Gov Sovereigns/Treasurys

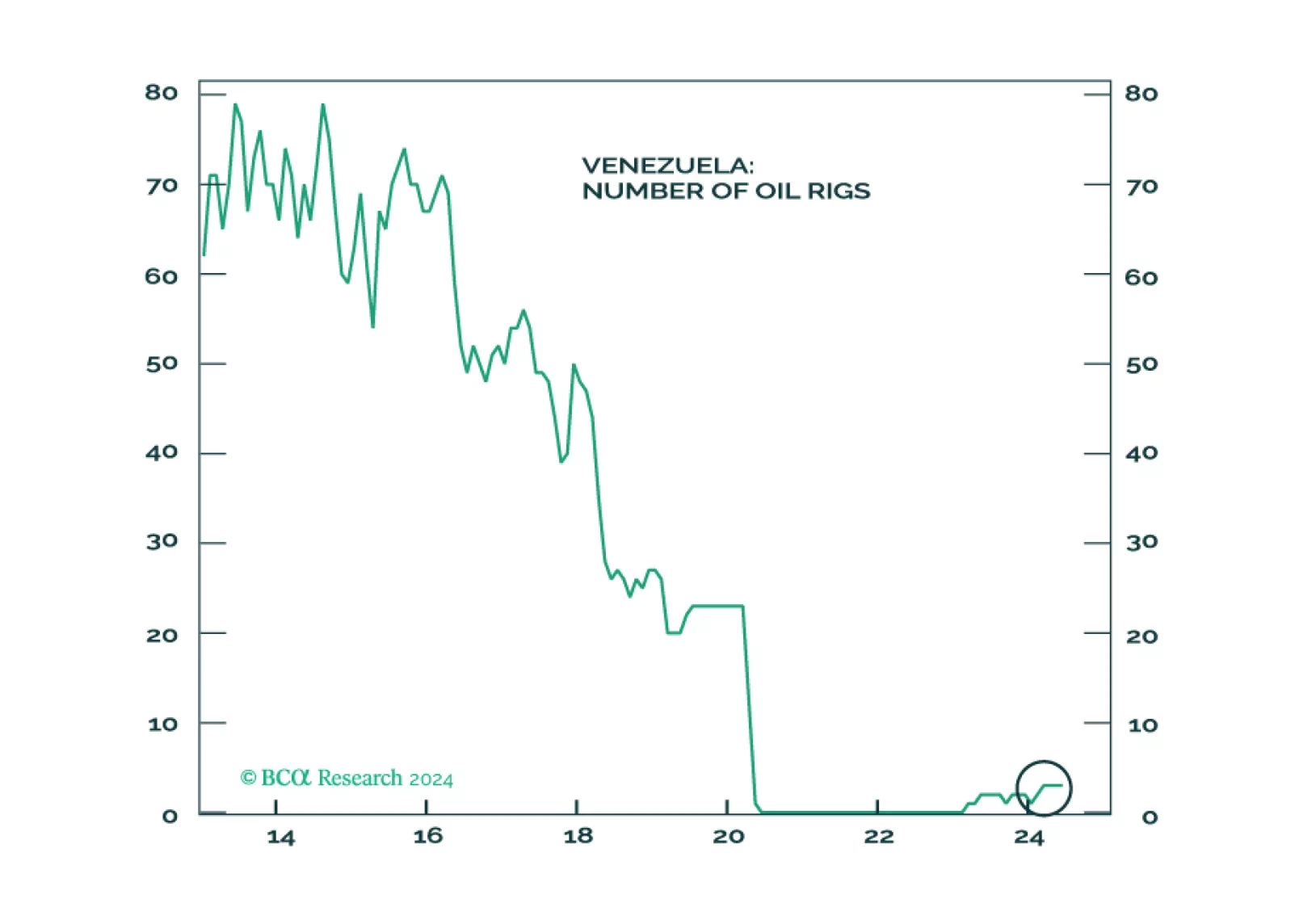

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.

