Geopolitics

One clear way for President Trump to achieve a policy victory and a boost to the economy would be to agree to a trade deal with China. Just as he raised the tariffs unilaterally, he can roll them back unilaterally to encourage the financial markets and CEO…

President Trump is a uniquely commercial president. He did not become president through experience in military or government, but because he was a bold businessman who claimed he could negotiate better deals for the United States. So he is even more…

Highlights China’s trade strategy toward the U.S. is not greatly affected by the early U.S. Democratic Party primary election. The sea change in American policy toward China began before Donald Trump and is grounded in U.S. grand strategy. Yet Trump is staging a tactical retreat in his trade war and China is reciprocating, suggesting that Beijing would rather avoid a “lame duck” Trump on the warpath. Beijing will not implement structural changes that would vindicate Trump’s negotiating strategy and set a precedent that is harmful to China’s national interests in the long run. Feature A U.S.-China trade ceasefire is in the works, based on the outcome of the latest high-level talks in Washington. President Trump, paying a surprise visit to the top Chinese negotiator, Vice Premier Liu He, agreed to pause the October 15 tariff hike in exchange for assurances that China would buy $40-$50 billion worth of agricultural goods to ease the economic pressure on Trump’s political base. Trump is now confirmed to attend the Asia Pacific Economic Cooperation summit in Santiago, Chile on November 16-17, where he hopes to cement this “phase one deal” with Chinese President Xi Jinping. Chart 1Global Policy Uncertainty To Fall

Global Policy Uncertainty To Fall

Global Policy Uncertainty To Fall

Our market-based GeoRisk Indicator for Taiwan island – which calculates Taiwanese political risk based on any excessive deviation of the Taiwanese dollar from economic fundamentals – is a good proxy for Sino-American trade tensions due to Taiwan’s high level of exposure to China and the United States. At the moment it is signaling a sharp drop in tensions. We expect global uncertainty to follow over the coming month as Trump and Xi agree to some kind of ceasefire (Chart 1). Our Taiwan risk measure tracks closely with the Global Economic Policy Uncertainty Index, which measures risk via the word count of key terms in influential global newspapers, because Taiwan is highly exposed to the world economy and trade. Taiwan is also uniquely vulnerable to the biggest source of global policy uncertainty today: the Sino-American trade war. Not only are U.S.-China relations slightly thawing, but also the risk of the U.K. leaving the EU without a withdrawal agreement has collapsed. This will reinforce Europe’s underlying political stability despite the manufacturing recession and help create a drop in global uncertainty (Chart 2). Chart 2American Policy Uncertainty To Buck The Trend

