Geopolitics

The macro backdrop is hardly encouraging: global export volumes are contracting and a huge spike in global policy uncertainty is providing additional support to the dollar. Any further rebound in the greenback will pile additional pressure onto trade flows,…

Highlights Currency markets continue to fight a tug of war between weak incoming data but easier financial conditions. Our thesis remains that the path of least resistance for the dollar is down, but the rising specter of global market volatility suggests it could catapult to new highs before ultimately reversing. Most of our pro-cyclical trades have been put offside in this environment of rising volatility. Maintain tight stops until more evidence emerges that global growth has bottomed. Large net short positioning in the Swiss franc and yen, together with cheap valuations, make them attractive from a contrarian standpoint. Hold on to CHF/NZD positions recommended on April 26. Feature Our thesis remains that global growth is in a volatile bottoming process. However, incoming data pretty much across the globe has been very weak, with the latest specter of a global trade war suggesting that economic softness could linger for longer than we originally anticipated. Given the shifting market dynamics, it is important to revisit our thesis on how to be positioned in currency markets. We do so this week via the lens of the Australian dollar, one of the market’s favorite short positions. Future reports will focus on additional global growth barometers, and when to time the shift towards a more pro-cyclical stance. Positive Divergences Chart I-1Global Growth Barometers Flashing Amber

Global Growth Barometers Flashing Amber

Global Growth Barometers Flashing Amber

On the surface, most data points appear negative for the Aussie dollar. Typical reflation indicators such as commodity prices, emerging market currencies, and industrial share prices are breaking down after a nascent upturn earlier this year. One of our favorite indicators on whether or not easing liquidity conditions will lead to higher growth are the CRB Raw Industrials index-to-gold, copper-to-gold, and oil-to-gold ratios. It is disconcerting that these indicators have moved decidedly lower together with U.S. bond yields, another global growth barometer (Chart I-1). On a similar note, currencies in emerging Asia that sit closer to the epicenter of Chinese stimulus are breaking down. This suggests that so far, policy stimulus in China has not been sufficient to lift global growth, and/or the transmission mechanism towards higher growth is not working. Not surprisingly, the Australian dollar has been breaking down at a rapid pace, putting our long AUD/USD position offside. We will respect our stop-loss at 0.68 if breached, but a few indicators suggest the bearish view on the Australian dollar is very late: Chart I-2Australian Stocks Hitting New Highs

Australian Stocks Hitting New Highs

Australian Stocks Hitting New Highs

Election Results: The recent general election outcome was a big surprise to the market, and has eased risks to both the country’s banks and housing market. The center-left Labour party, which moved further to the left in this electoral cycle, was defeated by a substantial margin. This has a few important implications. First, “negative gearing” – the practice of using investment properties that are generating losses to offset one’s income tax bill – will remain in place. This was a big overhang on the housing market, which likely exacerbated the downturn in Aussie house prices. Second, the capital gains tax exemption from selling properties will probably not be reduced from 50% to 25%, as previously pledged. Finally, the Liberal-National coalition government will maintain the policy of reimbursing investors for corporate taxes paid by the underlying company. This keeps the incentive for retirees to own high dividend-yielding equities such as those of Australian banks. Australian equities hit a new cyclical high following the election results. This suggests the return on capital for Aussie companies may have inched higher following the more pro-market leadership shift (Chart I-2). At low levels of interest rates, fiscal policy is much more potent than monetary policy. Interest Rates: The latest Reserve Bank Of Australia (RBA) minutes suggest that rate cuts are back on the agenda. But the question is, with the markets pricing in two rate cuts by the end of this year, does it still pay to be short the Aussie dollar on widening interest rate differentials? More importantly, fiscal policy is set to become decisively loose this year. The new government is slated to introduce income tax cuts as early as July. This is skewed towards lower-income households, meaning the fiscal multiplier may be larger than what the Australian economy is normally accustomed to. Meanwhile, infrastructure spending will remain high, which will be very stimulative for growth in the short term. At low levels of interest rates, fiscal policy is much more potent than monetary policy, and the RBA will be loath to cut rates more than is currently expected by the market, at a time when consumer indebtedness remains quite high, and policy rates are already close to rock-bottom levels. The key for the RBA will be the job market, which at the moment remains a pillar of support for the Aussie economy. Job growth is accelerating, and labor force participation is hitting fresh highs (Chart I-3). So long as these trends continue, the RBA can afford to remain on the sidelines for a while longer. Meanwhile, while Aussie rates continue to drift downward, it has not been particularly profitable to buy U.S. Treasurys on a hedged basis (Chart I-4). Chart I-3Australia Employment Remains Robust

Australia Employment Remains Robust

Australia Employment Remains Robust

Chart I-4It is Expensive To Short The Aussie

It is Expensive To Short The Aussie

It is Expensive To Short The Aussie

Housing Market: For more than two decades, the Australian dollar has tended to be mostly driven by external conditions, especially the commodity cycle. But for the first time in several years, domestic factors have joined in to exert powerful downward pressure on the currency. The Australian Prudential Regulation Authority (APRA) has been on a mission to surgically deflate the overvalued housing market, while engineering a soft landing in the economy. Initially, their macro-prudential measures worked like a charm, as owner-occupied housing activity remained resilient relative to “investment-style” housing. What has become apparent now is that the soft landing intended by the authorities has rapidly morphed into a housing crash (Chart I-5). This is negative for consumption, both via the wealth effect and as well as for the outlook for residential construction activity. Chart I-5Could Australian Housing Bottom Soon?

Could Australian Housing Bottom Soon?

Could Australian Housing Bottom Soon?

The good news is that policy is supposed to become supportive for Aussie homebuyers at the margin, with the government slated to introduce new initiatives to help first-time homebuyers. Should labor market improvements continue, it will also help household income levels. Over the past few decades, house prices in Australia have generally staged V-shaped recoveries when at this level of contraction. Betting on at least some stabilization going forward seems reasonable. Commodity Prices: One bright spot for the Aussie dollar has been rising terms of trade. Admittedly, most measures of Chinese (and global) growth remain weak. However, there have been notable improvements in recent months that suggest economic velocity may be picking up: Production of electricity and steel, all inputs into the overall manufacturing value chain, are inflecting higher. Intuitively, these tend to lead overall industrial production. If these advance any further, they will begin to exceed GDP growth, indicating a renewed mini-cycle (Chart I-6). Production of electricity and steel, all inputs into the overall manufacturing value chain, are inflecting higher. In recent months, both steel and iron ore prices have been soaring. Many commentators have attributed these increases to supply bottlenecks and/or seasonal demand. However, it is evident from both the manufacturing data and the trend in prices that demand is also playing a role. Meanwhile, Beijing’s clear environmental push has lifted the share of liquefied natural gas in Australia’s export mix (Chart I-7). Given that the reduction – if not the outright elimination – of pollution is a long-term strategic goal in China, this will be a multi-year tailwind. As the market becomes more liberalized and long-term contracts are revised to reflect higher spot prices, the Aussie dollar will get a boost. Chart I-6Some Green Shoots From China

Some Green Shoots From China

Some Green Shoots From China

Chart I-7Australian LNG Will Buffet Terms Of Trade

Australian LNG Will Buffet Terms Of Trade

Australian LNG Will Buffet Terms Of Trade

Valuation: In terms of currency performance, a lot of the bad news already appears priced in to the Australian dollar, which is down 15% from its 2018 peak, and 38% from its 2011 peak. Meanwhile, Australian dollar short positions appeared to have already hit a nadir. This suggests outright short AUD bets are at risk from either upside surprises in global growth or simply the forces of mean reversion (Chart I-8). One of our favorite metrics for the Australian dollar’s fair value is its real effective exchange rate relative to its terms of trade. On this basis, the Aussie dollar is cheap by about 10% (Chart I-9). Chart I-8Short AUD: ##br##A Consensus Trade

Short AUD: A Consensus Trade

Short AUD: A Consensus Trade

Chart I-9AUD Is Attractive From A Terms Of Trade Perspective

AUD Is Attractive From A Terms Of Trade Perspective

AUD Is Attractive From A Terms Of Trade Perspective

China Credit Cycle: We have discussed at length how a revival in the Chinese credit cycle will help global and Australian growth. On the real estate front, residential property sales remain soft, but evidence from tier-1 and even tier-2 cities is signaling that this may be behind us, given robust sales. Over the longer term, the ebb and flow of property sales have usually been in sync across city tiers. A revival in the property market will support construction activity and investment. Chart I-10How Long Will The Weakness In China Last?

How Long Will The Weakness In China Last?

How Long Will The Weakness In China Last?

