Geopolitics

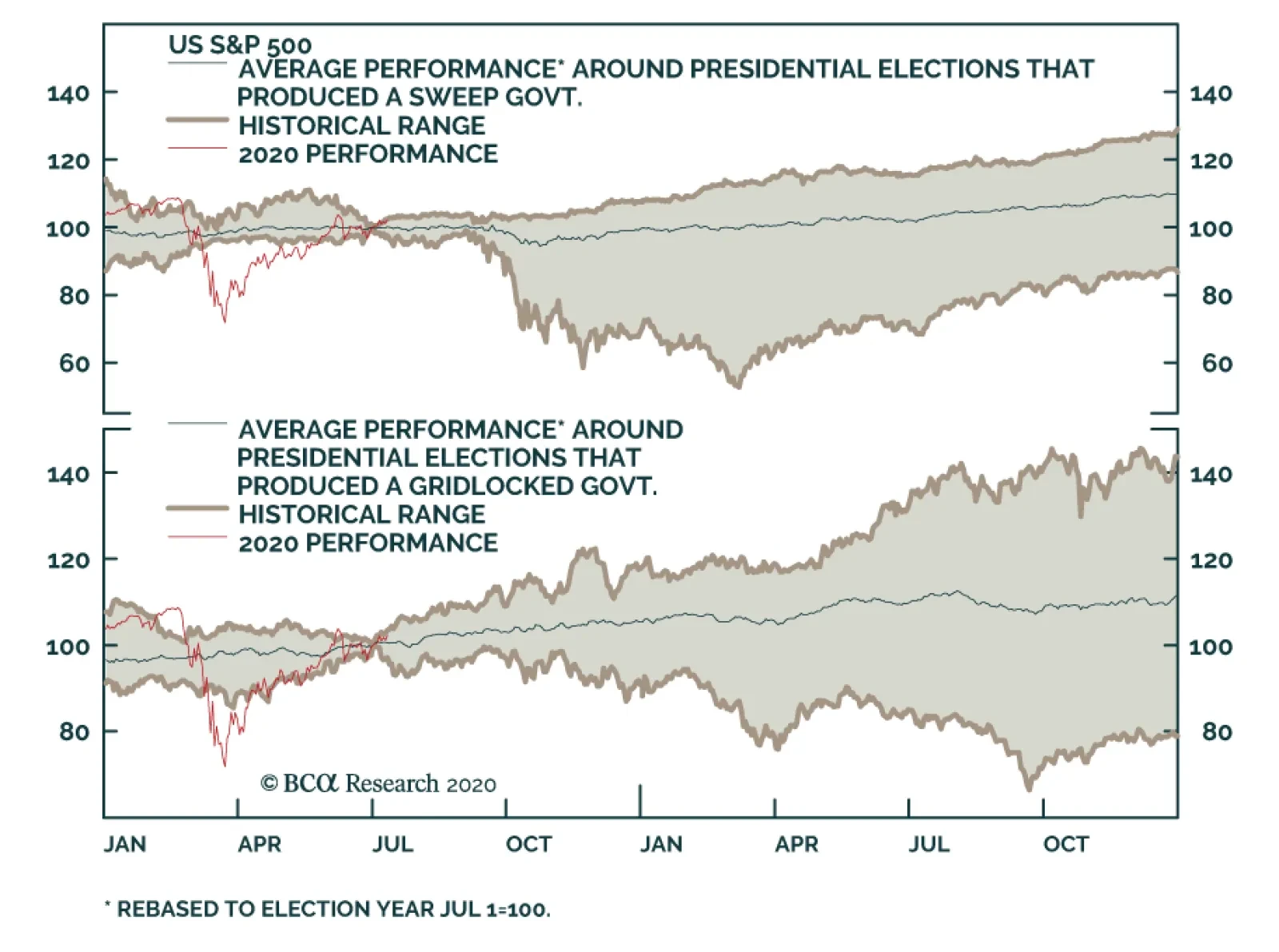

Highlights PORTFOLIO STRATEGY While our cyclically sanguine broad equity market view remains intact, we are cautious on the short-term prospects of the S&P 500, until the election uncertainty lifts. A contested election and legitimacy crisis is possible in the US, but the constitutional system is robust and the likely risk-off phase would be temporary. A depreciating US dollar, China’s rebounding economic activity, improving domestic operating metrics and compelling valuations all signal that it no longer pays to be bearish chemicals equities. An improving export backdrop, a depreciating greenback and commodity price inflation, labor cost discipline at home, along with a relative value proposition, all argue for an above benchmark allocation to the S&P materials sector. Recent Changes Lock in gains in the S&P chemicals index of 1% since inception, and upgrade to neutral today. Boost the S&P materials sector to an above benchmark allocation today. Feature Equities made fresh recovery highs last week cheering promising vaccine news, optimism on a fiscal package extension and a resumption in the Fed’s balance sheet expansion. Easy monetary and loose fiscal policies remain the key macro drivers of equity returns. Yet, the deeper we dig in the concentration of SPX returns the more worried we become. The top five stocks in the SPX (AAPL, MSFT, AMZN, GOOGL & FB) have added $4.82tn to the S&P 500 market cap since 2015, whereas the bottom 495 stocks have added $3.82tn. In percent return terms, these five tech titans’ market capitalization has gone up roughly four fold or 288% over the past 5 ½ years from $1.67tn to $6.49tn. In marked contrast, the S&P 495 market cap has barely budged, rising a mere 23% (increasing from 16.57tn to $20.39tn) during the same time frame (top panel, Chart 1). If investors have not been in these tech titans, then they have not really participated in the SPX’s run up. The measly return since 2015 in the Value Line Arithmetic index and negative return in the Value Line Geometric index gauging the mean and median US stock, respectively, corroborate our analysis (not shown). Clearly, such a steep divergence is unsustainable and the longer these handful of stocks defy gravity the steeper their eventual fall will be (bottom panel, Chart 1). While our cyclically sanguine broad equity market view remains intact, we are cautious on the short-term prospects of the S&P 500, until the election uncertainty lifts. Chart 1S&P 5 Versus S&P 495

S&P 5 Versus S&P 495

S&P 5 Versus S&P 495

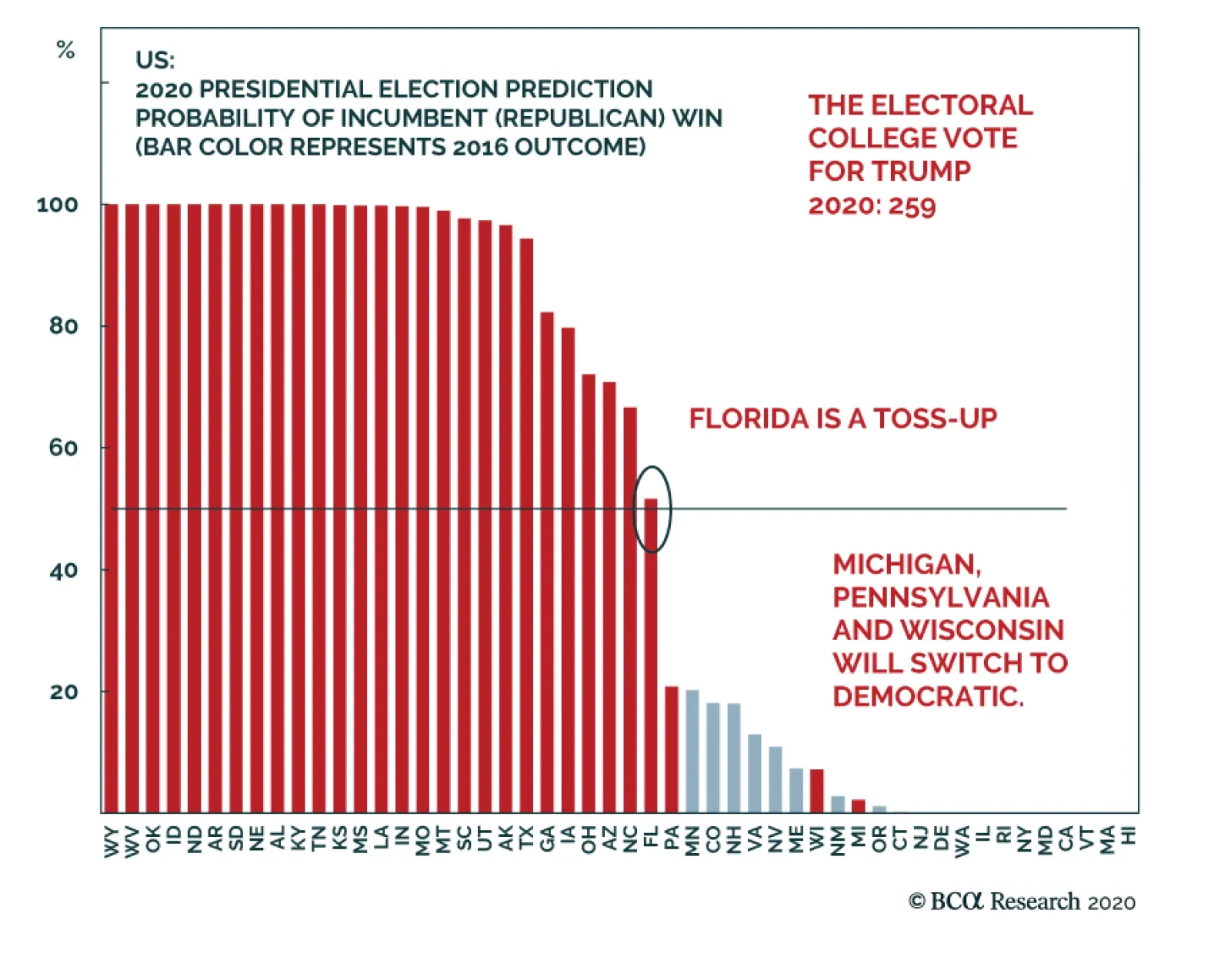

Following the recent Special Report we penned with our sister Geopolitical Strategy publication on a potential Democratic Party sweep in the US election, this week we address a common question from clients: What is the risk that President Trump refuses to leave the White House despite losing the election? We interpret this question more generally: What if the election is contested? A Contested Election? The odds of a contested election and legitimacy crisis are not small – they are bigger than a mere tail risk – perhaps 15%. However, at present all polling information and economic data suggest that President Trump will be defeated soundly, thus making a contested election unlikely (Chart 2). Our quantitative election model used to rank New Hampshire, Pennsylvania, and Wisconsin as “toss up” states, in which Trump had a 45%-55% chance of winning the state. Our latest update of the model, with June economic data, contains zero toss-up states, implying that Trump has less than a 45% chance of winning any of these states, or even Florida. The model projects that Trump will lose, receiving only 230 Electoral College votes (Chart 3). If the election were held today, there would be little risk of a contested outcome. The risk of a contested election hinges on Trump making a big comeback between now and November 3 that would tighten the election in at least two swing states (e.g. Florida and the Midwestern states). This is not impossible if one accepts our base case that he gets another ~$2 trillion in fiscal stimulus passed through Congress in early August and the V-shaped economic rebound continues. Chart 2Polling And Economic Data Suggest Significant Victory For Biden

What Is The Risk Of A Contested US Election?

