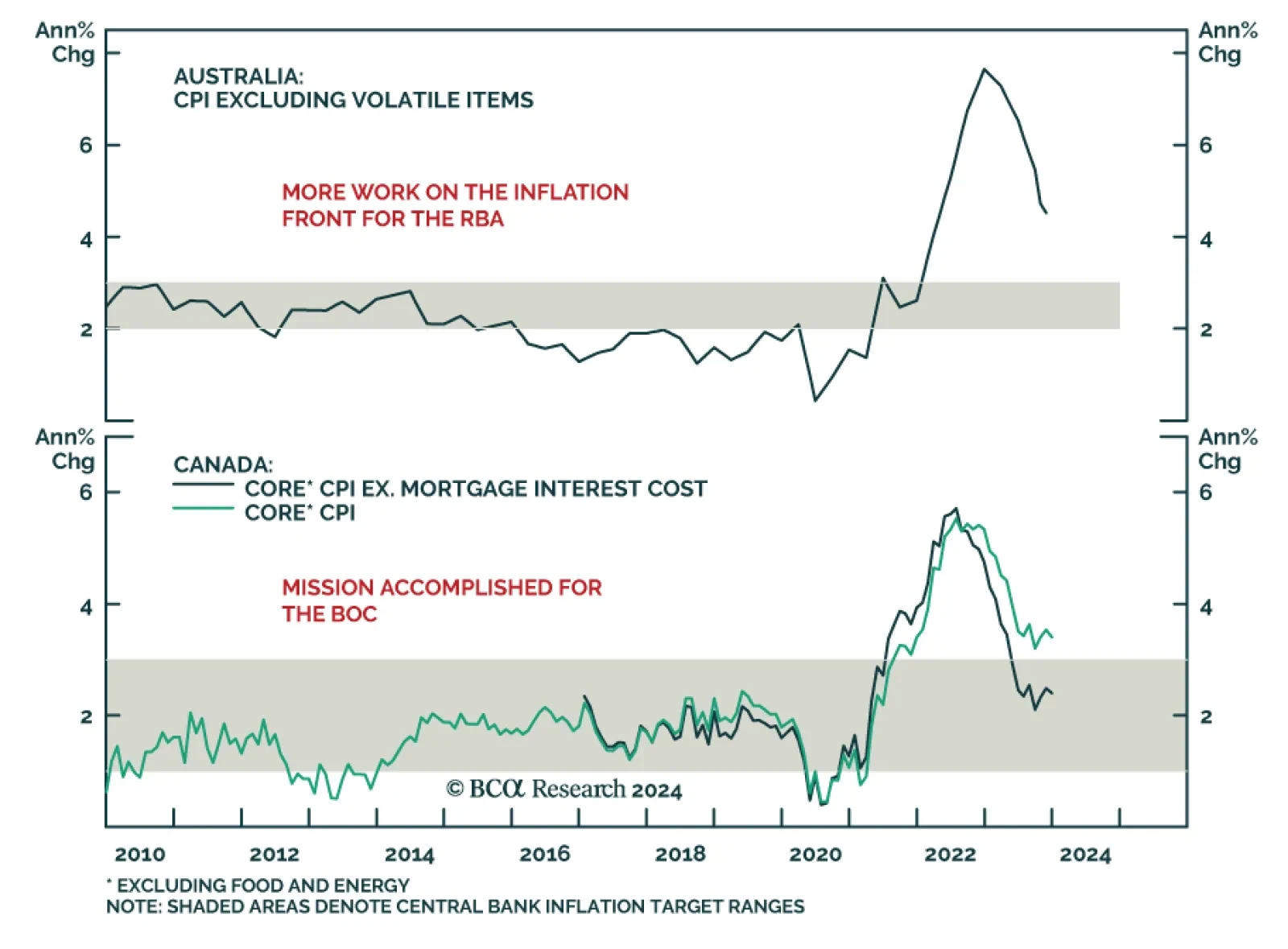

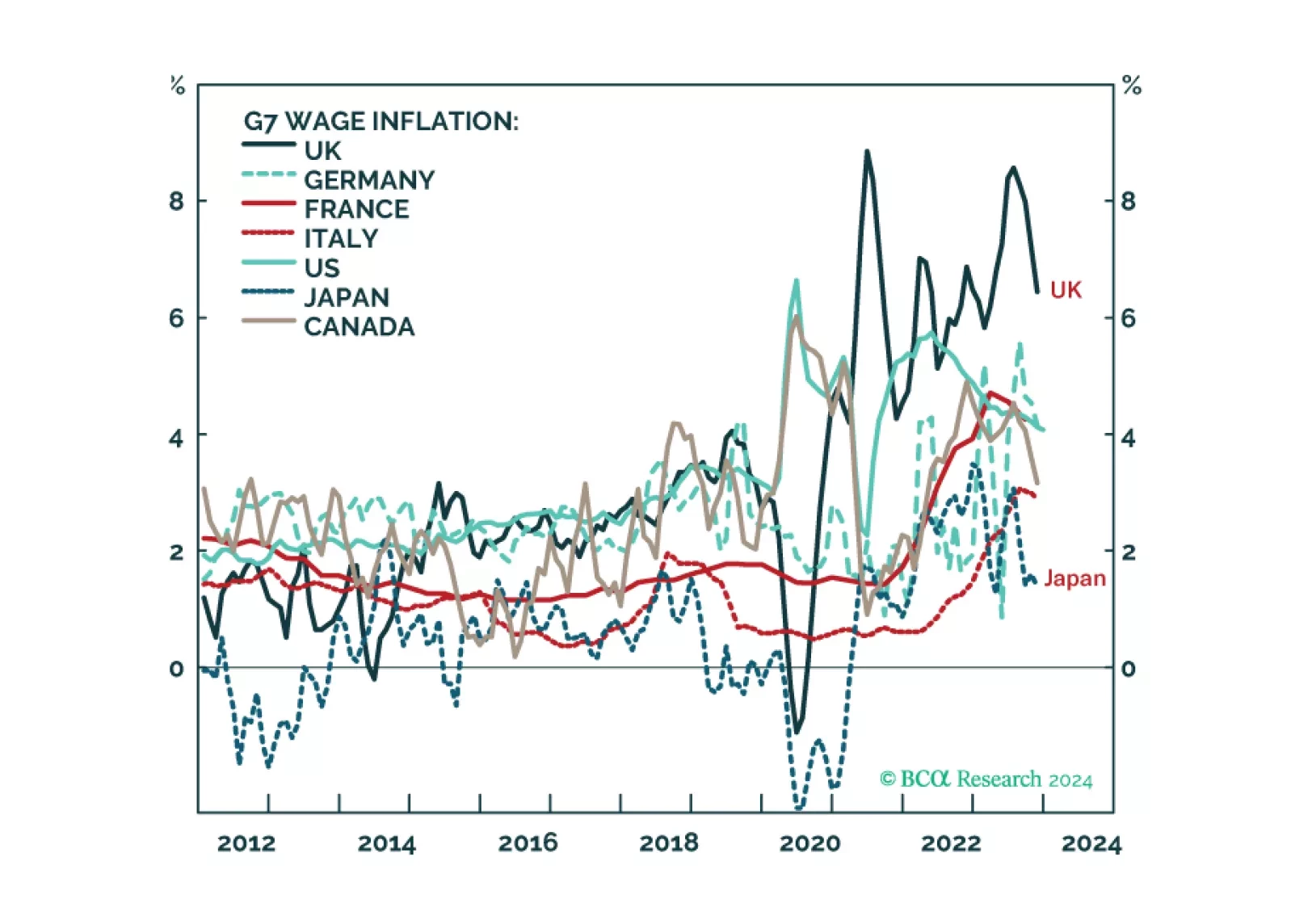

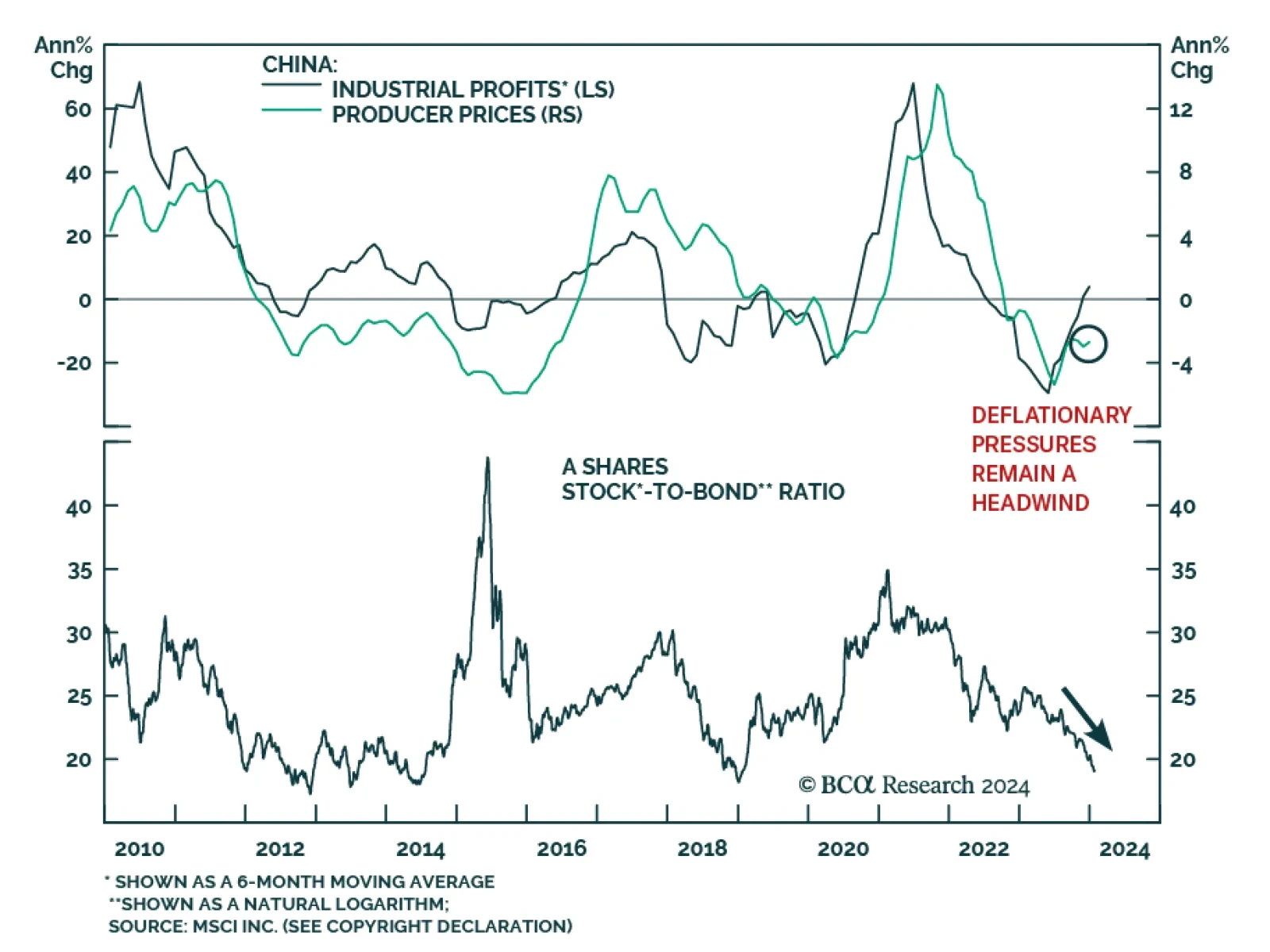

Inflation/Deflation

We describe and explain the wide disparity of wage inflation across G7 economies, and discuss what it means for the Fed, ECB, BoE, and BoJ policy moves in the coming year. Plus: we highlight two investments ripe for reversal, and two investments ripe for rebound.

