Inflation/Deflation

This week we present our outlook for the Fed in 2023.

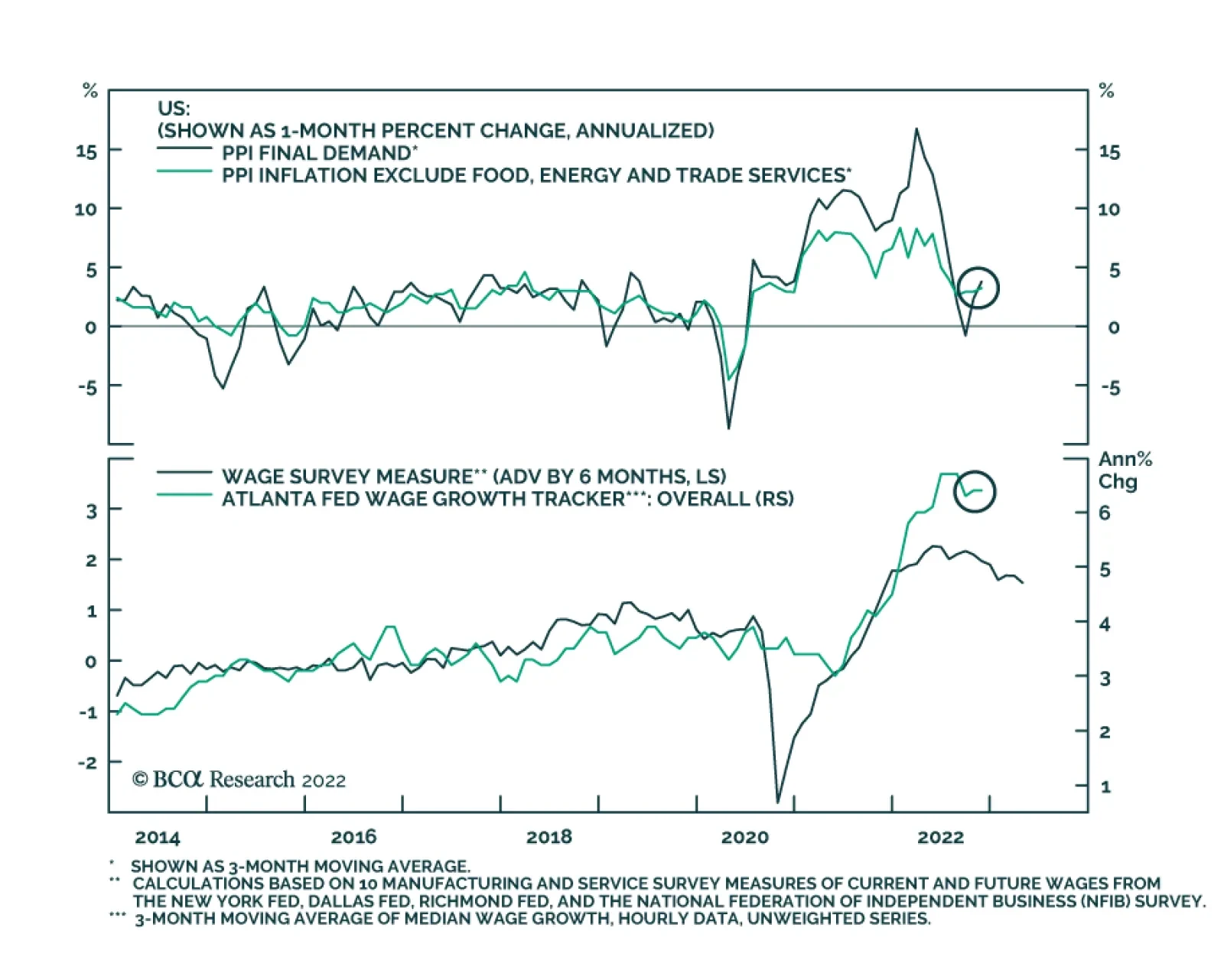

Investors were heartened by the November CPI report, but the Fed said not so fast. Although it snuffed out the latest mini-rally, ongoing disinflation will set the stage for another one early next year.

Both the US and China have structural imbalances that need correcting. The former has a structurally imbalanced labour market in which demand far outstrips supply. The latter has a massively overvalued housing market. The concurrent correction of these two structural imbalances in the world’s two largest economies will necessitate a sharp slowdown in global growth, and leads to several investment conclusions.

We explore the eight major themes that will define economic and market trends for Europe next year.

Prefer government bonds over stocks, defensive sectors over cyclicals, and large caps over small caps. Favor North America over other markets. Favor emerging markets like Southeast Asia and Latin America over Greater China, Turkey, and emerging Europe. Stick with aerospace/defense stocks.

Prefer government bonds over stocks, defensive sectors over cyclicals, and large caps over small caps. Favor North America over other markets. Favor emerging markets like Southeast Asia and Latin America over Greater China, Turkey, and emerging Europe. Stick with aerospace/defense stocks.

The pandemic gave older Americans and Brits a massive carrot and stick to retire early. The carrot being a surge in wealth, the stick being a risk to health. In other major economies, the carrots and sticks were smaller or non-existent. Hence, the shortage of older workers, and the resulting wage inflation, is a specific US and UK problem. We go through the important economic and investment implications for 2023.

Investors should maintain a conservative and defensive strategy until recession risks are clearly reduced.

European inflation will decline through 2023, which will greatly help households and consumption. But can European inflation remain low after that?