What Is The Risk Of A Contested US Election?

Chart 3Quant Model Also Points To Trump Loss And Zero Toss-Up States

What Is The Risk Of A Contested US Election?

What Is The Risk Of A Contested US Election?

A tighter race could then produce vote recounts and judicial interventions in one or more swing states on November 3-4. In an environment of extreme polarization, either President Trump or former Vice President Joe Biden would refuse to concede while recounts are underway and their vast armies of lawyers dispute the results in court. We assess that the risk of a Trump comeback and victory is about 35%-42%, so the 15% risk of a contested outcome is a subset of that 35%-42% probability. Our quantitative model gives 17% odds to a scenario in which Pennsylvania, Florida, Minnesota, and even Colorado become toss-up states again. This scenario serves as a proxy for a contested election because it creates several chances for contested results. The model also gives surprisingly high odds to an Electoral College tie of 269-269 votes due to the fact that several scenarios involve swing states that could produce this result.1 If the margins of victory prove narrow, like in 2000, then it is virtually certain that the losing candidate will not concede the election until votes have been recounted at least once. Extreme levels of political polarization combined with abnormal voting circumstances (COVID-19, mail-in voting, etc) suggest that results are more likely to be contested than usual. How would a contested election be resolved? In general, the constitution is more effective than the consensus holds. The market is likely to overreact, creating a buying opportunity for risk assets. The US possesses the world’s oldest continuously operating constitution. It is very robust. The Supreme Court and Congress will intervene, if necessary, to determine the succession of the presidency. The Supreme Court would intervene to settle disputes over recounting votes as it did in 2000. Already this year the high court has intervened to prevent “faithless electors” in the Electoral College, reducing one major source of uncertainty. The core institutions of the state would uphold the result. Similarly, Congress would intervene in the event of an Electoral College tie. Specifically the House of Representatives would vote to determine the next president. The voting procedure would involve each state delegation receiving a single vote. As such it would favor the Republican candidate despite the fact that the Democrats have a majority of seats in the House. The military is sworn to protect the constitution and would be available to enforce the transfer of power once the constitutional branches have spoken. But it is highly unlikely that the occupancy of the Oval Office would have to be effected by federal armed forces. Grievances on the losing side would persist for a long time and take a toll on the legitimacy of the next administration. This is particularly the case if Democrats lose, given that they are likely to win the popular vote. This could have market implications – e.g. driving a weak president to act abroad because he is constrained at home. But the state would have a legal leader and would continue to function. Financial markets would not be as confident or knowledgeable about the constitution so they could panic during a constitutional crisis. We fully expect volatility to rise (as mentioned in a recent webcast in case of a stalemate), risk assets to sell off, and safe haven flows to increase throughout the process of a contested election (bottom panel, Chart 4). Traditionally, the US dollar and US Treasury bonds rally during politically induced risk-off periods (second panel, Chart 4). Since COVID-19 we have seen counter-trends in which investors veer away from the USD due to the narrowing in interest rate differentials and the booming twin deficits. So the short-term reaction may be at odds with the long-term trend. We would expect the greenback to rally during the rise in uncertainty and then collapse once the final decision is determined. This is what occurred in 2000, with the exception of USDJPY (Chart 5). Chart 4Heed The…

Heed The…

Heed The…

Chart 5…2000 Election Parallels

…2000 Election Parallels

…2000 Election Parallels

Therefore, we would position for the USD to be flat, or up, in case of a deadlock in this year’s election (middle panel, Chart 4), and for the 10-year Treasury bond and other safe haven assets to catch a bid. However, cyclically the path of least resistance is lower for the trade-weighted US dollar. Gold should also perform well (fourth panel, Chart 4). First, gold generally rallies during political and geopolitical crises. Second, gold stands to benefit if a US constitutional crisis prompts global investors to diversify from the US dollar specifically. Third, a contested election does not change the fact that both candidates are fiscally profligate and the ultimate winner of the White House will double down on economic stimulus to help consolidate power and fend off the recession. In other words, a contested election is not deflationary, so gold should benefit. A Closer Look At Markets During The 2000 Election Crisis Taking a closer look at the 2000 election impasse is instructive. The top panel of Chart 4 shows that the SPX drifter lower in the aftermath of the election falling roughly 10%. Granted, stocks were also deflating from the dotcom bubble bust. Thus, it is reasonable to expect turbulence going into the election and in the weeks following the election. The equity volatility curve concurs as VIX futures currently have a hump for the months of September and October (Chart 6). Chart 6Buy December VIX Futures As A Hedge

What Is The Risk Of A Contested US Election?

What Is The Risk Of A Contested US Election?

One way to play a contested election is to buy the December VIX futures and short the January ones at a positive carry. Alternatively, buying the December futures straight up as a hedge to long equity positions makes sense, but that is a more expensive proposition. Geopolitical Strategy is going long December VIX futures versus the January ones. Defensive sectors caught a bid (with the exception of telecom services that were deflating alongside their TMT bubble peers, Chart 7), while technology and financials (the two largest S&P 500 sectors at the time) suffered a sizable setback (Chart 8). Chart 7Sector Performance…

Sector Performance…

Sector Performance…

Chart 8…During Last Contested Election

…During Last Contested Election

…During Last Contested Election

Surprisingly, within deep cyclicals, tech bore the brunt of the fall. Chart 8 shows that industrials, materials and energy stocks were on the ascent in November 2000. As a reminder, we recently downgraded financials to neutral and while we recommend a benchmark allocation in tech stocks we continue to have a barbell portfolio approach preferring software and services to hardware and equipment. Moreover, we remain overweight the unloved and undervalued industrials and energy stocks, and this week we are lifting exposure to a modest overweight in the niche S&P materials sector by locking in gains and upgrading the heavyweight chemicals subgroup to neutral. Lift Chemicals To Neutral… It no longer pays to be bearish on chemicals stocks and today we are booking gains of 1% since inception, and lifting the materials heavyweight S&P chemicals index to neutral. Four key drivers are behind our change of heart: a depreciating US dollar, China’s reflation, improving domestic operating metrics and compelling valuations. Chart 9 shows the close correlation between the EURUSD and relative share prices. In early-May we highlighted that the US dollar was about to give way versus the euro as relative shadow rates started moving in the euro’s favor. We posited that “while the Fed would never admit to it, it is trying to devalue the US dollar and reflate the global economy, which will indirectly boost S&P 500 revenues… as 40% of SPX sales are internationally sourced”. This could not be truer for US chemical manufacturers. Currently exports are sinking like a stone, but the slingshot recovery in the euro suggests that chemical exports will rebound in the back half of the year (bottom panel, Chart 9). China’s ongoing recovery also gives credence to this export rebound thesis. In fact, the Chinese authorities are injecting large amounts of liquidity, which is already bearing economic fruit. Chart 9Preparing For A Positive Chemical Reaction

Preparing For A Positive Chemical Reaction

Preparing For A Positive Chemical Reaction

Chart 10 shows that not only is the Chinese manufacturing PMI expanding anew (soft data), but also electricity generation is coming back to life (hard data). This backdrop is a boon to US chemical exports and is neither reflected in sell-side analysts’ relative forward sales nor profit estimates (bottom panel, Chart 10). Chart 10Export Lift Looms

Export Lift Looms

Export Lift Looms

On the domestic front, chemicals rail car loads are making an effort to bottom and the surge in the ISM manufacturing survey points to a significant pickup in railroad chemical shipments in the coming months (second panel, Chart 11). Importantly, chemicals industrial production is on the verge of expanding, in marked contrast with overall IP that is still falling at a 10%/annum rate (third panel, Chart 11). On the profit margin front, a big tug of war has enveloped chemicals producers. While selling prices are mired in deflation, executives have been very careful with headcount and continue to adjust input costs to lower run rates (Chart 12). Recent news of Dow Inc. shedding its labor force suggest industry CEOs remain very disciplined and focused on a return to profitability. Chart 11Firming Domestic Conditions