American Policy Uncertainty To Buck The Trend

American Policy Uncertainty To Buck The Trend

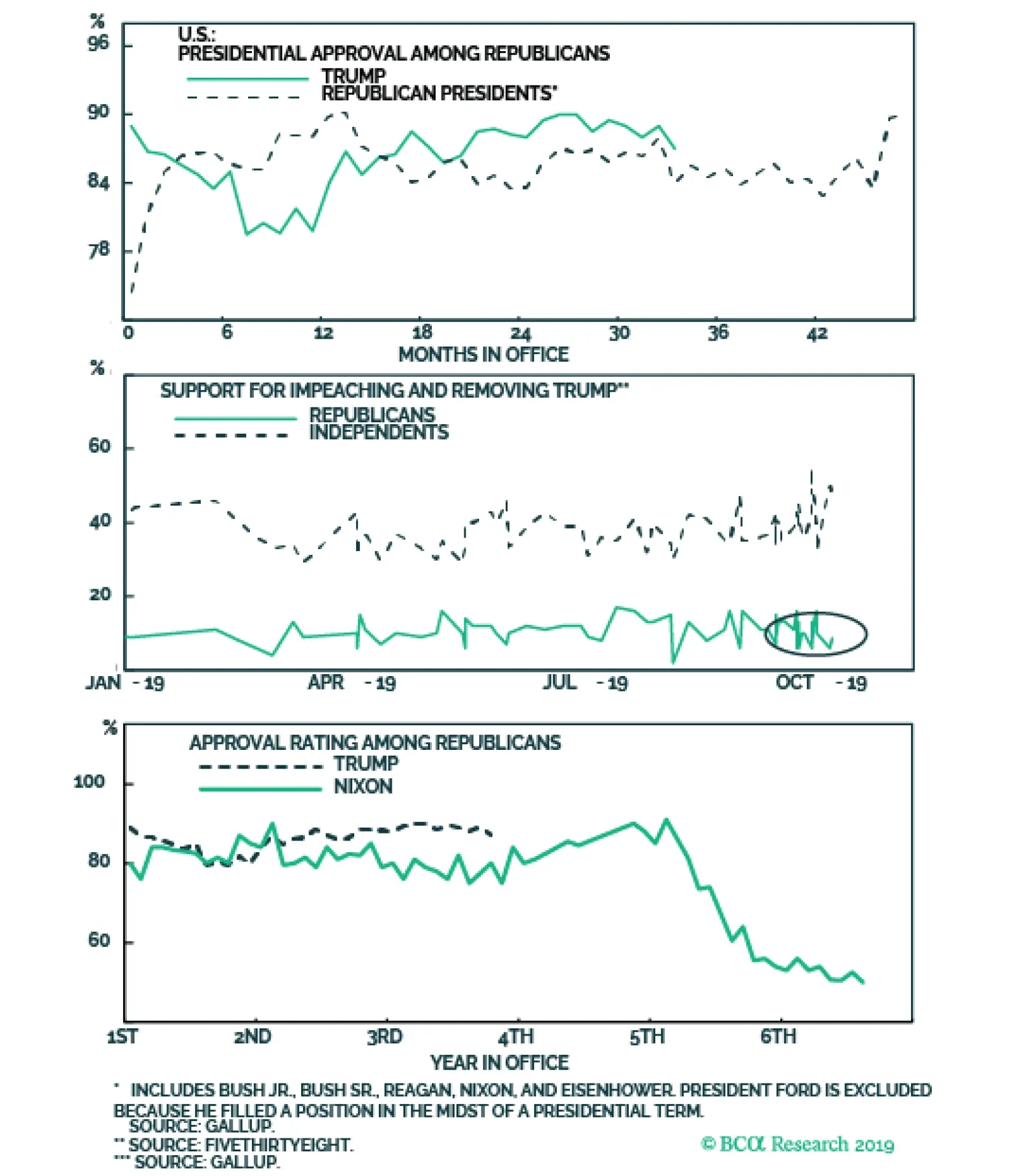

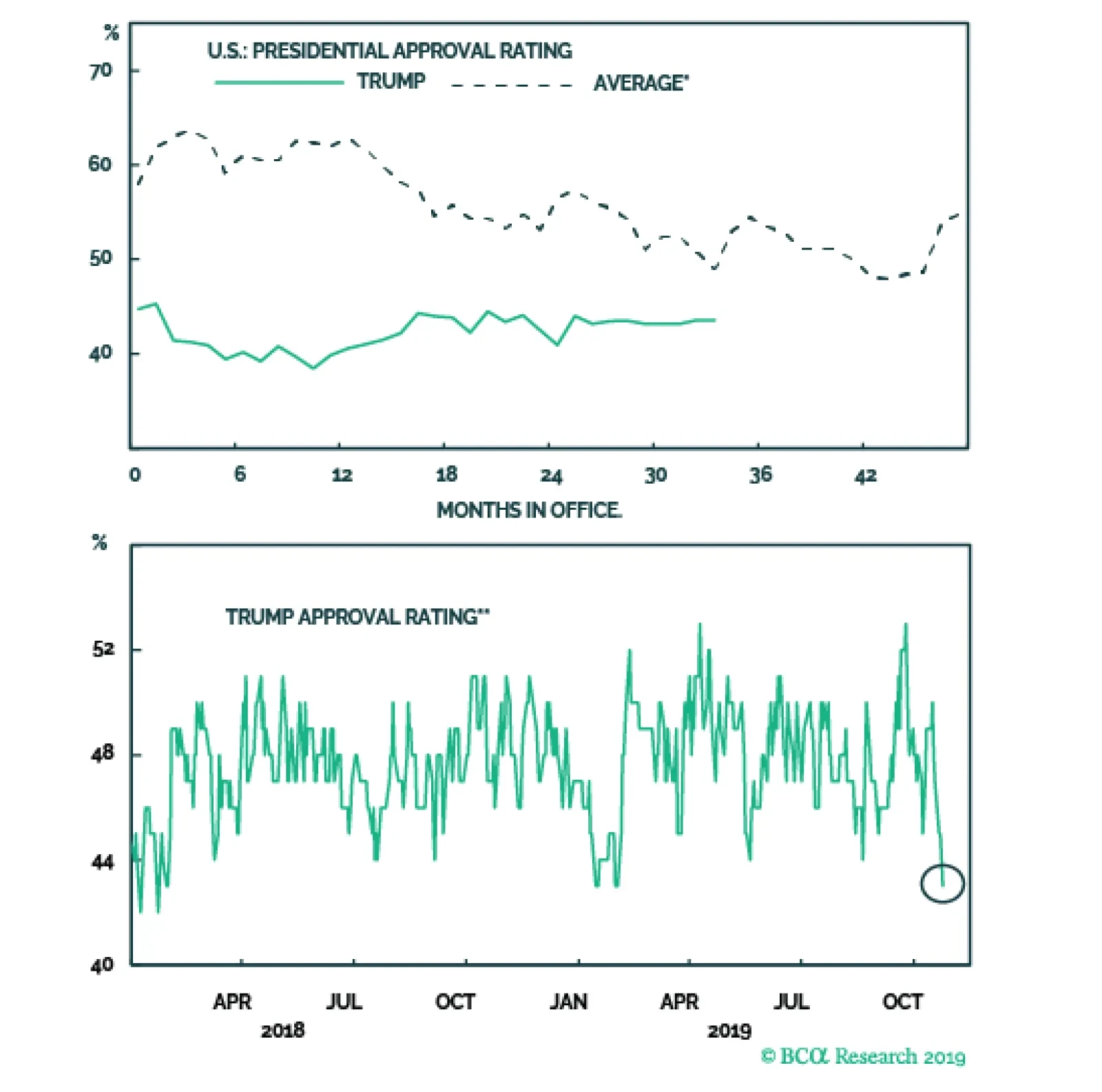

Uncertainty will remain elevated beyond the fourth quarter, however, for two main reasons. First, U.S. uncertainty will rise, not fall, as a result of the impending 2020 election. Second, the trade ceasefire is highly unlikely to resolve the slate of disagreements and underlying strategic distrust plaguing U.S.-China relations. This will cap the rebound we expect in global business sentiment. How can we be so sure that the U.S. and China will not strike a historic deal? We answer this question in this report, with particular reference to an important corollary question that has emerged in numerous client meetings: wouldn’t China rather deal with the “transactional” Trump than an “ideological” President Elizabeth Warren? Trump Is Not A “Lame Duck” Yet, Hence The Ceasefire President Trump is a uniquely commercial president. He did not become president through experience in military or government, but because he was a bold businessman who claimed he could negotiate better deals for the United States, including on immigration and trade. So he is even more vulnerable to an economic downturn than the average U.S. president. Industrial production, manufacturing, and core capital goods new orders are contracting, and sentiment is souring among both business leaders and average consumers (Chart 3). Trump faces a distinct risk that the manufacturing slowdown and psychological effects will morph into a general slowdown. Even if not outrightly recessionary, a generalized slowdown in the U.S. economy could easily lead to rising unemployment during the election year, which would all but ensure Trump’s loss of the White House. The degree of correlation between presidential approval and the unemployment rate fluctuates over time, but our survey of post-World War II presidents shows that the unemployment rate is the best indicator of the direction the approval rating will ultimately go by the end of the term in office. While Trump’s approval is highly correlated with unemployment, it is also very low – resembling President Obama’s at this point in his first term. Yet that was in the aftermath of the Great Recession, and Trump’s approval is declining as a result of the impeachment inquiry into his alleged attempt to convince Ukraine to interfere in the 2020 election in his favor. And his approval is low despite an incredibly low rate of unemployment, at 3.5%, that can hardly get better (Chart 4). Chart 3Trump Needs A Sentiment Boost For 2020

Trump Needs A Sentiment Boost For 2020

Trump Needs A Sentiment Boost For 2020

Chart 4Rising Unemployment Would Doom Trump 2020

Rising Unemployment Would Doom Trump 2020

Rising Unemployment Would Doom Trump 2020

In short, Trump has very little wiggle room. To be reelected he must not only keep unemployment from rising much, but also achieve some other policy wins in order to draw closer to the average approval rate among post-World War II presidents (top panel, Chart 5). Even the Republican-friendly pollster Rasmussen shows that Trump’s general approval is dangerously eroding (bottom panel, Chart 5). One way Trump can achieve a political and economic victory would be to agree to a trade deal with China.

Chart 5

One clear way to achieve a policy victory and a boost to the economy would be to agree to a trade deal with China. Passing the U.S.-Mexico-Canada Agreement through Congress is out of his control. Policy toward China, by contrast, is entirely within his control. Just as he raised the tariffs unilaterally, so he can roll them back unilaterally to encourage the financial markets and CEO confidence – as long as talks are making progress. The downside of this argument is that if Trump becomes a “lame duck,” with a falling economy and/or approval rating virtually ensuring that he cannot get reelected, he is no longer constrained by financial markets or the economy. He would have an incentive to initiate “Cold War 2.0” with China right here and now – or some other foreign conflict – and encourage Americans to rally around the flag amid a historic confrontation with a foreign enemy. This is a huge risk to the 2020 outlook, but it runs afoul of the economic constraint, so we expect Trump to try the “Art of the Deal” one last time. What about impeachment? When the House of Representatives brings formal impeachment articles against Trump, the Senate will hold the trial. Republicans have a 53-47 majority in the Senate, requiring 20 to defect against the president to generate the 67 votes needed to make him the first president in U.S. history to be removed from office in this way. A total of 16 senators hail from states that Trump won by less than 10% in the 2016 election – so 20 defectors is a strong political constraint.

Chart 6

Unless, of course, grassroots Republican support for Trump collapses. Right now it is falling but in line with the average (top panel, Chart 6). Republicans are not warming to the idea of impeachment and removal from office (middle panel, Chart 6). We will reassess the risk of removal if Trump’s intra-party approval heads further south and begins to look like Richard Nixon’s (bottom panel, Chart 6). Bear in mind that the election is one year away – it is easier for Republicans to kick the decision over to voters than to remove one of their own from the Oval Office. A scandal big enough to prompt an exodus of Republican support will doom any chances of Republicans retaining the White House through Vice President Mike Pence or other candidates. Bottom Line: Trump’s approval rating is in dangerously low territory but he is not yet a “lame duck” freed from the shackles of political and economic constraints. He still has a shot at extending the business cycle and saving his election campaign. This is driving him to retreat from tariffs and pursue a trade ceasefire with China. The result should be a decline in global policy uncertainty in Q4. However, this decline will not last long, as American uncertainty will skyrocket during the election year and U.S.-China tensions will reemerge once the economic constraint has been reduced. China Will Accept A Ceasefire In a special report in these pages in August, we raised a critical question: if Trump is forced to retreat from his trade war, will President Xi Jinping reciprocate? Or will he refuse to bargain, leaving Trump overextended to suffer the negative economic repercussions of the trade war without the political benefit of striking a new deal? We now have our answer, at least for the near term. China resumed negotiations in October and has confirmed that progress was made. Beijing is continuing to offer some accommodation of U.S. demands in both domestic and foreign policy (e.g. financial sector opening, enforcement of sanctions on Iran). In Hong Kong SAR, not only has Beijing avoided a violent intervention and suppression of civilian protesters, but there are rumors that Chief Executive Carrie Lam is on the way out by March (which we find highly plausible). There are still plenty of risks across the broad range of U.S.-China disputes, but from the past month’s developments we can infer that President Xi is not going on the offensive in order to destroy Trump’s latest “deal-making” bid. How far will Xi go to accommodate Trump? Not so far as to implement major structural concessions. And this will limit the positive impact of the deal. Xi does not face an electoral constraint, or the loss of office (having removed term limits), nor does he face a domestic political constraint on a 12-month time frame (the twentieth national party congress is not until 2022). Economically China is much more vulnerable – this is a valid constraint. But tariffs do not force Beijing to make major structural concessions and implement them rapidly, certainly not on Trump’s time frame. The economy is slowing but not plummeting (Chart 7). China does not face conditions like 2015-16 and policymakers have decided it is best to save ammunition in case they need to use “bazooka” stimulus later. Chart 7China's Economy Holding Up

China's Economy Holding Up

China's Economy Holding Up

Chart 8China Not Reflating Property Bubble (Yet)

China Not Reflating Property Bubble (Yet)

China Not Reflating Property Bubble (Yet)

The fact that Beijing has maintained restrictions on the property sector and not allowed reflation to fuel the property bubble (Chart 8) underscores the current policy disposition: some parts of the economy need to be shored up but there is no need to panic. When it comes to tariffs, China ultimately has the option of depreciating the currency to offset the impact. The fact that the CNY-USD exchange rate has not fallen as far as the headline tariff numbers suggest it should fall indicates that Beijing is still maintaining a negotiation rather than letting the currency absorb the full impact (Chart 9). Chart 9China Can Depreciate To Offset Tariffs

China Can Depreciate To Offset Tariffs

China Can Depreciate To Offset Tariffs

Since China is still capable of “irrigation-style” fiscal stimulus, the economic constraint can be mitigated further. Beijing can continue to fight if Trump returns to the offensive. Hence we do not expect major new trade concessions beyond what is already on the table – and many of the current offerings consist of promises more so than concrete actions (Table 1).

