Inflation

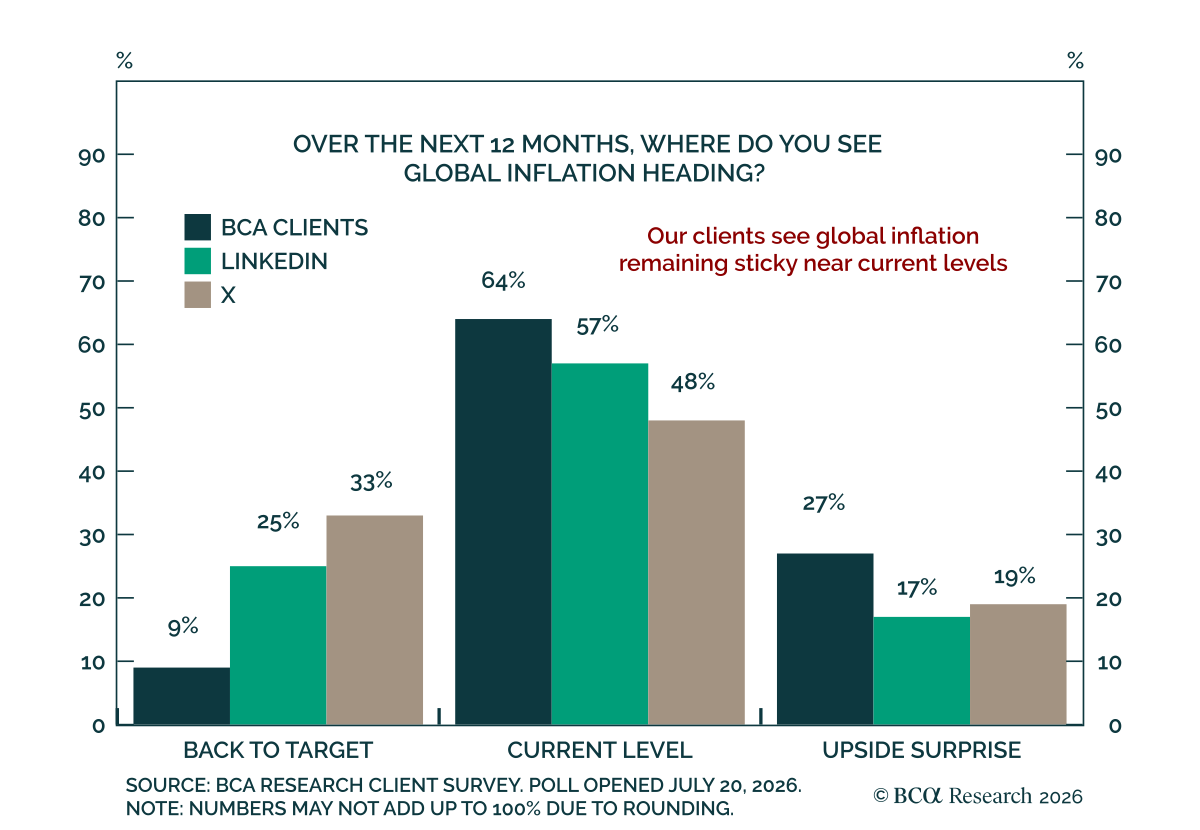

Our clients expect sticky inflation to persist. Last week’s client poll saw a clear majority expecting inflation to stay sticky near current levels over the next 12 months. The conclusions were similar across clients and social media respondents. The…