House prices have been rising to the tune of 10%-15% year-on-year, and may be sniffing an eventual pick-up in property volumes. Finally, Chinese retail sales including those of durable goods remain very weak. Car sales are deflating at the fastest pace in over two decades. But the latest VAT cut by the government is being passed through to consumers, with an increasing number of car manufacturers cutting retail prices. This should help retail sales (Chart I-10). Other Global Growth Barometers Investors looking for more clarity on the global growth picture from the April and May data prints remain in a quandary. And the preliminary European PMI numbers this morning offered no glimmers of hope. That said, the most volatile components of euro area growth tend to be investment and net exports. Should they both pick up on the back of stronger external demand, GDP could easily gravitate towards 1.5%-2%, pinning it well above potential. The German PMI is currently among the weakest in the euro zone. But forward-looking indicators suggest we may be on the cusp of a V-shaped bottom over the next month or so (Chart I-11). Chart I-11German Manufacturing Might Be At The Cusp Of A V-Shaped Recovery

German Manufacturing Might Be At The Cusp Of A V-Shaped Recovery

German Manufacturing Might Be At The Cusp Of A V-Shaped Recovery

The broad message is that global growth is in the midst of volatile bottoming process. However, before evidence of this fully unfolds, markets are likely to be swayed by the ebbs and flows of higher-frequency data. We recommend maintaining a pro-cyclical bias at the margin, but having tight stop losses as well as positions in both the Swiss franc and yen as insurance. Housekeeping Our buy-limit order on the British pound was triggered at 1.30 on March 29th. As we argued at the time, the pound was sitting exactly where it was after the 2016 referendum results, but the odds of a hard Brexit had significantly fallen. Since then, policy-induced volatility has led to a significant depreciation in the pound, with our position at risk of being stopped out at our 1.25 stop-loss this week. Given the rising specter of political volatility, we will respect our stop-loss if breached at 1.25. On the domestic front, economic surprises in the U.K. relative to both the U.S. and euro area continue to soar. The reality is that the pound and U.K. gilt yields should be much higher – solely on the basis of hard incoming data. Employment growth has been holding up very well, wages are inflecting higher, and the average U.K. consumer appears in decent shape (Chart I-12). The CPI data this week confirm that the domestic environment is hardly deflationary. That said, given the rising specter of political volatility, we will respect our stop-loss if breached at 1.25. Chart I-12Hold GBP/USD, But Stand Aside At 1.25

Hold GBP/USD, But Stand Aside At 1.25

Hold GBP/USD, But Stand Aside At 1.25

Chester Ntonifor, Foreign Exchange Strategist chestern@bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the U.S. have been soft: The Michigan consumer sentiment index jumped to 102.4 in May. However, the Chicago Fed national activity index fell to -0.45 in April. The Redbook index increased by 5.4% year-on-year in May. Existing home sales contracted by 0.4% month-on-month to 5.2 million in April. Moreover, new home sales fell by 6.9% month-on-month in April. The Markit composite index fell to 50.9 in April. The manufacturing and services PMI fell to 50.6 and 50.9 respectively. Importantly, this a just a nudge above the 50 boom/bust level. DXY index initially increased by 0.3%, then plunged on the weak PMI data, returning flat this week. The FOMC minutes released on Wednesday reiterated that the recent drop in core inflation is mostly transitory, and that no strong evidence exists for a rate change in either direction. With the forward market already pricing an 82% probability of a rate cut this year, any hawkish shift by the Fed will be a surprise. However, this will not necessarily be bullish for the dollar, if accompanied by a global growth bottom. We remain of the view that the path of least resistance for the dollar is down. Report Links: President Trump And The Dollar - May 9, 2019 Take Out Some Insurance - May 3, 2019 Currency Complacency Amid A Global Dovish Shift - April 26, 2019 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area have been mixed: Headline consumer price inflation was unchanged at 1.7% year-on-year in April, while core inflation increased to 1.3%. The current account balance narrowed to a surplus of 24.7 billion euros in March. However, this was above expectations. German GDP was unchanged at 0.6% year-on-year in Q1. The euro area Markit composite PMI was flat at 51.6 compared to the last reading of 51.5. Below the surface, both the manufacturing and services PMIs fell to 47.7 and 52.5, respectively. German composite PMI was held up at 52.4 by the services component that came in at 55. However, the manufacturing component fell to 44.3. German IFO current assessment dropped to 100.6 in May, and the business climate dropped to 97.9. In France, the Markit composite PMI came in at 51.3. The manufacturing and services PMIs both increased, to 50.6 and 51.7 respectively. This was the one bright spot in euro area data. EUR/USD has been flat this week, with recent data being on the softer side. The PMI data remain subdued, in particular. Meanwhile, political uncertainties continue to weigh on investors’ sentiment. Report Links: Take Out Some Insurance - May 3, 2019 Reading The Tea Leaves From China - April 12, 2019 Into A Transition Phase - March 8, 2019 The Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been mixed: Q1 annualized GDP grew by 2.1% quarter-on-quarter, well above estimates. Industrial production fell by 4.3% year-on-year in March, but was higher than the previous reading of -4.6% in February. Capacity utilization fell by 0.4% month-on-month in March. Exports contracted by 2.4% year-on-year in April, while imports increased by 6.4% year-on-year. The total trade balance thus narrowed from ¥528 billion to ¥64 billion. Notably, the exports to China fell by 6.3%, while exports to the U.S. increased by 9.6%. Machinery orders fell by 0.7% year-on-year in March. Nikkei manufacturing PMI fell below 50, coming in at 49.6 in May. USD/JPY fell by 0.5% this week. Yutaka Harada, a dovish member of the BoJ, warned during a news conference that by hiking the consumption tax rate at this critical juncture, Japan could risk sliding into a recession. With core CPI far from its 2% target, more monetary easing is probably exactly what the doctor ordered. Report Links: Beware Of Diminishing Marginal Returns - April 19, 2019 Tug OF War, With Gold As Umpire - March 29, 2019 A Trader’s Guide To The Yen - March 15, 2019 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data in the U.K. have been firm: The Rightmove house price index increased by 0.1% year-on-year in May. The orders component of the CBI industrial trends survey decreased to -10 in May. Retail sales increased by 3% year-on-year in April. Producer prices and input prices increased by 2.1% and 3.8%, year-on-year respectively in April. Headline inflation and core inflation increased by 2.1% and 1.8% year-on-year in April, both below expectations. GBP/USD decreased by 0.6% this week. Teresa May offered MPs a vote on a second referendum on Brexit, which considers a tighter customs union with the EU. The ongoing Brexit chaos has increased volatility in the pound. Report Links: Take Out Some Insurance - May 3, 2019 Not Out Of The Woods Yet - April 5, 2019 A Trader’s Guide To The Yen - March 15, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been mostly negative: ANZ Roy Morgan weekly consumer confidence index increased to 117.2 this week. Westpac leading index fell by 0.1% month-on-month in April. Completed construction work fell by 1.9% in Q1. AUD/USD fell by 0.3% this week. During this week’s federal election, the coalition government led by Prime Minister Scott Morrison won. Besides the political development, the RBA governor Philip Lowe gave a speech on Monday, highlighting external shocks to Australian economy. He also expressed the positive outlook for Australian economy in the second half of 2019 and 2020, supported by the ongoing capex in infrastructure and resources sectors, together with strong population growth. More importantly, he mentioned that the RBA would consider the case for lower interest rates, which is a dovish shift from previous speeches. We are long AUD/USD with a tight stop at 0.68. Report Links: Beware Of Diminishing Marginal Returns - April 19, 2019 Not Out Of The Woods Yet - April 5, 2019 Into A Transition Phase - March 8, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand have been mixed: Credit card spending growth missed expectations, coming in at 4.5% year-on-year in April. Retail sales increased by 0.7% quarter-on-quarter in Q1. Retail sales excluding autos increased by 0.7% quarter-on-quarter in Q1. NZD/USD fell by 0.3% this week. NZD/USD is currently trading at a 7-month low around 0.65. A bleak external picture is worrisome for the kiwi. We continue to favor the AUD/NZD cross, from a strategic standpoint. Report Links: Not Out Of The Woods Yet - April 5, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been solid: Retail sales increased by 1.1% month-on-month in March. In particular, retail sales excluding autos increased by 1.7% month-on-month, well above estimates. USD/CAD appreciated by 0.3% this week. The better-than-expected retail sales data in March sparked a small rally in the loonie. However, the rally proved to be short-lived following softer oil prices. Positive data surprises in Canada will have to be sustained for the loonie to find some measure of support. Report Links: Currency Complacency Amid A Global Dovish Shift - April 26, 2019 A Shifting Landscape For Petrocurrencies - March 22, 2019 Into A Transition Phase - March 8, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data in the Switzerland have been positive: Money supply (M3) growth was unchanged at 3.5% year-on-year in April. Industrial production increased by 4.3% year-on-year in Q1, albeit lower than the last reading of 5.1%. USD/CHF fell by 0.8% this week. As we argued in last week’s research note, the increasing global market volatility has reignited interest in the Swiss franc. We continue to recommend the franc as an insurance policy amid rising geopolitical risk. Report Links: What To Do About The Swiss Franc? - May 17, 2019 Beware Of Diminishing Marginal Returns - April 19, 2019 Balance Of Payments Across The G10 - February 15, 2019 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