Firming Domestic Conditions

Firming Domestic Conditions

Chart 12Big Tug Of War

Big Tug Of War

Big Tug Of War

Importantly, the American Chemistry Council’s Chemical Activity Barometer is corroborating all this marginally firming industry data and signals that relative forward profitability is likely nearing a trough (bottom panel, Chart 11). Tack on a fall below the neutral zone on our relative Valuation Indicator and it no longer pays to be bearish chemicals manufacturers (bottom panel, Chart 12). In sum, a depreciating US dollar, China’s rebounding economic activity, improving domestic operating metrics and compelling valuations entice us to lift the S&P chemicals index to neutral. Bottom Line: Crystalize gains of 1% in the S&P chemicals index since inception and upgrade to neutral. The ticker symbols for the stocks in this index are: BLBG S5CHEM – LIN, APD, ECL, SHW, DD, DOW, PPG, CTVA, LYB, FMC, IFF, CE, ALB, CF, EMN, MOS. …Which Boosts Materials To An Above Benchmark Allocation Our S&P chemicals index upgrade to neutral also lifts the S&P materials sector to overweight. We are positioning our portfolio for an eventual equity market sector rotation away from tech stocks and toward traditional deep cyclicals including materials, energy and industrials. We want to be ahead of the curve as we expect a violent rotation and the likely catalyst will be a definitive vaccine breakthrough announcement. Such a backdrop will unlock excellent value in a plethora of deep cyclical names that have been laggards, materials stocks included. Importantly, global mining behemoths are already sniffing out a robust global economic recovery, with BHP and RIO trouncing the global bourses since the March 23 trough (Chart 13). Emerging markets have also started to outperform the SPX in common currency terms, as the demise of the US dollar is becoming a mainstream theme. Chart 13Global Miners Sniffing Out Global Recovery

Global Miners Sniffing Out Global Recovery

Global Miners Sniffing Out Global Recovery

The JP Morgan EM FX index, Bloomberg’s EM Asian currency index (ADXY) and the China-levered AUDUSD are all in V-shaped recoveries, underscoring that global growth will make a sizable comeback as the year draws to a close (top & second panels, Chart 14). The USD debasing will lift materials exports and thus bodes well for the relative profit recovery in this deep cyclical sector (third & bottom panels, Chart 14). Not only will US materials profits get a boost from garnering a larger slice of the global export pie, but also materials revenues will rise on the back of an increase in commodity prices that are priced in US dollars (top & second panels, Chart 15). Chart 14Depreciating Dollar To The Rescue

Depreciating Dollar To The Rescue

Depreciating Dollar To The Rescue

Chart 15Chinese Recovery A Boon To S&P Materials

Chinese Recovery A Boon To S&P Materials

Chinese Recovery A Boon To S&P Materials

True, China’s insatiable appetite for commodities has taken a small breather, but it would be a mistake to write off this economy and the government’s power to successfully restart its engine. Chinese authorities are working on rekindling growth by injecting significant liquidity in order to jump start the economy. Money supply growth is shooting higher after kissing off the zero growth line earlier in the year. We would not be surprised if M1 growth makes a run for the 2016 highs when it surpassed the 25%/annum mark (third panel, Chart 15). Finally, on the domestic operating front, industry executives have been reining in labor costs of late as the COVID-19 pandemic has wreaked havoc in final demand. The materials sector wage bill is now contracting at 4%/annum a level last seen in the Great Recession. This input cost restraint will underpin industry profitability (bottom panel, Chart 15). All of this positive news will arrest the near uninterrupted de-rating of the niche materials sector that followed the reflex rebound in the aftermath of the GFC. Currently, our relative Valuation Indicator is hovering in the middle of the neutral and undervalued zones an area that has marked previous valuation bottoms five times in the past two decades (third panel, Chart 16). Our materials sector Cyclical Macro Indicator does an excellent job in encapsulating all these moving parts and the current message is positive for relative share prices (second panel, Chart 16). Netting it all out, an improving export backdrop, a depreciating greenback and commodity price inflation, labor cost discipline at home, along with a relative value proposition all argue for an above benchmark allocation to the S&P materials sector. Geopolitical Strategy recommends investors go long materials on a strategic time frame. Bottom Line: Upgrade the S&P materials sector to overweight, today. Chart 16Green Lights Flashing

Green Lights Flashing

Green Lights Flashing

Anastasios Avgeriou US Equity Strategist anastasios@bcaresearch.com Matt Gertken Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 Assuming the 2020 electoral map stays generally the same as in 2016, an Electoral College tie could be produced by Democrats winning AZ, MI, and either WI or MN; MI, MN, and WI plus NE’s Second District; or PA and MI plus NE’s Second District. Other variations are possible.

Highlights The epicenter of the new Middle East crisis is the Shia Crescent, which threatens global oil supply. However, the escalation of conflict in the Mediterranean is also relevant to global investors. The crises in Libya and the Eastern Mediterranean are escalating as President Erdogan makes a last attempt to benefit from his relationship with Trump before US elections in November. A breakup between Turkey and NATO is not our base case, but European sanctions against Turkey are likely. Turkish risk will rise. A revival in Libyan oil production would not be a meaningful risk to the recovery in oil markets. Stay strategically long Brent crude oil. Libya could become a “Black Swan” for market participants exposed to southern Europe, Turkey, and North Africa. We remain short our EM Strongman Currency Basket versus other emerging market currencies. Feature Dear Clients, This week we present to you a special report on Turkey by my colleague Roukaya Ibrahim, Editor, Geopolitical Strategy. Roukaya argues that President Erdogan is at a crossroads in which he will confront major military and economic constraints to his foreign policy adventurism. On Monday, July 27 you will receive a special report that I co-wrote with Anastasios Avgeriou, chief strategist of our US Equity Strategy. In this report we continue our analysis of the equity sector implications of the upcoming US election. Anastasios also provides analysis of two cyclical sectors that you may find of interest. On Friday, July 31 we will send you our regular monthly GeoRisk Update, which surveys our proprietary, market-based geopolitical risk indicators and what they imply for your portfolio. We trust you will enjoy these reports and look forward to your feedback. All very best, Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Chart 1Shia Crescent' Flailing Under Maximum Pressure And COVID-19

Shia Crescent' Flailing Under Maximum Pressure And COVID-19

Shia Crescent' Flailing Under Maximum Pressure And COVID-19

The Middle East is suffering a wave of instability after the COVID-19 crisis just as it did in the years after the 2008 financial crisis. The crises in Libya, Syria, and Yemen were never resolved and now new crises are emerging from Egypt and Turkey to Iran and Iraq. By contrast with the “Arab Spring” of 2011, the epicenter of the political earthquake this time around is likely to be the “Shia Crescent,” i.e. Iran, Iraq, eastern Saudi Arabia, Syria, and Lebanon. The US policy of maximum pressure on Iran, which is intensifying in the lead-up to the US election, has weakened Iran and its sphere of influence (Chart 1). Chart 2Dominant Arab States Also Face Struggles

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Meanwhile the pandemic and collapse in oil prices have destabilized the predominantly Arab states (Chart 2). Authoritarian regimes like Egypt and Saudi Arabia that consolidated power after the Arab Spring are more stable than they were but still vulnerable to external and internal forces. These cyclical developments are occurring against the backdrop of structural changes like the US’s energy independence and strategic pivot to Asia, which have created a power vacuum in the Middle East. The pivot to Asia is rooted in US grand strategy and has proceeded across partisan administrations, so it will continue. Indeed US-China tensions are escalating rapidly in 2020 despite the financial market’s lack of interest. Turkey and Russia are scrambling to take advantage of the US’s withdrawal and gain greater influence through regional proxy wars. This year has seen a marked escalation of their involvement in Libya, where the war is re-escalating and drawing in Egypt, Europe, and Gulf Arabs. At minimum a Mediterranean conflict could affect oil prices as well as Turkish, Russian, and other regional financial assets. At maximum it could affect European assets, which are exposed to geopolitical risk in Turkey and North Africa. The Shia Crescent is the crisis’s epicenter, but Libya is also investment relevant. Bottom Line: The epicenter of the new Middle East crisis is the Shia Crescent, which threatens global oil supply. However, the escalation of conflict in the Mediterranean is also relevant to global investors, primarily through its potential to impact European assets. Re-Escalation In Libya The Libyan crisis has been escalating since the beginning of the year and is on the verge of turning into a major multilateral conflict. The risk now is that Egypt, another regional power, will intervene in Libya against Turkey in a battle for North African hegemony (Map 1). Map 1Libya Could Become A "Black Swan" Event

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Several incidents since we outlined Egypt’s red lines on the Libyan conflict suggest that Cairo and Ankara will clash in Libya (Table 1). Table 1Egypt And Turkey Up The Ante In Libya

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

While Egypt has declared Sirte and al-Jufra as red lines, threatening military intervention if crossed, Turkey is calling for the Libyan National Army’s (LNA) withdrawal from these regions as a precondition for a ceasefire (Map 2). Egypt is allied with General Khalifa Haftar’s Libyan National Army, which is based in Benghazi and holds parliament in Tobruk. Map 2Libya’s Battlefront Is Closing In On The Oil Crescent

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

The next move is now in Turkey’s hands. The escalation depends on whether it insists on moving forward toward Egypt’s red line. Turkey’s recent movements do not suggest it is backing down. True on July 21, and again on July 22, top officials from Turkey’s foreign ministry referred to a political solution as being the only solution in Libya. However, these statements were made while Turkey held diplomatic meetings with Niger and Malta that could be aimed at establishing airbases there.1 At its core, the conflict in Libya is a clash between the two dominant geopolitical forces in the Middle East. On the one hand, Turkey and Qatar are independent economic forces to Saudi Arabia and supporters of political Islam. On the other hand, Saudi Arabia, the UAE, and Egypt form an economic bloc and support Saudi religious authority and political authoritarianism. Bottom Line: The crisis in Libya is heading toward an Egypt-Turkey confrontation. Be ready for an escalation. Egypt Has More To Lose Than Turkey In Libya Both Egypt and Turkey are nearing a point of no return in Libya. A last-minute change of heart from either side would be increasingly more humiliating, both domestically and regionally. Chart 3Defeat In Libya Would Accelerate Erdogan’s Decline