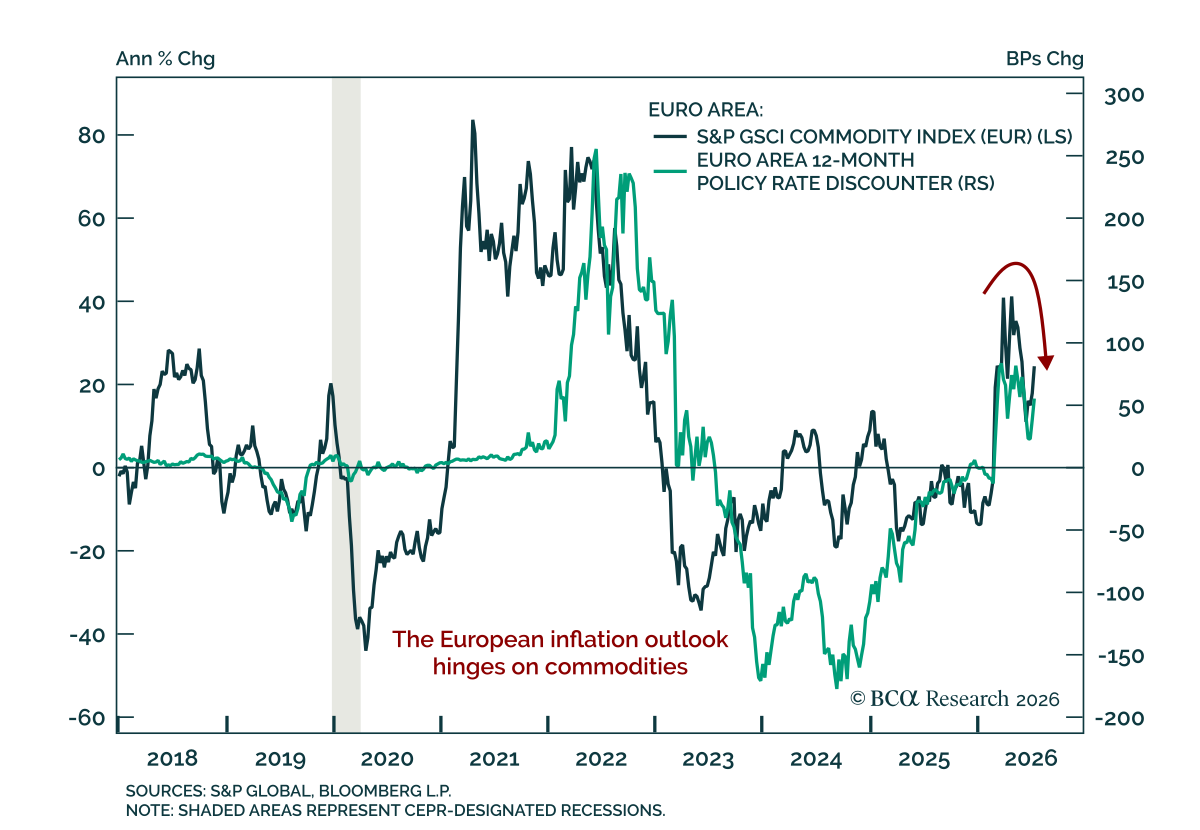

The ECB held rates at 2.25%, but kept the door open to further tightening in a near-term outlook still heavily shaped by energy prices. The hold was expected, but the ECB also signaled that every meeting remains upside risks to inflation, especially as the…

