Geopolitics

Highlights Four ghosts of 2016 are knocking at the door: Brexit, Trump, Brazil, Italy. President Trump and U.S. trade policy are keeping uncertainty high. Upgrade the odds of a no-deal Brexit to about 33%. Expect limited stimulus from Italy and Germany – for now. Brazil’s pension reform is entering its final stretch – buy the rumor, sell the news. Feature Four major political events of 2016 are returning to affect the global investment landscape this fall – though only two of these ghosts are truly frightening. In order of market relevance: Trump: The election of Donald J. Trump as U.S. president, November 8, 2016 Brexit: The U.K. referendum to leave the European Union, June 23, 2016 Italy: The Italian constitutional referendum, December 4, 2016 Brazil: The removal of Brazilian President Dilma Rousseff, August 31, 2016 Italy and Brazil are producing market-positive political results in the short run. Brexit and Trump pose substantial and immediate risks to the global bull market. A pivot by Trump is the headline risk to our view that no trade agreement will be concluded by November 2020, as we outlined in a Special Report last week. At the moment tensions are still escalating. President Trump has ordered an increase in tariffs (Chart 1) and threatened to invoke the International Economic Emergency Powers Act of 1977, which would give him the ability to halt transactions, freeze funds, and appropriate assets. China is retaliating proportionately and virtually incapable of softening its tone prior to its National Day celebration on October 1. The next round of negotiations, slated for Washington in September, could be a flop like the talks in July, or it could be canceled. Investors should stay defensive. The equity market will have to fall to force Trump to stage a tactical retreat. Meanwhile China could intervene violently in Hong Kong SAR. That possibility, the nationalist military parade on October 1, and U.S. actions toward the South China Sea and Taiwan, show that sabers are rattling, causing additional market jitters. Chart 1Trump's Latest Tariff Salvo

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

U.S.-China tensions underpin our tactical safe-haven trade recommendations. But we are not shifting to a cyclically bearish stance until we get clarity on Trump’s and Xi’s handling of their immediate predicament. Brexit is the other acute short-term risk. This was true even before Prime Minister Boris Johnson opted to prorogue parliament from September 10 to October 14, shortening the time that parliament has to either pass a law forbidding a no-deal exit or bring down Johnson’s government in a vote of no confidence. We are upgrading the odds of “no deal” to no higher than 33%, using a conservative decision-making process (Diagram 1). No-deal is not our base case because parliament, the public, and even Johnson himself want to avoid a recession, which is the likely outcome, even granting that the Bank of England will not stand idly by. We are upgrading the odds of “no deal” Brexit to about 33%. Diagram 1Brexit Decision Tree (Revised August 29, 2019)

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

From a bird’s eye point of view, the pound is very attractive (Chart 2). But in the near-term the twists and turns of Britain’s political struggle imply that we will see wild volatility. Our foreign exchange strategists expect that a no-deal Brexit would cause GBP/USD to collapse to 1 after October 31. Assuming our one-in-three odds of such an outcome, the probability-weighted average of cable is about 1.2. Hence investors should not short sterling from here, unless they strongly believe we are underrating the odds of no-deal exit. In the worst-case scenario, a no-deal Brexit will cause an economic shock at a time when Europe is on the brink of recession – Italy and Germany are virtually there. This means there is a substantial risk of additional deflationary pressure piling onto German bunds and sustaining the global bond rally. This pressure will be sharply reduced if Johnson loses an early no confidence vote, but that is a 50/50 call so we would not call time on this rally yet. Stay cautious. Chart 2Pound Can Only Go So Low

Pound Can Only Go So Low

Pound Can Only Go So Low

Italy: Stimulus … Without A Bruising Brussels Battle Italy has avoided a new election by producing an unusual tie-up between the establishment Democratic Party and the anti-establishment Five Star Movement (M5S). The coalition still needs to clear some internal hurdles and an online vote by Five Star members, but an agreement is to be presented to President Sergio Mattarella as we go to press. This is the most market-friendly outcome that could have been expected, as is clear through the sharp drop in Italian government bond yields (Chart 3). Our GeoRisk indicator for Italy is also collapsing. Chart 3Markets Cheer New Italian Coalition