There was little data out of Norway this week: The unemployment rate came in at 3.5% in March, well below consensus of 3.7% and the previous reading of 3.8%. USD/NOK fell by 0.4% this week. Rising geopolitical risks will be supportive of the oil market and put a floor under the krone. Aside from the U.S.-Iran tensions, the world faces the prospect of the loss of Venezuelan production, and significant outages in Libya, which are all bullish. Meanwhile, Norway remains one of few G10 countries that can hike interest rates in the near term. Report Links: Currency Complacency Amid A Global Dovish Shift - April 26, 2019 A Shifting Landscape For Petrocurrencies - March 22, 2019 Balance Of Payments Across The G10 - February 15, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data in Sweden have been positive: Capacity utilization increased by 0.5% in Q1. Moreover, the unemployment rate fell to 6.2% in April. This was well below expectations of 6.8% and the previous month’s reading of 7.1%. USD/SEK fell by 0.3% this week. While we favor both the NOK and SEK against the U.S. dollar, near-term factors are more bullish for the krone. Our long NOK/SEK position is currently 4.38% in the money. Stick with it. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Global Liquidity Trends Support The Dollar, But... - January 25, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Closed Trades

Highlights So What? Markets remain complacent about U.S.-China trade. Why? The U.S. has escalated the trade war by threatening sanctions on key Chinese tech firms. Chinese President Xi Jinping is preparing his domestic audience for protracted struggle. U.S. domestic politics do not prohibit, and likely encourage, a tough stance on China. Farmers are not a constraint on Trump — economic growth is. Go long spot gold and JPY-USD. Feature Markets remain complacent. Chart 1 suggests that while the combination of unilateral trade tariffs and spiking U.S. 10-year Treasury yields was enough to sink the S&P 500 in 2018, the former alone cannot do so today. Chart 1Tariffs Alone Not Enough To Sink Equities? Wrong.

Tariffs Alone Not Enough To Sink Equities? Wrong.

Tariffs Alone Not Enough To Sink Equities? Wrong.

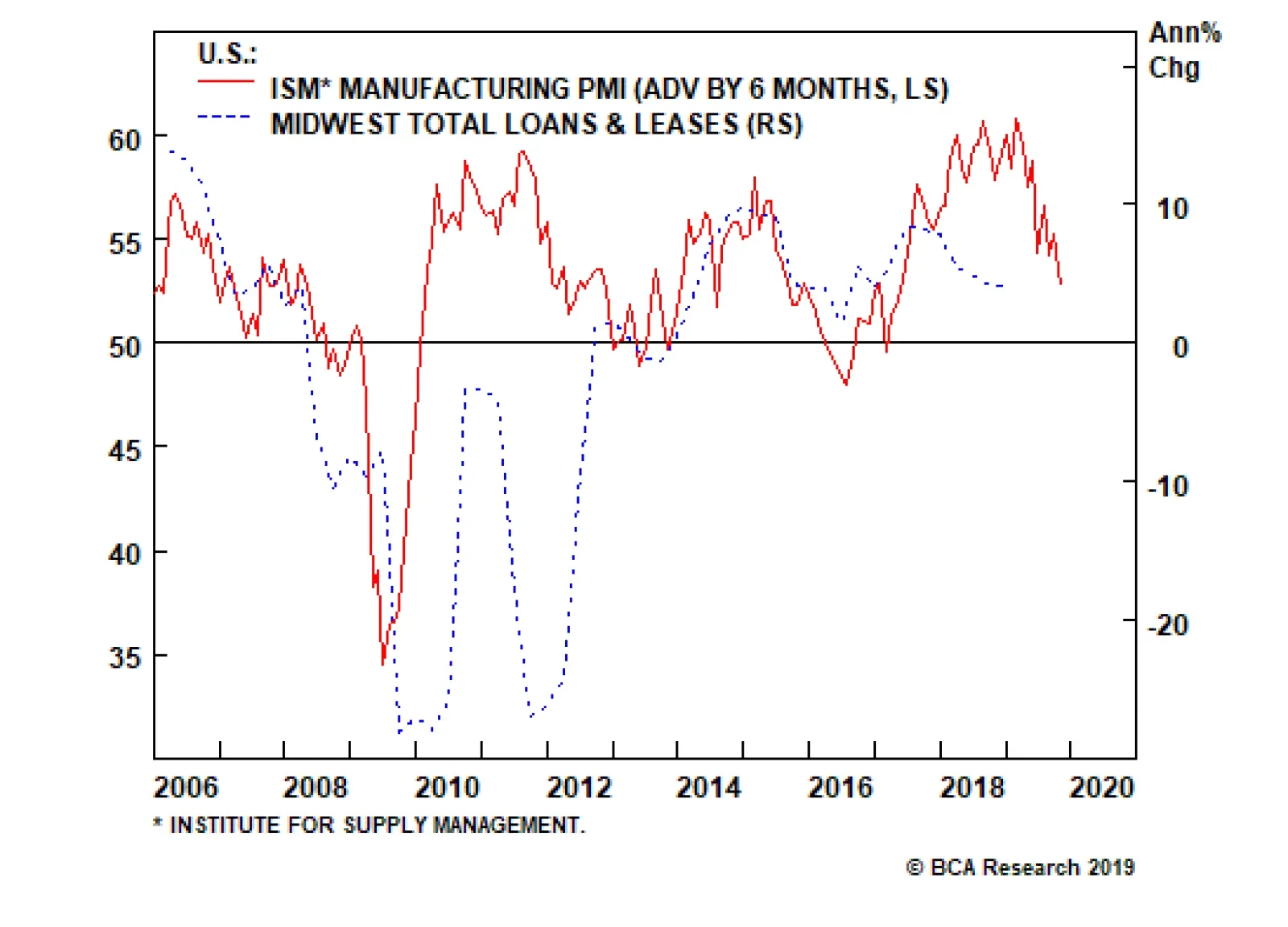

Specifically, the increase in the Section 301 tariff rate from 10% to 25% on $200 billion worth of Chinese imports and the threat of a new 25% tariff on the remaining $300 billion worth of Chinese imports in just a month’s time has only led to a 3% pullback in equities since May 3. That was the last trading day prior to President Donald Trump’s infamous tweet about hiking the tariff. Unlike the trade war escalation in October through November of last year, the Federal Reserve is no longer hiking rates, China’s economic indicators have bottomed, and U.S. equity investors have now fully imbibed the “Art of the Deal.” The consensus holds that the escalation of trade tensions with China is contained within the context of Trump’s well-known routine of inflicting pain and then compromising. We would wager that the bond market is right and equities are wrong. Equities will converge to the downside, unless the market receives a concrete positive catalyst that improves the near-term outlook for U.S.-China relations and hence global trade. The problem is that for equities such a catalyst could happen at any time in the form of additional Chinese stimulus. Therefore, higher volatility is the only guaranteed outcome. The sudden onslaught of U.S. pressure makes it harder for Chinese President Xi Jinping to offer structural concessions to his American counterpart without looking weak. It was easier to do so when the threat of tariffs was under wraps, as was the case between December 1 and May 5. This new obstacle informed our decision to close out our long China equities and long copper trades and downgrade our end-June trade deal probability from 50% to 40%. But the escalation of tensions makes stimulus more likely to surprise to the upside, which will at least partially offset the negative hit to global sentiment and the trade outlook. Waiting For A Positive Political Intervention Three negative geopolitical catalysts loom in plain sight, while investors are still waiting on a positive catalyst. The negatives: China has not yet announced retaliation to the U.S. Commerce Department’s blacklisting of Huawei and a handful of other Chinese tech firms; the U.S. could implement the blacklist within three months, increasing the risk of a broader “tech blockade” against China; and the U.S. authorities are prepared to extend tariffs to all Chinese goods in one month. Meanwhile there are no high-level talks currently scheduled between the principal Chinese and American negotiators as we go to press. This could change quickly. But if negotiating teams do not hold substantive meetings with positive reports afterwards, then investors cannot be sure that Presidents Donald Trump and Xi Jinping will speak to each other, let alone finalize a substantive trade deal, at the G20 in Japan on June 28-29. The macro backdrop is hardly encouraging: global export volumes are contracting and the dollar’s fall may be arrested amid a huge spike in global policy uncertainty. Any rebound in the greenback will pile additional pressure onto trade flows, at least until the market sees a substantial increase in Chinese stimulus (Chart 2). Furthermore, it is concerning that President Trump, a businessman president and champion of American manufacturing, is raising tariffs at a time when lending and factory activity are already slowing in the politically vital Midwestern states (Chart 3). The implication is that he is unfazed by economic risks and therefore less predictable. He is pursuing long-term national foreign policy objectives at the expense of everything else. This may be patriotic but it will be painful for global equity investors. Chart 2Trump Unfazed By Deteriorating Global Economy

