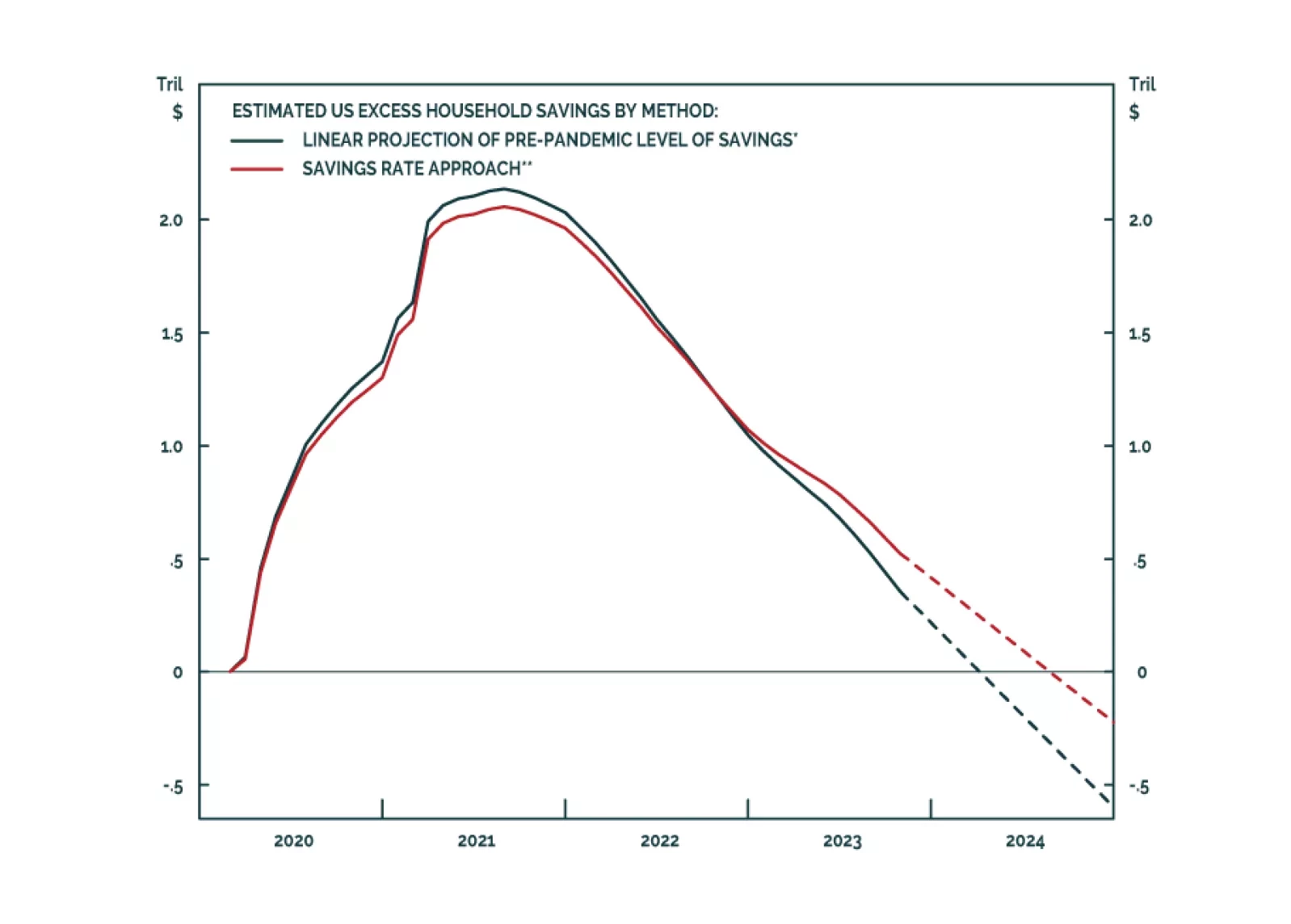

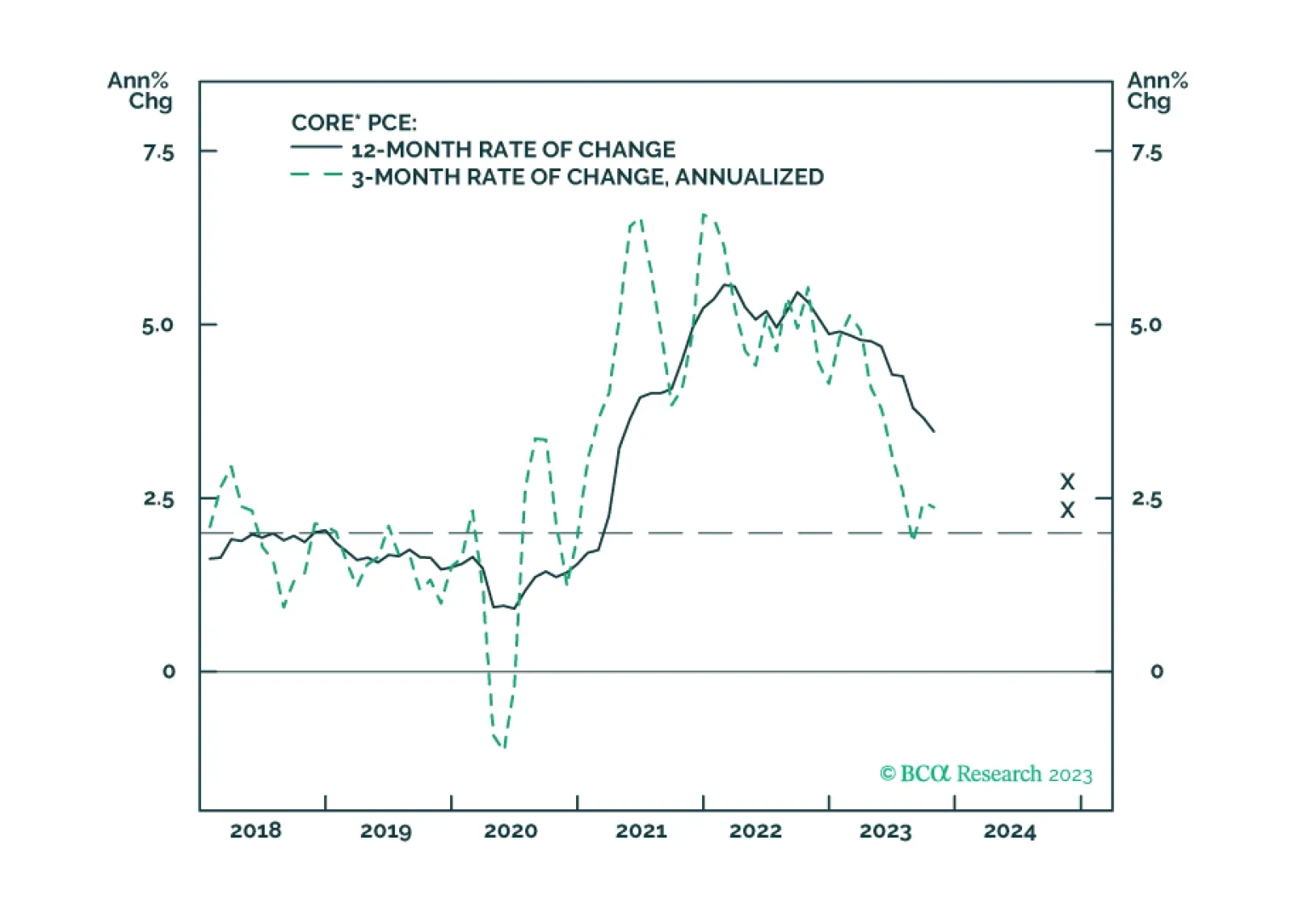

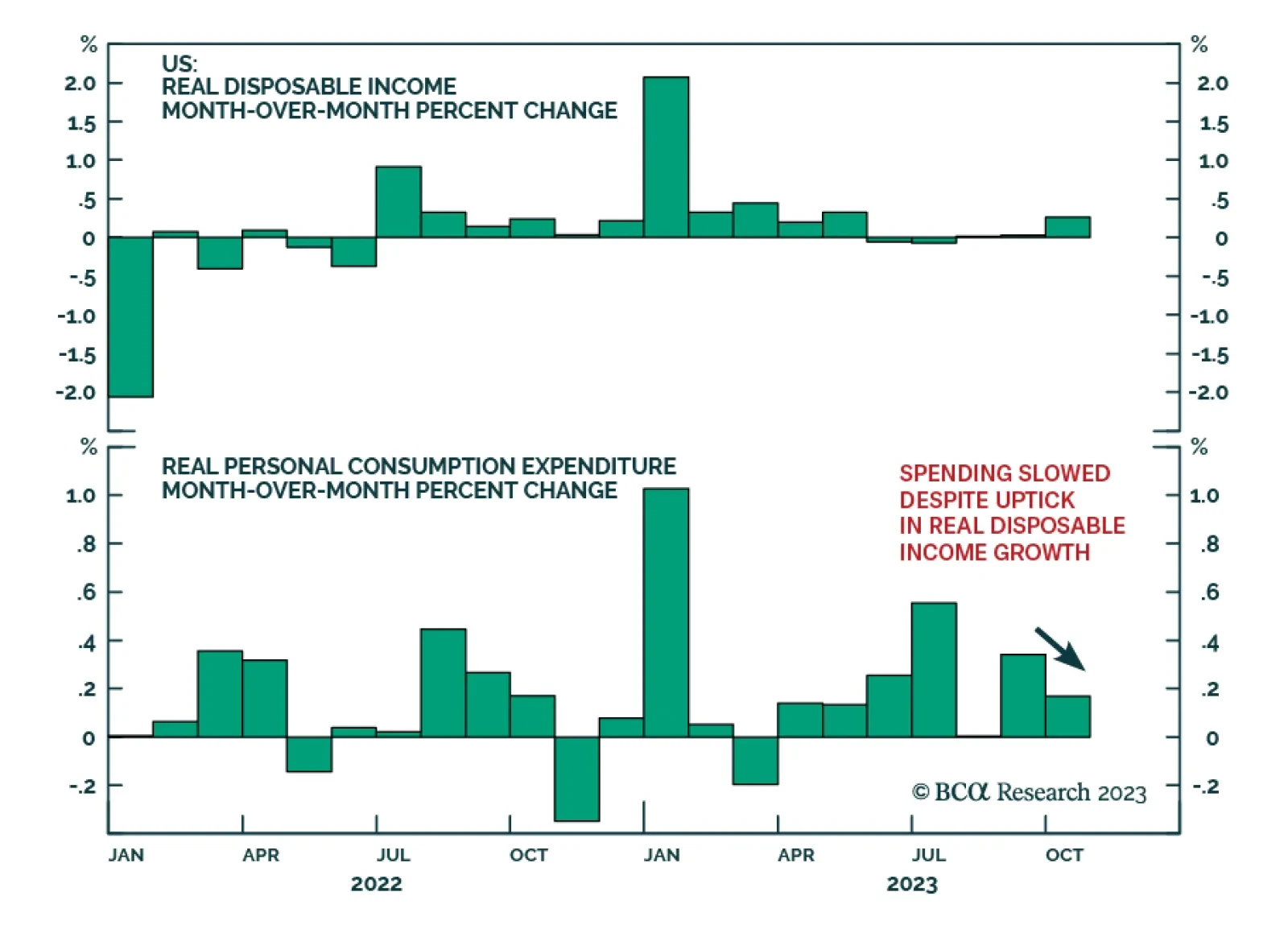

Inflation/Deflation

We enter 2024 as we were across the last four months of 2023, tactically equal weight across the board until the S&P 500 rally is complete and we gain a better entry point for underweighting equities and overweighting fixed income.

Treasury yields will sketch out a range between now and Q1 2024, with the upside determined by inflation and the downside determined by labor markets.