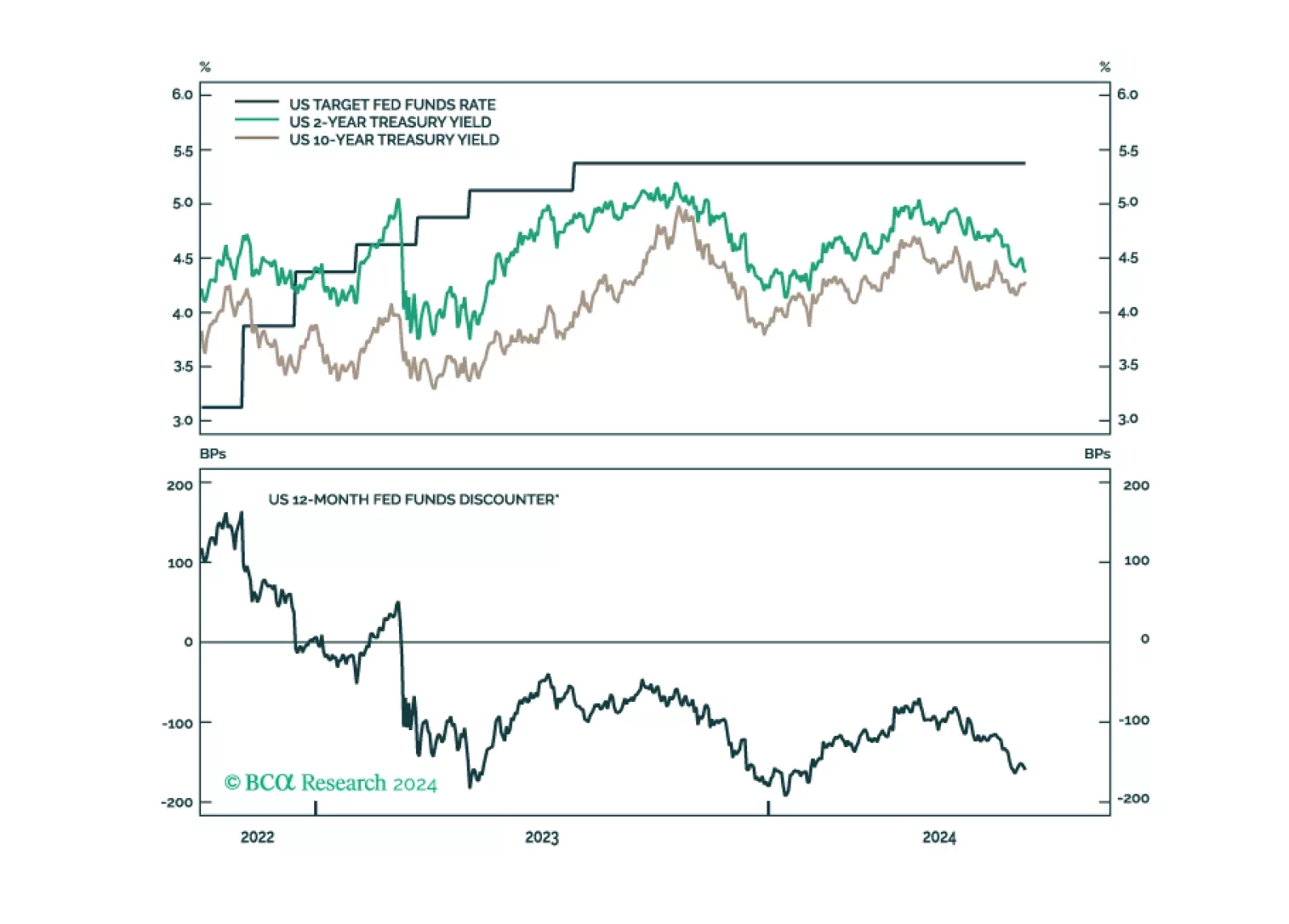

After this morning’s jobless claims number, we have now seen enough deterioration in our preferred labor market indicators to increase portfolio duration from “at benchmark” to “above benchmark”.