Trump Unfazed By Deteriorating Global Economy

Trump Unfazed By Deteriorating Global Economy

Chart 3Economic Activity Is Already Slowing

Economic Activity Is Already Slowing

Economic Activity Is Already Slowing

Chart 4Markets Blasé About Looming Risks

Markets Blasé About Looming Risks

Markets Blasé About Looming Risks

It is not only the S&P 500 that is failing to register the dangerous combination of weak global trade and escalating U.S.-China strategic conflict. Our colleague Anastasios Avgeriou of the BCA U.S. Equity Strategy points out that the “Ted spread,” the premium charged on interbank lending over the risk-free rate, is as docile as the safe-haven Japanese yen (Chart 4). President Xi Jinping, however, is not so blasé. He took a trip to Jiangxi province on May 20 to declare that China is embarking on a “new Long March.” This is a reference to the legendary strategic withdrawal executed by the early Chinese Communist Party in its civil war against the nationalists in 1934-35. It was an 8,000-mile slog across the rugged terrain of western and central China, peppered with battles against warlords and nationalists, in which nearly nine-tenths of the communist troops never made it. It is a historical event of immense propagandistic power used to celebrate the CPC’s resilience and ultimate triumph over corrupt and capitalist forces backed by imperialist Western powers. Most importantly, the Long March culminated in Mao Zedong’s consolidation of power over the party and ultimately the nation. In short, President Xi just told President Trump to “bring it on,” as he apparently believes that a conflict with the U.S. will strengthen his rule. The S&P 500 and the “Ted spread” are failing to register the dangerous combination of weak global trade and escalating U.S.-China strategic conflict. Trump, meanwhile, operates on a much shorter time horizon. He is coming closer to impeachment, as House Speaker Nancy Pelosi sharpens her rhetoric and negotiations over a bipartisan infrastructure bill collapse. Impeachment will fail and in the process will most likely help Trump’s reelection chances. But gridlock at home means that one of our top five “Black Swan” risks for 2019 is now being activated: Trump is at risk of becoming a lame duck and is therefore looking for conflicts abroad as a way of stirring up support at home. Bottom Line: The bad news in the trade war is all-too-apparent while good news is elusive. Yet key “risk off” indicators have hardly responded. We recommend going long JPY-USD on a cyclical basis on the expectation that the market will continue to have indigestion until a positive catalyst emerges in the trade talks. Trump’s Trade War Calculus

Chart 5

The trade war is focused on China more so than other states – and Trump likely has the public backing for such a conflict. President Trump delayed any Section 232 tariffs on auto and auto parts imports this month as the China trade war escalated (Chart 5). This confirms our reasoning that the nearly 50/50 risk of tariffs on car imports from Europe and Japan (recently upgraded from 35%) is contingent on first wrapping up a China deal. Another signal that Trump is conscientious not to saddle the equity market with too many trade wars is the decision finally to exempt Canada and Mexico from Section 232 aluminum and steel tariffs (Chart 6). It is now possible for Canada to ratify the deal before parliament dissolves in late June and for the U.S. and Mexico to follow. American ratification will involve twists and turns as the Democrats raise challenges but their obstructionism is ultimately fruitless as it will not hurt Trump’s approval ratings and labor unions largely support the new deal. Meanwhile a major hurdle relating to Mexican labor standards has already been met. These are positive developments for these markets and yet they call attention to a critical point about the Trump administration’s trade strategy: Trump has not shown much willingness to compromise his trade demands with allies in order to secure their cooperation in pressuring China. The threat of car tariffs is still looming over Europe (and even Japan and South Korea). In fact, a united front among these players would have made it much harder for China to resist structural changes (Chart 7). Chart 6Canada And Mexico Are Off The Hook

Canada And Mexico Are Off The Hook

Canada And Mexico Are Off The Hook

Chart 7A 'Coalition Of The Willing' Would Be More Effective

A 'Coalition Of The Willing' Would Be More Effective

A 'Coalition Of The Willing' Would Be More Effective

Nevertheless, we have long held that China, not NAFTA or Europe, would be the focus of Trump’s ire because there is much greater consensus within the U.S. political establishment on the need for a more muscular approach to China grievances, and hence fewer constraints on Trump. This view has now come full circle, at least for the time being. Bear in mind that while Republicans and even Democrats have a favorable view of international trade, in keeping with an improving economy (Chart 8), the U.S. as a whole is more skeptical of free trade than most other countries (Chart 9). The economy is insulated and globalization has operated unchecked for several decades, generating resentment.

Chart 8

Chart 9

Chart 10

This is especially relevant with China. Americans have an unfavorable view of China’s trade practices and China in general (Charts 10 and 11). This perception is getting worse as the great power competition heats up. Even a majority or near-majority of Democrats view China’s cyber-attacks, ownership of U.S. debt, environmental policies, and economic competition as causes of real concern (Chart 12). This means Trump is closer to the median voter when he is tough on China.

Chart 11

Chart 12

The result is a lower chance of a “weak deal,” i.e. a short-term deal to reduce the trade deficit primarily through Chinese purchases of commodities, since this will be a political liability for Trump. He may be forced into such a deal if the market revolts (say 35% odds). But otherwise he will hold out for something better, which Xi Jinping may be unwilling to give. China, not NAFTA or Europe, is the focus of Trump’s ire. This is why we rank “no deal” at 50%, more likely than any kind of deal (40%), though there is some chance of an extension of talks beyond the June G20 (10%). Bottom Line: The delay of auto tariffs and progress in replacing NAFTA suggest that the Trump administration is cognizant of the negative market impact of its trade wars and the need to focus on China. However, the risks to Europe and Japan are not yet removed. And any Chinese concessions will be weaker than might otherwise have been possible had Trump created a “coalition of the willing” to prosecute China’s violations of global trading norms. A weak deal makes it more likely that strategic conflict is the result. Trump Beats Bernie Beats Biden? Or Vice Versa? U.S. domestic politics are also pushing Trump in the direction of conflict with China. The American voter’s distrust of China explains why former Vice President Joe Biden, and leading contender for the Democratic Party nomination in 2020, recently caught flak from both sides of the aisle for being soft on China. At a campaign stop in Iowa on May 1, Biden said, “China is going to eat our lunch? Come on, man … They’re not competition for us.” He has made similarly dovish comments in the recent past. It makes sense, then, that Trump is trying to link “Sleepy Joe” (as he calls Biden) with weakness on China and trade. Biden, who is still enjoying a very sizable bump to his polling a month after formally announcing his candidacy (Chart 13), is a direct threat to Trump’s electoral strategy of maximizing white blue-collar turnout and support, particularly in the Midwestern swing states. Biden was on the ticket when President Barack Obama won these states in 2008 and 2012. He is a native son of Pennsylvania. And he appeals to the same voters as a plain-talking everyman.

Chart 13

Both Biden and Democratic Socialist Bernie Sanders of Vermont are beating Trump in the very early head-to-head polling for the 2020 presidential race. In fact, Sanders has a bigger lead over Trump than Biden in many of these polls (Chart 14).

Chart 14

Yet Sanders has a narrower path to victory in the general election – he is heavily dependent on the Rustbelt, where he could either win based on repeating the 2016 results in a new demographic context (the “Status Quo” scenario in Chart 15), or by winning back the blue-collar voters who abandoned the Democrats for Trump in 2016 (the “Blue Collar Democrats” scenario). Sanders performed well in these states in the Democratic primary in 2016, whereas he struggled in the South.