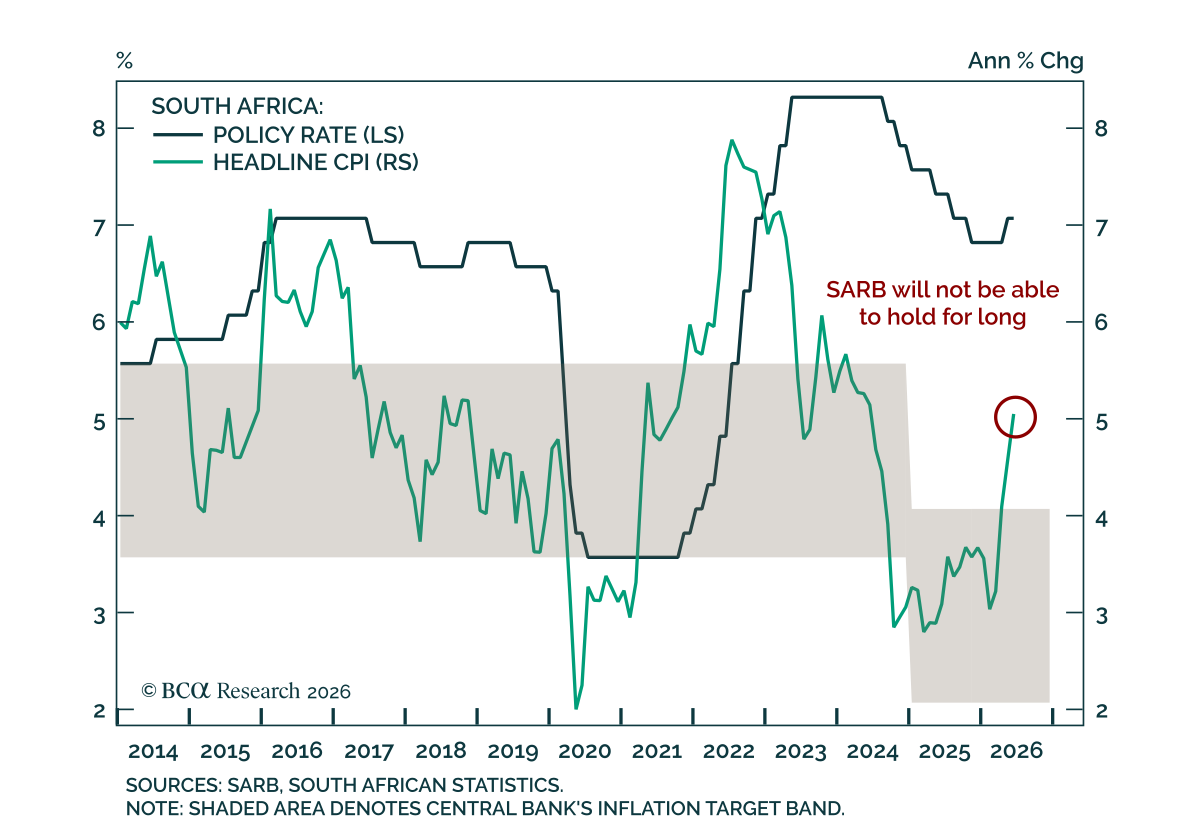

The South African Reserve Bank will not be able to hold rates for long. The SARB held its policy rate at 7%, defying expectations for a 25 bps hike. With inflation reaccelerating above the target band, our Emerging Markets strategists believe policymakers…