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

While Egypt’s geographic proximity to Libya makes it more interested in what goes on there and will give it a home advantage in any military confrontation, Egypt’s military may be overstretched as it is also at risk of conflict with Ethiopia over water resources.2 For Egypt, a victory would resuscitate its position as a regional power, bringing about a new era of greater Egyptian regional leadership. It would silence domestic skeptics who argue Egyptian President Abdel Fattah al-Sisi’s rule is based on the illegitimate ousting of Egypt’s only democratically elected leader. It would squash any prospect of a revival of the Muslim Brotherhood in Egypt and validate authoritarian rulers in the region. It could also annul the recent Libya-Turkey maritime demarcation agreement – a positive for Egypt’s natural gas ambitions. A loss would be a wake-up call for Egypt’s military, which has been spending scarce funds on costly equipment. It may also result in a change in leadership in Egypt or at the very least weaken al-Sisi’s domestic power and Egypt’s regional clout. The regime would persist over the short and medium term, but it would suffer a loss of legitimacy and the underground domestic opposition would intensify, creating a long-term threat. A complete defeat of LNA forces would pose a major security risk. Haftar’s LNA acts as a buffer between Egypt and unfriendly militias in Western Libya. Turkey does not have a vital national strategic interest in Libya and therefore the constraint pushing against on a protracted conflict is stronger than it is for Egypt. Given that Turkey is a democracy, President Recep Tayyip Erdogan has more to lose in the case of a military defeat. It would accelerate the decline in his popular support and that of his Justice and Development Party (AKP) (Chart 3). A conflict with Egypt is therefore a gratuitous gamble. However, victory would vindicate Erdogan’s efforts to create a strongman regime and revive memories of the great Ottoman empire.3 Such an accomplishment could mark a major turning point for Erdogan. His domestic blunders would be forgiven and he would be able to claim that he is one of the great leaders of Turkey. Given that Turkey lacks strategic necessity in Libya, and a defeat could dislodge Erdogan in 2023, one should expect Turkey not to cross Egypt’s red lines. However, Erdogan’s rule has been characterized by hubris, nationalism, and foreign assertiveness to distract from domestic economic mismanagement. Therefore we cannot have a high conviction that Turkey will bow to its political and military constraints. The risk of a large conflict is underrated. Bottom Line: Egypt has greater national interests at stake in Libya than Turkey. The implication is that Turkey should recognize Egyptian red lines. However, Turkey’s decision to intervene in Libya suggests that Erdogan could overreach. Libya could become a “Black Swan” for market participants exposed to southern Europe, Turkey, and North Africa. Will Turkey Break With NATO? Since signing the maritime and military cooperation agreements with Libya on November 27, Turkey has raised its stakes in Libya. Ankara has sent more armed drones, surface-to-air missile defense systems, naval frigates, a hundred officers, and up to 3,800 Syrian fighters. It has rolled back all of the strategic gains that the Libyan National Army made in 2019. The timing of the recent escalation is significant. The US election cycle offers Erdogan a chance to increase Turkey’s foreign assertiveness with minimal US retaliation. US-Turkish relations have been icy for years. Turkey is an ascendant regional power that is pursuing an increasingly independent national policy, while the US is no longer as dominant of a global hegemonic power capable of enforcing discipline among minor allies. The US alliance with the Kurds in Syria and Iraq has alienated Turkey. The 2016 Turkish coup attempt also increased the level of distrust between the two states. However, President Trump’s personal and political affinity for President Erdogan has resulted in a permissive policy toward Turkey. Trump seeks to distance the US from conflicts in Syria and Libya inherited from his predecessor. He has little commitment to the Kurds. More broadly he has embraced geopolitical multipolarity and avoided telling Erdogan what to do. The Trump administration has not retaliated against Turkey for purchasing Russia’s S400 missile defense system or for pursuing expansive maritime-territorial claims near Cyprus. Even though the Turkish arms purchase makes it eligible for sanctions under the Countering America’s Adversaries Through Sanctions Act (CAATSA), the Trump administration has yet to impose sanctions. Senator Lindsey Graham, who is close to the Trump administration, suggested in July 2019 that sanctions could be avoided if Turkey did not activate the system.4 Turkey, for its part, has yet to activate the system three months after the April target date for activation. Turkey blames the delay on COVID-19. With regard to Libya, the Trump administration has remained largely on the sidelines. It has promised to reduce American commitment to overseas conflicts and has criticized the Obama administration’s intervention in Libya in 2011 to bail out the European allies. Officially the US is aligned with Fayez al-Sarraj’s UN-backed Government of National Accord (GNA), but so far its role has been minimal, refraining from providing any military support. Moreover, Washington’s key allies in the region – Egypt, Saudi Arabia, the UAE, even France – support the Libyan National Army. Libya could become a “Black Swan” event. It is Haftar’s other main backer – Russia – that would present an incentive for greater American involvement. The US African Command reports that two thousand Russian mercenaries from the Kremlin-backed Wagner Group have fought in Libya. The US also reported in June that at least 14 MiG29 and Su-24 Russian warplanes were sent to Libya via Syria, believed to be located in the al-Jufra airbase. Moreover, the US State Department has accused Russia of printing billions of fake Libyan dinars to fund Haftar’s forces.5 The Trump administration has been permissive toward Russia as well as Turkey, letting them work out deals with each other, but US electoral politics could prompt Trump to make shows of strength against Russia to fend off criticism. Thus the months in the lead up to the US elections offer the Turkish leader what may be a closing opportunity to increase the country’s foreign assertiveness with minimal US retribution. If Trump loses, Erdogan may face a less sympathetic Washington. By contrast France, also a NATO ally, has taken a stronger position against Ankara over its involvement in Libya. Relations with other eastern Mediterranean countries have also been rocky due to Turkey’s exclusion from gas deals in the region and drilling in disputed waters near Cyprus and Greece. France has a commercial interest in Libya’s oil industry and backs Haftar’s Libyan National Army to some extent.6 Citing aggressive behavior by Turkish warships after an encounter in the Mediterranean, France suspended its involvement in NATO’s Operation Sea Guardian on July 1.7 France has also demanded EU sanctions against Turkey – both for its drilling activities around Cyprus as well as for its role in Libya.8 Still, Europeans have little appetite for direct intervention in Libya. The leaders of France, Italy and Germany have threatened sanctions against foreign states that violate the arms embargo in Libya. This warning comes after EU foreign ministers agreed to discuss the possibility of another set of sanctions against Turkey in their August meeting if Turkey persists in converting the Hagia Sophia from a museum to a mosque. Despite the fracturing within NATO, the alliance will not break up. Turkey’s geographic proximity to Russia, large number of troops, and military strength make it an essential member of the defense treaty (Chart 4). Chart 4NATO Will Not Break With Turkey

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Instead, the Europeans will retaliate against Erdogan’s foreign adventurism through sanctions, while maintaining the NATO alliance. This acts as a cyclical rebuke without damaging the secular relationship. Europe will use sanctions to retaliate against Turkey’s provocations. The Europeans will be particularly rattled if Turkey succeeds in its North African endeavor and amasses significant regional power as a result. Victory in Libya would make Turkey the gatekeeper to two major migrant entry points to the European continent, providing Ankara with leverage in its negotiations with Europe (Chart 5). It would also increase the likelihood that Turkey increases its assertive behavior in the Eastern Mediterranean, where Israel, Egypt, Greece, Cyprus, and Italy are seeking to develop a natural gas hub. Chart 5Turkish Victory In Libya Would Rattle Europe

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Although Erdogan shows no signs of backing down, constraints suggest that Erdogan may pull back from being perceived as overly provocative. The Turkish economy is highly dependent on Europe in trade and capital flows (Chart 6). Thus unlike American sanctions, which have little bearing on the Turkish economy short of radical financial measures, European sanctions suppress any chance of an economic recovery. Chart 6European Sanctions Would Reverse Turkey's Recovery

European Sanctions Would Reverse Turkey's Recovery

European Sanctions Would Reverse Turkey's Recovery

Chart 7Erdogan Risks Popularity By Overstepping In Libya And East Med

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Turkey’s frail economy and crackdown on opposition parties could weigh on Erdogan’s approval, which is losing its COVID-induced bounce (Chart 7). Thus, as in the case of Egypt, Erdogan should recognize these constraints and reduce his foreign assertiveness. If he does not, then he will hit up against material constraints that will harm the Turkish economy. Bottom Line: The Libyan crisis is escalating as Erdogan makes a last attempt to benefit from his relationship with Trump before US elections in November. Washington’s detached stance in Libya highlights that its foreign policy priorities lie elsewhere – in Asia and Iran. Meanwhile, Europe is divided over Libya. A breakup between Turkey and NATO is not our base case, but new European sanctions against Turkey are not unlikely. A Turkish victory in Libya would lead to a significant escalation in tensions between Turkey and the West. Investment Implications Turkish geopolitical risk is set to rise in the lead up to the November US elections as Turkey becomes increasingly embroiled in foreign conflicts – in Libya, Syria, Iraq, and most recently in the Azerbaijan-Armenia conflict (Chart 8). Ankara’s more provocative stances raise the risk of sanctions from the US and more significantly from the EU. This would hurt Turkish risk assets at a time of already heightened vulnerability. If Turkey manages to secure a victory in Libya, it would benefit economically from construction and energy contracts there. However, it would also result in a significant uptick in geopolitical tensions in the Middle East as the West and the West’s regional allies will be disturbed by Ankara’s expanding influence. Stay short our EM Strongman Currency Basket composed of the Turkish lira, Philippine peso, and Brazilian real versus other emerging market currencies. Even though the lira is already cheap against the US dollar, it faces more downside due to the risks highlighted in this report and the massive growth in money supply in Turkey. Similarly, the prospect of a military confrontation will raise the equity risk premium priced in Egyptian stocks. Egypt will continue underperforming emerging markets as long as it remains invested in an unsettled conflict in Libya (Chart 9). Chart 8Turkish Risk Will Rise

Turkish Risk Will Rise

Turkish Risk Will Rise

Libyan oil exports are unlikely to stage a major revival anytime soon (Chart 10). Although the Libyan National Oil Company lifted force majeure on July 10, Haftar’s Libyan National Army reintroduced the blockade a day later. Clashes are also occurring near oil facilities in the Brega region where Syrian, Sudanese, and Russian Wagner Group mercenaries currently have a presence. Chart 9Egyptian Risk Assets Will Underperform