Chart 15

Chart 16Democrats Swung Too Far Left For Many Independents

Democrats Swung Too Far Left For Many Independents

Democrats Swung Too Far Left For Many Independents

Biden, on the other hand, is capable of winning not only in these two scenarios, but also by rebuilding the Obama coalition. He has a better bid to win over the black community due to his close association with Obama and his command of Democratic Party machinery, plus potentially his choice of running mate (the “Obama vs. Trump” scenario). By this means Biden, unlike Sanders, can compete against Trump in the Sun Belt and South in addition to the Midwest. Therefore, it is all the more imperative for Trump to try to corner Biden and frame the debate about Biden early. Trump may also be betting that despite the head-to-head polling, Sanders is too far left for the median voter. While the Democratic Party swings sharply to the left, the median voter remains more centrist, judging by the fact that independent voters (who make up half the electorate now) only slightly favor Democrats over Republicans, a trend that is only slightly rising (Chart 16). Biden’s polling is strong enough that he holds out the prospect of winning the Democratic nomination relatively smoothly, without deepening the ideological split in the party too much. Whereas Trump would benefit in the general election if Democrats suffered an internal split over a bloody primary season in which Bernie Sanders clawed his way to the nomination. The hit to American farmers is probably not a significant political constraint on President Trump waging his trade war. The upshot is that Trump is vulnerable in U.S. politics and will attempt to take action to strengthen his position. Meanwhile if Biden’s position on trade changes then we will know that he reads the Midwestern voter the same way Trump does – as a protectionist. Bottom Line: Trump’s eagerness to attack Biden reveals the specific threat that Biden poses to Trump’s electoral strategy as well as Trump’s calculus that a belligerent position on China is a vote-getter in the key Midwestern swing states. We expect Biden to become more hawkish on China, which will emphasize the long-term nature of the U.S.-China struggle and confirm the median voter’s appetite for hawkish policy. American Farmers Unlikely To Alter The 2020 Playing Field

Chart 17

Chart 18

Yet can Trump’s political base withstand the trade war? And can he possibly win the swing states if the trade war is escalating and damaging pocketbooks? There are many stories about farmers in the Midwest and other purple states who are deeply alarmed at Trump’s trade policies, prompting questions about whether he could be unseated there. American farmers have been among the hardest hit in the trade war. China was a major market for U.S. agricultural exports prior to the conflict (Chart 17). Since then U.S. agriculture has struggled, as exports to China have declined by more than 50% y/y in 2018 (Chart 18). Agricultural commodity prices are down ~10% since a year ago, with soybeans – the poster child of the conflict – trading at 10 year lows. Net farm incomes – a broad measure of profits – were on a downward trend prior to the trade war (Chart 19). While the USDA estimates that overall U.S. farm income will increase by 8.1% y/y this year, this follows a nearly 18% y/y decline in 2018 to reach the lowest level since 2002 (Chart 20). The recent escalation of the trade war will weigh on these incomes.

Chart 19

Chart 20

A common narrative in the financial media is that this hit to American farmers is a significant political constraint on President Trump in waging his trade war. He could be forced to accept a watered-down deal with China to preserve this voting bloc’s support ahead of November 2020, the thinking goes. Possibly, but probably not because of farmers abandoning the Republican Party en masse. First of all, rural counties and small towns continued supporting the Republican Party in the 2018 midterms, at a time when the initial negative impact of the trade war was front-page news (Chart 21). Second, some of the key farm states are unlikely to be key swing states in the election. Take soybeans, for example. Prior to the trade war, nearly 60% of U.S. soybean exports, and more than a third of U.S. soybeans, ended up in China. Illinois is the top producer, followed by Iowa and Minnesota. Last year soybean production in these three states accounted for 15%, 13%, and 8% of total U.S. production, respectively. As such, agriculture and livestock products exports to China in 1Q2019 are down 76% y/y in Illinois and 97% y/y in Minnesota. However, Trump won Iowa by nearly 150 thousand votes, a 9.4% margin, and there are not enough farmers in the state to overturn that margin. The negative impact on soybeans could prevent Trump from picking up Minnesota, where he lost by only 1.5% of the vote. But Minnesota is unlikely to cost him the White House in 2020. The picture is different in the key swing states of Michigan, Pennsylvania, and Wisconsin. Farming accounts for only ~1% of jobs in Michigan, Ohio, and Pennsylvania – and 2.3% of jobs in Wisconsin – and thus farmers represent a small share of the voting bloc in these states (Chart 22). But Trump won Michigan by a mere 0.23% of the vote, Pennsylvania by 0.72%, and Wisconsin by 0.77%. If one-fifth of farmers in these states switched their vote, Trump’s 2016 margin of victory would vanish.

Chart 21

Chart 22

Of course, manufacturers are a much larger voting bloc (Chart 23). And rural voters are unlikely to shift to the Democrats on such a large scale. Moreover, ag exports from these states have generally held up (Chart 24), the majority of their exports are destined for North America rather than China. The benefit from the recent thaw in North American trade relations will outweigh the loss of China as a market (Chart 25).

Chart 23

Chart 24

The Trump administration is also producing an aid package worth at least $15 billion to shield farmers at least partially from the trade war impact.1 This compares to an estimated $12 billion loss in net farm income in 2018.

Chart 25

Chart 26

Ultimately, Trump is much more threatened by other voting groups in these states. Young voters, women, minorities, suburbanites, and college-educated white voters all pose a threat to his thin margins if they turn out to vote and/or increase their support for the Democratic Party in 2020. A surge in Millennials, for instance, played the chief role in unseating Republican Governor Scott Walker in Wisconsin in 2018 (Chart 26). While midterm elections differ fundamentally from presidential elections, the Republicans lost 10 out of 12 significant elections in the Midwest during the midterms (Table 1). Table 1Republicans Lost Almost All Significant Midwest Elections In The Midterm

Is Trump Ready For The New Long March?

Is Trump Ready For The New Long March?

It is true that the winning Democratic candidates in the six major statewide races in Michigan, Pennsylvania, and Wisconsin all had voters who believed Trump’s trade policies were more likely to “hurt” the local economy than help it, according to exit polls (Chart 27). At the same time, a majority of voters believed that the trade policies either “helped” the local economy or “had no impact,” as opposed to hurting it. And Democrats are somewhat divided on this issue. Health care, not the economy, was the primary concern of voters. Moreover, health care, not the economy, was the primary concern of voters, especially Democratic voters (Chart 28). Republicans cared more about the economy and tended to support Trump’s trade policies.

Chart 27

Chart 28

In sum, unless the trade war causes a general economic slowdown that changes voter priorities, Trump’s chief threat in 2020 comes from urban and suburban voters angry over his attempt to dismantle the Affordable Care Act, rather than from farmers suffering from the trade war. The large bloc of manufacturing workers in the Midwestern battleground states helps to explain why Trump is willing to wage a trade war at such a critical time: loyal rural counties bear the brunt of the economic pain yet a tough-on-China policy could bring out swing voters from the manufacturing sector in suburbs and cities. Bottom Line: Trump could very well lose agriculture-heavy swing states in 2020, but it would not be because of losing his base among rural voters. Rather, it would be a result of a broader economic slowdown – or a superior showing of key demographic groups in favor of Democrats for other reasons like health care. The large bloc of manufacturing voters relative to Trump’s margins of victory helps to explain his aggressive posture on the trade war. Investment Conclusions Go long JPY-USD on a cyclical, 12-month horizon in the context of escalating trade war, complacent markets, and yet the prospect of additional Chinese stimulus improving global growth. This trade should be reinforced by the specific hurdles facing Japan over the next three to 18 months. While we would not be surprised if a trade agreement with the U.S. is concluded quickly, even ahead of any U.S.-China deal, nevertheless Japan faces upper house elections, a potential consumption tax hike, and preparations for a contentious constitutional revision and popular referendum on the cyclical horizon. On the expectation of greater Chinese stimulus, we are maintaining our long China Play Index call, which is up 2.2%. As a hedge against both geopolitical risk and the impact of Chinese stimulus over the cyclical horizon, go long spot gold. Matt Gertken, Vice President Geopolitical Strategy mattg@bcaresearch.com Roukaya Ibrahim, Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com Footnotes 1 While the plan is yet to be finalized, payments of ~$2/bushel to soybean farmers, $0.63/bushel to wheat farmers, and $0.04/bushel to corn farmers are under consideration. Unlike last year when the payments were distributed according to farmers’ current production, a potential modification to this year’s plan is that the payments will be distributed based on this years’ planted acreage and past yields.