Chart

Chart 10Beijing Throws Trump A Bone

Beijing Throws Trump A Bone

Beijing Throws Trump A Bone

We do expect China to try to avoid the worst-case scenario, since it would be destabilizing for China’s medium and long-term economy and single-party rule. Stimulus will increase as necessary to ensure that growth rebounds as Beijing seeks to improve the job market and manufacturing sector. And this also supports the logic for agreeing to a ceasefire with Trump. That China is reciprocating is apparent from the U.S.’s rebounding market share in China’s agricultural imports (Chart 10). The relevant constraint for China is that Trump could be rendered a “lame duck” and go ballistic on China, activating the full slate of threats – from high-tech export controls, to banking sanctions, to capital controls. The U.S. is still the more powerful nation in absolute terms, with enormous financial, economic, military, and technological leverage over China. Beijing also sees the danger in deliberately thwarting Trump only to have him somehow win reelection. He would then have a renewed passion for punitive measures, yet he would lack the first term’s electoral constraints. Hence there is a clear basis for President Xi to accept Trump’s tactical trade retreat. Bottom Line: President Xi does not face an imminent domestic political constraint, which gives him greater leverage than President Trump. Nevertheless he does face short term economic pressures, and enough of a geopolitical and economic constraint from a full-blown escalation of tensions to accept Trump’s offer of a ceasefire. Wouldn’t China Rather Deal With Trump Than Warren? What about the upside risk? What are the chances that Xi offers additional concessions – structural concessions – in order to achieve a groundbreaking deal with the American president? A grand compromise will not occur. Republicans and Communist Party leaders have a history of such deals, which pave the way for a new multi-year stint of deepening bilateral economic engagement. We have a high conviction view that such a grand compromise will not occur. But could the U.S. 2020 election change China’s calculus? In particular, wouldn’t China prefer to deal with Trump than Senator Elizabeth Warren? More and more investors are asking this last question as the early U.S. Democratic Party primary election heats up. Warren is a democratic progressive who aims to revolutionize U.S. trade policy to promote human rights, organized labor, and strict environmental standards. She is seen as more “ideological,” whereas Trump is more “transactional” – i.e. willing to make business tradeoffs while staying away from sensitive issues affecting China’s internal affairs. Moreover Trump is a known quantity, whereas Warren would represent an unknown – a progressive populist as president and another revolution in U.S. policy, reducing predictability for Beijing. Our assessment is that the U.S. election process is too early and too uncertain to serve as a driver of Beijing’s trade negotiating strategy over the fourth quarter. Moreover there is not a clear basis for China to favor Trump to Warren. Chart 11Trade Dispute Precedes Trump

Trade Dispute Precedes Trump

Trade Dispute Precedes Trump

There are three major trends to bear in mind: The sea change in U.S. policy toward China began under the Obama administration. President Obama entered office by slapping tire tariffs on Beijing. He endorsed Congress’s “Buy American” provisions in the fiscal stimulus package to fight the Great Recession. Under his administration, the U.S. effectively capped steel imports from China (Chart 11). The Obama administration orchestrated the “Pivot to Asia,” a diplomatic and military initiative to rebalance U.S. strategic commitment to focus on China and the western Pacific more than the Middle East. This included the Trans-Pacific Partnership (TPP), an advanced trade deal that deliberately excluded China. It eventually also included a robust reassertion of U.S. maritime supremacy via bulked up Freedom of Navigation Operations (FONOPs) in the South China Sea, a critical global sea lane where Beijing had become increasingly assertive (Diagram 1).

Chart

Chart 12U.S.-China THAAD Dispute Under Obama

U.S.-China THAAD Dispute Under Obama

U.S.-China THAAD Dispute Under Obama

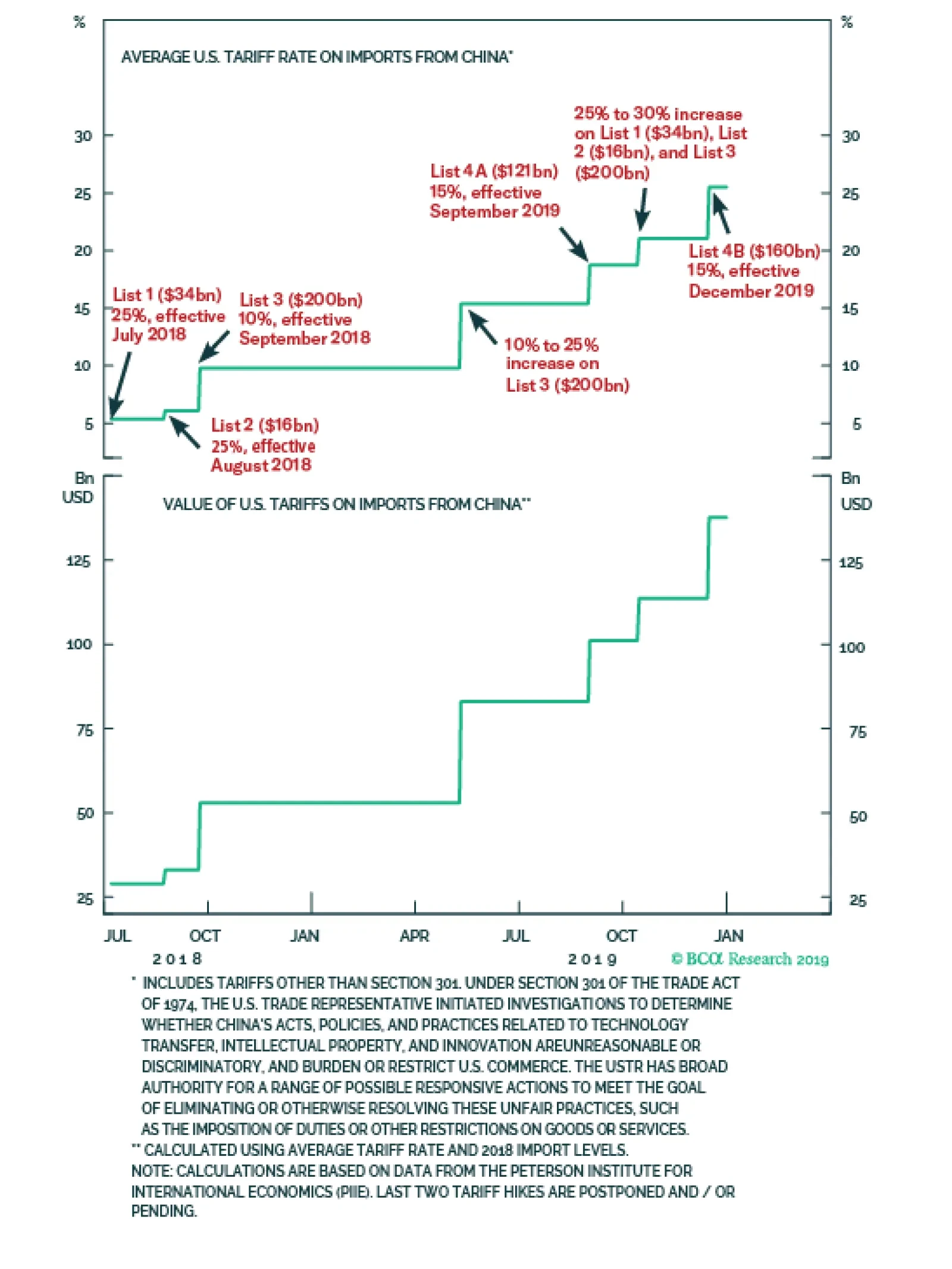

The Obama administration’s attempt to install the Terminal High Altitude Area Defense (THAAD) missile defense system in South Korea caused a strategic showdown with China, emblematized by Chinese sanctions against the Korean economy (Chart 12). Obama’s one major policy handover to President Trump was to focus attention on North Korea’s advancing nuclear weaponization and missile capabilities – another source of friction with China. There can be little doubt that if the Democrats win the 2020 election, they will return to some or all of these policies. But this says more about U.S. national policy than it does about which political party China should favor in 2020, because … 2. The Trump administration is unpredictable and disruptive to both the global status quo and China’s economy. President Trump’s significance is that he shifted the Republican Party from its traditional pro-corporate, pro-free trade, pro-China orientation to a more populist, protectionist, and China-bashing approach. He stole the thunder of protectionist Democrats in the manufacturing heartland. He continued the pivot to Asia, albeit by another name (a “free and open Indo-Pacific”). This approach emphasized coercive unilateral “hard power” rather than multilateral “soft power” and resulted in a negative impact on China’s economy. This change, while it has pros and cons, demonstrates that a harder line on China has policy consensus across administrations. Few doubt that this is the new bipartisan consensus in Washington. Trump has executed this policy shift in a way that is fundamentally unsettling and unpredictable for China: sweeping unilateral tariffs against China on national security grounds (Chart 13); sanctions on tech companies critical for China’s economic future (Chart 14); and tightening relations with Taiwan. This policy eschews traditional diplomacy, which is where China thrives, and it unsettles global supply chains, where China once enjoyed centrality. To some extent Trump is even prisoner to his own logic: as he softens policy to get a trade ceasefire, he faces challenges from Congress on everything from tech export controls to Hong Kong human rights to Chinese corporate listings on U.S. stock exchanges. The Democrats will accuse him of caving to China if he agrees to a deal. Still, if China were to grant Trump deep trade concessions, it would effectively vindicate Trump’s approach. Future American presidents could always threaten across-the-board tariffs whenever they want to extract rapid structural changes from China’s policymakers. This is an intolerable precedent to set. A hard line on China has policy consensus across U.S. administrations. Chart 13Trump's Trade Policy Highly Disruptive