Markets Cheer New Italian Coalition

Markets Cheer New Italian Coalition

This development marks the climax of a story line that we outlined in 2016, when Prime Minister Matteo Renzi lost a constitutional referendum that aimed to strengthen Italian governments to enable deeper structural reforms (he subsequently resigned). At that time we argued that Italy would emerge as a market-relevant political risk due to rampant anti-establishment sentiment, but that this risk would subside when Italy’s populists were shown to be pragmatic at heart, i.e. unwilling to push their conflicts with Brussels to a point that truly reignited European break-up risk. This view is now vindicated – and not only for the short-term. The new coalition comes at the nick of time, with Europe teetering on recession and the risk of a no-deal Brexit rising. The new government will have to deliver the 2020 budget to the European Commission by October 15. The budget will aim to provide fiscal support, including a delay of the legislatively mandated hike in the Value Added Tax from 22% to 24.2%, already rolled over from 2019. The Five Star Movement will demand as a price for its participation in the coalition that social spending go up; the Democratic Party will have learned a lesson while out of power and will be more fiscally permissive and strike a tougher tone with Brussels. The Italian budget talks will be a non-issue: the coalition will cooperate with Brussels. The episode demonstrates that the Italian risk to financial markets is overrated. This point goes beyond the fact that the Democrats and Five Star were able to cooperate. Italy’s leading populist parties have already shown that they are pragmatic and will play the game with Brussels to avoid a financial breakdown. In May 2018, the newly formed populist coalition proposed a gigantic “wish list” budget that would have increased the budget deficit to roughly 7.3% of GDP in 2019. They also appointed a euroskeptic economy minister who almost prevented government formation. The ensuing conflict with Brussels triggered considerable turmoil (Chart 4). Ultimately, however, the populists did precisely what we expected: they bowed to the severe financial constraint on Italy’s banking system. They agreed to a 2019 and 2020 deficit of 2.04% and 2.1%, respectively (Chart 5). Chart 4Italian Populists Prove Pragmatic

Italian Populists Prove Pragmatic

Italian Populists Prove Pragmatic

Chart 5Even Salvini Compromised On Budget Clash

Even Salvini Compromised On Budget Clash

Even Salvini Compromised On Budget Clash

At present, the market is relieved that an election was avoided that might have seen Salvini and the League form a government with a much smaller right-wing party (Fratelli D’Italia) (Chart 6) – but the truth is that Salvini had already capitulated to the EU, both on budget matters and the euro currency. He was hardly likely to push for a budget more aggressive than that of the initial proposal in 2018. The clash with Brussels would have been a flash in the pan; the result would have been greater fiscal thrust, which would have been market-positive in the current environment. Chart 6Election Would Have Meant More Stimulus ... And More Political Risk

Election Would Have Meant More Stimulus ... And More Political Risk

Election Would Have Meant More Stimulus ... And More Political Risk

M5S will also push for more spending and has also moderated their stance on the euro. A coalition with the Democrats will not work if the purpose is to push a euroskeptic agenda. There will be a focus on counter-cyclical fiscal policy, pragmatic reforms that the two can agree on, and fighting corruption. The budget talks will be a non-issue: the Democratic Party is an establishment party and the coalition will cooperate with Brussels. Furthermore, the context has changed since 2018 in a way that will reduce budget frictions. There is a need for countercyclical fiscal policy in light of the global slowdown, so the European Commission will have to be more flexible on the budget. This is particularly true if Germany itself loosens its belt on a cyclical basis. The risk to the above is that the coalition shaping up between the Democrats and Five Star is an alliance of convenience that will break down over time. Five Star will remain hard-line on immigration, which is driving anti-establishment sentiment. Italian elections are a frequent affair. Salvini and the League will be waiting in the wings, especially if Brussels proves too tight-fisted or if the Democrats do not toughen their stance on immigration. But as outlined above, Salvini’s own evolution on the euro, on northern Italy, and on the budget and financial stability shows that the economy will have to get a lot worse before Italian euroskepticism presents a renewed systemic risk. Bottom Line: The tentative coalition taking shape in Italy will produce a modest increase in fiscal thrust with minimal frictions with Brussels. As such it is the most market-friendly outcome that could have occurred from Salvini’s push to seize power. Beneath this episode of government change is the political arrangement taking shape in Italy, and across Europe, which calls for a commitment to the European project and currency. The price of this commitment is a tougher line on immigration from European leaders. Germany: Fiscal Loosening, But Not For The States (Yet) Our GeoRisk indicator for Germany is pointing to an increase in risk in recent weeks. Germany is threatened by a potential technical recession and while fiscal stimulus is in preparation, there will not be a fiscal game-changer until Merkel steps down in 2021 – barring a total collapse in the economy that forces her hand in the meantime. The outlook is not improving (Chart 7, top panel). The economy shrank by 0.1% in Q2 2019, exports are falling, and passenger car production is at the lowest level ever recorded (Chart 7, bottom panels). Chart 7German Economy Gets Pummeled