Highlights The risk premium in crude oil prices is rising again, as policy risk – and the potential for large policy-driven errors – increases (Chart of the Week).1 This is not being fully reflected in options markets, where implied volatilities are trading close to their long-term average levels (Chart 2). In the past month, risks to oil flows – military and otherwise – and supply have risen, which is keeping a bid under prices. The Sino – U.S. trade war has worsened, and threatens to put global supply chains at risk, along with EM demand growth in the medium term. Meanwhile, amid global monetary easing, the USD has strengthened, producing a more immediate headwind for EM commodity demand. Against this backdrop of opposing forces, oil prices remain elevated and relatively stable in the low $70/bbl range for Brent. Our balances estimates and price forecasts have not changed materially this month. However, the balance of risks has widened in both tails of the price distribution. We expect implied volatilities in the crude oil options markets – particularly Brent – to move higher, as a result. As for prices, we continue to expect Brent to average $75/bbl this year and $80/bbl next year, with WTI trading $7/bbl and $5/bbl below those levels in 2019 and 2020, respectively. Energy: Overweight. The U.S. EIA moved closer to our fundamental assessment and Brent forecast in its most recent market update, lifting its Brent spot-price expectation for this year to an average of $70/bbl, ~ $5/bbl above its April forecast. The EIA’s revision reflects “tighter expected global oil market balances in mid-2019 and increasing supply disruption risks globally.” Base Metals: Neutral. In the wake of Vale’s January supply disaster at its Córrego do Feijão mine, iron ore shipments from Brazil were down 60% in April y/y. Cyclones disrupted supply in Western Australia, pushing 62% Fe iron ore prices to a 5-year high above $100/MT last week. Chinese steelmakers registered a 12.7% y/y gain in crude steel output last month, which, along with dockside iron ore inventory draws of ~ 20 MT ytd, is supporting prices generally. Precious Metals: Neutral. A stronger USD is weighing on gold. Global geopolitical tensions – chiefly in the Persian Gulf and in Sino – U.S. trade relations – are keeping prices above $1,270/oz. We remain long gold as a portfolio hedge. Ags/Softs: Underweight. Severe weather conditions in the Midwest continues to delay corn planting, and is contributing to a rally this week in corn prices to $3.94/bushel on Tuesday, up $3.48/bushel from last week’s level. Feature The risk of a military confrontation between the U.S. and Iran is higher than it was a month ago and rising. Should it erupt, such a confrontation would threaten oil exports from the Persian Gulf through the Strait of Hormuz, where ~ 20% of global supply transits daily.2 Bellicose rhetoric from the U.S. – some of it directed at materially reducing Iran’s influence in Iraq – alternately is ramped up and walked back, while attacks on soft targets in the Kingdom of Saudi Arabia (KSA) – e.g., oil shipping and west-bound oil pipelines – draw attention to the exposure of this critical infrastructure, upon which global oil markets rely.3 Iran, meanwhile, uses the media to prepare its population for further economic deprivation, and to lob its own vituperative rhetoric at the U.S.

Chart 1

Venezuela’s collapse as an oil producer and exporter continues unabated, keeping markets for the heavier sour crude favored by U.S. refiners tight. Civil war threatens to cut into Libyan production, which we are carrying at just over 1mm b/d, while whiffs of another Arab Spring can be detected in Algeria, where popular discontent with ruling elites grows.4 On the demand side, the summer driving season is about to kick off in the Northern Hemisphere, heralding increased gasoline demand. Countering that, the Sino – U.S. trade war shows signs of devolving into a Cold War, which could force a re-ordering of supply chains globally, lifting costs and consumer-level inflation in the process. Longer-term, this could work against central-bank easing globally, and retard growth in EM consumer demand. The risk of a military confrontation between the U.S. and Iran is higher than it was a month ago and rising. Should it erupt, such a confrontation would threaten oil exports from the Persian Gulf through the Strait of Hormuz. For the present, we continue to expect EM demand growth to hold up, expanding by 1.5mm b/d this year and 1.6mm b/d next year. This will be supported by continued monetary easing globally, and additional fiscal stimulus from China if its trade war with the U.S. worsens. There is a chance weakness in DM demand will persist, but we think the odds of a normal seasonal pick-up in 2H19 will continue to support demand overall (Chart 3). That said, given the threats to demand growth – an expanded Sino – U.S. trade war and stronger USD, in particular – we will continue to monitor the health of EM demand closely. Chart 2Brent Implied Volatility Will Move Higher

Brent Implied Volatility Will Move Higher

Brent Implied Volatility Will Move Higher

Chart 3DM Oil Demand Growth Wobbles, EM Steady

DM Oil Demand Growth Wobbles, EM Steady

DM Oil Demand Growth Wobbles, EM Steady

OPEC 2.0 Maintains Production Discipline Chart 4OPEC 2.0's Production Discipline, Strong Demand Drained Inventories

OPEC 2.0's Production Discipline, Strong Demand Drained Inventories

OPEC 2.0's Production Discipline, Strong Demand Drained Inventories

The goal of OPEC 2.0 from its inception at the end of 2016 has been to drain OECD inventories, which swelled to 3.1 billion barrels in July 2016, on the back of a market-share war launched by the old OPEC under the leadership of KSA, and a surge in U.S. shale-oil production. KSA continues to stress the need to restrain crude oil production so as to draw down global oil inventories, and has done much of the heavy lifting this year to make that happen (Chart 4). The other putative leader of OPEC 2.0, Russia, continues to express misgivings with such a strategy, arguing instead the producer coalition should make more oil available to the market. We are more aligned with Russia’s view, and continue to believe OPEC 2.0 will need to increase production. In our balances (Table 1), our base case assumes those producers that can lift production – core OPEC and Russia – will do so to keep prices below $85/bbl (Chart 5). We expect OPEC 2.0 will be able to offset the loss of ~ 700kb/d from Iran exports by increasing production gradually from May to September in proportion to its quota agreement. In our base case, we have Iranian exports falling to 600k b/d. We continue to expect OPEC 2.0 to be able to offset the loss of Venezuela’s production throughout the year, which we expect to fall to 500k b/d by December (vs. ~ 735k b/d presently). Going into next month’s Vienna meeting, we do not expect KSA to dramatically increase production, but would not be surprised if it took production from its current 9.8mm b/d level closer to its OPEC 2.0 quota of 10.33mm b/d in 2H19. Table 1BCA Global Oil Supply - Demand Balances (MMb/d, Base Case Balances)

Policy Risk Sustains Oil's Unstable Equilibrium

Policy Risk Sustains Oil's Unstable Equilibrium

Going into next month’s Vienna meeting, we do not expect KSA to dramatically increase production, but would not be surprised if it took production from its current 9.8mm b/d level closer to its OPEC 2.0 quota of 10.33mm b/d in 2H19. We also expect Russia to lift its production closer to 11.6mm b/d from ~ 11.4mm b/d at present. Even with OPEC 2.0 lifting production ~ 900k b/d in 2H19 vs. 1H19, the bulk of global production increases will be concentrated in the U.S., where we expect shale-oil output to grow 1.2mm b/d this year, and 840k b/d next year. This will account for 85% of the overall increase of 2.4mm b/d we expect in the U.S. this year and next. Our estimates of production growth in the U.S. shales is tempered by a growing conviction the large integrated oil majors and stand-alone E&P companies will continue to put the interests of shareholders above their desire to increase production just for the sake of increasing it, as was done in the past. This is driven by a desire to attract and retain capital, which will be critical to the majors and the big E&Ps in the years ahead.5 We continue to see demand growth exceeding supply growth this year. This will produce a physical deficit, which will continue to drain inventories. Even with these production increases, we continue to see demand growth exceeding supply growth this year. This will produce a physical deficit, which will continue to drain inventories (Chart 6). Chart 5Core OPEC 2.0 Will Lift Production

Core OPEC 2.0 Will Lift Production

Core OPEC 2.0 Will Lift Production

Chart 6Balances Continue To Tighten

Balances Continue To Tighten

Balances Continue To Tighten

Spare Capacity Will Be Stretched

Chart 7

In addition to Iran and Venezuela, we are closely following what appears to be the early stages of another civil war in Libya, which threatens the ~ 1mm b/d of production flowing from there. In addition, we are seeing signs of growing civil discontent in Algeria not unlike that of 2011, which was sparked by popular dissatisfaction with ruling elites throughout the Middle East in the lead-up to the Arab Spring. We have maintained existing spare capacity can handle the loss of Iranian and Venezuelan production and exports we’ve built into our balances and price-forecast models. However, covering these losses will stretch the capacity of global supply to accommodate unplanned outages, which could leave markets extremely tight in the event of production losses in Libya or Nigeria, or in producing provinces prone to natural disasters (e.g., Canadian wildfires or U.S. Gulf hurricanes). At present, markets appear to be comfortable with OPEC 2.0’s ability to cover losses from Iran and Venezuela, given current spare capacity of ~ 3mm b/d, most of which remains in KSA, and continued growth in non-OPEC output (Chart 7). As inventories continue to draw globally, markets’ attention will turn more toward this spare capacity. Expect Higher Volatility We remain long Brent call spreads in July and August 2019, which are up an average 101% since they were recommended in February. These positions benefit from higher prices and higher volatility. Chart 8Geopolitics, Increasing Backwardation Support Higher Brent Implied Volatility