Trump's Trade Policy Highly Disruptive

Trump's Trade Policy Highly Disruptive

Chart 14China's Tech Sector Under Threat

China's Tech Sector Under Threat

China's Tech Sector Under Threat

3. China cannot predict the outcome of U.S. primary or general elections. No one knows who will win the Democratic Party’s primary election. Joe Biden is the frontrunner and has clear advantages in terms of electability versus Trump. But Elizabeth Warren is gaining on him and her chief progressive rival, Senator Bernie Sanders of Vermont, is likely to continue flagging in the polls and feeding her rise due to his ill health. It is highly unlikely that Xi Jinping will make decisions regarding a ceasefire with Trump, as early as next month, based on up-and-down developments in a primary election that has not technically even begun (the first vote is in February). Once Biden or Warren have clinched the nomination, it is not clear who will win in November 2020. President Trump narrowly seized the electoral college in 2016 and the risks to his reelection are extreme, as outlined above. Yet he is the incumbent and BCA Research does not expect a recession next year, which should create a baseline case of reelection. Meanwhile Biden’s debate performances and polling are lackluster, despite being the establishment pick and front runner. Warren’s far-left ideology is a liability, although she is at least capable of beating Trump. Chinese policymakers will assess the developments, but Beijing will conduct strategy to be prepared for any outcome. Summing up the above, all that China knows for certain is that Trump is the current standard-bearer of a broader sea change in the Republican Party and Washington. The new consensus is broadly antagonistic toward China’s growing global influence. Hence China is preparing for “protracted struggle” regardless of whether Trump or a Democrat sits in the Oval Office after 2020. The logical conclusion is to continue negotiating with Trump, and offer some concessions to maintain credibility, but not to capitulate to his gunboat diplomacy. Finally, there are a two key arguments that work against the argument that China prefers Warren to Trump: Democrats will need time to build a multilateral anti-China coalition: Trump’s greatest mistake in the trade war is arguably his failure to form a “coalition of the willing” among western nations to take on China’s mercantilist trade practices together. Chart 15Trump Missed Chance To Build Grand Coalition

Trump Missed Chance To Build Grand Coalition

Trump Missed Chance To Build Grand Coalition

Such a coalition would have represented a much greater economic constraint for Chinese leaders (Chart 15), making structural concessions more likely. A future Democratic president would have better luck in galvanizing such a coalition. Thus, by favoring Trump, Beijing could perpetuate the division between “America First” and “the liberal Western order.” Yet western nations will still be reluctant to confront China and it will take years of diplomacy to build such a concerted effort. These are years in which China can improve its economic self-sufficiency and use diplomacy to undermine western cohesion. By contrast, a second-term Trump could pursue punitive measures immediately (beyond tariffs) and could also pursue more western alignment, for instance on tech sanctions. A Chinese policy focused on overall stability would not clearly prefer the latter. As for a Warren presidency, her trade policy has more in common with Trump’s than with Biden’s or the status quo. It is not at all clear that she would be able to unify the West against China on the issue of trade. Hence there is no clear advantage to China of preferring Trump. Biden is probably a greater threat to China on this front, since he would “renegotiate” (i.e. rejoin) the Trans-Pacific Partnership, and court the Europeans, while likely maintaining Obama’s line on China. Yet Biden is viewed as the most pro-China candidate of all. In short, trade policy is a wash from China’s point of view. The U.S. has already taken a more protectionist turn. From China’s view, the U.S. as a whole has taken a protectionist turn. Democrats will not prioritize China: Trump will be unshackled from concerns about bear markets and recessions if he is reelected to a second term due to the two-term limit. Warren would enter as a first-term president and would therefore face the reelection constraint that has hindered Trump’s own trade policy. If Trump loses, Warren faces an implicit threat should she clash with China. Chart 16Market Sees Warren As Health Care Risk

Market Sees Warren As Health Care Risk

Market Sees Warren As Health Care Risk

Warren will also, like President Obama, spend the majority of her first term engrossed in an ambitious domestic policy agenda. Her policy priority is a universal single-payer health care system, which is a much more dramatic undertaking than Biden’s proposal of restoring and enhancing Obamacare, which is why health sector equities are sensitive to Warren’s election chances (Chart 16). Obama did not devote his full attention to Iran and China until his second term, and it is normal for the second term to be the “foreign policy term” due to the absence of electoral constraints. Several of Warren’s policy priorities would also be more favorable to China. In particular, Warren’s desire to impose tougher restrictions on U.S. financials, energy companies, and tech companies is broadly beneficial to China’s efforts to create globally competitive champions. At the same time, Trump is more likely to continue the buildup in U.S. military spending, which, combined with the unlikelihood that Trump will ultimately abandon U.S. allies in Asia, poses a strategic threat for China (Chart 17). China cannot calculate its trade negotiations according to the ups and downs of volatile U.S. politics. Instead it has an incentive to play both sides: to give Trump promises while hesitating to implement them, so as not to render him a dangerous “lame duck” (Chart 18) but also not to gift-wrap the election for him. Chart 17Trump's Military Buildup

Trump's Military Buildup

Trump's Military Buildup

Chart 18

The one thing that can be expected over the next two years is that China will try to maintain economic stability to attract Europe and Asia deeper into its orbit. This means incrementally more stimulus, as mentioned above. China cannot allow itself to risk debt-deflation while encouraging other economies to become less reliant on Chinese demand. Bottom Line: China cannot predict the future. Its best play is to try to undermine the emerging U.S. policy consensus to be tough on China. This means agreeing to a ceasefire to pacify Trump without giving him major structural concessions that improve his chances of reelection. If he loses, future presidents will be afraid of tackling China aggressively. If he wins, yes, China can try to exploit his “America First” policy to keep the U.S. divided within itself and with the rest of the West. If a Democrat wins, China will have set a precedent that gunboat diplomacy fails. It can try to bind the Democrat to the Trump ceasefire terms. If the Democrats tear up the deal then China will have a basis to begin negotiations as an aggrieved party. Investment Conclusions The problem for President Trump is that a weak, short-term ceasefire – in which China does not verifiably implement structural concessions and the threat of “tech war” continues to loom – will not have as positive of an impact on global and American economic sentiment as Trump hopes. Moreover it could collapse under the weight of Sino-American strategic distrust in areas outside trade. Thus while we expect global policy uncertainty to drop off – as we outlined at the beginning of this report – we expect the reduction to be moderate rather than dramatic and not to last all the way to the U.S. election. Our colleagues Bob Ryan and Hugo Belanger have demonstrated that a rise in global policy uncertainty is correlated with a rise in the trade weighted dollar (Chart 19). If uncertainty falls, it will help the dollar ease, which improves global financial conditions and cultivates a rebound in global growth and trade. Chart 19Policy Uncertainty Boosts The Dollar

Policy Uncertainty Boosts The Dollar

Policy Uncertainty Boosts The Dollar

Chart 20Falling Uncertainty Hurts US Outperformance

Falling Uncertainty Hurts US Outperformance

Falling Uncertainty Hurts US Outperformance

This is corroborated by the U.S. trade policy uncertainty index, which reinforces not only the point about the dollar but also the implication that global equities can begin to outperform U.S. equities (Chart 20). With trade sentiment recovering, and U.S. domestic political risk rising due to the election, there is a basis for equity rotation. This assumes that China’s growth does incrementally improve, as we expect. Matt Gertken Geopolitical Strategist mattg@bcaresearch.com

Highlights The U.S. and China are moving toward formalizing a trade ceasefire that reduces geopolitical risk in the near term. The risk of a no-deal Brexit is finished – removing a major downside to European assets. Spanish elections reinforce our narrative of general European political stability. Go long 10-year Italian BTPs / short 10-year Spanish bonos for a trade. Geopolitical risks will remain elevated in Turkey, rise in Russia, but remain subdued in Brazil. A post-mortem of Canada’s election suggests upside to fiscal spending but further downside to energy sector investment over the short to medium term. Feature After a brief spike in trade war-related geopolitical risk just prior to the resumption of U.S.-China negotiations, President Trump staged a tactical retreat in the trade war. Chart 1Proxy For Trade War Shows Falling Risk

Proxy For Trade War Shows Falling Risk

Proxy For Trade War Shows Falling Risk

Negotiating in Washington, President Trump personally visited the top Chinese negotiator Liu He and the two sides announced an informal “phase one deal” to reverse the summer’s escalation in tensions: China will buy $40-$50 billion in U.S. agricultural goods while the U.S. will delay the October 15 tariff hike. More difficult issues – forced tech transfer, intellectual property theft, industrial subsidies – were punted to later. The RMB is up 0.7% and our own measures of trade war-related risk have dropped off sharply (Chart 1). We think these indicators will be confirmed and Trump’s retreat will continue – as long as he has a chance to save the 2020 economic outlook and his reelection campaign. Odds are low that Trump will be removed from office by a Republican-controlled senate – the looming election provides the republic with an obvious recourse for Trump’s alleged misdeeds. However, Trump’s approval rating is headed south. While it is around the same level as President Obama’s at this point in his first term, Obama’s started a steep and steady rise around now and ended above 50% for the election, a level that is difficult to foresee for Trump (Chart 2). So Trump desperately needs an economic boost and a policy victory to push up his numbers. Short of passing the USMCA, which is in the hands of the House Democrats, a deal with China is the only way to get a major economic and political win at the same time. Hence the odds of Presidents Trump and Xi actually signing some kind of agreement are the highest they have been since April (when we had them pegged at 50/50). Trump will have to delay the December 15 tariff hike and probably roll back some of the tariffs over next year as continuing talks “make progress,” though we doubt he will remove restrictions on tech companies like Huawei. Still, we strongly believe that what is coming is a détente rather than the conclusion of the Sino-American rivalry crowned with a Bilateral Trade Agreement. Strategic tensions are rising on a secular basis between the two countries. These tensions could still nix Trump’s flagrantly short-term deal-making, and they virtually ensure that some form of trade war will resume in 2021 or 2022, if indeed a ceasefire is maintained in 2020. Both sides are willing to reduce immediate economic pain but neither side wants to lose face politically. Trump will not forge a “grand compromise.” Our highest conviction view all along has been – and remains – that Trump will not forge a “grand compromise” ushering in a new period of U.S.-China economic reengagement in the medium or long term. China’s compliance, its implementation of structural changes, will be slow or lacking and difficult to verify at least until the 2020 verdict is in. This means policy uncertainty will linger and business confidence and capex intentions will only improve on the margin, not skyrocket upward (Chart 3). Chart 2Trump Needs A Policy Win And Economic Boost