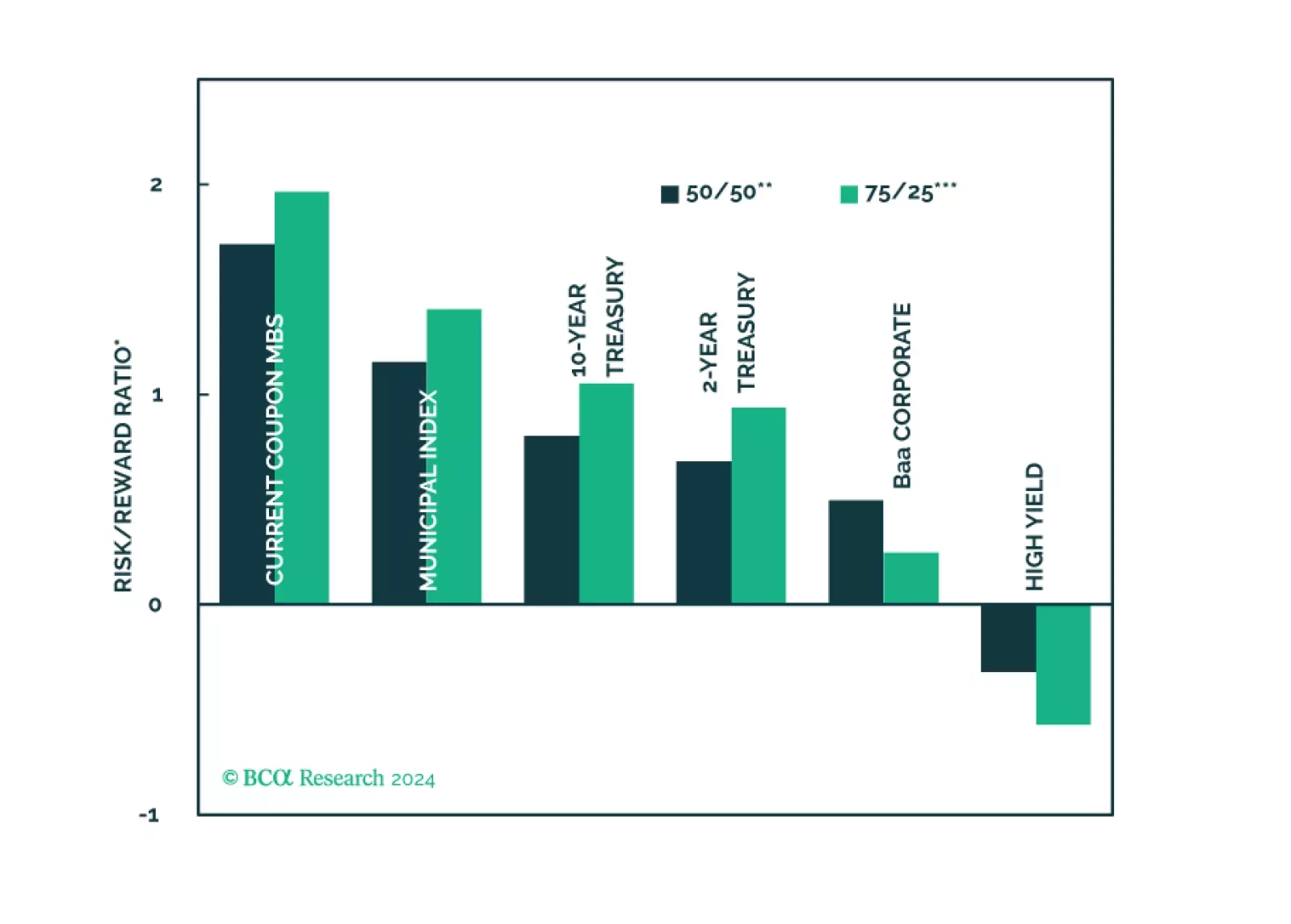

We calculate expected returns for several different US fixed income sectors with a focus on how municipal bonds stack up against the investment alternatives.

Don't buy the dip. The equity bull market is over. The US will enter a recession in late 2024 or in early 2025.

