Inflation/Deflation

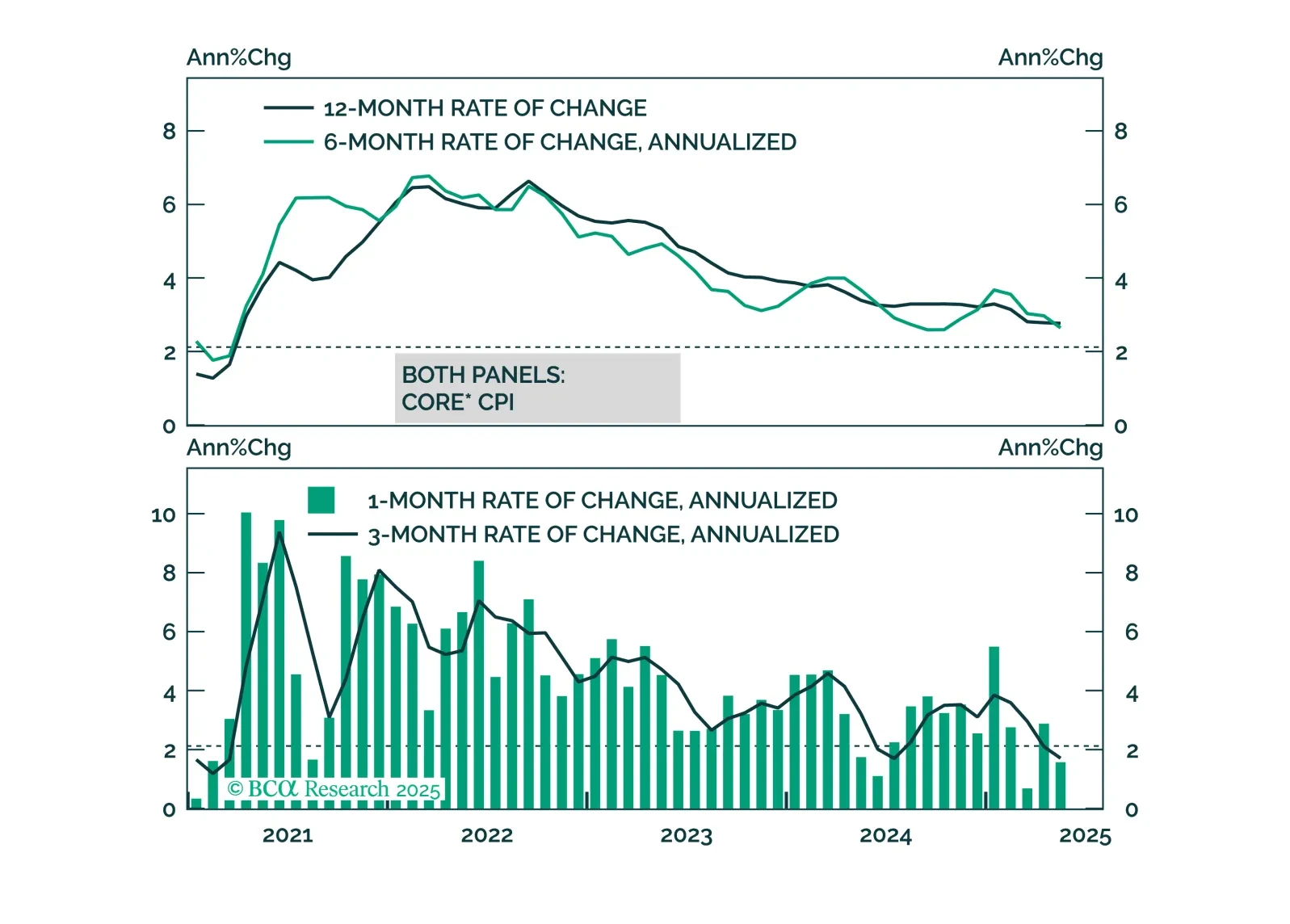

Colder May CPI reinforces our overweight in government bonds and tactical steepener trades as growth slows and the Fed stays cautious. Headline inflation rose 0.1% (2.4% y/y), below expectations, as did core CPI (2.8% y/y). Goods inflation was flat, and…