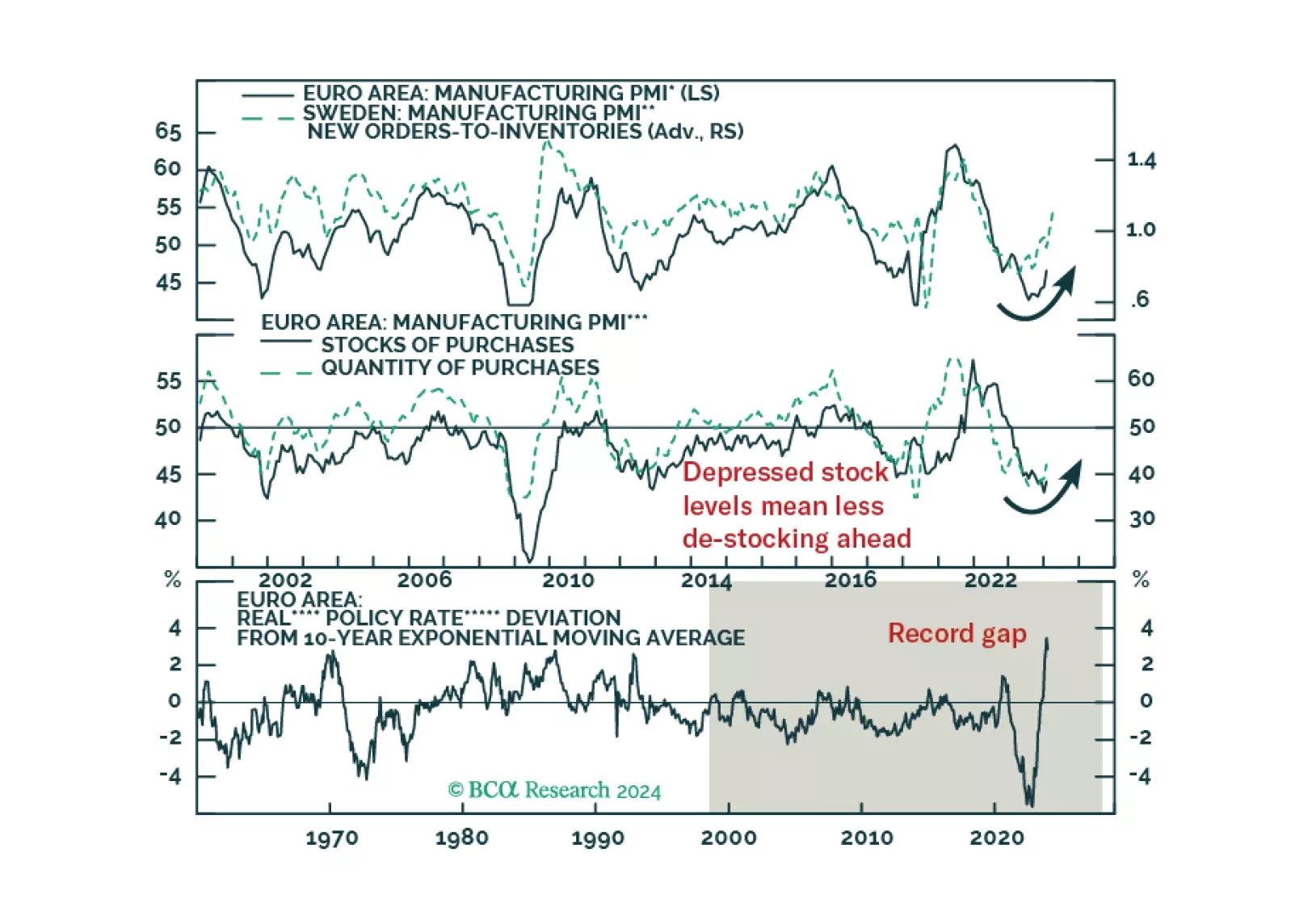

Is the rebound in European PMIs enough to boost the appeal of European risk assets?