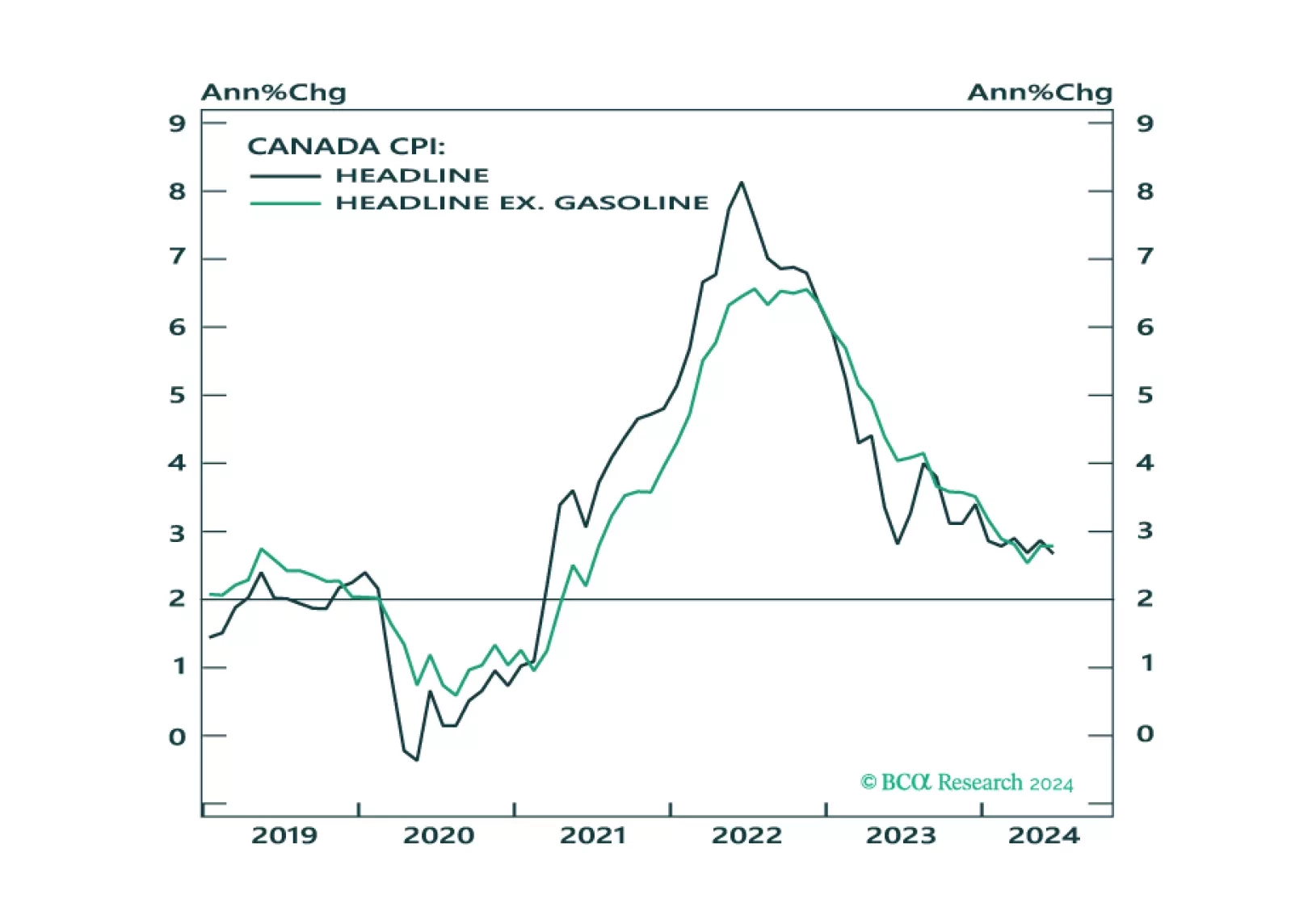

In this Insight, we look into the recent CPI release in Canada, and the possible implications for fixed-income market trades.