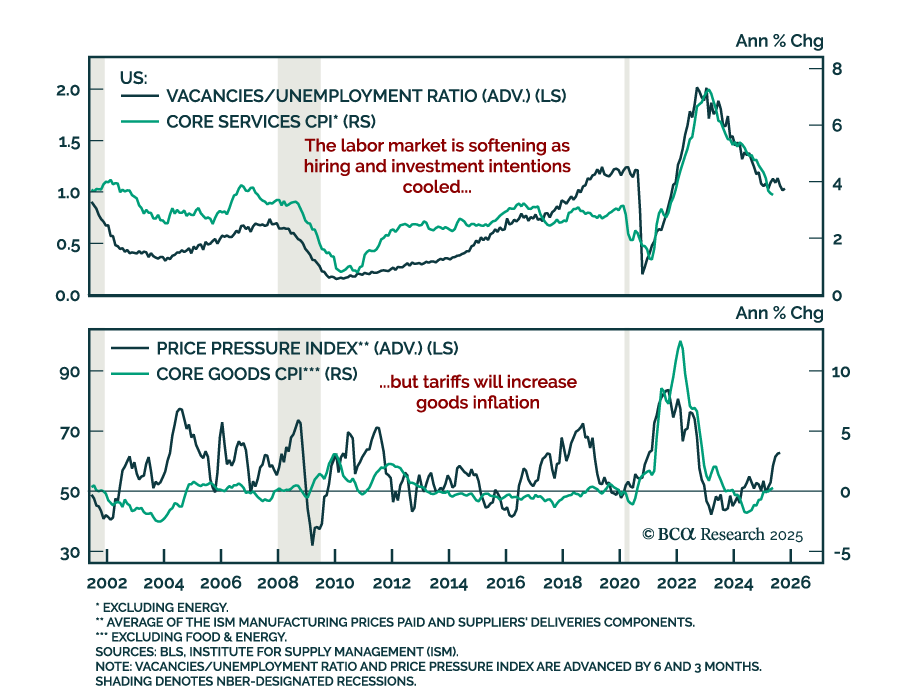

While we anticipate higher inflation in June, it looks increasingly likely that the price impact from tariffs will be less aggressive and long-lasting than many feared.

