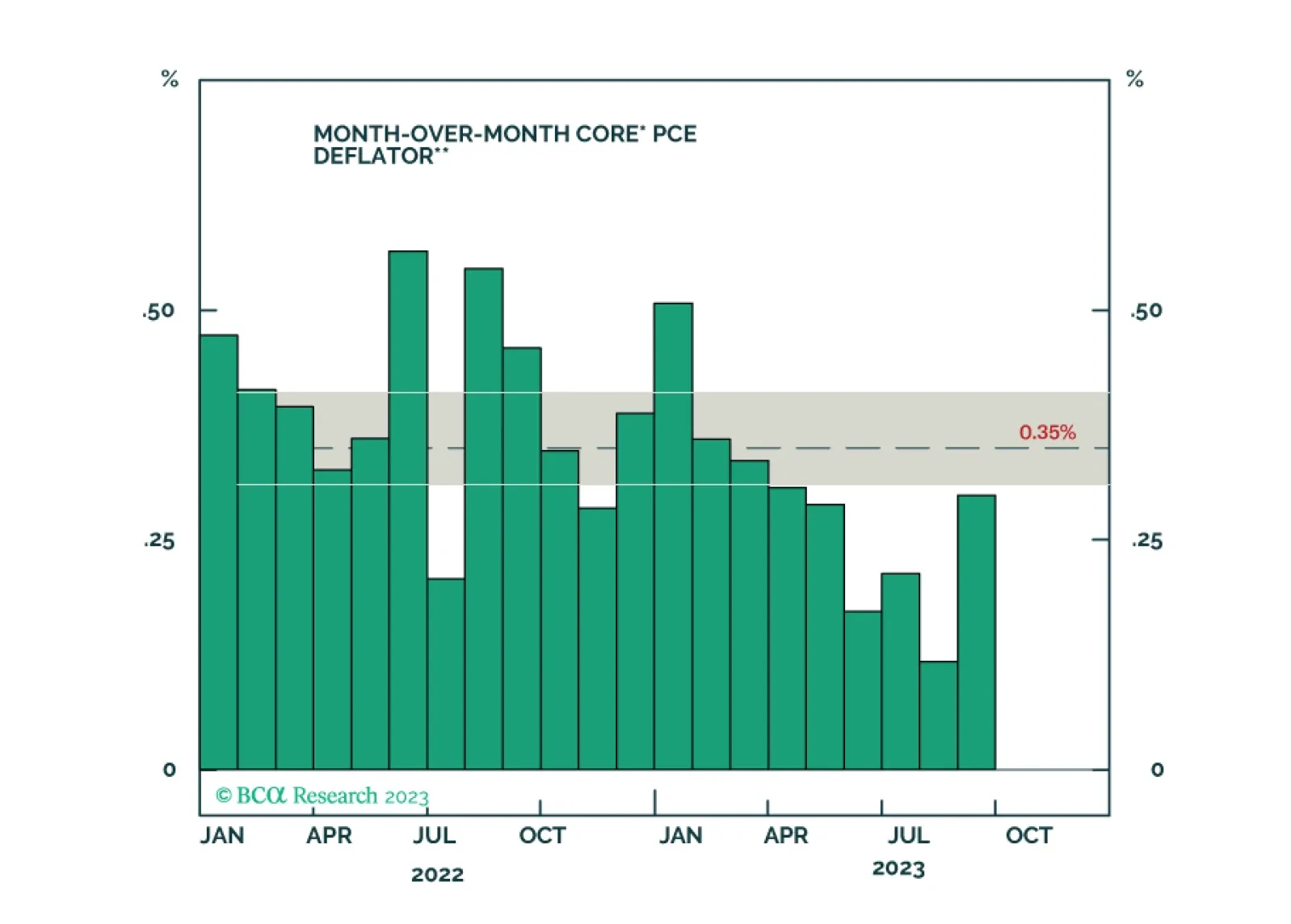

The US PCE report confirmed the signal from Thursday's preliminary GDP release that consumer spending was resilient in Q3. Although personal income growth unexpectedly slowed, both nominal and real spending growth accelerated and beat expectations in…