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

Chart 3Sentiment Will Improve ... Somewhat

Sentiment Will Improve ... Somewhat

Sentiment Will Improve ... Somewhat

The problem for bullish investors is that even if global trade uncertainty falls, and the dollar’s strength eases, fear will shift from geopolitics to politics, and from international equities to American equities (Chart 4). Trump, hit by impeachment and an explosive reaction to his Syria policy, is entering into dangerous territory for the 2020 race. Trump’s domestic weakness threatens imminent equity volatility for two reasons. Chart 4American Outperformance Falls With Trade Tensions

bca.gps_wr_2019_10_25_c4

bca.gps_wr_2019_10_25_c4

Chart 5Democratic Win In 2020 Is Market-Negative

Democratic Win In 2020 Is Market-Negative

Democratic Win In 2020 Is Market-Negative

First, if Trump’s approval rating falls below today’s 42%, investors will begin pricing a Democratic victory in 2020, i.e. higher domestic policy uncertainty, higher taxes, and the re-regulation of the American economy (Chart 5). This re-rating may be temporarily delayed or mitigated by the fact that former Vice President Joe Biden is still leading the Democratic Party’s primary election race. Biden is a known quantity whose policies would simply restore the Obama-era status quo, which is only marginally market-negative. Contrary to our expectations Biden's polling has not broken down due to accusations of foul play in Ukraine and China. Nevertheless, Senator Elizabeth Warren will gradually suck votes away from fellow progressive Senator Bernie Sanders and in doing so remain neck-and-neck with Biden (Chart 6). When and if she pulls ahead of Biden, markets face a much greater negative catalyst. (Yes, she is also capable of beating Trump, especially if his polling remains as weak as it is.) Chart 6Warren Will Rise To Front-Runner Status With Biden

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

Second, if Trump becomes a “lame duck” he will eventually reverse the trade retreat above and turn into a loose cannon in his final months in office. Right now we see a decline in geopolitical risk, but if the economy fails to rebound or the China ceasefire offers little support, then Trump will at some point conclude that his only chance at reelection is to double down on his confrontation with America’s enemies and run as a “war president.” A cold war crisis with China, or a military confrontation with Iran (or North Korea, Venezuela, or some unexpected target) could occur. But since September we have been confirmed in believing that Trump is trying to be the dealmaker one last time before any shift to the war president. Bottom Line: The “phase one” trade deal is really just a short-term ceasefire. Assuming it is signed by Trump and Xi, it suggests no increase in tariffs and some tariff rollback next year. However, as recessionary fears fade, and if Trump’s reelection chances stabilize, U.S.-China tensions on a range of issues will revive – and there is no getting around the longer-term conflict between the two powers. For this and other reasons, we remain strategically short RMB-USD, as the flimsy ceasefire will only briefly see RMB appreciation. BoJo's Brexit Bluff Is Finished Our U.K. indicator captured a sharp decline in political risk in the past two weeks and our continental European indicators mirrored this move (Chart 7). The risk that the U.K. would fall out of the EU without a withdrawal agreement has collapsed even further than in September, when parliament rejected Prime Minister Boris Johnson’s no-deal gambit and we went long GBP-USD. We have since added a long GBP-JPY trade. Chart 7Collapse In No-Deal Risk Will Echo Across Europe

Collapse In No-Deal Risk Will Echo Across Europe

Collapse In No-Deal Risk Will Echo Across Europe

Chart 8Unlikely To See Another Tory/Brexit Rally Like This

Unlikely To See Another Tory/Brexit Rally Like This

Unlikely To See Another Tory/Brexit Rally Like This

The risk of “no deal” is the only reason to care about Brexit from a macro point of view, as the difference between “soft Brexit” and “no Brexit” is not globally relevant. What matters is the threat of a supply-side shock to Europe when it is already on the verge of recession. With this risk removed, sentiment can begin to recover (and Trump’s trade retreat also confirms our base case that he will not impose tariffs on European cars on November 14). Since Brexit was the only major remaining European political risk, European policy uncertainty will continue to fall. The Halloween deadline was averted because the EU, on the brink of recession, offered a surprising concession to Johnson, enabling him to agree to a deal and put it up for a vote in parliament. The deal consists of keeping Northern Ireland in the European Customs Union but not the whole of the U.K., effectively drawing a new soft border at the Irish Sea. The bill passed the second reading but parliament paused before finalizing it, rejecting Johnson’s rapid three-day time table. The takeaway is that even if an impending election returns Johnson to power, he will seek to pass his deal rather than pull the U.K. out without a deal. This further lowers the odds of a no-deal Brexit as it illuminates Johnson's preferences, which are normally hidden from objective analysis. True, there is a chance that the no-deal option will reemerge if Johnson’s deal totally collapses due to parliamentary amendments, or if the U.K. and EU have failed to agree to a future relationship by the end of the transition period on December 31, 2020 (which can be extended until the end of 2022). However, the chance is well below the 30% which we deemed as the peak risk of no-deal back in August. Johnson created the most credible threat of a no-deal exit that we are likely to see in our lifetimes – a government with authority over foreign policy determined to execute the outcome of a popular referendum – and yet parliament stopped it dead in its tracks. Johnson does not want a no-deal recession and his successors will not want one either. After all, the support for Brexit and for the Tories has generally declined since the referendum, and the Tories are making a comeback on the prospect of an orderly Brexit (Chart 8). All eyes will now turn toward the impending election. Opinion polls still show that Johnson is likely to be returned to power (Chart 9). The Tories have a prospect of engrossing the pro-Brexit vote while the anti-Brexit opposition stands divided. No-deal risk only reemerges if the Conservatives are returned to power with another weak coalition that paralyzes parliament. Chart 9Tory Comeback As BoJo Gets A Deal

Tory Comeback As BoJo Gets A Deal

Tory Comeback As BoJo Gets A Deal

Chart 10Brexit Means Greater Fiscal Policy

Brexit Means Greater Fiscal Policy

Brexit Means Greater Fiscal Policy

Whatever the election result, we maintain our long-held position that Brexit portends greater fiscal largesse (Chart 10). The agitated swath of England that drove the referendum result will not be assuaged by leaving the European Union – the rewards of Brexit are not material but philosophical, so material grievances will return. Voter frustration will rotate from the EU to domestic political elites. Voters will demand more government support for social concerns. Johnson’s own government confirms this point through its budget proposals. A Labour-led government would oversee an even more dramatic fiscal shift. Our GeoRisk indicator will fall on Brexit improvements but the question of the election and next government will ensure it does not fall too far. Our long GBP trades are tactical and we expect volatility to remain elevated. But the greatest risk, of no deal, is finished, so it does make sense for investors with a long time horizon to go strategically long the pound. The greatest risk, of a no deal Brexit, is finished. Bottom Line: Brexit posed a risk to the global economy only insofar as it proved disorderly. A withdrawal agreement by definition smooths the process. Continental Europe will not suffer a further shock to net exports. The Brexit contribution to global policy uncertainty will abate. The pound will rise against the euro and yen and even against the dollar as long as Trump’s trade retreat continues. Spain: Further Evidence Of European Stability We have long argued that the majority of Catalans do not want independence, but rather a renegotiation of the region's relationship with Spain (Chart 11). This month’s protests in Barcelona following the Catalan independence leaders’ sentencing are at the lower historical range in terms of size – protest participation peaked in 2015 along with support for independence (Table 1). Table 1October Catalan Protests Unimpressive

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

Our Spanish risk indicator is showing a decline in political risk (Chart 12). However, we believe that this fall is slightly overstated. While the Catalan independence movement is losing its momentum, the ongoing protests are having an impact on seat projections for the upcoming election. Chart 11Catalonians Not Demanding Independence

Catalonians Not Demanding Independence

Catalonians Not Demanding Independence

Chart 12Right-Wing Win Could Surprise Market, But No Worries

Right-Wing Win Could Surprise Market, But No Worries

Right-Wing Win Could Surprise Market, But No Worries

Since the April election, the right-wing bloc of the People’s Party, Ciudadanos, and Vox has been gaining in the seat projections at the expense of the Socialist Party and Podemos. Over the course of the protests, the left-wing parties’ lead over the right-wing parties has narrowed from seven seats to one (Chart 13). If this momentum continues, a change of government from left-wing to right-wing becomes likely. However, a right-wing government is not a market-negative outcome, and any increase in risk on this sort of election surprise would be short-lived. The People’s Party has moderated its message and focused on the economy. Besides pledging to limit the personal tax rate to 40% and corporate tax rate to 20%, the People’s Party platform supports innovation, R&D spending, and startups. The party is promising tax breaks and easier immigration rules to firms and employees pursuing these objectives. Chart 13Spanish Right-Wing Parties Narrow Gap With Left

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

Another outcome of the election would be a governing deal between PSOE and Podemos, along with case-by-case support from Ciudadanos. After a shift to the right lost Ciudadanos 5% in support since the April election, leader Albert Rivera announced in early October that he would be lifting the “veto” on working with the Socialist Party. If the right-wing parties fall short of a majority, then Rivera would be open to talks with Socialist leader Pedro Sanchez. A governing deal between PSOE, Podemos, and Ciudadanos would have 175 seats, as of the latest projections, which is just one seat short of a majority. As we go to press, this is the only outcome that would end Spain’s current political gridlock, and would therefore be the most market-positive outcome. Bottom Line: Despite having a fourth election in as many years, Spanish political risk is contained. This is reinforced by a relatively politically stable backdrop in continental Europe, and marginally positive developments in the U.K. and on the trade front. We remain long European versus U.S. technology, and long EU versus Chinese equities. We will also be looking to go long EUR/USD when and if the global hard data turn. Following our European Investment Strategy, we recommend going long 10-year Italian BTPs / short 10-year Spanish bonos for a trade. Turkey, Brazil, And Russia Chart 14Turkish Risk Will Rise Despite 'Ceasefire'