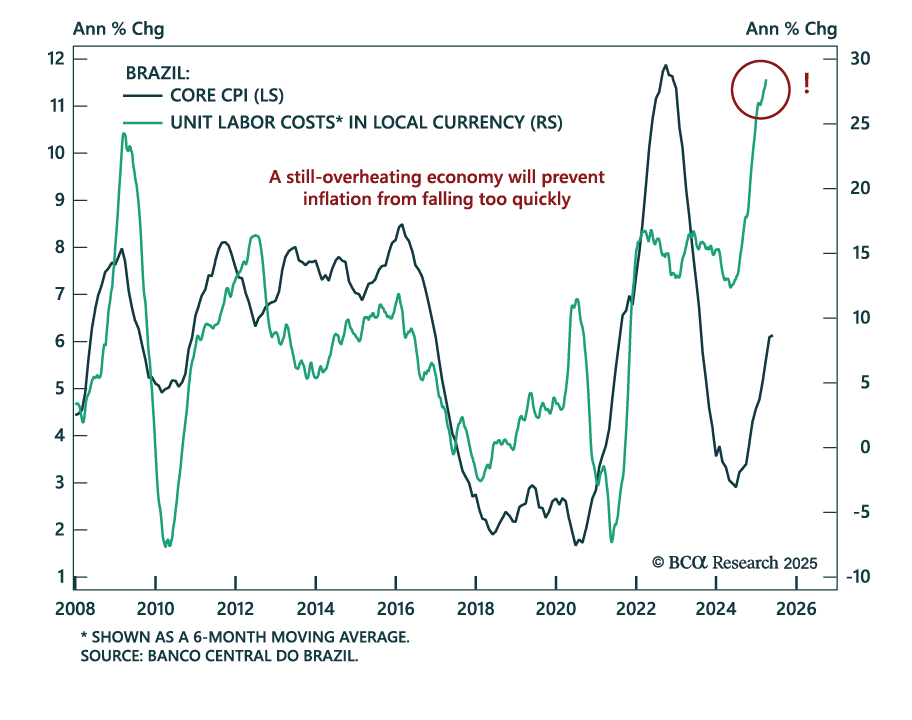

The May Brazilian CPI suggests that price pressures may have reached a peak, but do not expect immediate monetary easing to support fixed income markets. Headline CPI slowed to 5.3% y/y from 5.5% April, but core CPI remained flat at 6.1%. Despite…

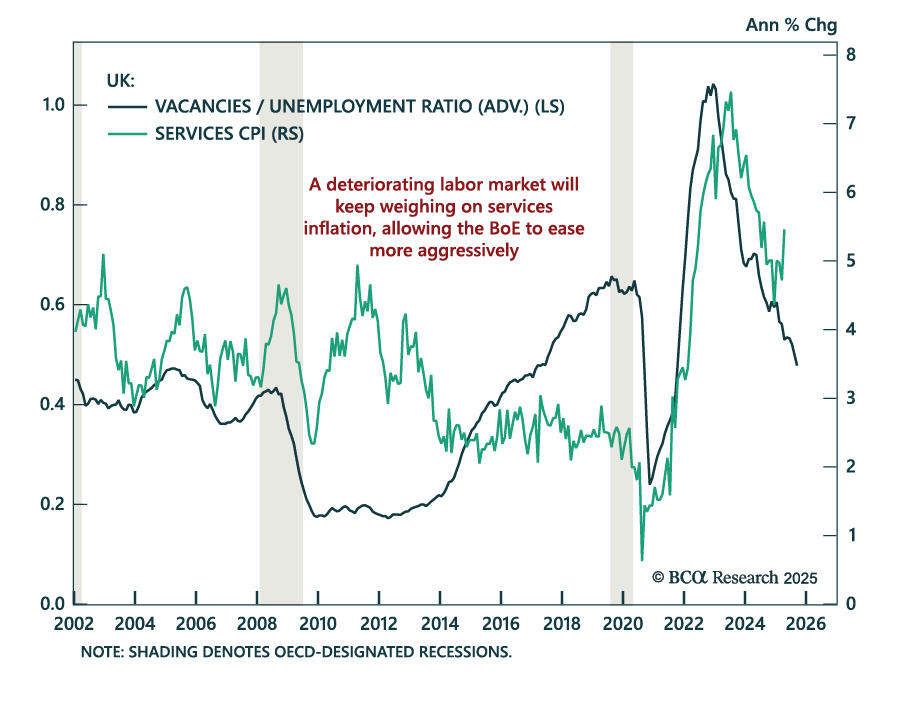

UK labor market deterioration reinforces our overweight on Gilts and dovish BoE policy trades. Payrolls fell by 109k in May, an acceleration from the 55k revised decline for April (originally reported as -33k), and job vacancies continued to slide. Slower…