Egyptian Risk Assets Will Underperform

Egyptian Risk Assets Will Underperform

Chart 10Libyan Oil Handicapped By Haftar’s Blockade

Erdogan’s Neo-Ottoman Bid Hits Constraints

Erdogan’s Neo-Ottoman Bid Hits Constraints

Chart 11Stay Bullish Euro Over The Long Run

Stay Bullish Euro Over The Long Run

Stay Bullish Euro Over The Long Run

Even in the best-case scenario, in which force majeure is promptly lifted, the blockade damaged both the reservoirs and oil and gas infrastructure, preventing a resurgence of exports to pre-January levels. The Libyan National Oil Company warned that unless oil production restarts immediately, output will average 650,000 barrels per day in 2022. This is significantly less than the over 1 million barrels per day just prior to the blockade, and the 2.1 million barrels per day Libya had planned to produce by 2024. In any case these figures pale in comparison to the production curtailments currently in place by OPEC 2.0, which are set to decrease to 8.3 million barrels per day beginning in August from 9.6 million barrels per day now. Given OPEC 2.0’s demonstrated commitment to production discipline, a revival in Libyan oil production is not a meaningful risk to the recovery in oil markets. We remain strategically long Brent crude oil, which is up 78% since inception in March. This trade could experience near-term volatility due to any hiccups in global economic stimulus or risk-off events from geopolitical risks. But over a 12-month time frame we expect oil prices to rise higher. BCA Research’s Commodity & Energy strategists expect Brent prices to average $44/bbl in 2H2020, and $65/bbl in 2021. The recent rise in the euro is rooted in global macro and structural factors but a major Mediterranean crisis and/or other geopolitical risks we have highlighted surrounding the US election cycle could create headwinds in the short term. Over the long run we are bullish euro (Chart 11). Roukaya Ibrahim Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com Footnotes 1 In Niger, Turkish Foreign Minister Mevlut Cavusoglu met with his Nigerien counterpart and stated the two states’ willingness to boost bilateral relations in agriculture, mining, energy, industry, and trade. A day earlier, Turkey and Qatar’s defense ministers met with Libya’s minister of interior in Ankara to discuss the situation in Libya. And on July 20, a trilateral meeting was held between Turkey’s defense minister, Libya’s interior minister, and Malta’s minister of home affairs and national security. The inclusion of Malta – located just north of Libya in the Mediterranean – is perplexing. The three discussed defense cooperation and efforts toward regional stability and peace. These recent meetings could suggest that Turkey is negotiating agreements to fortify its strategic approaches to Libya. This could involve greenlighting airbases in Niger and Malta in exchange for economic support and Qatari funding. 2 The latest developments suggest that the Egypt-Ethiopia conflict is de-escalating. On July 21, Ethiopian Prime Minister Abiy Ahmed tweeted that Egypt, Ethiopia and Sudan had reached a “common understanding on continuing technical discussions on filling.” But Ethiopia will have an opportunity if Egypt becomes embroiled in Libya. 3 The Turks ruled Tripolitania from the mid-1500s until Italy’s 1912 victory in the Italo-Turkish War. Surveys conducted by Metropoll reveal that the share of Turks with a positive perception of Turkey’s active role in Libya shot up to 58% in June from 35% in January. 4 Senate Majority Whip John Thune has even proposed using the US Army’s missile procurement account to buy the Russian missiles from Turkey, thus reducing tensions between the two NATO allies. This is unlikely to occur because it would look politically weak in the US, while Turkey would face Russian pressure. The US suspended Turkey from the F35 Joint Strike Fighter program, banning it from purchasing F35s, and removing it from the aircraft’s production program. US Secretary of Defense Mark Esper stated that the US would only consider allowing Turkey back into the F35 Joint Strike Program if the Russian defense system were moved out of the country. The Turkish purchase of the Russian defense system was partly driven by the need to work with Russia and partly driven by Erdogan’s desire to reduce the risk of another coup attempt. Ankara was indefensible against the Turkish Air Force’s F-16s during the 2016 coup attempt since its military relies heavily on US built missile defense. 5 Moscow has denied all allegations of involvement in Libya. 6 US-made javelin missiles purchased by France were found at the pro-Haftar base in Gharyan in June last year, raising suspicion that France was backing Haftar’s offensives. 7 On June 10, French frigate Courbet approached a Tanzanian-flagged ship heading to Libya in suspicion that it was violating the UN arms embargo. France accused three Turkish vessels that were escorting the Tanzanian vessel of harassment by targeting the Courbet’s fire control radars. Turkey denied harassing the Courbet and maintains that the Tanzanian vessel was transporting humanitarian aid to Libya. A NATO investigation into the incident was inconclusive. 8 The EU agreed to impose sanctions on two Turkish oil company officials in February in protest against Turkish drilling activity in the Eastern Mediterranean. However these sanctions are mostly just political symbolism.

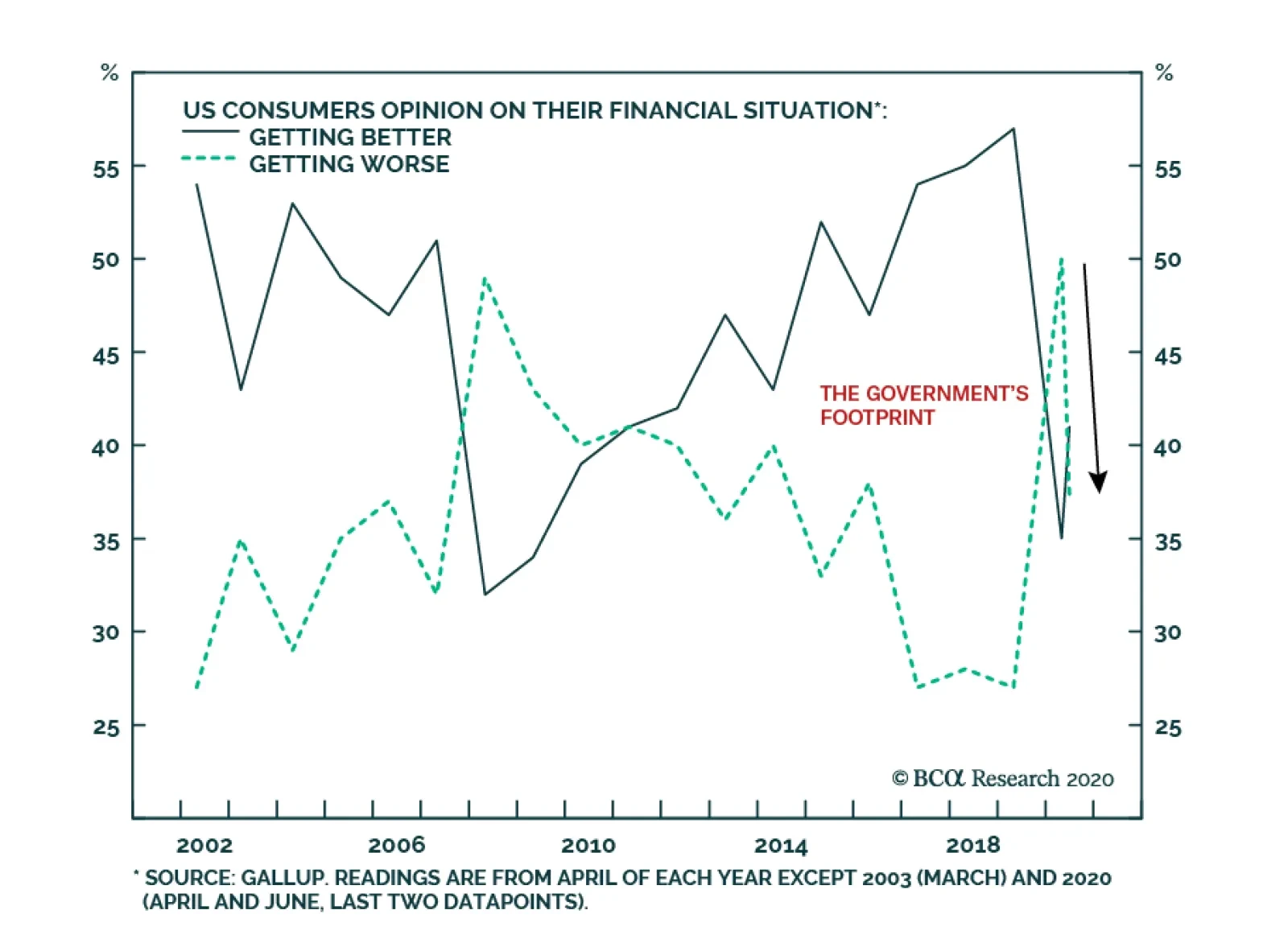

Gallup regularly surveys American households about their financial situation. In April, the largest proportion of US households since the Great Financial Crisis felt that their financial situation was deteriorating. Gallup conducted the survey once again in…

BCA Research's Geopolitical Strategy service collaborated with Elmo Wright a former senior civilian executive at the US Army National Ground Intelligence Center. Elmo’s work for this report is in his personal capacity and does not represent any position of…