Turkish Risk Will Rise Despite 'Ceasefire'

Turkish Risk Will Rise Despite 'Ceasefire'

Turkey’s political risk skyrocketed upward after we issued our warning in September (Chart 14). We maintain that the Trump-Erdogan personal relationship is not a basis for optimism regarding Turkey’s evading U.S. sanctions. Both chambers of the U.S. Congress are preparing a more stringent set of sanctions, focusing on the Turkish military, in the wake of Trump’s decision to withdraw U.S. forces from northeast Syria. At a time when Trump needs allies in the senate to defend him against eventual impeachment articles, he is not likely to veto and risk an override. Moreover, Turkey’s military incursion into Syria, which may wax and wane, stems from economic and political weakness at home and will eventually exacerbate that weakness by fueling the growing opposition to Erdogan’s administration and requiring more unorthodox monetary and fiscal accommodation. It reinforces our bearish outlook on Turkish lira and assets. Chart 15Brazilian Risk Will Not Re-Test 2018 Highs

Brazilian Risk Will Not Re-Test 2018 Highs

Brazilian Risk Will Not Re-Test 2018 Highs

Brazil’s political risk has rebounded (Chart 15). The Senate has virtually passed the pension reform bill, as expected, which raises the official retirement age for men and women to 65 and 63 respectively. This will generate upwards of 800 billion Brazilian real in savings to improve the public debt profile. Of course, the country will still run primary deficits and thus the public debt-to-GDP ratio will still rise. Now the question shifts to President Jair Bolsonaro and his governing coalition. Bolsonaro’s approval rating has ticked up as we expected (Chart 16). If this continues then it is bullish for Brazil because it suggests that he will be able to keep his coalition together. But investors should not get ahead of themselves. Bolsonaro is not an inherently pro-market leader, there is no guarantee that he will remain disciplined in pursuing pro-productivity reforms, and there is a substantial risk that his coalition will fray without pension reform as a shared goal (at least until markets riot and push the coalition back together). Therefore we expect political risk to abate only temporarily, if at all, before new trouble emerges. Furthermore, if reform momentum wanes next year, then Brazil’s reform story as a whole will falter, since electoral considerations emerge in 2021-22. Hence it will be important to verify that policymakers make progress on reforms to tax and trade policy early next year. Our Russian geopolitical risk indicator is also lifting off of its bottom (see Appendix). This makes sense given Russia’s expanding strategic role (particularly in the Middle East), its domestic political troubles, and the risks of the U.S. election. The latter is especially significant given the risk (not our base case, however) that a Democratic administration could take a significantly more aggressive posture toward Russia. Political risk in Turkey and Russia will continue to rise. Bottom Line: Political risk in Turkey and Russia will continue to rise. Russia is a candidate for a “black swan” event, given the eerie quiet that has prevailed as Putin devotes his fourth term to reducing domestic political instability. Brazil, on the other hand, has a 12-month window in which reform momentum can be reinforced, reducing whatever spike in risk occurs in the aftermath of the ruling coalition’s completion of pension reform. Canada: Election Post-Mortem Prime Minister Justin Trudeau returned to power at the head of a minority government in Canada’s federal election (Chart 17). The New Democratic Party (NDP) lost 15 seats from the last election, but will have a greater role in parliament as the Liberals will need its support to pass key agenda items (and a formal governing coalition is possible). The NDP’s result would have been even worse if not for its last-minute surge in the polls after the election debates and Trudeau’s “blackface” scandal. Chart 17Liberals Need The New Democrats Now

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

The Conservative Party won the popular vote but only 121 seats in parliament, leaving the western provinces of Alberta and Saskatchewan aggrieved. The Bloc Québécois, the Quebec nationalist party, gained 22 seats to become the third-largest party in the House. Energy investment faces headwinds in the near-term. The Liberal Party will face resistance from the Left over the Trans Mountain pipeline. Trudeau will not necessarily have to sacrifice the pipeline to appease the NDP. He may be able to work with Conservatives to advance the pipeline while working with the NDP on the rest of his agenda. But on the whole the election result is the worst-case scenario for the oil sector and political questions will have to be resolved before Canada can take advantage of its position as a heavy crude producer near the U.S. Gulf refineries in an era in which Venezuela is collapsing and Saudi Arabia is exposed to geopolitical risk and attacks. More broadly, the Liberals will continue to endorse a more expansive fiscal policy than expected, given Canada’s low budget deficits and the need to prevent minor parties from eating away at the Liberal Party’s seat count in future. Bottom Line: The Liberal Party failed to maintain its single-party majority. Trudeau’s reliance on left-wing parties in parliament may prove market-negative for the Canadian energy sector, though that is not a forgone conclusion. Over the longer term the sector has a brighter future. Matt Gertken Geopolitical Strategist mattg@bcaresearch.com Ekaterina Shtrevensky Research Analyst ekaterinas@bcaresearch.com Appendix GeoRisk Indicator

TRADE WAR GEOPOLITICAL RISK INDICATOR

TRADE WAR GEOPOLITICAL RISK INDICATOR

U.K.: GeoRisk Indicator

U.K.: GEOPOLITICAL RISK INDICATOR

U.K.: GEOPOLITICAL RISK INDICATOR

France: GeoRisk Indicator

FRANCE: GEOPOLITICAL RISK INDICATOR

FRANCE: GEOPOLITICAL RISK INDICATOR

Germany: GeoRisk Indicator

GERMANY: GEOPOLITICAL RISK INDICATOR

GERMANY: GEOPOLITICAL RISK INDICATOR

Spain: GeoRisk Indicator

SPAIN: GEOPOLITICAL RISK INDICATOR

SPAIN: GEOPOLITICAL RISK INDICATOR

Italy: GeoRisk Indicator

ITALY: GEOPOLITICAL RISK INDICATOR

ITALY: GEOPOLITICAL RISK INDICATOR

Canada: GeoRisk Indicator

CANADA: GEOPOLITICAL RISK INDICATOR

CANADA: GEOPOLITICAL RISK INDICATOR

Russia: GeoRisk Indicator

RUSSIA: GEOPOLITICAL RISK INDICATOR

RUSSIA: GEOPOLITICAL RISK INDICATOR

Turkey: GeoRisk Indicator

TURKEY: GEOPOLITICAL RISK INDICATOR

TURKEY: GEOPOLITICAL RISK INDICATOR

Brazil: GeoRisk Indicator

BRAZIL: GEOPOLITICAL RISK INDICATOR

BRAZIL: GEOPOLITICAL RISK INDICATOR

Taiwan: GeoRisk Indicator

TAIWAN: GEOPOLITICAL RISK INDICATOR

TAIWAN: GEOPOLITICAL RISK INDICATOR

Korea: GeoRisk Indicator

KOREA: GEOPOLITICAL RISK INDICATOR

KOREA: GEOPOLITICAL RISK INDICATOR

What's On The Geopolitical Radar?

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

How Much To Buy An American President? – GeoRisk Update: October 25, 2019

Section III: Geopolitical Calendar

Highlights Shifting Trends: The factors that have driven bond yields lower throughout 2019 – slowing growth, rising uncertainty, demand for safe assets and dovish monetary policy expectations – have all started to turn in a more bond-bearish direction. Duration & Country Allocation Strategy: Maintain a moderate below-benchmark stance on aggregate bond portfolio duration. Favor lower-beta countries with central banks that are more likely to stay relatively dovish as global yields drift higher, like core Europe, Australia and Japan. Credit Allocation Strategy: Stay overweight corporate bonds versus government debt in the U.S. and Europe, both for investment grade and high-yield. Maintain just a neutral stance on EM USD-denominated spread product, but look to upgrade if global growth improves further and the USD begins to weaken. Feature Chart of the WeekBond Yields Sniffing A Turn In Global Growth?

Bond Yields Sniffing A Turn In Global Growth?

Bond Yields Sniffing A Turn In Global Growth?