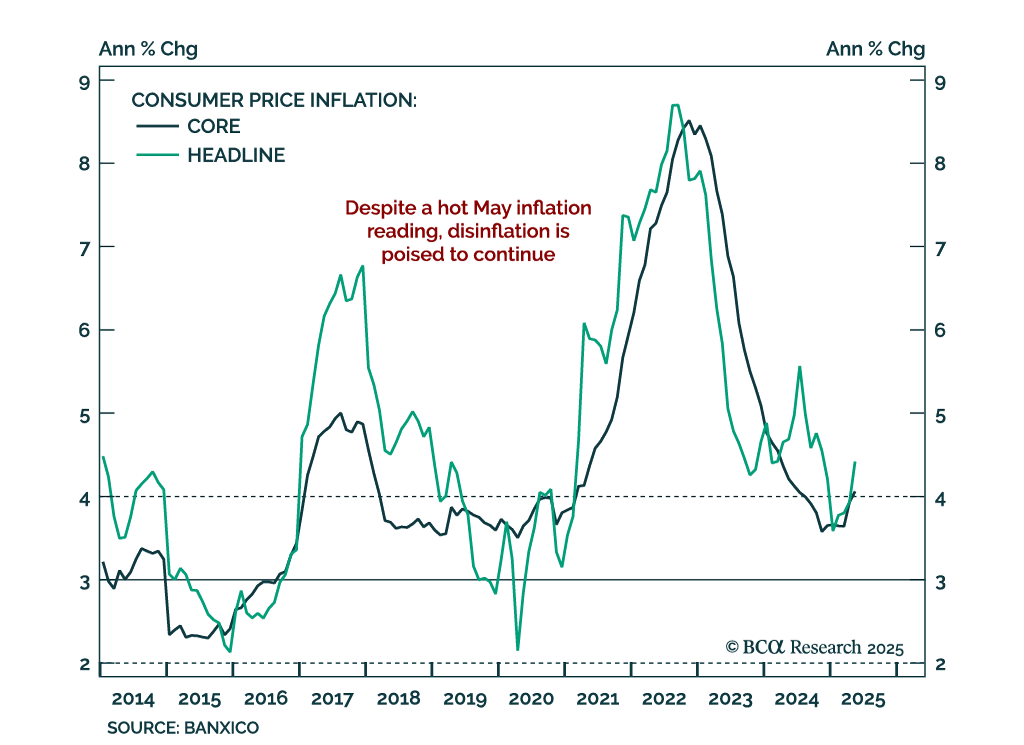

Hot May inflation should not derail Banxico’s easing cycle; we remain long Mexican local bonds. Headline inflation accelerated to 4.4% y/y from 3.9%, above expectations, while core inflation was roughly flat at 4.1% from 3.9%. The upside surprise was driven…