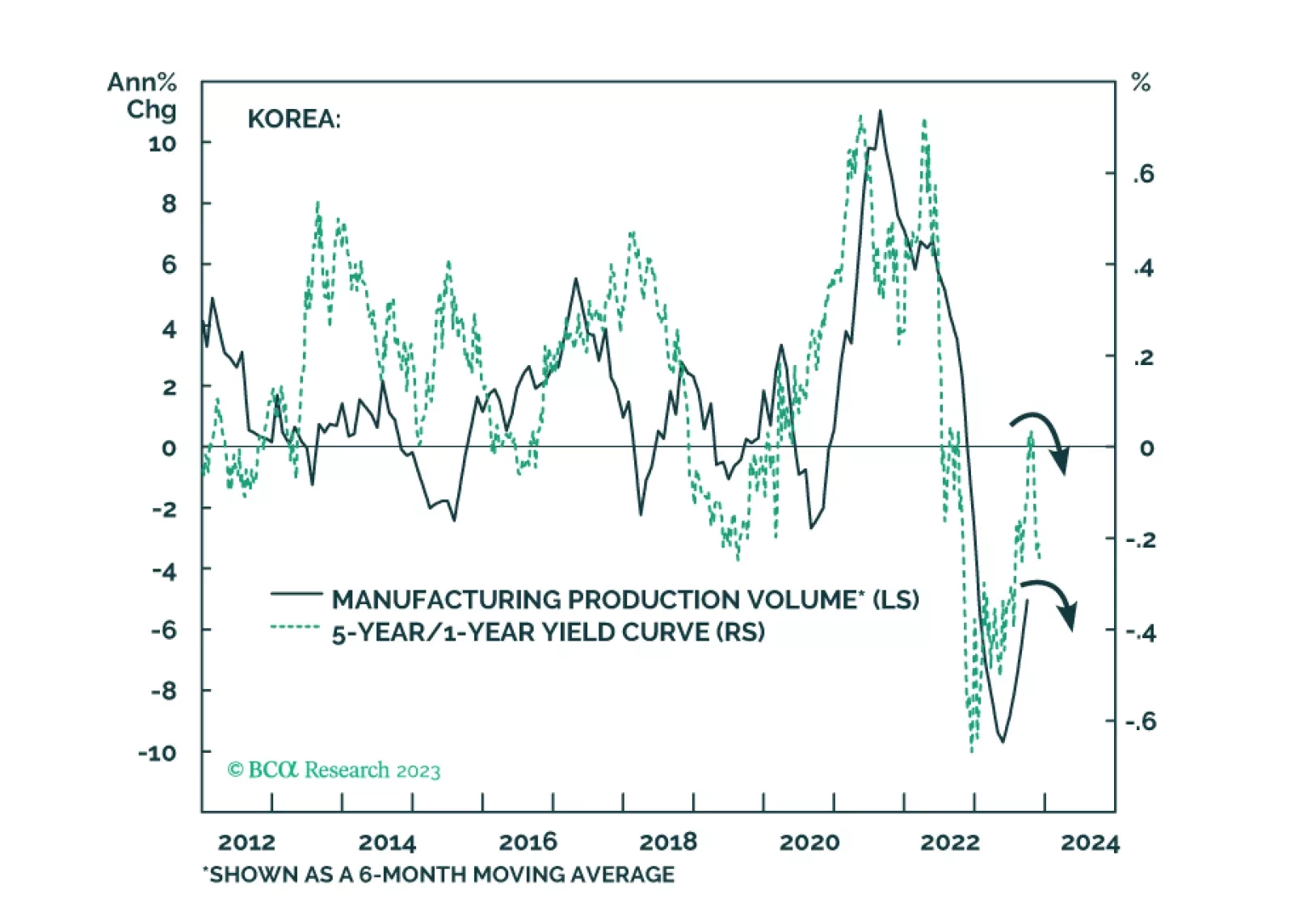

The recent increase in Korean exports will likely prove to be a mid-cycle rebound within a cyclical downtrend. Korea’s households and enterprises are among the most indebted globally, and their debt service ratio is among the highest in the world. Korea’s 10-year bond yields have peaked. We discuss opportunities in Korean stocks as well as in fixed income and currency markets.