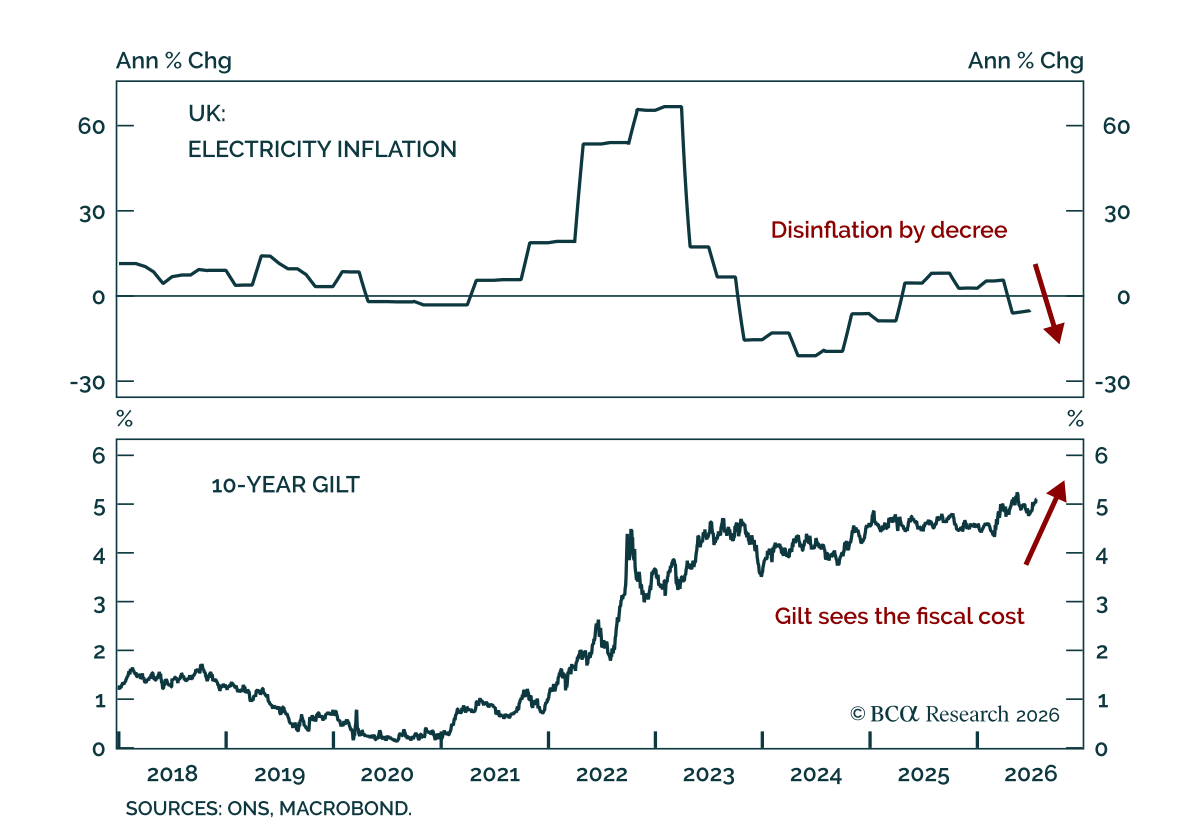

The UK’s latest cost of living relief may lower measured inflation, but it risks worsening concerns about fiscal credibility. June CPI was cooler than expected, falling to a 15-month low at 2.6%. Yet, this is not a clean disinflation story. UK inflation has…

Our FICC strategists stay overweight global inflation-linked bonds (ILBs), betting that markets underprice the inflation risk from energy and shipping disruptions. Within this stance, our colleagues view US and UK ILBs as particularly attractive relative to…

In this Strategy Insight, we assess how Middle East-related energy and shipping disruptions are shaping the global inflation outlook and review the implications for inflation-linked bond markets. We also examine the outlook for core inflation and the resulting implications for central bank policy and duration positioning.