Dear Clients, This week we offer you a Special Report on Russia and cyber security by our colleague and friend, Elmo Wright. Elmo recently retired from US Army civil service after 43 years working in intelligence, either on active duty, reserves, or as a civilian. From 2018 to 2020, he served as the senior civilian executive at the US Army National Ground Intelligence Center. He has served on five continents and provided analysis of the most pressing global trends in national security and intelligence. In this Special Report with BCA’s Geopolitical Strategy team, Elmo analyzes Russia’s cyber capabilities and argues that structural and cyclical factors, including COVID-19, will ensure the continued salience of Russian and global cyber security challenges in the coming years. His thesis reinforces our recommendation that investors buy cyber security equities. Elmo’s work for this report is in his personal capacity and does not represent any position of the US government. Only publicly available information was used as background research material for Elmo’s contribution to the report. All very best, Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Highlights As the US elections come closer, there will be a return to news about Russia and its potential interference via social media. Russia will continue to use cyber, both state sponsored attacks, and in coordination with criminal groups, to advance Russian national security objectives. In contrast to nuclear doctrine, there is no commonly accepted framework for cyber warfare between Russia and other nations that provides understandable signals for escalation, de-escalation, appropriate targets, or goals. US efforts to conduct military operations against Russia or China would likely be countered by Russian or Chinese cyber operations before any physical military operations could be initiated. Cyber security stocks offer a way for investors to capitalize on our long-term themes of nationalism, multipolarity, and de-globalization. The ISE Cyber Security Index offers value relative to the broad NASDAQ and S&P 500 indexes as well as the S&P tech sector. Feature As the national elections in the US come closer, there will be a return to news about Russia and its potential interference via social media. Indeed Russia is making headlines even as we go to press. This report aims to provide context for Russian cyber capabilities in general as a contributor to overall geopolitical instability (Chart 1). We forecast Russia will continue to use cyber, both state sponsored attacks, and in coordination with criminal groups, to advance Russian national security objectives. Chart 1Russian Cyber Interference Resurfaces Around US Elections

Russian Cyber Interference Resurfaces Around US Elections

Russian Cyber Interference Resurfaces Around US Elections

As background, the word cyber is commonly accepted to be derived from cybernetics, a phrase attributed to Norbert Wiener, an MIT scientist. The phrase itself is related to the ancient Greek word for steering or helmsman, in other words, control. Chart 2Russian Excellence In Math Makes It Competitive In Cybernetics

Russia And Cyber Security After COVID-19

Russia And Cyber Security After COVID-19

Russia has a long history of excellence in science, especially theoretical work in mathematics and physics (Chart 2). Those fields can explain natural phenomena in formulas and mathematical relationships. The Soviets believed that centralized state planning that manipulated data in formulas could lead to better outcomes in all aspects of the society. Although central state economic planning did not work out for the Soviet economy, Soviet military science built on the concept of data relationships in formulas to develop its theory of troop control, a derivative of reflexive control, that is, the presenting of data to the recipient, either friendly or enemy, in order to get that recipient to act in a way favorable to Soviet military plans. One can see the Soviets embraced the idea of cybernetics as very congruent to their desire for top down control. Russia, as the core part of the Soviet Union, retained significant numbers of scientists and mathematicians who were naturally drawn to the ability of computers to take data and manipulate that data according to formulas. Other Russian scientists and mathematicians emigrated to the West where their expertise was rewarded in the rise in the use of computers to manipulate data. Over time, the term cyber has come to be associated with many aspects of computers, especially the intellectual and physical structures hidden behind the direct interface of a person with a keyboard and screen. Russian expertise in the use of computers to do cyber work was not limited to working for the State. As the Soviet Union broke apart and many people lost their jobs working for the State, there were those persons who took their talents to criminal ventures. And in the symbiotic nature of society in Russia, many of those who went into criminal ventures were former intelligence and security personnel who could maintain their connection to the official organizations that were successors to the KGB, the GRU, and others. Senior Russian military officials, such as General Valery Gerasimov, Chief of the General Staff of the Russian Federation armed forces, equivalent to the US Chairman of the Joint Chiefs of Staff, have noted the growth of nonmilitary means of achieving strategic goals, and specifically in the information space. Gerasimov, in an article in 2013, has been widely quoted that all elements of national power have to be harnessed, including cyber capabilities. One Soviet and Russian military concept that relates to the information space is maskirovka, the use of camouflage, deception, and disinformation to confuse the enemy. Maskirovka is intimately connected with the Soviet/Russian concept of “active measures”. Active measures include actions taken generally by intelligence services to provide propaganda, false information, and otherwise sow discord and confusion among the enemy ranks at all levels of war as well as in the political, economic, and social spheres. In today’s time period, cyber, especially social media, offers the opportunity for the wide spread of aspects of maskirovka and active measures to all users, as well as targeted groups (Chart 3). Reporting indicates a continued Russian emphasis on cyber as a means for active measures concealed by maskirovka. Chart 3Social Media Offers Russia An Opportunity For The Spread Of Maskirovka

Russia And Cyber Security After COVID-19

Russia And Cyber Security After COVID-19

Wikileaks has provided a platform for the dissemination of information normally hidden from the general public. It is noteworthy how much of the information on the Wikileaks platform relates to the US and the West, and relatively little on Russia. Possible factors that explain that characteristic include the disparity in penalties for disclosing information between the US and the West versus Russia; the greater number of journalists and other persons involved in the media, both for profit and personal reasons, in the West; and the language barriers involved in understanding Russian versus English. A final possible factor in Wikileaks greater dissemination of Western information might be an aspect of active measures undertaken by Russia. Russia is the source of the most sophisticated cyber threats to the US. There are numerous actions attributed to Russian state actors in the cyber field in the recent past (Table 1). They include a distributed denial of service attack on Estonia (2007); hacking the Ministry of Defense in the country of Georgia during a military conflict (2008); attacks on Ukrainian energy infrastructure (2015); and the hacking of the Democratic National Committee (2016). Chancellor Angela Merkel recently publicly named and shamed Russia for a cyber-attack on Germany circa 2015 (Appendix). Table 1Russian State Actors Responsible For Many Of This Year’s Cyber Attacks

Russia And Cyber Security After COVID-19

Russia And Cyber Security After COVID-19

Senior US officials have cited Russia as the source of the most sophisticated cyber threats to the US, both for espionage and state sponsored attacks against US national security capabilities such as energy, transportation, and telecommunications infrastructure; as well as for criminal activity such as ransom ware and identity theft. Russian use of cyber, both state sponsored and sponsoring criminal actors, has been the top threat to the US in each of the US intelligence community’s annual threat assessments for 2017, 2018, and 2019 (Chart 4). Although the 2020 annual threat assessment was not made public in Congressional testimony, there’s little reason to suspect that Russian use of cyber would not continue to be cited as the top threat. Chart 4Russian Use Of Cyber Is A Top Threat To The US

Russia And Cyber Security After COVID-19

Russia And Cyber Security After COVID-19

Other nation states have state sponsored cyber capabilities which are of national security concern to the US, including China, Iran, and North Korea. These nation states are called out in the US intelligence community Annual Threat Assessments. Each of these nation states has been identified as committing intelligence and economic cyber attacks against the US and other Western nations. The recent speech by the Director of the Federal Bureau of Investigation designates China as the top threat. Given the nature of the internet, the pathway of a cyber attack will likely bounce around multiple countries before reaching its intended target. As the Director notes, forensic identification of the source of a cyber attack takes time and expertise. However, there is a clear record of specifically identifying the state sponsored entity that commits attacks on US or Western government information technology and infrastructure. More likely than confusing one state sponsored cyber actor from one country to another would be the potential blending of criminal elements across national boundaries. In this case, cyber criminal elements with Russian backgrounds or connections are clearly the most capable. The stages of cyber conflict include reconnaissance, penetration, mapping, exfiltration, and operations. The US National Security Agency has an extensive technical cyber threat framework which goes into much detail. Cyber security professionals note the ongoing actions in cyber space and the attempts by elements suspected to be linked to Russia to gain and maintain access to US networks for potential military operations, or to exfiltrate data for criminal or other purposes. Part of the frustration of cyber security experts is the lack of transparency and timely reporting of those affected by malign cyber activities. Although some cyber activities may go on for multiple months, the exfiltration of data, or the emplacement of malware may only take a few seconds. Many networks lack the ability to detect penetration and mapping. Companies with large resources devoted to cyber security may have that investment negated if they have affiliations with other companies with lax cyber security which can allow for hostile intrusions into the connected network. Unfortunately, public and open attribution for cyber attacks has lagged. As an example, although the attack on the Democratic National Committee email servers was noted in 2016, it was not until 2018 that specific Russian individuals were charged with the crime. Factors that cause lags in public and open attribution include the difficulty of tracing specific computer code through cyberspace; the disjointed nature of the internet; the lack of an easy and accepted mechanism for involvement of US intelligence agencies in providing assistance to private sector parties; and the reticence of individuals and organizations negatively affected by cyber attacks to publicly disclose their injuries. Chart 5Unlike Nuclear Doctrine, Cyber Lacks A Framework To Control Escalation

Russia And Cyber Security After COVID-19

Russia And Cyber Security After COVID-19

Doctrine for the use of nuclear weapons developed over a period of years in the US and the West and in the Soviet bloc. The Soviets developed a coherent doctrine for the use of nuclear weapons that was understandable to the West. Arms control agreements between nuclear powers established mechanisms for controlling escalation of tensions (Chart 5). The Soviet doctrine was adopted by the Russians after the breakup of the Soviet Union. Russia and Western nations continue to have a common understanding of the role of nuclear weapons in military affairs that allows for discussion of escalation and de-escalation. In contrast to nuclear doctrine, there is no commonly accepted framework for cyber warfare between Russia and other nations that provides understandable signals for escalation, de-escalation, appropriate targets, or goals. This is reflected in the Russian information security doctrine of 2016 which notes “The absence of international legal norms regulating inter-State relations in the information space…” The US Director of National Intelligence also noted this lack of agreement in his annual threat assessment testimony of 2017. The rapid growth of the internet, and reliance on it by government and private sectors reflects its founding as an open system, vulnerable to negative actors and actions (Chart 6). The intermingling of hardware and software, the information infrastructure used both by individuals and states, by the private sector and by government, makes separating doctrine and practice for cyberwar from legitimate use very difficult. Since non-cyber military capabilities, both conventional, and nuclear, rely upon the use of commercial information technology infrastructure, the use of offensive cyber is subject to the problem of blowback. As the NotPetya incident of 2018 indicated, damage from malware installed on one computer can rapidly spread across networks, industries, and international boundaries. The code for StuxNet and the code released by the more recent hack of CIA cyber tools have been noted in other cases of cyber attacks. Chart 6Rapid Growth Of Internet Raises Vulnerability To Harmful Actions