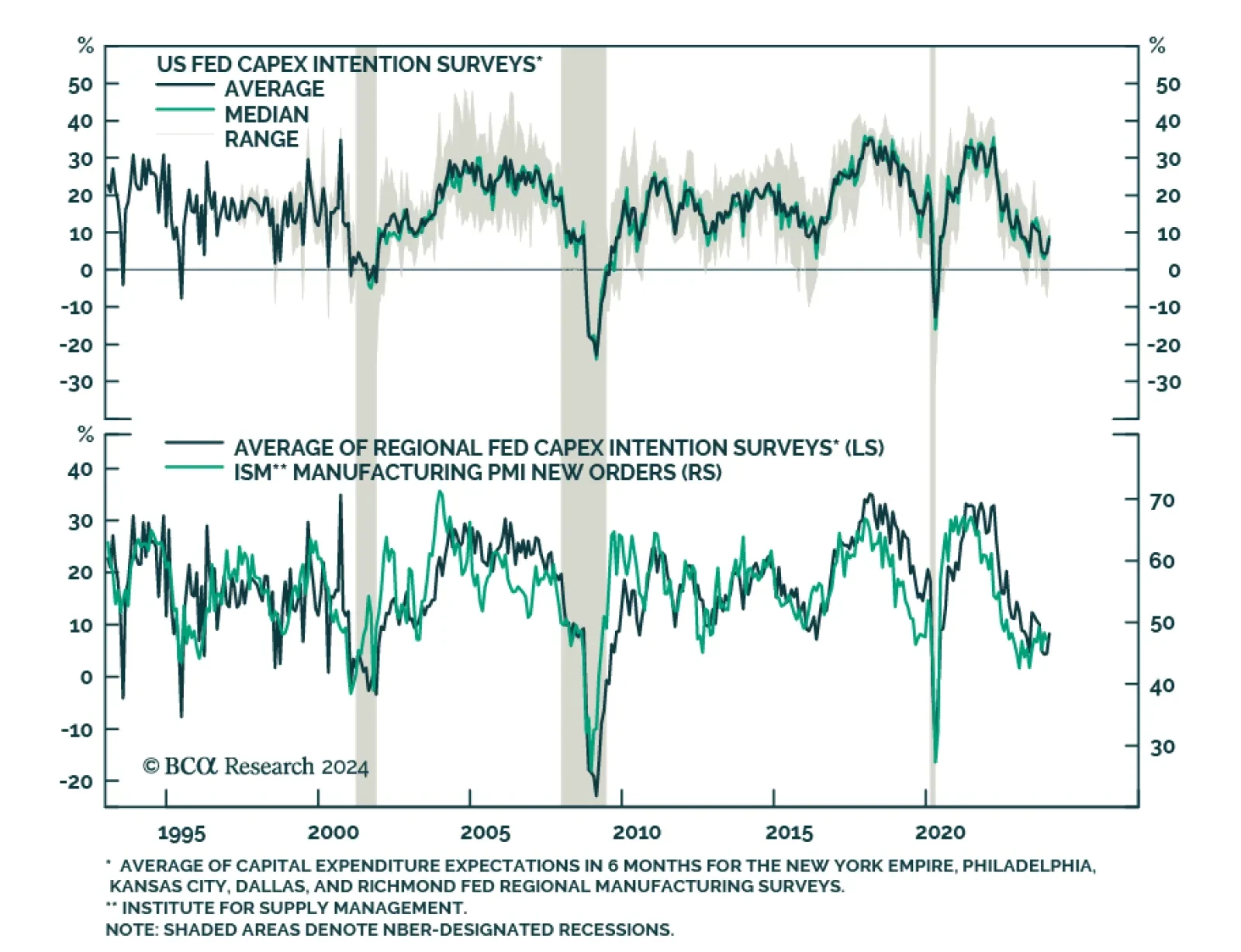

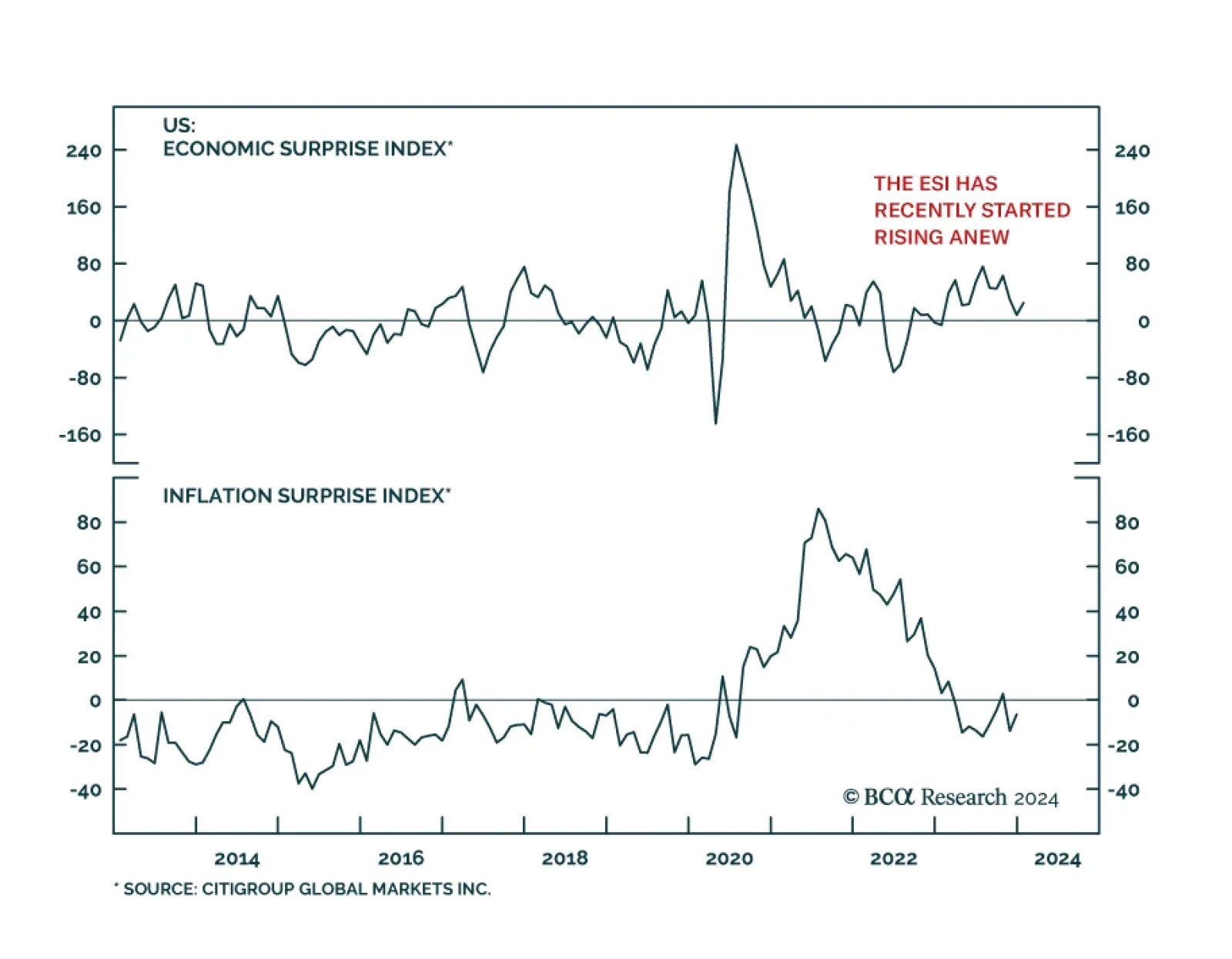

A recent slew of macroeconomic data has reassured us that the runway to a recession is longer than many thought. However, that positive realization comes with two caveats. First, the Fed pivot is not imminent, and the magnitude of rate cuts may disappoint. Second, the recession has been delayed but not avoided. Further, geopolitical risk is elevated. We will overweight Tech on the next dip and upgrade Retail to an overweight.