It has been fifty days (and counting) since the 2019 low for the benchmark 10-year U.S. Treasury yield was reached on September 3. The year-to-date low for the benchmark 10-year German bund yield was seen six days before that on August 28. Yields have risen by a healthy amount since those dates, up +34bps and +37bps for the 10yr Treasury and Bund, respectively. This has occurred despite the significant degree of bond-bullish pessimism on global growth and inflation that can be found in financial media reporting and investor surveys. The fact that yields are now steadily moving away from the lows suggests that the 2019 narrative for financial markets – slowing global growth, triggered by political uncertainty and the lagged impact of previous Fed monetary tightening and China credit tightening, forcing central banks to turn increasingly more dovish – is no longer correct. If that is true, yields have more near-term upside as overbought government bond markets begin to “sniff out” a bottoming out of global growth momentum (Chart of the Week). In this Weekly Report, we take a look at the changing state of the factors that fueled the sharp decline in bond yields in 2019. We follow that up with a review of all our current recommended investment positions on duration, country allocation and spread product allocations in light of recent developments. We conclude that maintaining a below-benchmark duration exposure, while favoring lower-beta countries in sovereign debt and overweighting corporate debt in the U.S. and Europe, is the most appropriate fixed income strategy for the next 6-12 months. The timing of the bottoming of yields in the major developed markets (DM) should not be surprising, given the more bond-bearish turn of reliable leading directional yield indicators. Yields Are Rising At The Right Time, For The Right Reasons Chart 2Bond-Bullish Growth & Inflation Factors Are Turning

Bond-Bullish Growth & Inflation Factors Are Turning

Bond-Bullish Growth & Inflation Factors Are Turning

The timing of the bottoming of yields in the major developed markets (DM) should not be surprising, given the more bond-bearish turn of reliable leading directional yield indicators. The diffusion index of our global leading economic indicator (LEI), which leads the real (ex-inflation expectations) component of DM bond yields by twelve months, is at an elevated level (Chart 2). At the same time, the slowing of the annual rate of growth in the trade-weighted U.S. dollar, which leads 10-year DM CPI swap rates by around six months, is signaling that bond yields have room to increase from the inflation expectations side. Finally, the rising trend of positive data surprises for the major DM countries is also pointing to higher yields. Breaking it down at the country level, the pickup in DM 10-year bond yields since the 2019 lows has been widespread (Charts 3 & 4). The range of yield increases is as low as +16bps in Japan, where the Bank of Japan (BoJ) is pursuing a yield target, to +46bps in Canada where the economy and inflation are both accelerating. Chart 3Pricing Out Some Expected Rate Cuts …

Pricing Out Some Expected Rate Cuts ...

Pricing Out Some Expected Rate Cuts ...

Chart 4… Across All Developed Markets

... Across All Developed Markets

... Across All Developed Markets

The increase in yields has also occurred alongside reduced expectations for easier monetary policy. Our 12-month discounters, which measure the expected change in short-term interest rates priced into Overnight Index Swap (OIS) curves, show that markets have partially priced out some (but not all) expected rate cuts in all major DM countries. The Three Things That Have Changed For Global Bond Markets So what has changed to trigger a reduction in rate cut expectations and an increase in global yields? The bond-bullish narrative that we refer to in the title of this report can be broken down into the following three elements, which have all turned recently: Slowing global growth (now potentially bottoming) Chart 5Global Growth Bottoming Out

Global Growth Bottoming Out

Global Growth Bottoming Out

Current global growth is still trending lower, when looking at measures like manufacturing PMIs or sentiment surveys like the global ZEW index. Forward-looking measures like our global LEI, however, have been moving higher in recent months, suggesting that a bottom in the PMIs may soon unfold (Chart 5). We investigated that improvement in our global LEI in a recent report and concluded that the move higher was focused almost exclusively within the emerging market (EM) sub-components that are most sensitive to improving global growth.1 This fits with the improvement shown in the OECD LEI for China, a bottoming of the annual growth rate of world exports, and the general acceleration of global equity markets – the classic leading economic indicator. Rising political uncertainty (now potentially fading) The U.S.-China trade war (including the implications for the upcoming 2020 U.S. presidential election) and the U.K. Brexit saga have been the main sources of bond-bullish political uncertainty over the past several months. Yet recent developments have helped reduce the odds of the most negative tail risk outcomes, providing a bit of a boost to global bond yields. The U.S. and China have agreed (in principle) to a “phase one” trade deal that, at a minimum, lowers the chances of a further escalation of the trade dispute through higher tariffs. Meanwhile, the momentum has shifted towards a potential final Brexit agreement between the U.K. and European Union that can avoid an ugly no-deal outcome. Our colleagues at BCA Research Geopolitical Strategy believe that developments are likely to continue moving away from the worst-case scenarios, given the constraints faced by policymakers.2 U.S. President Donald Trump is now in full campaign mode for the 2020 elections and needs a deal (of any kind) to deflect criticism that his trade battle with China is dragging the U.S. economy into recession. Already, there has been a sharp decline in income growth for workers in swing states that could vote for either party’s candidate in next year’s election (Chart 6). Trump cannot afford to lose voters in those states, many of which are in the U.S. industrial heartland (i.e. Ohio, Michigan) that helped put him in the White House. In other words, he is highly incentivized to turn down the heat on the trade war or else face a potential loss next November. While these political uncertainties have not been fully resolved by these latest developments, the shift in momentum away from worst-case scenarios has likely been enough to reduce the safe-haven bid for DM government bonds, helping push yields higher. Meanwhile, China is facing a slowing economy and rising unemployment, but with reduced means to fight the downtrend given high private sector debt that has impaired the typical response between easier monetary conditions and economic activity (Chart 7). While the Chinese government does not want to be seen as caving in to U.S. pressure on trade policy, its desire to maintain social stability by preventing a further rise in unemployment from the trade war provides a powerful incentive to try and ratchet down tensions with the U.S. Chart 6Political Reasons For Trump To Retreat On Trade

Political Reasons For Trump To Retreat On Trade

Political Reasons For Trump To Retreat On Trade

In the U.K., a no-deal Brexit is an economically painful and politically unpopular outcome that would severely damage the re-election chances of Prime Minister Boris Johnson and his Conservative party. Thus, even a hard-line Brexiteer like Johnson must respond to the political constraints forcing him to try and get a Brexit deal done (Chart 8). Chart 7Economic Reasons For China To Retreat On Trade

Economic Reasons For China To Retreat On Trade

Economic Reasons For China To Retreat On Trade

Chart 8Political Reasons To Retreat On A No-Deal Brexit

Political Reasons To Retreat On A No-Deal Brexit

Political Reasons To Retreat On A No-Deal Brexit

While these political uncertainties have not been fully resolved by these latest developments, the shift in momentum away from worst-case scenarios has likely been enough to reduce the safe-haven bid for DM government bonds, helping push yields higher. Bull-flattening pressure on yield curves (now turning into moderate bear-steepening) The final leg down in bond yields in August had a technical aspect to it, fueled by the demand for duration and convexity from asset-liability managers like European pension funds and insurance companies. Falling yields act to raise the value of liabilities for that group of investors, forcing them to rapidly increase the duration of their assets to match the duration of their liabilities (the technique used to limit the gap between the value of assets and liabilities). That duration increase is carried out by buying government bonds with longer maturities (and higher convexity), but also through the use of interest rate derivatives like long maturity swaps and swaptions. The end result is a bull flattening of yield curves (both for government bonds and swaps) and a rise in swaption volatility (i.e. the price of swaptions). Those dynamics were clearly in play in August after the shocking imposition of fresh U.S. tariffs on Chinese imports early in the month. Bond and swaption volatilities spiked, and bond/swap yield curves bull-flattened, in both Europe and the U.S. (Chart 9). That effect only lasted a few weeks, however, and volatilities have since declined and curves have steepened. This suggests that the “convexity-buying” effect has run its course and is now starting to work in the opposite direction, with asset-liability managers looking to reduce the duration of their assets as higher yields lower the value of their liabilities. This is putting some upward pressure on longer-maturity global bond yields. Chart 9Signs Of Reduced Convexity-Related Bond Buying

Signs Of Reduced Convexity-Related Bond Buying

Signs Of Reduced Convexity-Related Bond Buying

Chart 10Bull-Flattening Yield Curve Pressures Easing Up A Bit

Bull-Flattening Yield Curve Pressures Easing Up A Bit

Bull-Flattening Yield Curve Pressures Easing Up A Bit

Chart 11Fed & ECB Actions Should Help Steepen Up Curves

Fed & ECB Actions Should Help Steepen Up Curves

Fed & ECB Actions Should Help Steepen Up Curves

The steepening seen so far must be put in context, however, as yield curves remain very flat across the DM world (Chart 10). Term premia on longer-term bonds remain very depressed, although those should start to increase as global growth stabilizes and the massive safe-haven demand for global government debt begins to dissipate. Some pickup in inflation expectations would also help impart additional bear-steepening momentum to yield curves – a more likely result now that the Fed and ECB have both cut interest rates and, more importantly, will start provide additional monetary easing by expanding their balance sheets (Chart 11). Bottom Line: The factors that have driven bond yields lower throughout 2019 – slowing growth, rising uncertainty, demand for safe assets and dovish monetary policy expectations – have all started to turn in a more bond-bearish direction. Reviewing Our Recommended Bond Allocations In light of these shifting global trends described above, the fixed income investment implications are fairly straightforward: Yields are rising around the world, suggesting that the current move is a shift higher driven by non-country-specific factors like more stable future global growth prospects. Duration: A moderate below-benchmark overall duration stance is warranted for global fixed income portfolios, with yields likely to continue drifting higher over at least the next six months. A big surge in yields is unlikely, as central banks will need to see decisive evidence that global growth is not only bottoming, but accelerating, before shifting away from the current dovish bias. Given the reporting lags in the economic data, such evidence is unlikely to appear until the first quarter of 2020 at the earliest. Yet given how flat yield curves are across the DM government bond markets, the trajectory of forward rates is quite stable relative to spot yield levels, making it much easier to beat the forwards by positioning for even a modest yield increase. Country Allocation: Yields are rising around the world, suggesting that the current move is a shift higher driven by non-country-specific factors like more stable future global growth prospects. In that case, using yield betas to the “global” bond yield is a good way to consider country allocation decisions within a fixed income portfolio. We looked at those yield betas in an August report, using Bloomberg Barclays government bond index data for the 7-10 year maturity buckets of individual countries and the Global Treasury aggregate (Chart 12).3 The rolling 3-year betas were highest in the U.S. and Canada, making them good countries to underweight within a global government bond portfolio in a rising yield environment. The yield betas were lowest in Japan, Germany and Australia, making them good overweight candidates. The U.K. was a unique case of having a relatively high historical yield beta prior to the 2016 Brexit referendum and a lower yield beta since then - making the U.K. allocation highly conditional on the resolution of the Brexit uncertainty. Spread Product Allocation: The backdrop described in this report, where global growth is bottoming out but where central banks maintain a dovish bias, is a perfect sweet spot for global spread product like corporate bonds and Peripheral European government debt. Thus, an overweight stance on overall global spread product versus governments is warranted. The backdrop described in this report, where global growth is bottoming out but where central banks maintain a dovish bias, is a perfect sweet spot for global spread product like corporate bonds and Peripheral European government debt. With regards to our current strategic fixed income recommendations and model bond portfolio allocations, we already have much of the positioning described above in place. We are below-benchmark on overall duration, underweight higher-beta U.S. Treasuries; overweight government bonds in lower-beta Germany, France, Japan and Australia (Chart 13); overweight investment grade corporate bonds in the U.S., euro area and U.K.; and overweight high-yield corporate bonds in the U.S. and euro area. Chart 12Favor Lower-Beta Government Bond Markets