Russia And Cyber Security After COVID-19

Russia And Cyber Security After COVID-19

The view of the international cyber environment by Russia is very similar to views in the US and the West. The Russian national security doctrine of 2015 notes “... An entire spectrum of political, financial-economic, and informational instruments have been set in motion in the struggle for influence in the international arena. Increasingly active use is being made of special services' potential … The intensifying confrontation in the global information arena caused by some countries' aspiration to utilize informational and communication technologies to achieve their geopolitical objectives, including by manipulating public awareness and falsifying history, is exerting an increasing influence on the nature of the international situation.” Although much of the Russian information security doctrine of 2016 is concerned with noting threats to Russia’s information space, what might be called counterintelligence in other documents, there are key comments that note the suitability of using attacks in the information space as an effective means of projecting Russian power, such as “… improving information support activities to implement the State policy of the Russian Federation …” As per usual Soviet and Russian state doctrinal documents, the 2016 doctrine notes all the negative activity of other actors in this field. This practice is consistent with historical Soviet and Russian open press documents which ascribe to other states the activities in which Russia engages or plans to engage. Cyber-crime is rising despite deterrence. Unlike other forms of national security alliances, such as for intelligence, there is little public literature on cyber alliances, especially for offensive action. For example, the US and Israel have never publicly acknowledged a government alliance to emplace the StuxNet virus into the Iranian nuclear development program. Should there be offensive cyber alliances in the West, it is likely they fall along traditional intelligence and defense lines. There is no public reporting on any sort of offensive cyber alliances that involve Russia. There are public efforts at common standards for information technology security, but these efforts are foundering on citizen and government concerns over privacy, as well as commercial proprietary advantage. It is an open question as to whether cyber alliances among friendly nations would deter would-be cyber attackers or hackers. Certainly the growth of complaints to the FBI’s Internet Crime Complaint Center would indicate that statements of deterrence and even prosecutions are failing to reduce cyber attacks (Chart 7). Chart 7Cyber Attacks Are On The Rise

Russia And Cyber Security After COVID-19

Russia And Cyber Security After COVID-19

Both the US national intelligence community and private sector cybersecurity companies agree Russia has a sophisticated state sponsored effort to acquire intelligence via hacking and insert favorable themes into cyberspace via the use of social media. There is also agreement that Russia state elements have a close relationship with criminal elements which can provide a plausibly deniable means of engaging in cyber warfare activities favorable to Russia, as well as engaging in activities for illegal economic advantage. For example, see this quote from the CYBEREASON Intel team: “The crossing of official state sponsored hacking with cybercriminal outfits has created a specter of Russian state hacking that is far larger than their actual program. This hybridization of tools, actors, and missions has created one of the most potent and ill-defined advanced threats that the cybersecurity community faces. It has also created the most technically advanced and bold cybercriminal community in the world. When, as a criminal, your patronage is the internal security service that is charged with tracking and arresting cybercrime, your only concern becomes staying within their defined bounds of acceptable risk and not what global norms, laws, or even domestic Russian law states.” The US Department of Justice in June 2020 noted a Russian national was sentenced to prison for malicious cyber activities. Key points of his illegal activity were the operation of websites open only to Russian speakers, and the vetting or recommendation of other criminals before allowing entry to the websites. One analysis of this situation notes the ties to Russian state security organs and personnel which likely held up the Russian national’s extradition for trial in the US. Government leaders in the US have noted the potential for major cyber attacks in the US affecting physical infrastructure and causing significant economic and social damage, including further attacks on the political election process. However, they have been reticent to state any explicit sort of retaliation. The US Cyber Command notes it is actively combatting hostile cyber actors. Therefore, the question remains open as to what level of cyber attacks would be considered serious enough to be treated as an act of war by the US. There has been public speculation of both Russian and Chinese implants of malware into the US information technology infrastructure that might be activated in the case of open hostilities. US efforts to conduct military operations against Russia or China would likely be countered by Russian or Chinese cyber operations before any physical military operations could be initiated, especially since US based forces would have to transit oceans, taking many days, when cyber operations could happen in seconds. Russian “gray zone” tactics, that is, actions short of large scale conventional war, many of which involve cyber attacks, active measures, and maskirovka, are the subject of much Department of Defense planning and action. To combat such gray zone activity analysis from the RAND Corporation notes the need for a spectrum of diplomatic, informational, military, and economic actions, which would involve commercial partners and allied nations. The difficulty of coordinating such counter action is one reason the Russians continue their gray zone efforts. Russia’s unique characteristics, some of which are weaknesses compared to the US and the West, are indicative of why Russia engages in state sponsored as well as criminal cyber activities (Chart 8). Russian scientific history, the intertwining of state and criminal elements, and continent-spanning location are factors which promote the use of cyber. Russia’s economic position vis-à-vis the US, Russia’s relative lack of military power projection capability beyond the states on its borders (the Near Abroad), except for its nuclear forces, and Russia’s declining demographic situation are negative factors which push Russia to use cyber as a cost effective means of advancing national security and economic policy (Chart 9). Despite US and Western imposed sanctions on Russia for past misdeeds, none of the factors noted above will be changed in the near future. Therefore, those factors, and published Russian doctrine should indicate to Western governments and businesses that Russia will continue to use cyber as a means to advance Russian national security objectives, as well as a means to siphoning off wealth from the West via criminal activities. Chart 8Russia's Relative Weakness Drives Engagement In Cyber Activities

Russia's Relative Weakness Drives Engagement In Cyber Activities

Russia's Relative Weakness Drives Engagement In Cyber Activities

Chart 9Deteriorating Demographics Also Drive Russia’s Cyber Activities

Russia And Cyber Security After COVID-19

Russia And Cyber Security After COVID-19

US preparedness for Russian cyber activity in the upcoming months should be greater given several factors. First, there is clearly awareness of a Russian cyber threat to US interests across government and in the private sector. Second, the US has established new organizations, shifted resources of money and people, and had practice defending against cyber attacks since the 2016 US election cycle. However, the US information technology infrastructure is vast and porous, making it hard to protect against every threat. Russian cyber actors, both state sponsored and criminal, are smart and persistent. Investment Takeaways Cyber security companies offer a way for investors to capitalize on major themes arising from the COVID-19 crisis and its aftermath. These themes include not only changes in worker behavior, e-commerce, corporate culture, and network security, but also our major geopolitical themes like nationalism and the retreat from globalization. Reports as we go to press that Russian hackers have targeted vaccine developers in the US, UK, and Canada underscore the point. The trend is not limited to Russia or COVID-19 vaccines. It is all too apparent from the actions of Russia and China – as well as the increasing efforts by the US and its allies to patrol their own cyber realms, IT systems, and ideological discourse – that governments view the Internet as a frontier to be conquered and fortified rather than as a free space of human exchange in which globalization can operate unfettered (Map 1). Map 1Governments View The Internet As A Frontier To Be Conquered

Russia And Cyber Security After COVID-19

Russia And Cyber Security After COVID-19

Formal measures of country risk are inadequate but provide some perspective as to which countries and companies are least prepared. The International Telecommunication Union (ITU) is the United Nations body charged with monitoring information technology and communications. It ranks countries according to their commitment to cyber security and their exposure to cyber security risks (Chart 10). Chart 10Countries Have An Imperative To Strengthen Cyber Security

Russia And Cyber Security After COVID-19

Russia And Cyber Security After COVID-19

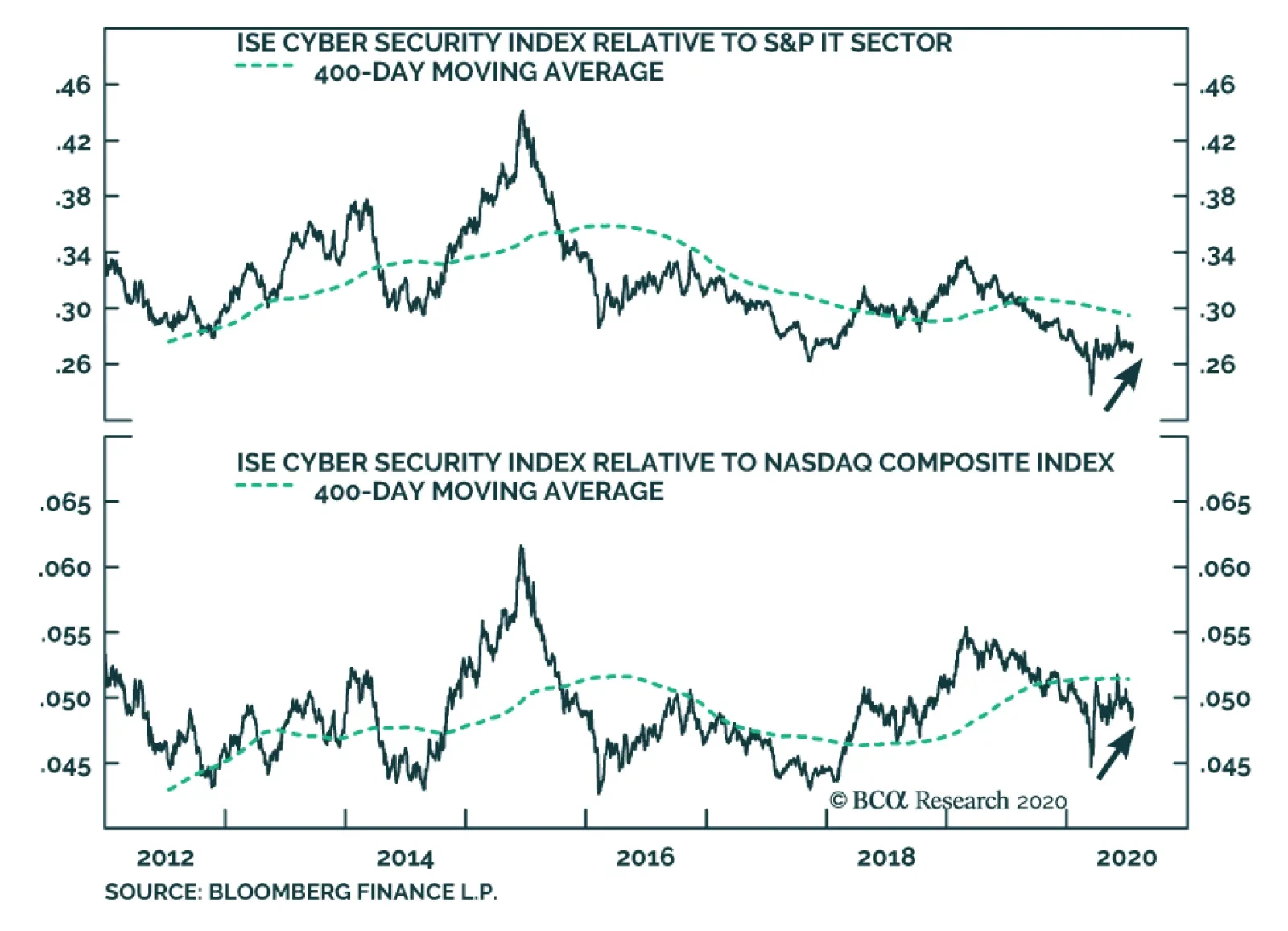

We take these rankings with a grain of salt knowing that advanced countries like the US and UK rank near the top of the list, and yet are the prime targets of hackers and thus face enormous cyber security risks. What is clear is that no country is safe and every country has an economic and national security imperative to strengthen its cyber security. These indexes also suggest that several European countries are less well prepared than one would think and that emerging markets are grossly underprepared. China, Russia and Iran should not be thought of only as aggressors – they will increasingly become targets as the West seeks to counteract them. As Russia expands operations it becomes a target of cyber counter-strikes as well as economic sanctions. And as China accelerates its drive to become a high tech giant, it encourages economic decoupling from the West and retaliation for its use of cyber-theft and state-based hacking. China, Russia, and Iran will also increasingly become victims of cyber attacks. There are two main cyber security equity indexes – the NASDAQ CTA Cybersecurity Index (NQCYBR) and NASDAQ ISE Cyber Security Index (HXR). These indexes trade in line with each other and have rallied extensively since the COVID-19 crisis (Chart 11). Investors are aware that the surge in working from home and companies conducting operations off-site, as well as geopolitical great power struggle, have created extensive new vulnerabilities and capex requirements. Chart 11Cyber Security Stocks Have Benefited From COVID-19 ...

Cyber Security Stocks Have Benefited From COVID-19 ...

Cyber Security Stocks Have Benefited From COVID-19 ...

On April 24, we recommended that investors go long the ISE index relative to the S&P 500 information technology sector. We are also going long the ISE index relative to the NASDAQ on a strategic horizon. Chart 12... But Not So Much Relative To Broad Tech Sector

... But Not So Much Relative To Broad Tech Sector

... But Not So Much Relative To Broad Tech Sector

Tech has been the prime beneficiary of the COVID-19 crisis while the necessary corollary of the tech companies’ continued success is the need for security of their information, property, and customers (Chart 12). We also favor the ISE index because it has a slightly heavier cyclical component due to the fact that 13% of its companies are in the industrial sector, compared to 10% for the CTA index. The industrial side should benefit more as economies reopen and recover. These indexes are tracked by two ETFs. The First Trust NASDAQ Cybersecurity ETF (CIBR) tracks the NASDAQ CTA index with an emphasis on larger companies, while the ETFMG Prime Cyber Security ETF (HACK) tracks the ISE index, companies with market capitalization lower than $250 million, and a slightly lower exposure to the communications sector as opposed to IT and software. The HACK ETF has lagged the CIBR this year so far and offers an opportunity for investors to invest in data protection and up-and-coming firms. Over the past ten years cyber security has proven to be a volatile investment space with rapidly increasing competition for market share. But the secular tailwinds are powerful and a diversified exposure to the sector will be rewarding for investors positioning for the post-COVID-19 world. Elmo Wright Consulting Editor Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Appendix Appendix TableMajor Cyber-Attacks Over The Past Decade

Russia And Cyber Security After COVID-19

Russia And Cyber Security After COVID-19

Footnotes Coats, Dan. “Statement For The Record Worldwide Threat Assessment Of The Us Intelligence Community,” May 23, 2017. Coats, Dan. “Statement For The Record Worldwide Threat Assessment Of The Us Intelligence Community,” March 6, 2018. Coats, Dan. “Annual Threat Assessment Opening Statement,” January 29, 2019. CyberReason Intel Team, “Russia And Nation-State Hacking Tactics: A Report From Cybereason Intelligence Group,” cybereason.com, June 5, 2017. Department of Justice, “Russian National Sentenced To Prison For Operating Websites Devoted To Fraud And Malicious Cyber Activities”, June 26, 2020. Department of Justice, “U.S. Charges Russian FSB Officers And Their Criminal Conspirators For Hacking Yahoo And Millions Of Email Accounts, Fsb Officers Protected, Directed, Facilitated And Paid Criminal Hackers”, March 15, 2017. Gerasimov, Vasily. “The Value Of Science In Prediction,” Military Industrial Courier, Feb 27, 2013. Federal Bureau of Investigation, “Internet Crime Complaint Center Marks 20 Years From Early Frauds to Sophisticated Schemes, IC3 Has Tracked the Evolution of Online Crime,” May 8, 2020. Fedorov, Yuriy Ye. “Arms Control In The Information Age” Symposium “Emerging Challenges In The Information Age,” 23 January 2002, Arlington, Virginia. Galeotti, Mark. “The ‘Gerasimov Doctrine’ And Russian Non-Linear War,” In Moscow’s Shadows, July 6, 2014. Greenberg, Andy. “The Untold Story Of Notpetya, The Most Devastating Cyberattack In History,” Wired Magazine, August 22, 2018. Krebs, Brian. “Why Were the Russians So Set Against This Hacker Being Extradited?,” Krebs on Security, Nov 18, 2019. Lusthaus, Jonathan. “Cybercrime in Southeast Asia Combating a global threat locally,” May 20, 2020. Mattis, James. Department of Defense, “Summary Of The 2018 National Defense Strategy Of The United States Of America”. Meakins, Joss. “Living in (Digital) Denial: Russia’s Approach To Cyber Deterrence,” Russia Matters, July 2018. Ministry of Foreign Affairs of the Russian Federation. “Doctrine Of Information Security Of The Russian Federation,” Dec 5, 2016. Nakasone, Paul. “Cybercom Commander Briefs Reporters At White House,” Department of Defense video briefing, Aug 2, 2018. National Security Agency, “NSA/CSS Technical Cyber Threat Framework V2”, a report from: Cybersecurity Operations The Cybersecurity Products And Sharing Division, 29 November 2018. Pettijohn and Wasser. “Competing In The Gray Zone,” RAND Corporation, 2019. Putin, Vladimir. “Strategy of National Security of the Russian Federation,” Office of the President of the Russian Federation, Dec 31, 2015. Russian National Security Strategy 31 Dec 2015, Russia Matters. Snegovaya, Maria. “Putin’s Information Warfare In Ukraine: Soviet Origins Of Russia's Hybrid Warfare,” Institute for the Study of War, Sep 22, 2015. Tsygichko, V. N. “About Categories of “Correlation Of Forces” for Potential Military Conflicts in the New Era,” Symposium “Emerging Challenges In The Information Age,” 23 January 2002, Arlington, Virginia. Wiener, Norbert, Cybernetics: Or Control and Communication in the Animal and the Machine. Cambridge, Massachusetts: MIT Press, (1948).

Dear Client, Next Monday, July 20, we will be hosting our quarterly webcast, one at 10am EST for our US and EMEA clients and one at 9pm for our Asia Pacific, Australia and New Zealand clients; our regular weekly publication will resume on Monday July 27, 2020. Kind Regards, Anastasios Highlights A Democratic sweep would not prevent the stock market from grinding higher over the 12 months after the election. With this year’s massive stimulus, this cyclical view is reinforced. Whether Biden governs as a centrist or a left-winger will depend not on Biden’s preferences but on whether Republicans have a majority in the Senate to constrain the Democratic Party. But the party that wins the White House is highly likely to win the Senate in this cycle. Investors should expect Biden to govern from the left. A Biden presidency would lead to negative surprises on regulation, taxes, health care, trade, energy, and tech. Democrats would remove the Senate filibuster. Yet the macro agenda is reflationary. A blue trifecta would dent S&P 500 profit margins and take a bite out of EPS in 2022. Small caps will also likely suffer at the margin versus mega caps. While select Tech Titans are exposed to a blue sweep regulatory shock, the broad technology sector will prove to be more resilient especially compared with banks and health care equities. Feature Online political betting markets are still not fully pricing our “Blue Wave” scenario for the US election this year. The odds are closer to 50%-55% than 35%. Hence the equity market, especially the NASDAQ, is complacent about rising political risks to US equity sectors (Chart 1). The immediate risk to the rally is not politics but the pandemic, namely the COVID-19 resurgence in the United States, which is causing governors of major states like Texas, California, and Florida to slow down the economic reopening. The US’s failure to limit the spread of the virus has not yet led to a spike in deaths in aggregate, but it is leading to a spike in major states like Texas and Florida (Chart 2). Deaths are ultimately what matter to politicians and financial markets, since governments will not shut down all of society for less-than-lethal ailments. Fear will weigh on consumer and business confidence, including fear of a deadly second wave this winter. Near-term risks to the equity rally are elevated. Chart 1Blue Wave Expected, Equities Unconcerned

Blue Wave Odds Rising, Equities Hesitate

Blue Wave Odds Rising, Equities Hesitate

Chart 2COVID-19 Outbreak Still A Risk

Blue Trifecta: Broad Equity Market And Sector Specific Implications

Blue Trifecta: Broad Equity Market And Sector Specific Implications