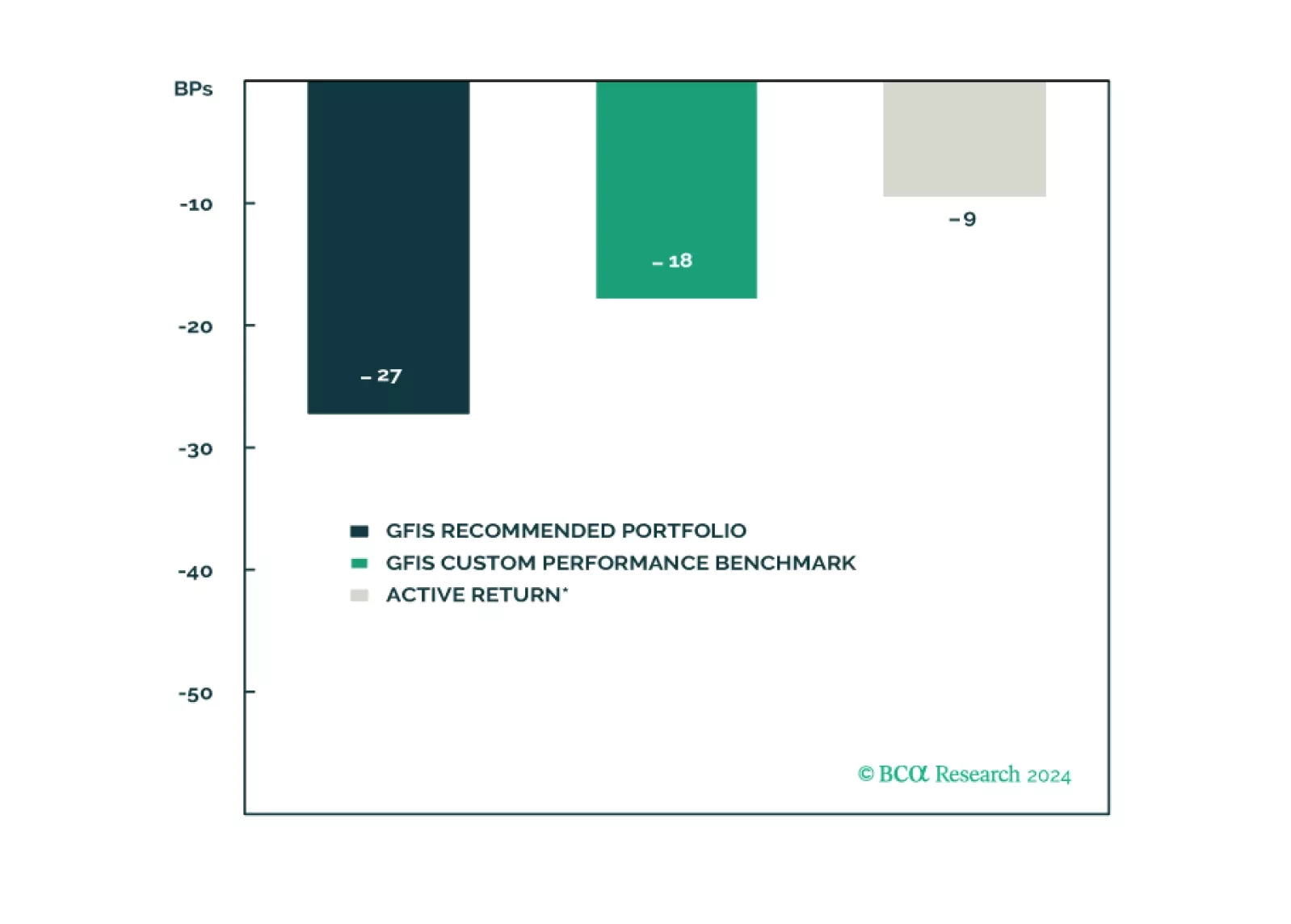

In this report, we present the quarterly review of our Model Bond Portfolio. Rebounding growth and political instability led to slightly negative portfolio performance in Q2/2024. As global growth starts to moderate, we continue to favor government bonds over credit. Maintain a defensive portfolio stance.

US dollar liquidity has been shrinking, which has important ramifications for global asset prices, including currencies. In this report, we delve into the process of dollar liquidity creation and the outlook for currencies over the next six-to-twelve months.

The conventional wisdom is wrong: Trump is not going to substantially cut taxes once in office; he is going to raise taxes by jacking up tariffs. To the extent that this dampens economic activity, it is bad news for stocks but good news for bonds.