German Economy Gets Pummeled

German Economy Gets Pummeled

Chart 8Germany: Expect Orthodox Stimulus For Now

Germany: Expect Orthodox Stimulus For Now

Germany: Expect Orthodox Stimulus For Now

Finance Minister Olaf Scholz has announced that Germany could increase government spending by $55 billion within the context of European and German budget constraints. Split proportionally between 2019 and 2020, this additional spending would not put Germany in violation of the “black zero” rule – a commitment to a balanced budget that limits the federal structural deficit to 0.35% of GDP – even without any additional revenue (Chart 8). There will not be a fiscal game-changer in Germany until Merkel steps down – barring a crisis. The German Chancellery reports that it does not see the need for stimulus in the short term – as long as trade tensions do not escalate and there is no hard Brexit. At present, however, trade tensions are escalating and the odds of a no-deal Brexit are increasing. Moreover China’s economy and stimulus efforts continue to disappoint. In this context Germany’s ruling coalition is putting together a climate change package that would entail additional spending (while stealing some thunder from the increasingly popular Green Party). Given the European Commission’s forecast of Germany’s 2020 budget surplus, 0.8% of GDP, the government could ultimately go further than Scholz’s ~$50bn. This is because the black zero rule provides for exceptions in case of recession (or natural disasters or other crises out of governmental control) with a majority vote in the Bundestag. Hence we are not so much concerned about the magnitude of the stimulus as its timing. First, Merkel and her coalition typically move slower than the market would like in the face of financial and economic challenges. Second, according to the black zero rule, which is transcribed in the German constitution (the Basic Law), the Länder cannot run budget deficits from 2020. Amending the constitution to delay this deadline requires a two-thirds majority in the Bundestag and the Bundesrat – a much taller order than the simple majority needed to boost federal deficits. The governing coalition currently holds 56% of the seats in the Bundestag. If the Greens were brought on board, which they would be inclined to do, this number falls just short of two-thirds at 65.6%. In order to obtain a two-thirds majority in the Bundesrat, the Social Democrats, Christian Democrats, and the Greens would need the support of another party, either the Left or the Free Democrats. This could be done but it would require political will, which is only likely to be sufficient if the German and global economy get worse from here. Meanwhile financial markets will have to settle for the gradual implementation of a stimulus package on the order of 1% of GDP – the one the government is planning. Bottom Line: While Germany will likely roll out a stimulus package by Q4, if third quarter GDP data confirm that the country is in a technical recession, Merkel’s hesitation and budget limits mean that this stimulus will likely be moderate. A marginal upside surprise is possible but it will not represent a true “game changer” on fiscal policy in Germany. The game changer is more likely after Merkel steps down in 2021. The Green Party is surging in Germany and could possibly lead the next government. Even if it doesn’t, its success and Europe-wide developments are pushing German leaders to become more accommodative. Brazil: Reform Or Bust Political turmoil in Brazil over the past five years has ultimately resulted in a right-wing populist government under President Jair Bolsonaro. Bolsonaro is pursuing a pension reform that is universally acknowledged as necessary to straighten out Brazil’s fiscal books, but that the previous government tried and failed to pass. On this front the news is market-positive: having cleared the lower Chamber of Deputies, the pension reforms are now likely to pass the senate. This will lift investor confidence and give Bolsonaro an initial success that he may then be able to translate into additional economic reforms. The Brazilian economy and financial markets are moving in opposite directions. The currency and equities staged a mid-year rally despite negative data releases – shrinking retail sales and industrial production amid high unemployment (Chart 9). More recently these assets relapsed despite tentative signs of improvement on the economic front (Chart 10). All the while, chaos and controversies surrounding Bolsonaro’s government have weighed on his approval rating, ending the honeymoon period after election (Chart 11). Chart 9Brazil: Signs Of Improvement