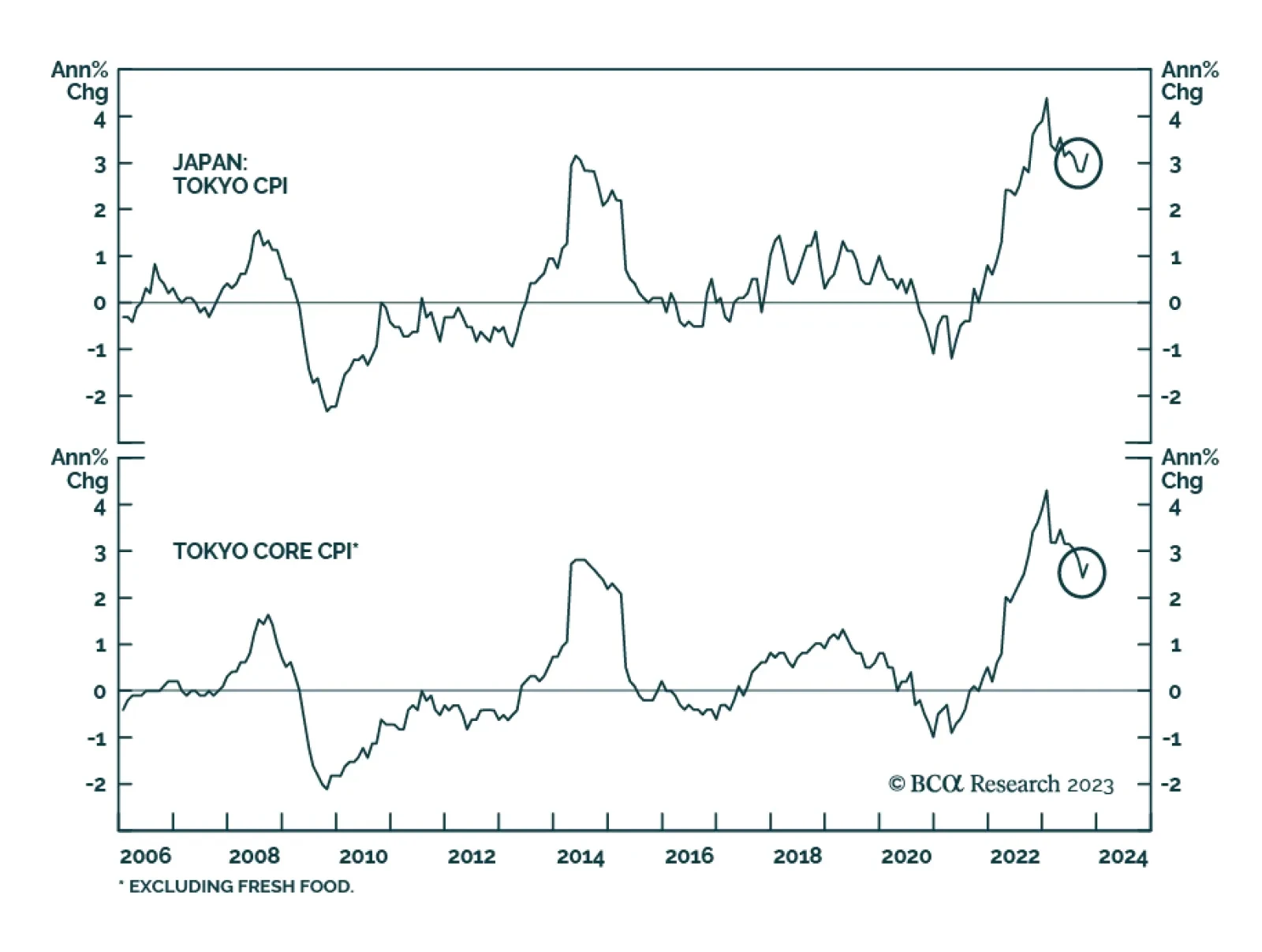

Friday's Tokyo CPI release suggests that inflationary pressures are picking back up again in Japan. Headline inflation accelerated to 3.3% y/y – surprising expectations it would remain unchanged at 2.8% y/y. The ex-fresh food component also unexpectedly rose…

A look at recent data on economic growth, inflation and the labor market, and a discussion of the implications for Fed policy and bond strategy.