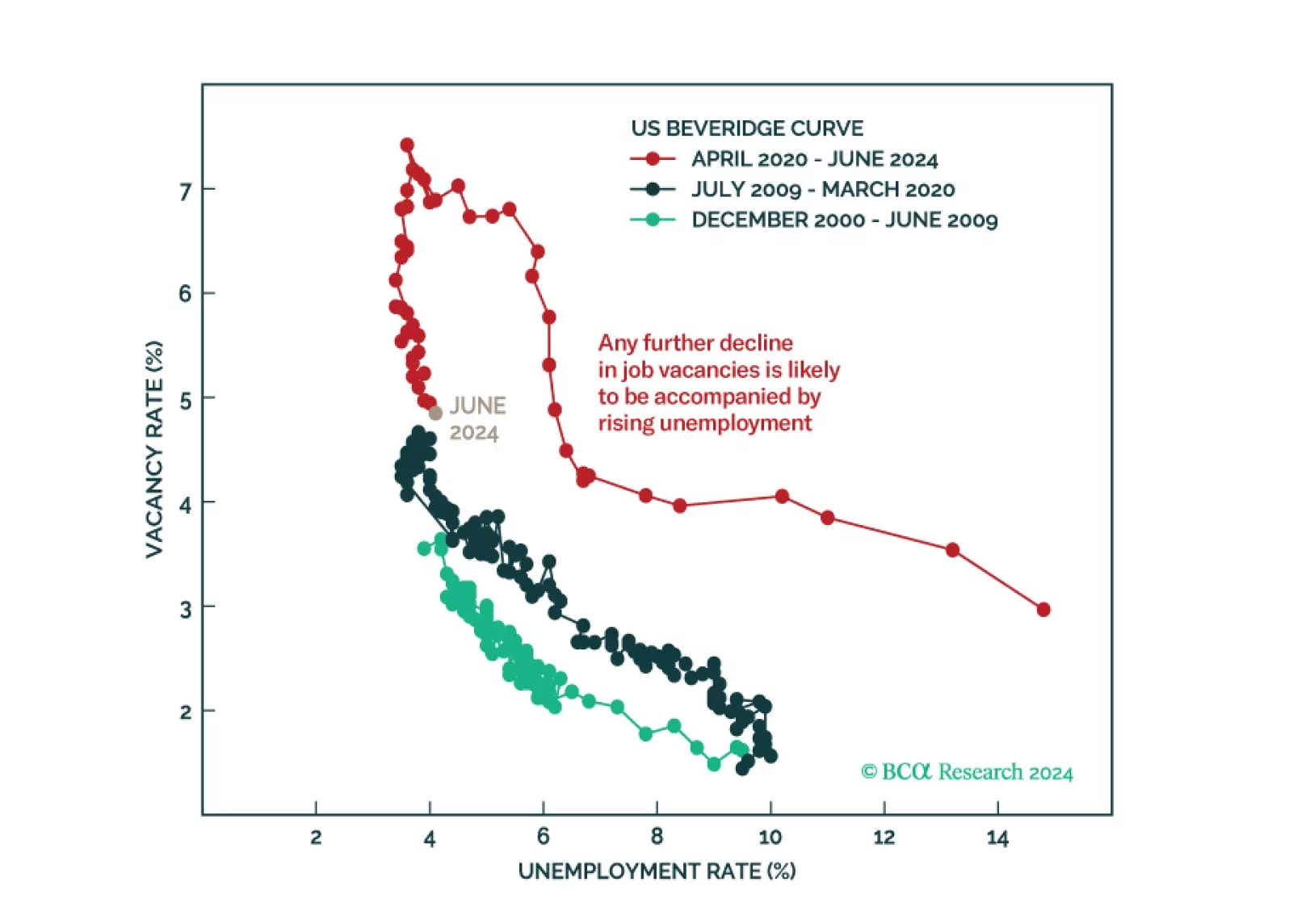

Our labor market indicators have softened meaningfully during the past month but aren’t yet signaling an imminent recession. That said, the Fed can no longer ignore the labor market with the unemployment rate above 4% and rising.