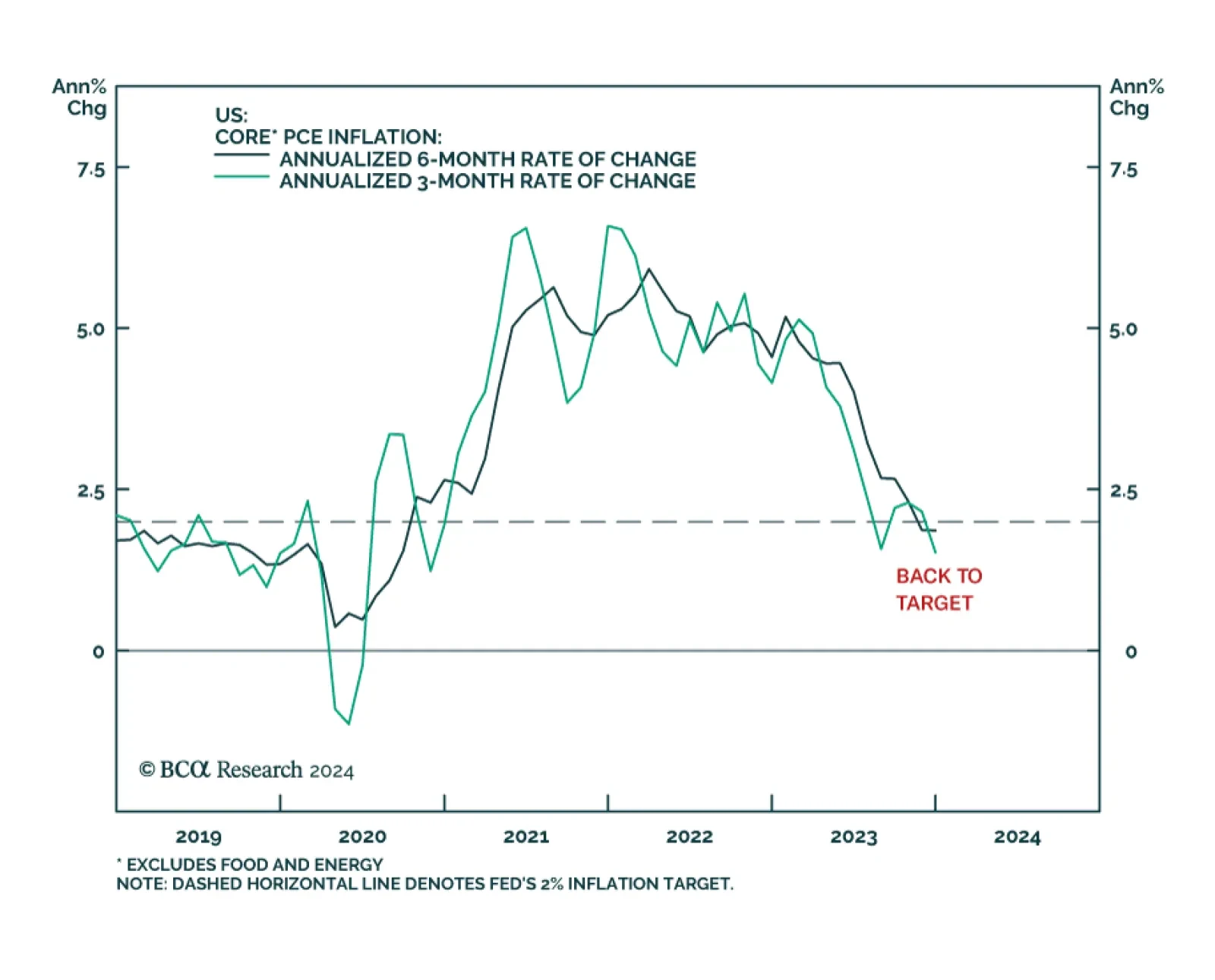

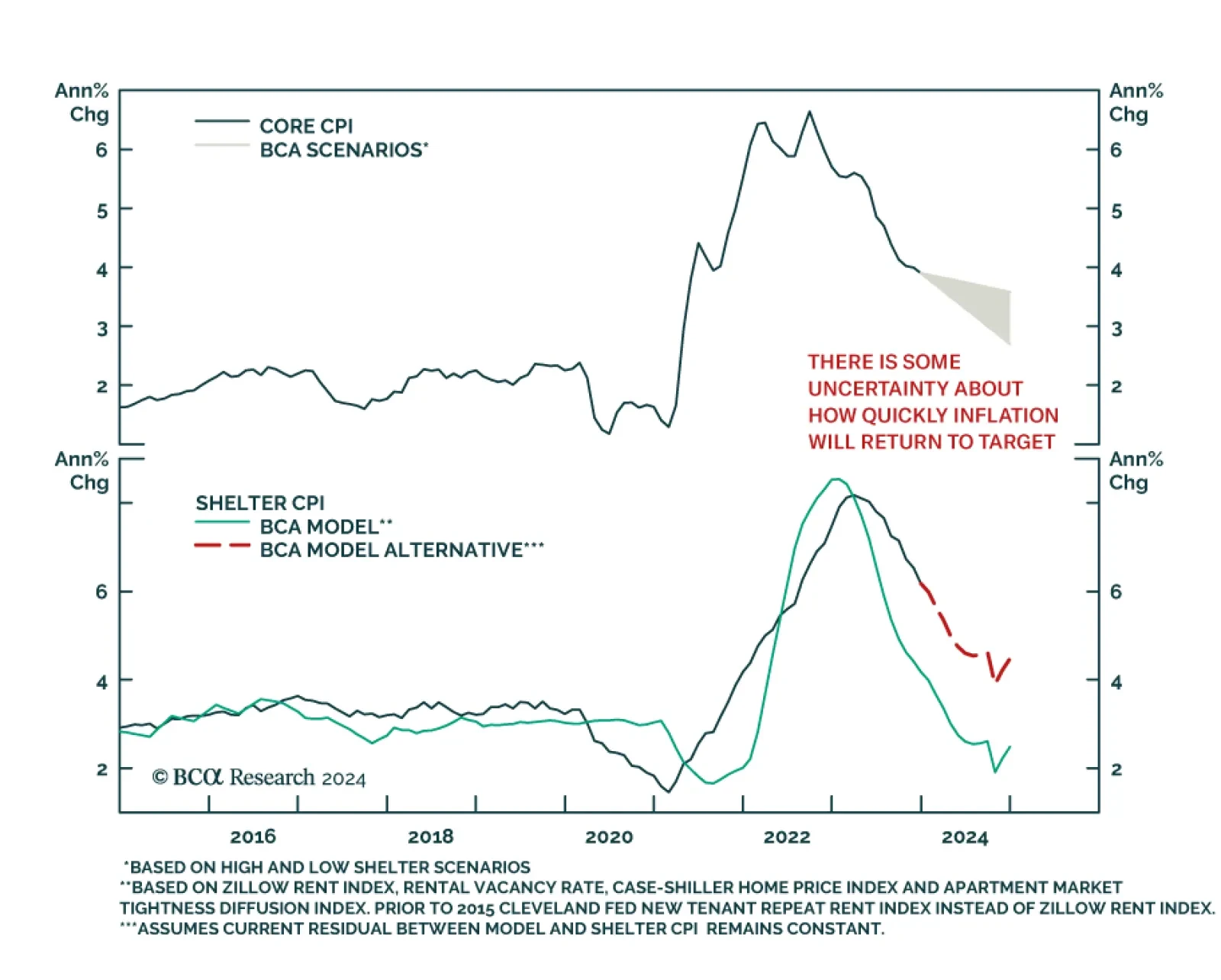

Low inflation argues for the Fed to move relatively quickly toward rate cuts. Continued above-trend GDP growth poses a risk to this view, but leading indicators point to slower growth in the coming quarters.