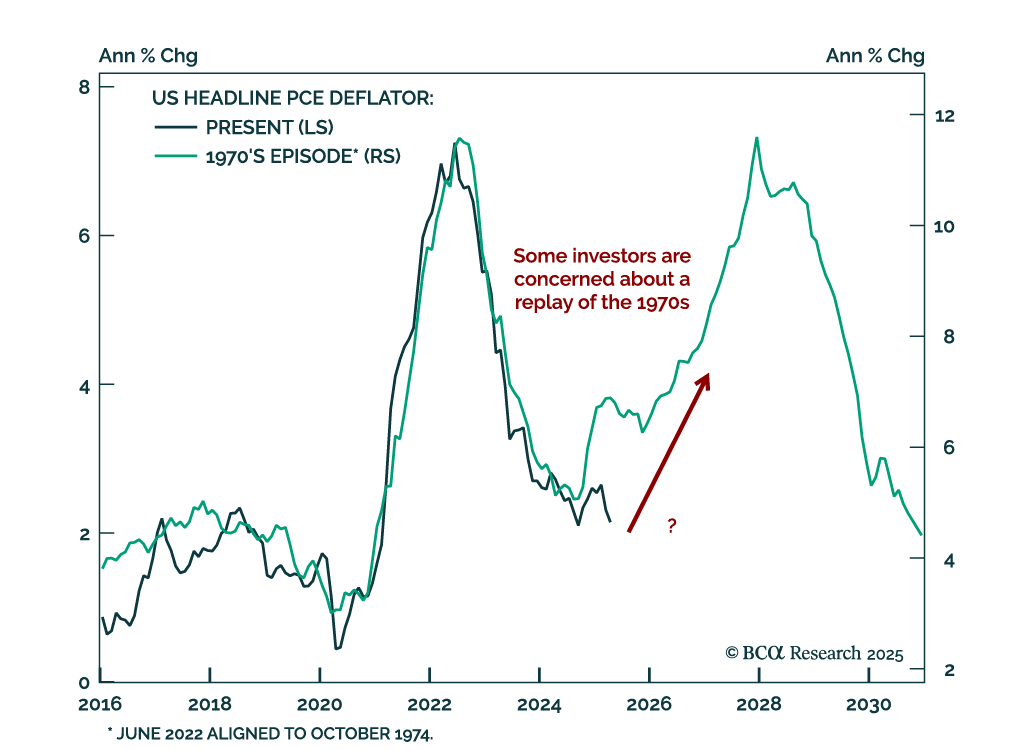

Our Special Reports Unit evaluates whether US inflation is likely to remain structurally elevated. While our base case is for inflation to hover around or modestly above 2% over the long run, there are several risks to that view. Demographics are the most…

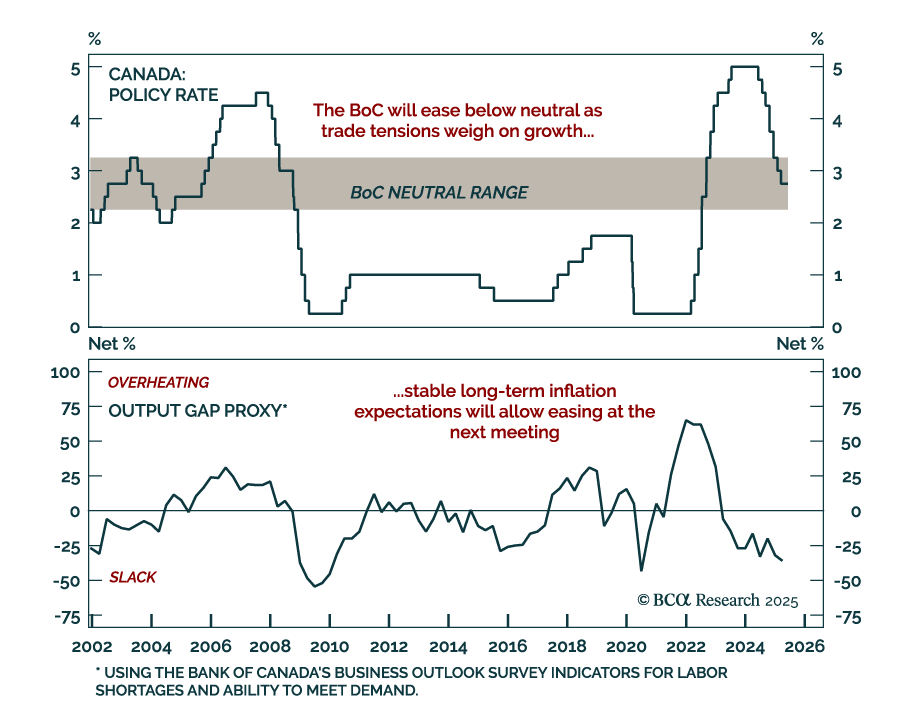

The Bank of Canada held rates at 2.75% but signaled a dovish shift, pushing us to overweight Canadian government bonds and go long CORRA futures. The policy rate remains within the BoC’s neutral range, allowing the Bank to wait for more clarity on trade…