Favor Lower-Beta Government Bond Markets

Favor Lower-Beta Government Bond Markets

There are areas where our positioning could change, however. Chart 13Lower-Beta Laggards Should Start To Outperform

Lower-Beta Laggards Should Start To Outperform

Lower-Beta Laggards Should Start To Outperform

In terms of government bonds, we are currently overweight the U.K. and neutral Canada. A final Brexit deal would justify a downgrade of Gilts to at least neutral, if not underweight, as the Bank of England has signaled that rate hikes would be justified if the Brexit uncertainty was resolved. A downgrade of higher-beta Canadian government debt to underweight could also be justified, although the Bank of Canada is not signaling that a change in monetary policy (in either direction) is warranted. For now, we will hold off on any change to our U.K. stance, as it is now likely that there will be another extension of the Brexit deadline beyond October 31. As for Canada, we remain neutral for now but will revisit that stance in an upcoming Weekly Report. With regards to spread product, we are only neutral EM USD-denominated sovereign and corporate debt, as well as Spanish sovereign bonds; and underweight Italian government debt. An EM upgrade to overweight would require two things that are not yet in place: a weaker U.S. dollar and accelerating Chinese economic growth. Chart 14Stay Overweight Corporates In The U.S. & Europe

Stay Overweight Corporates In The U.S. & Europe

Stay Overweight Corporates In The U.S. & Europe

As for Peripheral governments, we have preferred to be overweight European corporate debt relative to sovereign bonds in Italy and Spain. The recent powerful rally in the Periphery, however, has driven the spreads over German bunds in those countries down to levels in line with corporate credit spreads (Chart 14). We will maintain these allocations for now, but will investigate the relative value proposition between euro area Peripheral sovereigns and corporates in an upcoming report. Bottom Line: Maintain a moderate below-benchmark stance on aggregate bond portfolio duration. Favor lower-beta countries with central banks that are more likely to stay relatively dovish as global yields drift higher, like core Europe, Australia and Japan. Stay overweight corporate bonds versus government debt in the U.S. and Europe, both for investment grade and high-yield. Maintain just a neutral stance on EM USD-denominated spread product, but look to upgrade if global growth improves further and the USD begins to weaken. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Research Global Fixed Income Strategy Weekly Report, “What Is Driving The Improvement In The BCA Global Leading Economic Indicator?”, dated October 2, 2019, available at gfis.bcaresearch.com. 2 Please see BCA Research Geopolitical Strategy Weekly Report, “Five Constraints For The Fourth Quarter”, dated October 11, 2019, available at gps.bcaresearch.com. 3 Please see BCA Research U.S. Bond Strategy/Global Fixed Income Strategy Weekly Report, “Where’s The Positive Carry In Bond Markets?", dated August 20, 2019, available at usbs.bcaresearch.com and gfis.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Cracks Are Forming In The Bond-Bullish Narrative

Cracks Are Forming In The Bond-Bullish Narrative

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

If Turkey is the loser, who is the winner? First, Trump, who benefits from fulfilling a campaign pledge to reduce U.S. involvement in foreign wars – a stance that will ultimately be rewarded (or at least not punished) by a war-weary public. Second, Iran…

Despite the many hurdles that remain, prospects of a détente in the 18 month-long trade war are significantly rising. As a self-professed “master negotiator,” President Trump has put his credibility on the line by describing the negotiations as a “love fest,”…

Highlights The investors we met last week were ready to hear some good news: The constructive story we told across three days of client meetings is more sanguine than the consensus view, but clients were open to considering it. Global economic weakness and the elevated risk of a U.S. recession were primary concerns, … : As our Global Investment Strategy colleagues have suggested, it will take some time for investors to be convinced that global manufacturing really has seen the bottom and that the U.S. isn’t flirting with a recession. … followed by trade tensions and corporate indebtedness, … : Our small sample suggests that investors may have become de-sensitized to the daily ebb and flow of the U.S.-China conflict, though we continue to believe it looms large in the minds of corporate managements. … but nothing matches the anxiety provoked by Elizabeth Warren’s ascent: Every client asked about the potential consequences of a Warren White House. Feature We spent most of last week meeting with a subset of wealth management and family office clients. They are more focused on absolute returns than relative returns, but their primary concerns are nearly identical to their relative-return peers’. Our meetings touched on a broad constellation of questions about the fate of the expansion, the equity bull market, global growth and the U.S.-China trade negotiations. Clients also asked about the credit outlook and if inflation should be on their radar, but the topic that they raised with the most fervor, in every single one of our meetings, was the prospect of a Warren or Sanders presidency. Q: What is the bond market telling us? We think of the bond market as having two distinct components, rates (Treasuries) and credit (spread product). We have gotten used to regular retracements in the 10-year Treasury yield since it bottomed in July 2016, but watching it melt from 3.25% last November to 1.5% this August has challenged our constructive take on the U.S. economy. Falling yields are not necessarily signaling imminent economic trouble, however, so we continue to hold the view that a recession won’t occur before late 2021 or early 2022. We see this year’s falling Treasury yields as a coincident reflection of decelerating growth, not a harbinger of a recession. On a purely domestic basis, the principal driver of the decline in yields has been the shift in monetary policy expectations. The Fed’s dovish pivot did not occur in a vacuum, of course. Clear signs of decelerating growth set the stage for easier policy, both here and abroad. Whether or not the Fed was always calling the tune, all three step-function declines in 12-month forward fed funds rate expectations occurred as it was guiding markets to expect easier policy: ahead of the March FOMC meeting, when Fed speakers began warning of the danger of inflation expectations becoming unanchored on the downside; in May, when they were busily preparing the ground for a rate cut; and after the July meeting raised the prospect that the July cut would not be a one-off event (Chart 1). Chart 1The Fed's Dovish Pivot, ...

The Fed's Dovish Pivot, ...

The Fed's Dovish Pivot, ...

Sovereign rates are not entirely determined domestically, and much of the softness in Treasury yields reflects the softness in yields in the rest of the world. So far this year, 10-year sovereign yields have moved in lockstep on either side of the Atlantic (Chart 2), preserving no-arbitrage conditions in currency-hedged Treasuries, gilts and bunds. Crude prices are another global variable, and their decline has weighed on inflation break-even rates (Chart 3), dampening the inflation compensation demanded by Treasury buyers. From a rates perspective, we think the bond market is telling us that global growth has slowed, central banks have taken monetary accommodation up a notch, and oil prices have slid. That’s not exactly an ideal growth backdrop, but it hardly spells the end of the expansion. Chart 2... And European Sovereigns' Gravitational Pull Have Dragged Treasury Yields Lower

... And European Sovereigns' Gravitational Pull Have Dragged Treasury Yields Lower

... And European Sovereigns' Gravitational Pull Have Dragged Treasury Yields Lower

The credit market concurs. It doesn’t betray a whit of concern that the expansion is in trouble. Spreads quickly unwound last year’s fourth-quarter spike, and have since hung around their post-crisis lows (Chart 4). Non-financial corporations have become more indebted throughout the expansion, but servicing the debt is not at all onerous with yields at rock-bottom levels (Chart 5). Our U.S. Bond Strategy service’s proprietary corporate health monitor is signaling that corporate balance sheets have weakened (Chart 6, third panel), but the other elements required for a meaningful widening of spreads – a completed monetary tightening cycle1 (Chart 6, second panel), and a tightening of lending standards (Chart 6, bottom panel) – are not yet in place. Chart 3Falling Oil Prices Have Smothered Inflation Worries

Falling Oil Prices Have Smothered Inflation Worries

Falling Oil Prices Have Smothered Inflation Worries

Chart 4Spreads Are Tight, ...

Spreads Are Tight, ...

Spreads Are Tight, ...

Chart 5... And Debt Service Is Easy

... And Debt Service Is Easy

... And Debt Service Is Easy

Q: Isn’t it time to reduce credit exposures? Tight spreads may be a contrarian warning sign. Though it is sensible to shift some of a company’s financing burden to debt when it is so much cheaper than equity, combining a larger debt burden with degraded covenant protections is a concern. Low interest rates will keep debt service costs from chafing, and help keep defaults in check for now, but the bond market is increasingly vulnerable. Chart 6Spread Widening Conditions Aren't Yet In Place

Spread Widening Conditions Aren't Yet In Place

Spread Widening Conditions Aren't Yet In Place

Chart 7Income Investors Need Not Apply

Income Investors Need Not Apply

Income Investors Need Not Apply