Geopolitics, Increasing Backwardation Support Higher Brent Implied Volatility

Geopolitics, Increasing Backwardation Support Higher Brent Implied Volatility

Our fundamental assessments of supply, demand and inventory levels remain fairly steady. Thus, our price forecasts – $75 and $80/bbl this year and next for Brent, with WTI trading $7 and $5/bbl under that – remain unchanged. With OPEC 2.0 maintaining production discipline and U.S. shale producers maintaining capital discipline, the rate of growth on the supply side will be restrained, and below the rate of growth in global demand. These forces combine to keep inventories drawing this year, which will lead to a steeper backwardation in forward curves, particularly Brent’s (Chart 8). Coupled with true uncertainty re how the U.S. – Iran confrontation in the Persian Gulf is resolved, and how the Sino – U.S. trade war plays out, this steepening backwardation will lead to higher implied volatility in crude oil options markets. Bottom Line: Our expectation of higher prices and steepening backwardation in forward curves is supported by our analysis of fundamentals and the current political economy of global oil markets, which emphasizes policy risk arising from the actions of geopolitically significant states. These factors also will push implied volatility in options markets higher. As a result, we remain long Brent call spreads in July and August 2019, which are up an average 101% since they were recommended in February. These positions benefit from higher prices and higher volatility. We also remain long 2H19 Brent vs. short 2H20 Brent futures in line with our view backwardation will increase; this position is up 155.4% since it was initiated in February, as a result of the steepening of backwardation in the forward curve. Steepening backwardation also will benefit our long S&P GSCI recommendation, which is heavily weighted to energy markets; this position is up 8% since inception. Lastly, we remain long spot WTI, which is up 34.6% since it was recommended in January. Robert P. Ryan, Chief Commodity & Energy Strategist rryan@bcaresearch.com Hugo Bélanger, Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com Footnotes 1 In the price decomposition shown in our Chart of the Week, we account for the contribution that changes in global supply, demand and inventory levels make to the evolution of Brent prices, using a proprietary econometric model. We treat the residual term of the model – what’s left of the price decomposition after these fundamental variables are accounted for – as a measure of the risk premium in prices. An expansion of the risk premium – in the positive or negative direction – is coincident with an expansion of the implied volatility of Brent crude oil options typically expands (sometimes with a lag or two), and vice versa. This is intuitively appealing, since risk premia and volatility expand as uncertainty in the market rises. 2 We considered this topic in depth in a Special Report written with BCA Research’s Geopolitical Strategy entitled “U.S., OPEC Talk Oil Prices Down; Gulf Tensions Could Become Kinetic,” published July 19, 2018, and in “Brinkmanship Fuels Chaos In Oil Markets, And Raises The Odds Of Conflict In The Gulf,” published July 5, 2018. Both reports are available at ces.bcaresearch.com. 3 Iran’s influence in Iraq is an internally divisive issue, and a focal point of the U.S., a view we share. Please see, “Iraq: The Fulcrum Of Middle East Geopolitics And Global Oil Supply,” a Special Report we published with BCA Research’s Geopolitical Strategy September 5, 2018. KSA and Western intelligence agencies allege Iran is behind the attacks on Saudi oil infrastructure. Please see “Saudi Arabia accuses Iran of ordering drone attack on oil pipeline,” published by reuters.com. The westbound pipelines in KSA are critical to maintaining the Kingdom’s export capacity, as we noted in “Risk Premium In Oil Prices Rising; KSA Lifts West Coast Export Capacity,” published by BCA Research’s Commodity & Energy Strategy October 25, 2018. This report is available at ces.bcaresearch.com. 4 Please see “Algeria Has a Legitimacy Problem,” posted on the LSE’s Middle East Centre Blog by Benjamin P. Nickels on May 20, 2019, and “Algeria’s Second Arab Spring?” by Ishac Diwan posted at project-syndicate.org March 28, 2019. 5 We will be exploring this topic in depth in a Special Report next month. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades TRADE RECOMMENDATION PERFORMANCE IN 2019 Q1

Policy Risk Sustains Oil's Unstable Equilibrium

Policy Risk Sustains Oil's Unstable Equilibrium

Commodity Prices and Plays Reference Table Trades Closed in 2019 Summary of Trades Closed in

Policy Risk Sustains Oil's Unstable Equilibrium

Policy Risk Sustains Oil's Unstable Equilibrium

With all U.S. imports from China affected, price rises will percolate upward through all tradable industries and consumer goods. Two points are worth noting: The domestic value-add of Chinese exports to the U.S. is not as low as consensus holds. China’s…

There are at least five reasons for the true cost of a trade war being higher than expected. A trade war would degrade the value of the existing stock of human and physical capital. This would result in lower potential GDP. It would also lead to…

Highlights Duration: We see current bond market behavior as very similar to mid-2016, when heightened political uncertainty obscured the economy’s true strength and kept bond yields lower for longer than was justified by the economic fundamentals. The correct strategy at that time was to sell into the bond market’s strength, and we advocate a similar strategy today. China: Any attempt by the Chinese government to retaliate in the trade war by selling U.S. Treasury securities would be either self-defeating or ineffective, depending on the exact strategy employed. In either case, U.S. Treasury yields will be unaffected. Fed: At least part of the Fed’s dovish turn might represent a desire to send the labor share of national income higher. We introduce a new data series for Fed Watchers to track. Feature The Trump Administration fired the latest salvo in the trade war two weeks ago, expanding tariffs to a broader swathe of Chinese imports. Then last week, the escalation of tensions spilled over to the bond market, sending global yields abruptly lower. Chart 1Flight To Safety

Flight To Safety

Flight To Safety

The 10-year U.S. Treasury yield bounced off 2.35% last Thursday and has since settled at 2.39% (Chart 1). Meanwhile, the overnight index swap curve is now priced for 44 bps of Fed rate cuts over the next 12 months (Chart 1, bottom panel). It is possible, and even likely, that geopolitical tensions will keep yields low during the next month or two. In fact, our Geopolitical Strategy service places the odds of a complete breakdown in trade negotiations by the end of June at 50%.1 But we would encourage investors to sell into rallies, positioning for higher yields on a 6-12 month horizon. To see why, we return to a Weekly Report from early April where we walked through different factors that would be useful in the creation of a macroeconomic model for the 10-year U.S. Treasury yield.2 We consider what has changed during the past six weeks and what those developments mean for bond yields going forward. Back In The Bond Kitchen In early April, we ran through four different factors that should be included in any bond model and suggested macroeconomic indicators that best capture the trends in each. The four factors are: Global Growth: Best proxied by the Global Manufacturing PMI and Bullish Dollar Sentiment Policy Uncertainty: Best proxied by the Global Economic Policy Uncertainty Index Output Gap: Best proxied by Average Hourly Earnings Sentiment: Best proxied by the U.S. Economic Surprise Index We consider each factor in turn. Global Growth Chart 2Monitoring Global Growth

Monitoring Global Growth

Monitoring Global Growth

The Global Manufacturing PMI, our preferred series for tracking global growth, ticked down during the past month, continuing the free-fall that has been in place since the end of 2017 (Chart 2). At 50.3, it is now only slightly above the 50 boom/bust line and is close to where it was in mid-2016, when the 10-year yield hit its cyclical low. But on a positive note, several leading indicators have hooked up in recent months, suggesting that the Global PMI could soon trough and move higher in the second half of the year. Specifically, the ZEW survey of global economic sentiment is off its lows, as is the BCA Global Leading Economic Indicator (LEI). Meanwhile, the Global LEI Diffusion Index has surged, indicating that 74% of the 23 countries in our sample are seeing improvement in their LEIs. Historically, the Global LEI Diffusion Index leads changes in both the Global LEI and the Global Manufacturing PMI (Chart 2, panel 3). Financial market prices that are highly geared to global growth had been singing a similar tune, but they rolled over as trade tensions flared during the past two weeks. For example, cyclical equity sectors recently started to underperform defensive sectors (Chart 2, bottom panel), and the important CRB Raw Industrials index took a nosedive. We place particular importance on the CRB Raw Industrials index as a timely indicator of global growth, because the ratio between the CRB index and gold correlates nicely with the 10-year Treasury yield (Chart 3).3 Unsurprisingly, the ratio’s recent dip coincides with last week’s drop in the 10-year. Several leading indicators have hooked up in recent months, suggesting that the Global PMI could soon trough and move higher in the second half of the year. In addition to the Global Manufacturing PMI, we recommend including a survey of bullish sentiment toward the U.S. dollar in any bond model. More bullish dollar sentiment coincides with lower Treasury yields, and vice-versa. Our preferred survey shows that dollar sentiment remains elevated, but hasn’t changed much since April (Chart 4). The dollar itself, however, has begun to appreciate during the past two weeks (Chart 4, bottom panel). Chart 3A Falling CRB/Gold Ratio...