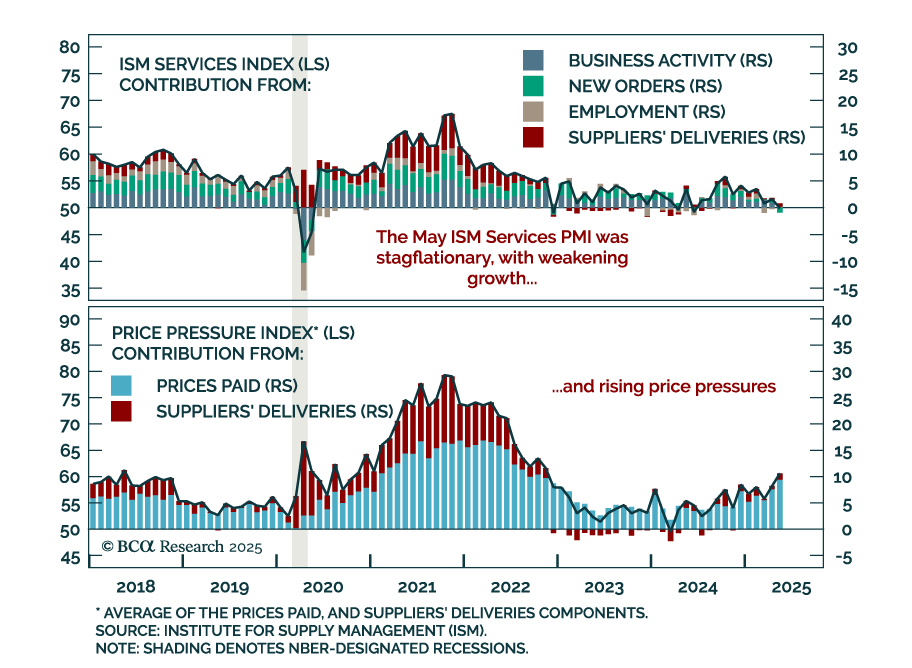

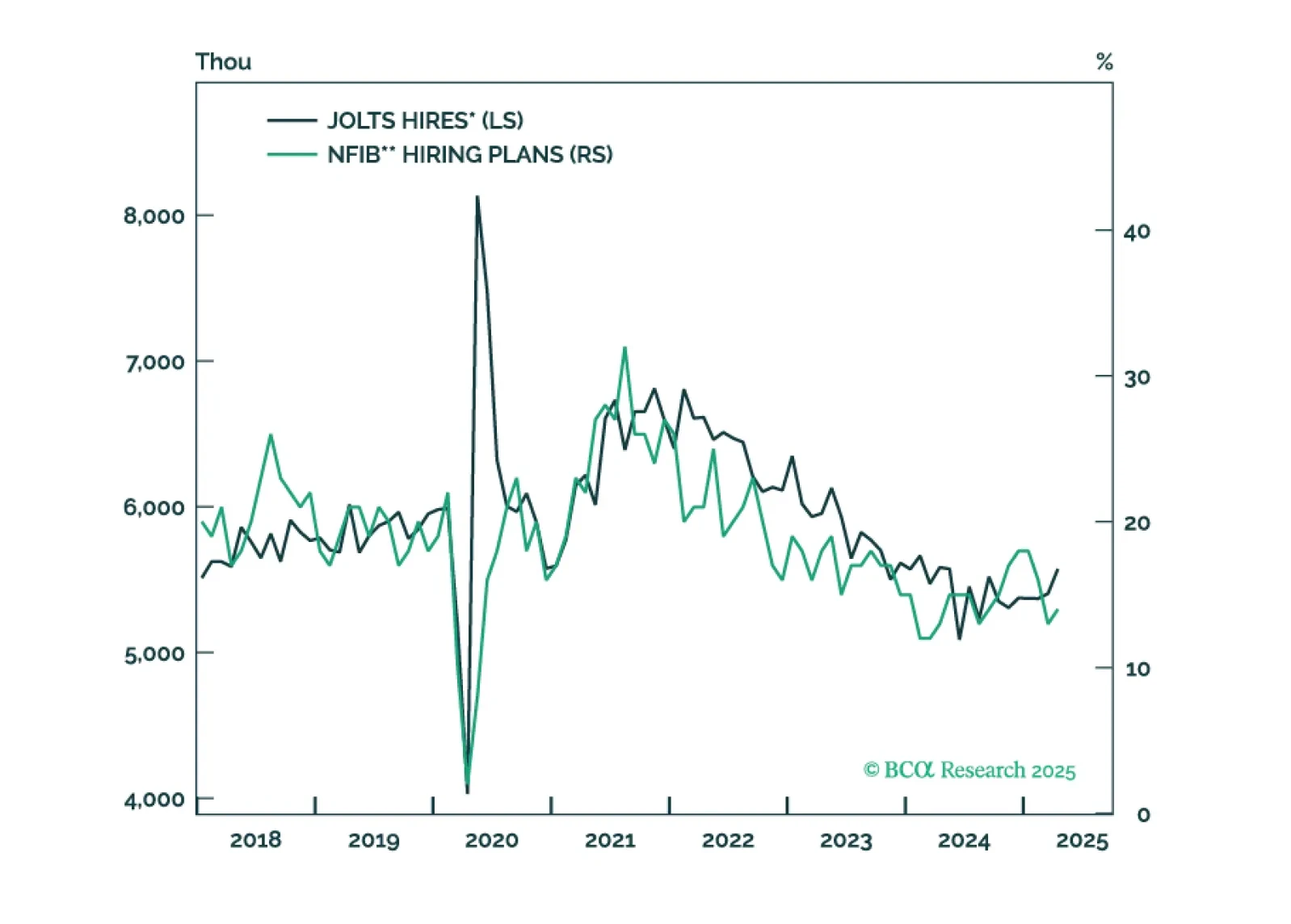

The May ISM Services PMI sent a stagflationary signal, reinforcing the case for defensive positioning. The headline index slipped into contraction at 49.9 from 51.6 in April, missing expectations. New orders collapsed to 46.4 from 52.3, while employment edged…