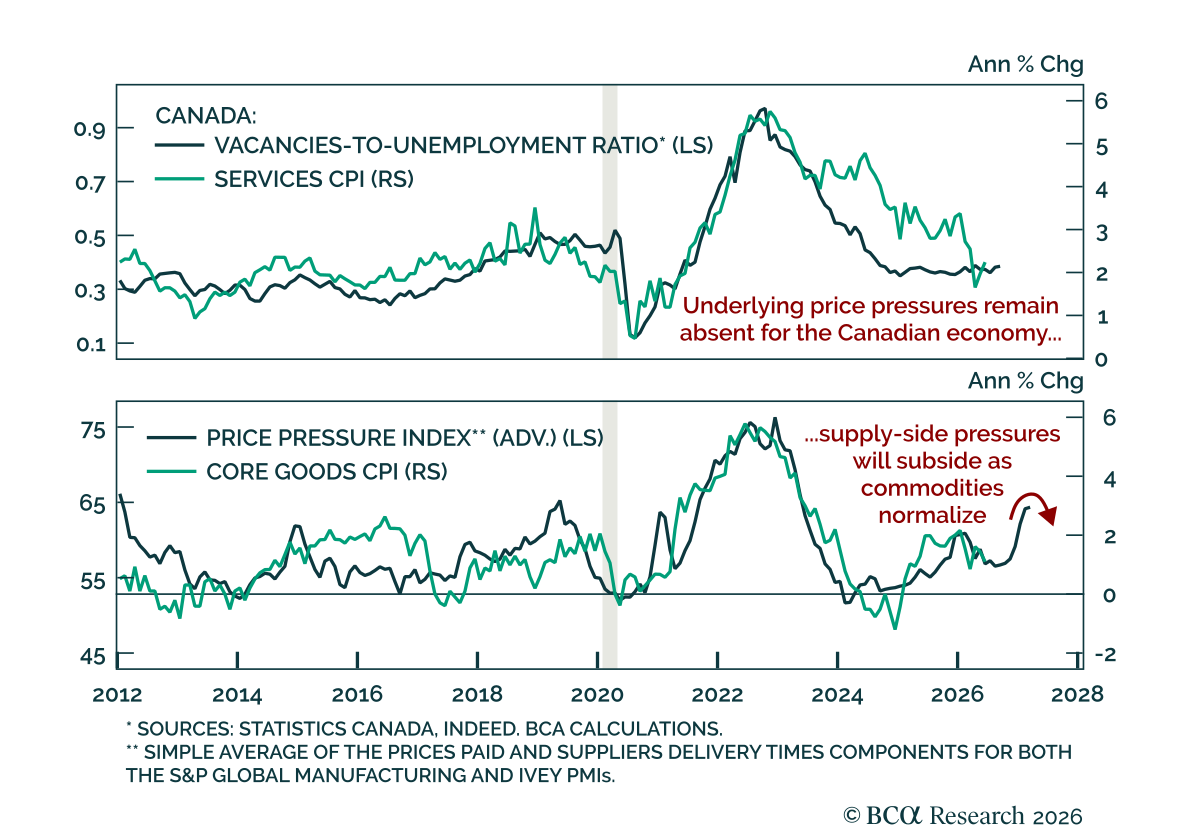

Canadian June inflation came in colder than estimates, reinforcing the case for fading CORRA pricing. Headline CPI ticked down to 2.8% y/y, within the Bank of Canada’s 1%-to-3% target range. The BoC’s preferred core measures also cooled, with median down to…

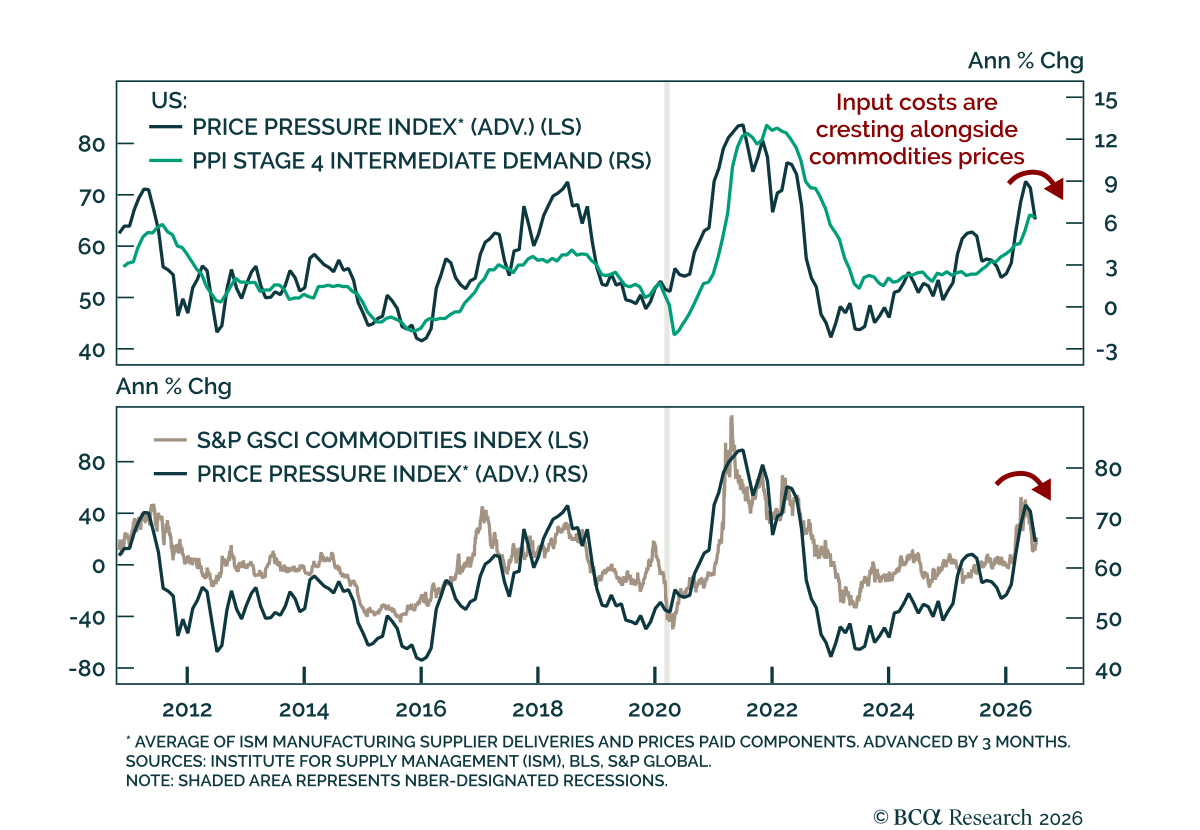

The June PPI report came in cooler than estimates, reinforcing the view that pipeline inflation pressures are easing and the Fed can stay on hold for now. Headline PPI contracted 0.3% m/m, lowering the annual rate to 5.5% y/y from 6.5%. The core measure,…