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

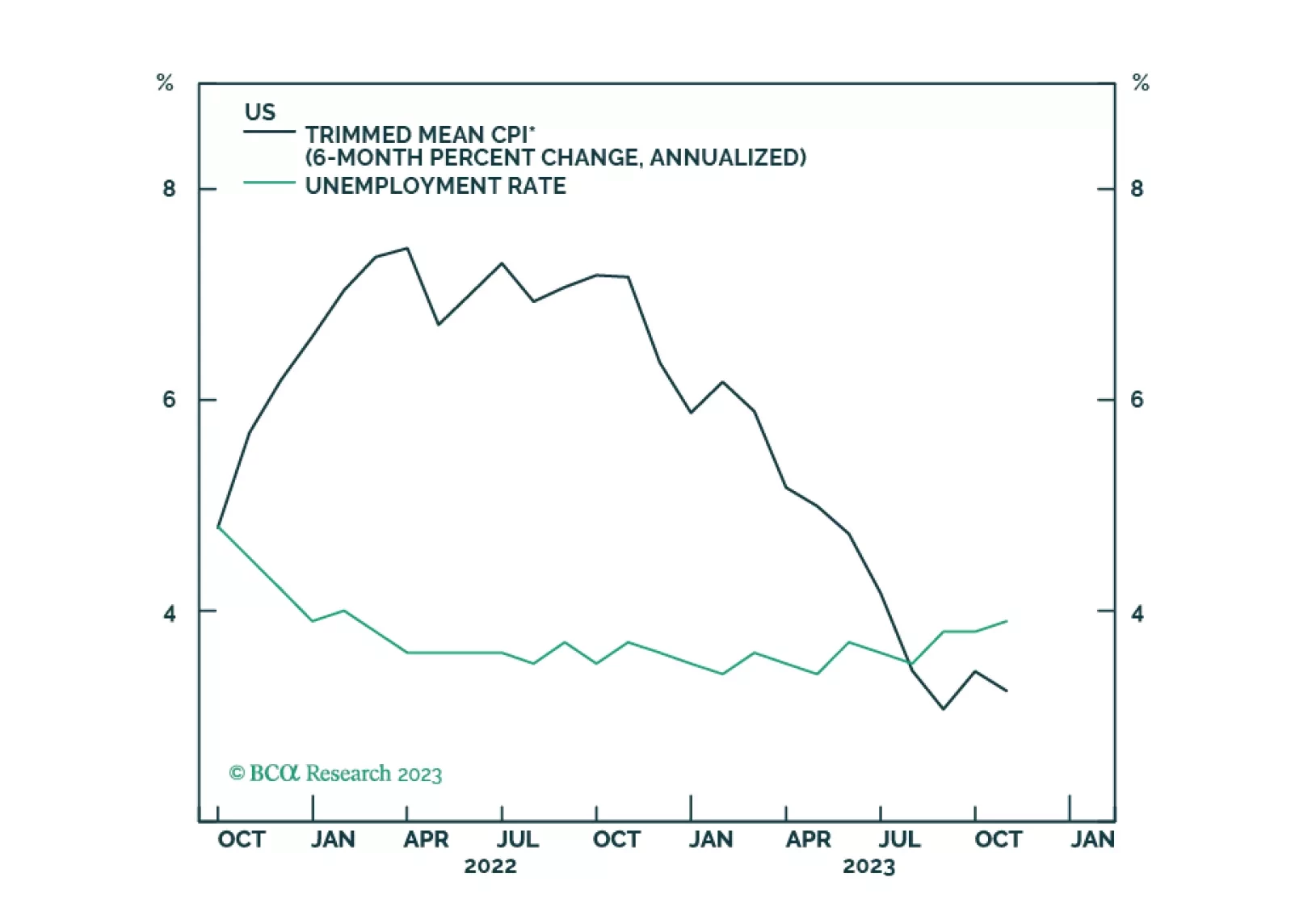

Our kinked Phillips curve framework predicted the immaculate disinflation of 2023. That same framework is now warning that the global economy is heading towards a recession in the second half of 2024.