Our Portfolio Allocation Summary for June 2025.

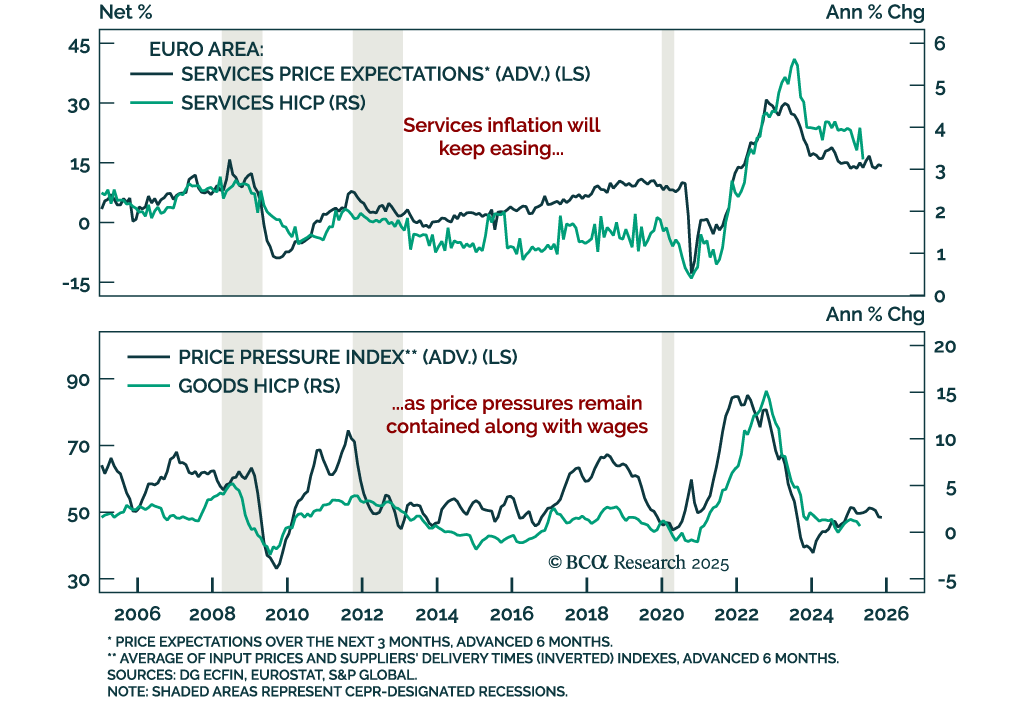

Cooler May inflation in the Eurozone and Switzerland reinforces the case for an ECB rate cut and supports our defensive positioning across European rates and FX. Headline Eurozone HICP fell to 1.9% y/y from 2.2%, with core down to 2.3% from 2.7%. Services…