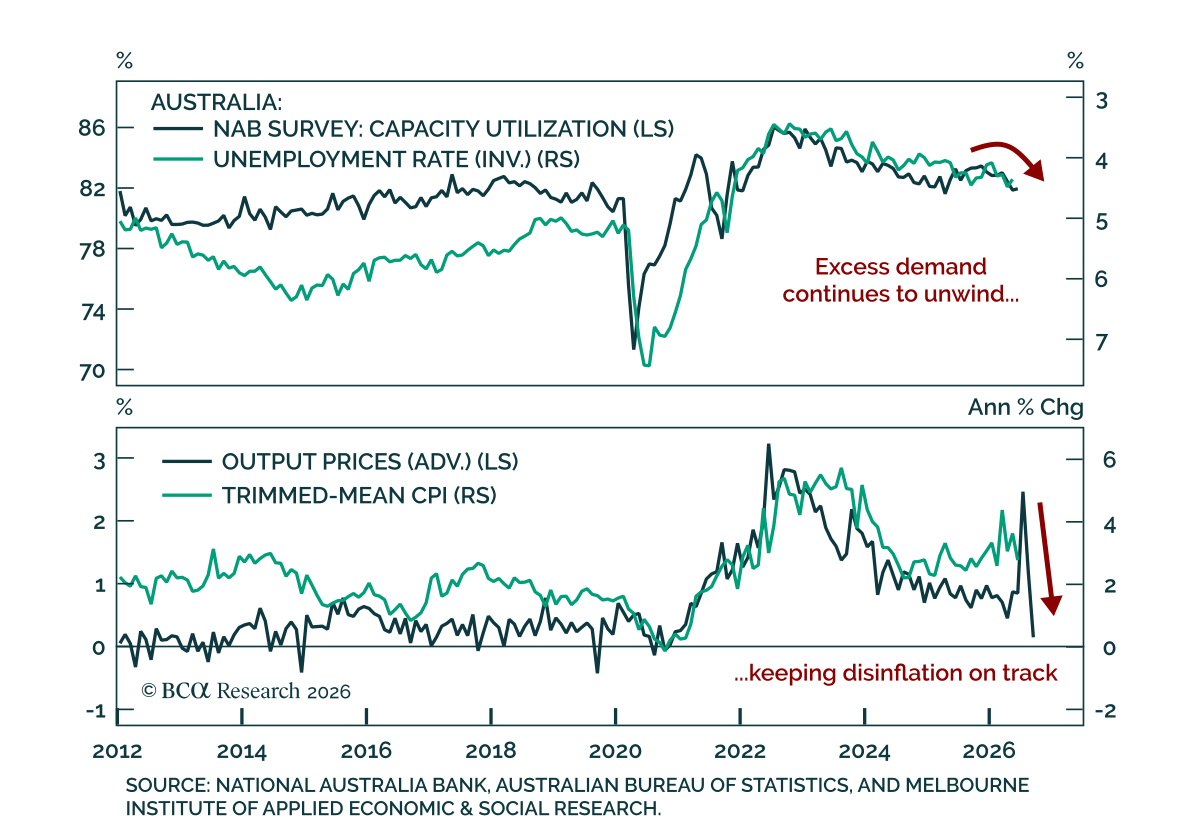

Australia's June NAB Business Survey points to a cooling economy, reinforcing the case for an extended RBA pause. Business conditions held at +3 for a third consecutive month, while business confidence, the more forward-looking measure, rebounded from -14 to…

The June US CPI report was cooler than expected, reinforcing the case for the Fed to stay on hold in July. Headline CPI contracted 0.4% m/m, the first monthly decline since June 2024 and the most severe since April 2020, cooling the annual rate to 3.5% y/y…