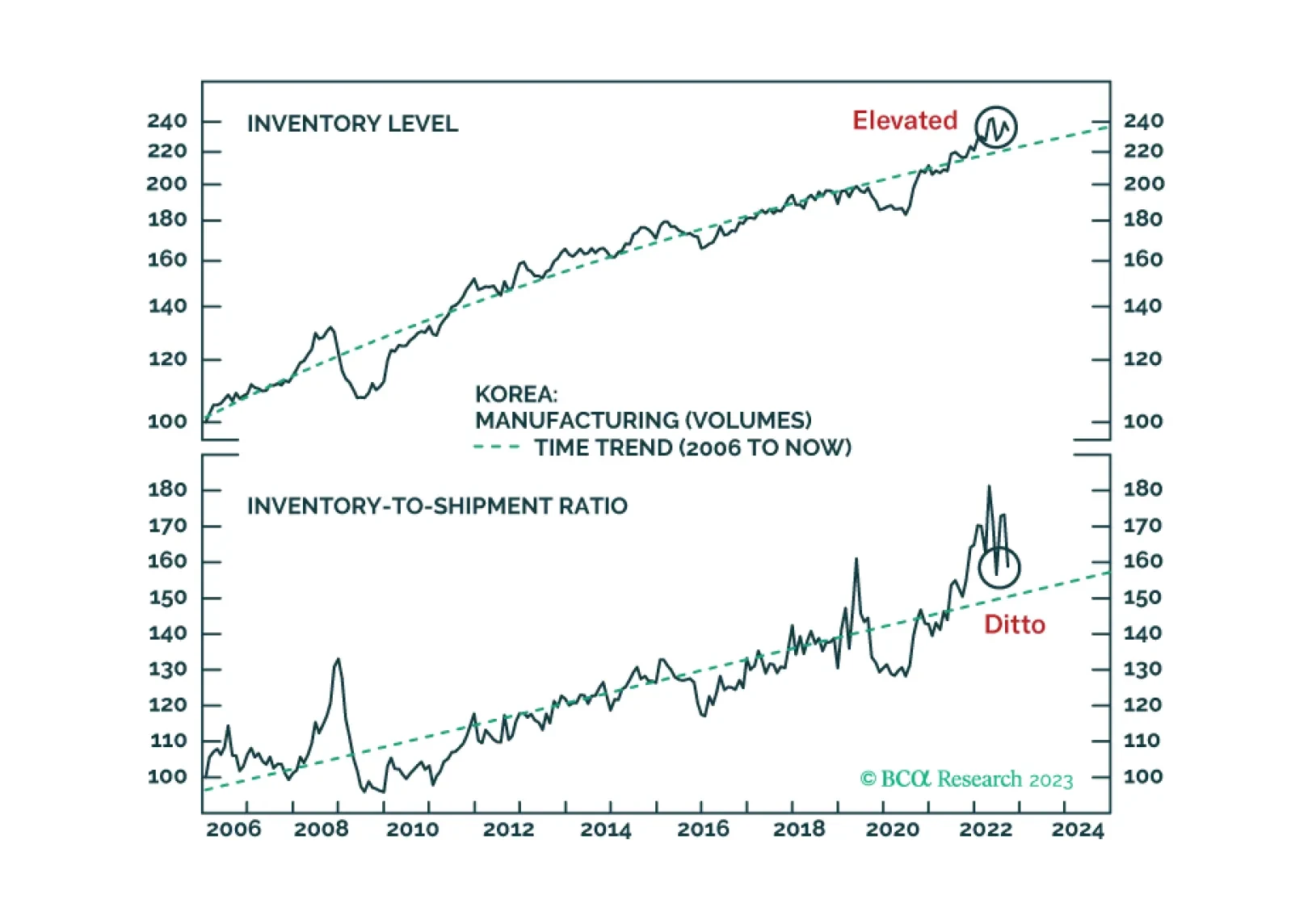

Contrary to the prevalent belief in the global investment community, goods/merchandise inventories in the US and East Asia are rather elevated. Financial markets respond to final demand fluctuations, not inventory restocking. Global manufacturing/trade will continue contracting, even though the pace of contraction might moderate in the near run. We recommend that investors fade the current rally.