A Falling CRB/Gold Ratio...

A Falling CRB/Gold Ratio...

Chart 4...And The Greenback Is On The Rise

...And The Greenback Is On The Rise

...And The Greenback Is On The Rise

Bottom Line: The coincident global growth indicators that correlate best with bond yields – the Global Manufacturing PMI and Dollar Bullish Sentiment – are sending a similar message as in April. Meanwhile, leading economic indicators continue to suggest that we should expect improvement in the second half of the year. The biggest change from April is that global growth indicators derived from financial market prices – cyclical versus defensive equities, the CRB Raw Industrials index and the trade-weighted dollar – have responded negatively to heightened political risk. If this weakness persists and eventually infects the economic data, then it could prevent a second-half rebound in global growth, keeping Treasury yields low for even longer. Policy Uncertainty Spikes in the monthly Global Economic Policy Uncertainty Index often cause capital to seek out the safety of U.S. Treasuries, and we recommend including this index in any macroeconomic bond model (Chart 5A). Spikes in the monthly Global Economic Policy Uncertainty Index often cause capital to seek out the safety of U.S. Treasuries. While there have been no updates to the monthly index since the trade war’s recent escalation, one of its components – a daily index that tracks the number of relevant news stories – has surged during the past two weeks (Chart 5B). This clearly illustrates that a sharp increase in political uncertainty has been the catalyst for the bond market rally. Investors are obviously concerned that an ongoing and intensifying trade war might derail the economic recovery, and they are seeking out Treasuries as a hedge. Chart 5AGlobal Uncertainty Set To Spike

Global Uncertainty Set To Spike

Global Uncertainty Set To Spike

Chart 5BMarkets Are Concerned

Markets Are Concerned

Markets Are Concerned

In such situations, the traditional playbook is to fade any purely uncertainty-driven rally, on the view that markets tend to overreact to headline risk. This strategy worked well following the mid-2016 Brexit vote. The uncertainty shock from the vote sent the 10-year quickly down to 1.37%, but it then increased in the second half of the year when it became apparent that the economic recovery would continue. While higher tariffs will certainly be a drag on growth going forward, accommodative Fed policy and a probable increase in Chinese economic stimulus will mitigate the impact, keeping the economic recovery intact.4 Output Gap Chart 6Wages Are Headed Higher

Wages Are Headed Higher

Wages Are Headed Higher

The output gap is a concept that represents where the economy is operating relative to its peak capacity, and its progress during the past three years is the main reason why bond yields will not re-test 2016 lows. We have found that wage growth is the most reliable way to measure the output gap: higher wage growth signals less spare capacity, and less spare capacity coincides with higher bond yields. We recommend Average Hourly Earnings as the best wage measure to include in any bond model. Since April, average hourly earnings growth has been roughly flat, but leading indicators suggest that further acceleration is highly likely in the coming months (Chart 6). While the Fed is keen to let wage growth accelerate, rising wage growth also makes a rate cut difficult to justify. The combination of rising wage growth and an on-hold Fed should put a rising floor under long-maturity bond yields. Sentiment The final factor that should be included in any bond model is sentiment. In April, we suggested that the U.S. Economic Surprise Index is the best measure of sentiment. When the surprise index has been deeply negative for a long time, it usually means that investors are downbeat on the economy and that the bar for a positive surprise is low. This has actually been the case in recent months, and our simple auto-regressive model suggests that the surprise index is biased higher (Chart 7). Positioning data confirm this message, and in fact show that investors are taking as much duration risk as they were when yields troughed in mid-2016 (Chart 8). Chart 7Low Bar For Positive Surprises

Low Bar For Positive Surprises

Low Bar For Positive Surprises

Chart 8Similar Positioning As In Mid-2016

Similar Positioning As In Mid-2016

Similar Positioning As In Mid-2016

The overall message is that bond investors have a very dim view of the economy, and it will not take much positive news to send yields higher. Investment Strategy We see current bond market behavior as very similar to mid-2016, when heightened political uncertainty obscured the economy’s true strength and kept bond yields lower for longer than was justified by the economic fundamentals. The correct strategy at that time was to sell into the bond market’s strength, and we advocate a similar strategy today. Timing when the next move higher in bond yields will occur is difficult, but we take some comfort in the fact that the flatness of the yield curve makes it less costly than usual to carry below-benchmark duration positions. In fact, the average yield on the Bloomberg Barclays Cash index is 7 bps higher than the average yield on the Bloomberg Barclays Treasury Master Index. Bond investors have a very dim view of the economy, and it will not take much positive news to send yields higher. To further mitigate the cost of keeping duration low, we advocate taking duration-neutral positions that are short the belly (5-year & 7-year) part of the yield curve and long the very long and very short ends of the curve. Such trades are also provide a positive yield pick-up, and will earn capital gains when Treasury yields move higher.5 A Quick Note On China’s Treasury Purchases Chart 9Do Not Expect Treasuries To Be Used As A Weapon In This War

Do Not Expect Treasuries To Be Used As A Weapon In This War

Do Not Expect Treasuries To Be Used As A Weapon In This War

The trade war’s recent escalation has led some to speculate that China could retaliate against higher tariffs by dumping U.S. Treasury securities onto the open market. The speculation only increased when the TIC data revealed that Chinese net Treasury purchases totaled -$24 billion in March, the most deeply negative figure since October 2016 (Chart 9). We see low odds that China will employ this tactic in the trade war, and no meaningful impact on Treasury yields in any case. To see why, let’s consider two possible scenarios. In the first scenario, China sells a large amount of U.S. Treasury securities and keeps the proceeds from the sales in its domestic currency. Assuming the amounts in question are sufficiently large, these transactions would cause the RMB to appreciate and lead to a tightening of Chinese monetary conditions. Tighter monetary conditions are exactly what the Chinese government does not want as it seeks to counteract the negative economic impact from tariffs. In fact, China is much more likely to engineer a further easing of monetary conditions, much like in 2015/16 (Chart 9, bottom panel). In the second scenario, China could sell U.S. Treasuries and purchase other foreign bonds (German bunds, for example). This would nullify any impact on Chinese monetary conditions, but it would not have much impact on U.S. Treasury yields. With Chinese money still flowing into global bond markets, the re-balancing would only push other investors out of non-U.S. bond markets and into U.S. Treasuries. Without changing the overall demand for global bonds, it is difficult to envision much of an impact on U.S. yields. Bottom Line: Any attempt by the Chinese government to retaliate in the trade war by selling U.S. Treasury securities would be either self-defeating or ineffective, depending on the exact strategy employed. In either case, U.S. Treasury yields will be unaffected. A New Data Series For Fed Watchers: Rich’s Ratio A number of recent Fed speeches have referred to the time series plotted in Chart 10: The share of national income going to labor, as opposed to corporate profits. Chart 10Introducing Rich's Ratio

Introducing Rich's Ratio

Introducing Rich's Ratio

Vice-Chair Richard Clarida brought this analysis to the Fed, and the data series was actually once dubbed “Rich’s Ratio” by Clarida’s old PIMCO colleague Paul McCulley. The idea behind Rich’s Ratio is that while some late-cycle wage gains are passed through to prices, a portion also eat into corporate profits. Notice in Chart 10 that Rich’s Ratio has a tendency to rise late in the economic recovery. Based on his past writings, we would not be surprised if at least part of the Fed’s recent dovish turn represents a desire to send Rich’s Ratio higher, even if that goal might entail a modest overshoot of the Fed's 2 percent inflation target. We will have more to say about Rich’s Ratio in the coming weeks. For now, we simply want to make Fed Watchers aware that they have a new series to track. Stay tuned. Ryan Swift, U.S. Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see Geopolitical Strategy Weekly Report, “How Trump Became A War President”, dated May 17, 2019, available at gps.bcaresearch.com 2 Please see U.S. Bond Strategy Weekly Report, “Bond Kitchen”, dated April 9, 2019, available at usbs.bcaresearch.com 3 The rationale for why the CRB/Gold ratio tracks the 10-year Treasury yield is found in U.S. Bond Strategy Weekly Report, “The Search For Aaa Spread”, dated March 12, 2019, available at usbs.bcaresearch.com 4 Please see Global Investment Strategy Weekly Report, “Tarrified”, dated May 16, 2019, available at gis.bcaresearch.com 5 Please see U.S. Bond Strategy Weekly Report, “Paid To Wait”, dated February 26, 2019, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification