Geopolitics

President Trump’s inaugural speech outlined his second term agenda. The theme was that the US will become “far more exceptional” than it already is. Trump pledged to reverse America’s decline, rebalance the justice system, streamline government, protect…

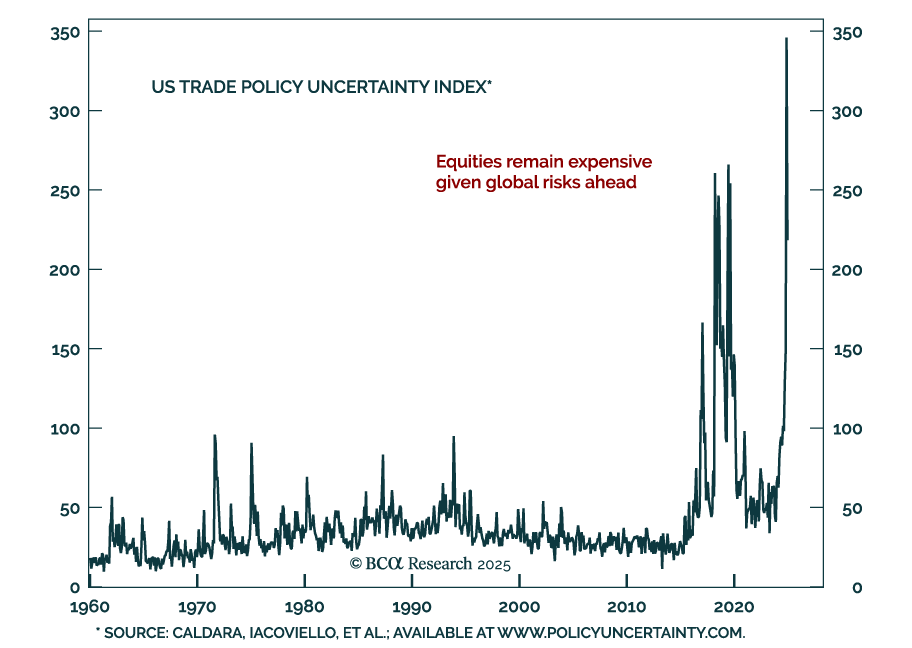

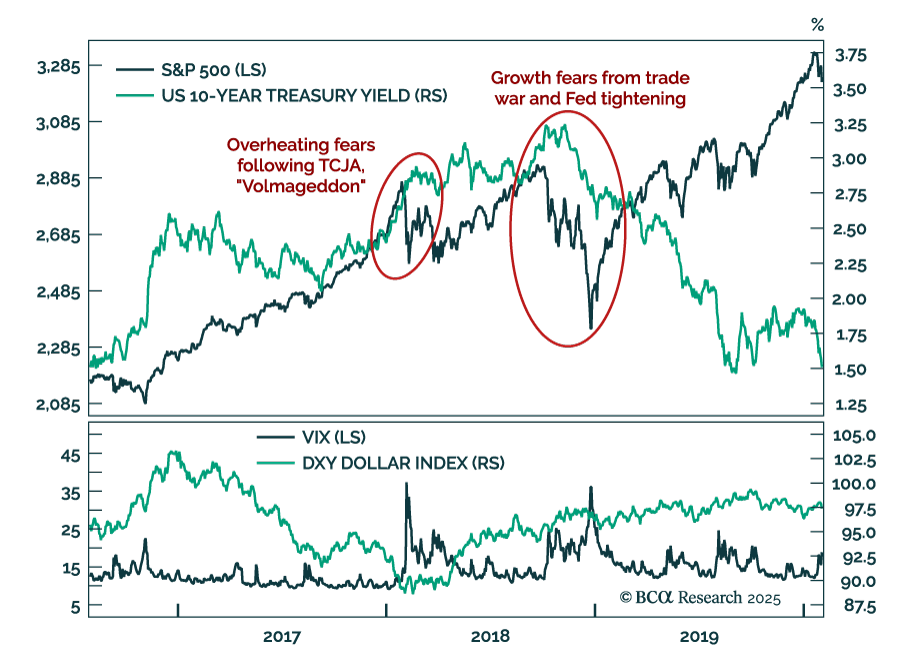

We look at President Trump’s first mandate for lessons on how markets would likely react to different policies. On the fiscal front, the 2017 Tax Cuts and Jobs Act (TCJA) was the first pro-cyclical stimulus in decades. Markets pushed back, as the early 2018…

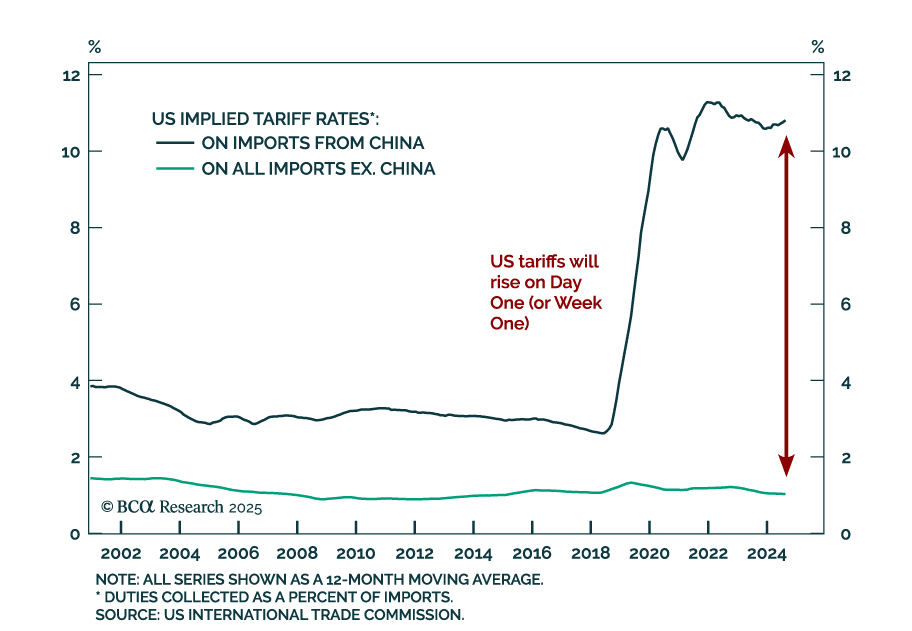

Our US Political strategists published a Special Report on the trade and fiscal policies likely to be implemented on Day One as the Trump administration takes over Washington. Trump is likely to implement significant tariffs early in his term,…

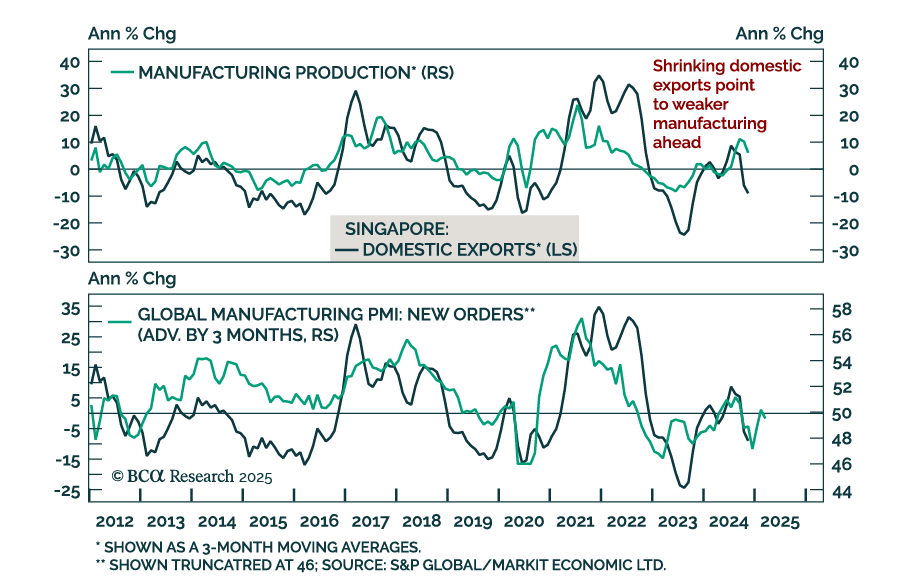

Our Emerging Markets strategists just published a report on Singapore stocks after a significant rally over the past year. Singapore’s manufacturing sector faces headwinds from contracting global new orders, which signals that a recovery in exports is…

Please join us for a BCA Expert Webcast, Thursday, January 16 at 10:00 AM EDT, with Brendan Kelly, former Director for China Economics on the US National Security Council, veteran of the New York Federal Reserve, Treasury Department, Defense Department, and life member of the Council on Foreign Relations.

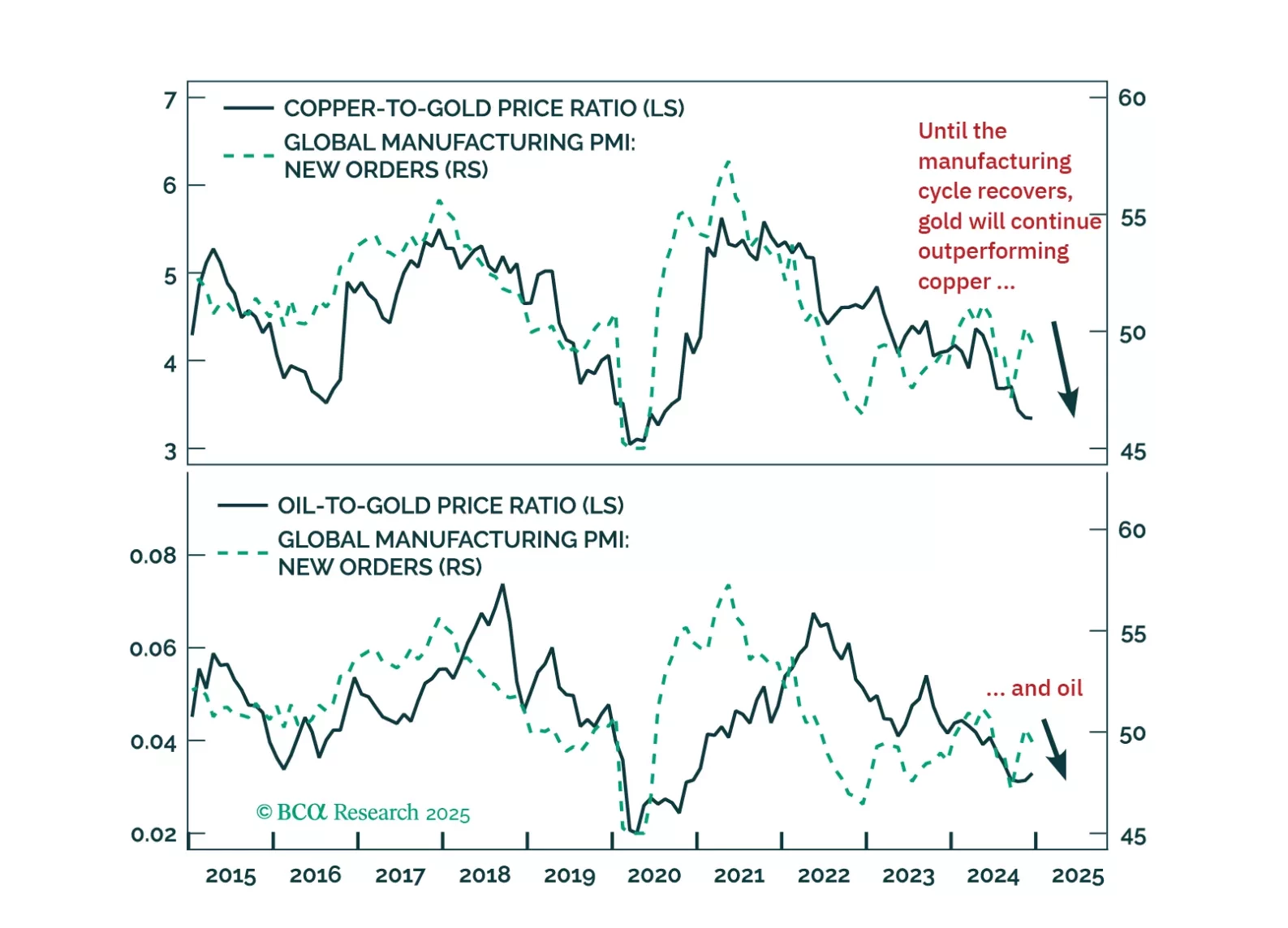

In this Special Report, we outline the three themes that we believe will drive commodity markets this year: (1) demand growth will remain sluggish across cyclical commodities (2) supply-side developments will ultimately be bearish for oil prices, and (3) traditional relationships between commodity prices and financial variables may not hold.

The outgoing Biden administration has launched a slew of macro-relevant executive orders and regulatory actions. The one with immediate macro implications are the sanctions against Russian oil traders and its “dark fleet” of oil tankers.

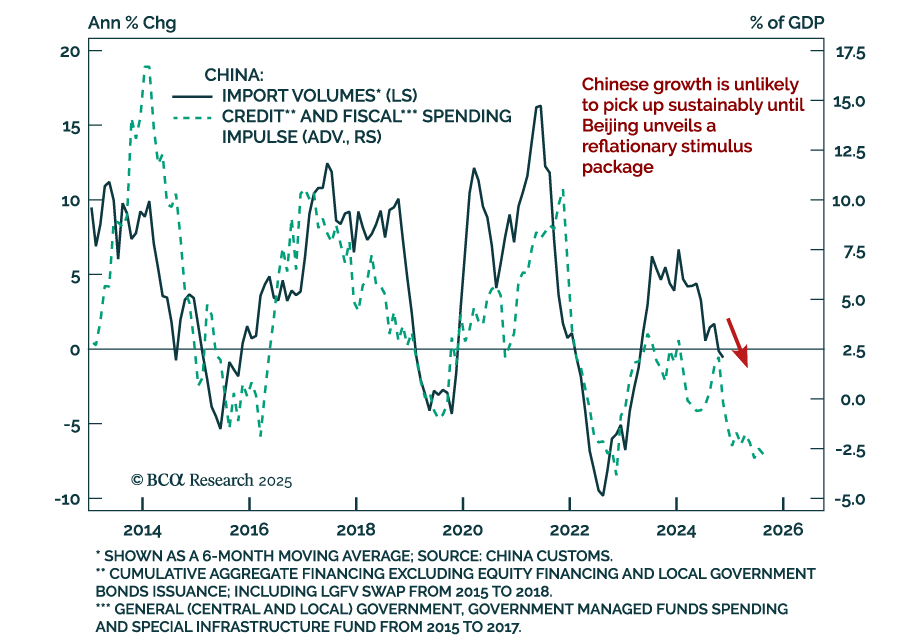

China’s December trade data was positive, with exports in USD terms rebounding to 10.7% y/y from 6.7% in November, and imports rebounding to 1.0% from -3.9%. Taken at face value, the numbers are positive for both the Chinese and global economies. However, our…

The global economy is subject to numerous cycles displaying reflexivity and feedback loops. One of these is the relationship between financial conditions and growth. Given this relationship, economic strength can plant the seeds of its own demise.Markets are…

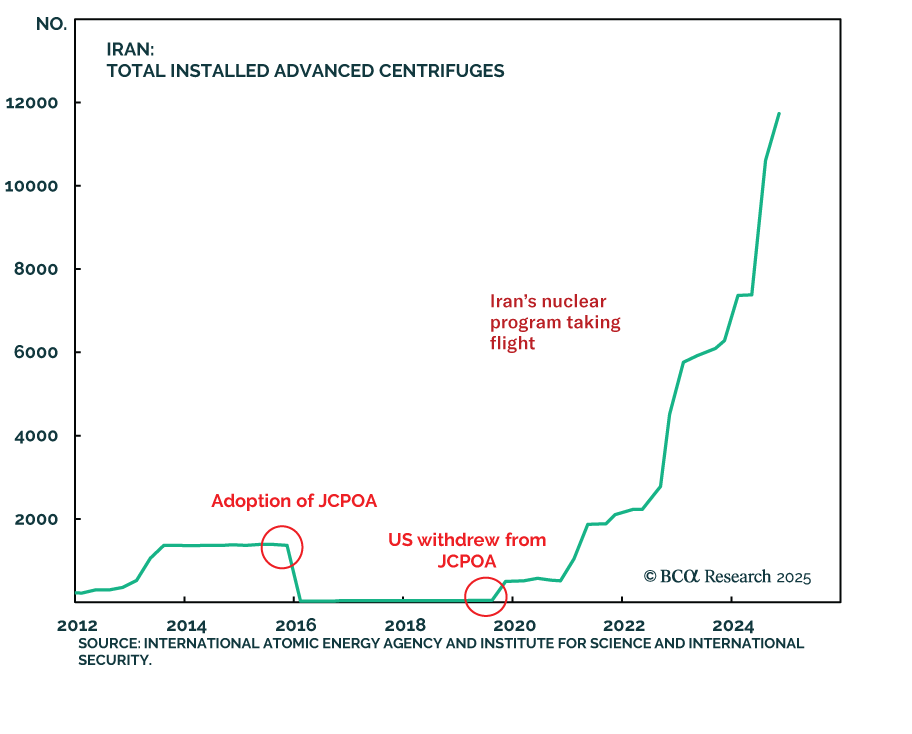

Our Geopolitical Strategy colleagues published their annual “Black Swan” report, where they outline low-odds scenarios that could have a major impact on financial markets. Here is the 2025 edition: China’s Policy Reversal: A complete policy shift by…