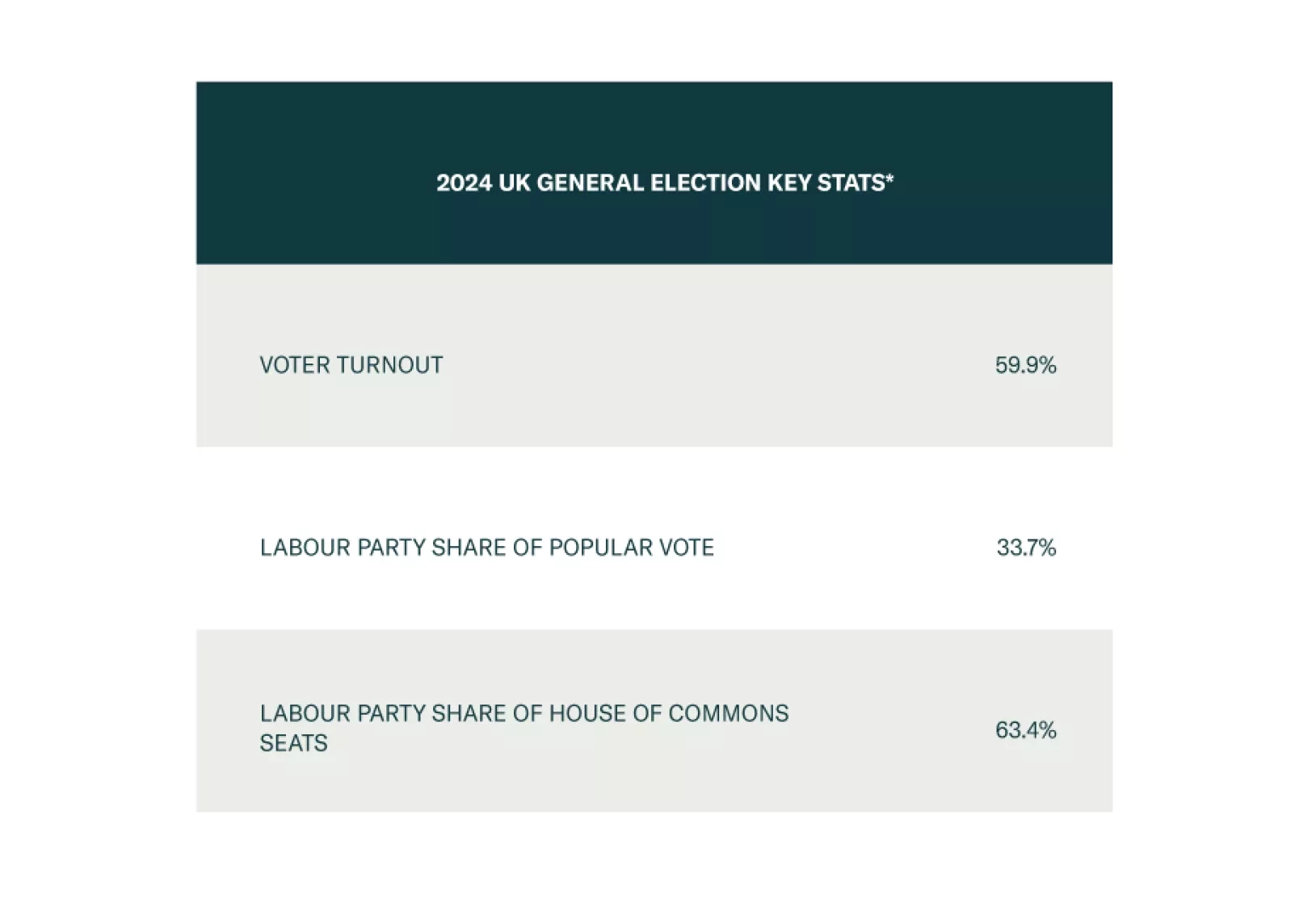

The new Labour government will have flexibility to respond to macro shocks, which is positive for the UK in general, namely GBP-EUR, and also gilts in absolute terms. But over the long run, tax hikes will likely surprise to the upside, which poses a risk to corporate earnings.