Brazil: Signs Of Improvement

Brazil: Signs Of Improvement

Chart 10Brazil: Markets Sold Despite Pension Progress

Brazil: Markets Sold Despite Pension Progress

Brazil: Markets Sold Despite Pension Progress

Chart 11Bolsonaro’s Honeymoon Is Long Gone

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

The mid-year equity re-rating was driven by an improvement in sentiment on the back of the government’s pension reform. The relapse occurred despite the passage of the pension reform bill in the lower house, indicating that global economic pessimism has dominated. The bill’s next step goes to the senate where it faces two rounds of voting before enactment (Diagram 2). It should clear this hurdle by a large margin, though we expect delays. Diagram 2Brazil: Pension Reform Timeline

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

In the second round vote in the lower house on August 6 – which had a smaller margin of victory than the first round – deputies voted largely in line with party alliances (Charts 12A & 12B). Assuming legislators in the senate behave in the same way, the reform should gain the support of 64 of the 81 senators – easily surpassing the 49 votes needed. Even in a more pessimistic scenario where all opposition parties and all independent parties vote against the bill – along with two defecting senators from government-allied parties – the reform would pass by 56-25. Chart 12APension Bill Sailed Through Lower House ...

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Chart 12B... And Should Pass Senate In Time

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

This favorable outlook is also supported by popular opinion, which indicates that the majority of those polled agree that pension reforms are necessary (Chart 13). This leaves two questions: How soon will the bill clear the senate? According to senate party leaders’ proposed timetable, the bill will undergo its first upper house vote on September 18 with the second round slated for October 2. This is ambitious. The strategy of Senator Tasso Jereissati – who has been appointed senate pension reform rapporteur – is to approve the text in its current form and create a parallel proposed amendment to the constitution (PEC) which will bring together the amendments that senators make to the original text. Dozens of amendments have been filed with the Commission on Constitution and Justice. These will prolong the enactment of the final bill and dilute its impact. We doubt the senate will let Jereissati have his way entirely and hence expect delays and dilution. Chart 13Brazil: Public Now Favors Pension Reform

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Chart 14Brazil: Pension Reform Not Enough

Brazil: Pension Reform Not Enough

Brazil: Pension Reform Not Enough

How much savings will the bill generate? Will the reforms be sufficient to improve public debt dynamics in Brazil? The Independent Fiscal Institute of the senate estimates that the reform will generate BRL 744 billion of savings. This is significantly less than the BRL 1.2 trillion initially proposed, and lower than the BRL 860 billion that Economy Minister Paulo Guedes has indicated as the minimum fiscal savings required. Our Emerging Markets strategists argue that the bill falls short of what is needed. While the plan will reduce the fiscal deficit and slow debt accumulation, it will be insufficient to generate primary surpluses over the coming years (Chart 14).1 Moreover, estimated savings in the final bill will likely be further revised down as the bill undergoes more amendments in the senate. What comes after pension reform? The market has focused almost exclusively on this issue to the neglect of Bolsonaro’s wider economic reform agenda. The agenda includes privatization, trade liberalization, tax reforms, and deregulation. Here we are more skeptical. First, Bolsonaro will have spent a lot of political capital on pensions. Second, while the economy and unemployment are always important, they are not the foremost concern for Brazilians (Chart 15). Chart 15Bolsonaro Will Lose Political Capital After Pension Bill

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Third, the economic agenda is often at odds with Bolsonaro’s social, foreign, and environmental policies: The new Mercosur-European Union trade agreement and ongoing trade negotiations between Mercosur and Canada are positive developments. However the G7 summit in France highlighted that the deal with the EU is at risk due to dissatisfaction with Bolsonaro’s response to the Amazon fires. France and Ireland have threatened to withhold support of the ratification. With world leaders concerned about the political risks of trade liberalization, and with Trump having issued a license to foreign leaders for trade weaponization, an escalation of tensions between the Europeans and Bolsonaro could lead to punitive measures even beyond the delay to the Mercosur-EU deal. Brazil’s China problem: Bolsonaro has been cozying up to President Donald Trump while striking a more aggressive tone with China. This is a risky strategy as it may undermine Brazil’s economic interests. The country’s exports are much more leveraged to China than to the U.S. and have been benefitting on the back of the trade war as China substitutes away from the U.S. (Chart 16). The president’s planned trip to China in October reveals an attempt to mend ties after having accused China of dominating key Brazilian sectors during his election campaign. But it is not clear yet that Bolsonaro will stage a retreat. And if President Trump backtracks on his trade war in order to clinch a deal, Bolsonaro may have lost some goodwill with China without receiving the benefit of China’s substitution effects. Hence Bolsonaro will have to soften his approach to China to make progress on the trade aspect of the reform agenda. Chart 16Brazil: Time To Mend Ties With China

Brazil: Time To Mend Ties With China

Brazil: Time To Mend Ties With China

Bottom Line: We expect the passage of a diluted pension reform bill that will slow the growth of public debt to some extent. However global headwinds are persisting. And any success on pensions should not be extrapolated to other items on the economic reform agenda. Bolsonaro’s trade liberalization faces difficulties on the surface. Other domestic reforms are even more difficult to achieve in the wake of painful pension cuts. Reforms that enjoy public support and do not require a complicated legislative process are the most likely to be implemented, but even then, legislation and implementation are likely to be long-in-coming in Brazil’s highly fractured congress. As a result we share the view with our Emerging Markets Strategy that the pension reform is a “buy the rumor, sell the news” phenomenon. Housekeeping We are booking gains on our long BCA global defense basket for a 17% gain since inception in October 2018. The underlying thesis for this trade remains strong and we will reinstitute it at an appropriate time, though likely on a relative basis to minimize headwinds to cyclical sectors. We are also finally throwing in the towel on our long rare earth / strategic metals equity trade. The logic behind the trade is intact but it was very poorly timed and the basket has depreciated 24% since inception. Matt Gertken, Vice President Geopolitical Strategist mattg@bcaresearch.com Roukaya Ibrahim, Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com Ekaterina Shtrevensky, Research Analyst ekaterinas@bcaresearch.com Footnotes 1 Please see BCA Research’s Emerging Markets Strategy Weekly Report “On Chinese Banks And Brazil,” dated July 18, 2019, available at ems.bcaresearch.com. France: GeoRisk Indicator

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

U.K.: GeoRisk Indicator

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Germany: GeoRisk Indicator

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Italy: GeoRisk Indicator

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Spain: GeoRisk Indicator

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Russia: GeoRisk Indicator

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Korea: GeoRisk Indicator

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Taiwan: GeoRisk Indicator

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Turkey: GeoRisk Indicator

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Brazil: GeoRisk Indicator

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

What's On The Geopolitical Radar?

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Four Ghosts Of 2016 - GeoRisk Update: August 30, 2019

Geopolitical Calendar

Highlights The chance of a U.S.-China trade agreement by November 2020 is still only 40% – but an upgrade may be around the corner. Trump is on the verge of a tactical trade retreat due to fears of economic slowdown and a loss in 2020. Xi Jinping is now the known unknown. His aggressive foreign policy is a major risk even if Trump softens. Political divisions in Greater China – Hong Kong unrest and Taiwan elections – could harm the trade talks. Maintain tactical caution but remain cyclically overweight global equities. Feature “I am the chosen one. Somebody had to do it. So I’m taking on China. I’m taking on China on trade. And you know what, we’re winning.” – U.S. President Donald J. Trump, August 21, 2019 On August 1, United States President Donald Trump declared that he would raise a new tariff of 10% on the remaining $300 billion worth of imports from China not already subject to his administration’s sweeping 25% tariff. Then, on August 13, with the S&P 500 index down a mere 2.4%, Trump announced that he would partially delay the tariff, separating it into two tranches that will take effect on September 1 and December 15 (Chart II-1). Chart II-1Trump's Latest Tariff Salvo

Trump's Latest Tariff Salvo

Trump's Latest Tariff Salvo

Six days later Trump’s Commerce Department renewed the 90-day temporary general license for U.S. companies to do business with embattled Chinese telecom company Huawei, which has ties to the Chinese state and is viewed as a threat to U.S. network security.

Chart II-2

The same pattern played out on August 23 when President Trump responded to China’s retaliatory tariffs by declaring he would raise tariffs to 30% on the first half of imports and 15% on the remainder by December 15. Within a single weekend he softened his rhetoric and said he still wanted a deal. Trump’s tendency to take two steps forward with coercive measures and then one step back to control the damage is by now familiar to global investors. Yet this backpedaling reveals that like other politicians he is concerned about reelection. After all, there is a clear chain of consequence leading from trade war to bear market to recession to a Democrat taking the White House in November 2020. Trump’s approval rating is already similar to that of presidents who fell short of re-election amid recession (Chart II-2) – an actual recession would consign him to history. Will Trump Stage A Tactical Retreat On Trade? Yes. Trump’s predicament suggests that he will have to adjust his policies. Global trade, capital spending, and sentiment have deteriorated significantly since the last escalation-and-delay episode with China in May and June. Beijing’s economic stimulus measures disappointed expectations, exacerbating the global slowdown (Chart II-3). This leaves him less room for maneuver going forward. The fourth quarter of 2019 may be Trump’s last chance to save the business cycle and his presidency. Even “Fortress America” – consumer-driven and relatively insulated from global trade – has seen manufacturing, private investment, and business sentiment weaken. GDP growth is slowing and has been revised downward for 2018 despite a surge in budget deficit projections to above $1 trillion dollars (Chart II-4). Chart II-3China's Gradual Stimulus Yet To Revive Global Economy

China's Gradual Stimulus Yet To Revive Global Economy

China's Gradual Stimulus Yet To Revive Global Economy

Chart II-4Trump's Economy Grew Slower Than Thought Despite Fiscal Stimulus

Trump's Economy Grew Slower Than Thought Despite Fiscal Stimulus

Trump's Economy Grew Slower Than Thought Despite Fiscal Stimulus

The U.S. Treasury yield curve inversion is deepening. While we at BCA would point out reasons that this may not be a reliable signal of imminent recession, Trump cannot afford to ignore it. He is sensitive to the widening talk of “recession” in American airwaves and is openly contemplating stimulus options (Chart II-5). His approval rating has lost momentum, partly due to his perceived mishandling of a domestic terrorist attack motivated by racist anti-immigrant sentiment in El Paso, Texas, but negative financial and economic news have likely also played a part (Chart II-6). Chart II-5Trump Fears Growing Talk Of Recession

Trump Fears Growing Talk Of Recession

Trump Fears Growing Talk Of Recession

In short, the fourth quarter of 2019 may be Trump’s last chance to save the business cycle and his presidency. The core predicament for Trump continues to be the divergence in American and Chinese policy. In the U.S., the stimulating effect of Trump’s Tax Cut and Jobs Act is wearing off just as the deflationary effect of his trade policy begins to bite. In China, the lingering effects of Xi’s all-but-defunct deleveraging campaign are combining with the trade war, and slowing trend growth, to produce a drag on domestic demand and global trade. The result is a rising dollar, which increases the trade deficit – the opposite of what Trump wants and needs (Chart II-7).

Chart II-6

Chart II-7Trump's Fiscal Policy Undid His Trade Policy

Trump's Fiscal Policy Undid His Trade Policy

Trump's Fiscal Policy Undid His Trade Policy

The United States is insulated from global trade, but only to a point – it cannot escape a global recession should one develop (Chart II-8). With global and U.S. equities vulnerable to additional volatility in the near term, Trump will have to make at least a tactical retreat on his trade policy over the rest of the year. First and foremost this would mean: Chart II-8If Total Trade War Causes A Global Relapse, The U.S. Economy Cannot Escape

If Total Trade War Causes A Global Relapse, The U.S. Economy Cannot Escape

If Total Trade War Causes A Global Relapse, The U.S. Economy Cannot Escape

Expediting a trade deal with Japan – this should get done before a China deal, possibly as early as September. Ratifying the U.S.-Mexico-Canada “NAFTA 2.0” agreement – this requires support from moderate Democrats in Congress. The window for passage is closing fast but not yet closed. Removing the threat to slap tariffs on European car and car part imports in mid-November. There is some momentum given Europe’s need to boost growth and recent progress on U.S. beef exports to the EU. Lastly, if financial and economic pressure are sustained, Trump will be forced to soften his stance on China. The problem for global risk assets – in the very near term – is that Trump’s tactical retreat has not fully materialized yet. The new tariff on China is still slated to take effect on September 1. This tariff hike or other disagreements could result in a cancellation of talks or failure to make any progress.1 Even if Trump does pivot on trade, China’s position has hardened. It is no longer clear that Beijing will accept a deal that is transparently designed to boost Trump’s reelection chances. Thus, the biggest question in the trade talks is no longer Trump, but Xi. Is Xi prepared to receive Trump kindly if the latter comes crawling back? How will he handle rising political risk in Hong Kong SAR and Taiwan island,2 and will the outcome derail the trade talks? The biggest question in the trade talks is no longer Trump, but Xi. Bottom Line: Global economic growth is fragile and President Trump has only rhetorically retracted his latest salvo against China. Nevertheless, the clear signal is that he is sensitive to the financial and economic constraints that affect his presidential run next year – and therefore investors should expect U.S. trade policy to turn less market-negative on the margin in the coming months. This is positive for the cyclical view on global risk assets. But the risk to the view is China: whether Trump will take a conciliatory turn and whether Xi will reciprocate. Can Xi Jinping Accept A Deal? Yes. It is extremely difficult for Xi Jinping to offer concessions in the short term. He is facing another tariff hike, U.S. military shows of force, persistent social unrest in Hong Kong, and a critical election in Taiwan. Certainly, he will not risk any sign of weakness ahead of the 70th anniversary of the People’s Republic of China on October 1, which will be a nationalist rally in defiance of imperialist western powers. After that, however, there is potential for Xi to be receptive to any Trump pivot on trade. China’s strategy in the trade talks has generally been to offer limited concessions and wait for Trump to resign himself to them. Concessions thus far are not negligible, but they can easily be picked apart. They consist largely of preexisting trends (large commodity purchases); minor adjustments (e.g. to car tariffs and foreign ownership rules); unverifiable promises (on foreign investment, technological transfer, and intellectual property); or reversible strategic cooperation (partial enforcement of North Korean and Iranian sanctions) (Table II-1). Many of these concessions have been postponed as a result of Trump’s punitive measures.

Chart II-

It is unlikely that Beijing will offer much more under today’s adverse circumstances. The exception is cooperation on North Korea, which should improve. So the contours of a deal are generally known. This is what Trump will have to accept if he seeks to calm markets and restore confidence in the economy ahead of his election. But this slate of concessions is ultimately acceptable for the U.S. Chart II-9China's Ultimate Economic Constraint

China's Ultimate Economic Constraint

China's Ultimate Economic Constraint

China’s demands are that Trump roll back all his tariffs, that purchases of U.S. goods must be reasonable in scale, and that any agreement be balanced and conducted with mutual respect. Of these three, the tariffs and the “respect” pose the most trouble. Trade balance: Washington and Beijing can agree on the terms of specific purchases. China can increase select imports substantially – it remains a cash-rich nation with a state sector that can be commanded to buy American goods. Tariff rollback: This is tougher but can be done. The U.S. will insist on some tariffs – or the threat of tech sanctions – as an enforcement mechanism to ensure that Beijing implements the structural concessions necessary for an agreement. But China might accept a deal in which tariffs were mostly rolled back – say to the original 25% tariff on $50 billion worth of goods. This would likely offset the degree of yuan appreciation to be expected from the likely currency addendum to any agreement. Balance and respect: This qualitative demand is the sticking point. Fundamentally, China cannot reward Trump for his aggressive and unilateral protectionist measures. This would be to set a precedent for future American presidents that sweeping tariffs on national security grounds are a legitimate way of coercing China into making economic structural reforms. Moreover if the U.S. wants to improve the trade balance, China thinks, it cannot embargo Chinese high-tech imports but must actually increase its high-tech exports. Clearly this is a major impasse in the talks. The last point, mutual respect, is the likeliest deal-breaker. It may ultimately hinge on strategic events outside of the realm of trade. But before discussing it further, it is important to recognize that China is not invincible – it has a pain threshold. Deterioration in China’s labor market is of utmost seriousness to any Chinese leader (Chart II-9). And the economy is still struggling to revive. Xi’s reform and deleveraging campaign of 2017-18 has largely been postponed but the lingering effects are weighing on growth and the property sector remains under tight regulation. Moreover the removal of implicit guarantees, and rare toleration of creative destruction (Chart II-10), have left banks and corporations afraid to take on new risks. The state’s reflationary measures, including a big boost to local government spending, have so far been merely sufficient for domestic stability. Chart II-10Creative Destruction In China

Creative Destruction In China

Creative Destruction In China

These problems can be addressed by additional policy easing. But the domestic political crackdown and the break with the U.S. have shaken manufacturers and private entrepreneurs to the bone, suppressing animal spirits and reducing the demand for loans. Ultimately a short-term trade deal to ease this economic stress would make sense for Xi Jinping, even though he knows that U.S. protectionism and the conflict over technological acquisition will persist beyond 2020 and beyond Trump. The threat of a sharp and destabilizing divorce from the U.S. is a real and present danger to the long-term stability of China’s economy and the Communist regime. Xi is a strongman leader, but is he really ready for Mao Zedong-style austerity? Is he not more like former President Jiang Zemin (ruled 1993-2003), who imposed some austerity while prizing domestic economic and political stability above all? To this question we now turn. Bottom Line: China has become the wild card in the trade war. Trump’s need to prevent a recession is known. Beijing has a higher pain threshold and could walk away from the deal to punish Trump (upsetting the global economy and diminishing Trump’s reelection prospects). This would set the precedent for future American presidents that China will not bow to gunboat diplomacy. Will Xi Jinping Overplay His Hand? Be Afraid. For decades China’s main foreign policy principle has been to “lie low and bide its time,” to paraphrase former leader Deng Xiaoping. In the current context this means maintaining a willingness to engage with the U.S. whenever it engages sincerely. This approach implies making the above concessions to minimize the immediate threat to stability from the trade war, while biding time in the longer run rivalry against the United States. Such an approach would also imply assisting the diplomatic process on the Korean peninsula, avoiding a military crackdown in Hong Kong, and refraining from aggressive military intimidation ahead of Taiwan’s election in January. Chart II-11China's Vast Market Its Most Persuasive Tool

China's Vast Market Its Most Persuasive Tool

China's Vast Market Its Most Persuasive Tool

After all, there is no better way for the Communist Party to undercut dissidents in Hong Kong and Taiwan than to strike a deal with the United States. This would demonstrate that Xi is a pragmatic leader who is still committed to “reform and opening up.” It would help generate an economic rebound that would bring other countries deeper into Beijing’s orbit (Chart II-11). China’s vast domestic market is ultimately its greatest strength in its contest with the United States. In short, conventional Chinese policy suggests that Xi should perpetuate the long success story since 1978 by striking another deal with another Republican president. The catch is that Xi Jinping is not conventional. Since coming to power in 2012, Xi has eschewed the subtle strategies of Sun Tzu and Deng Xiaoping in favor of a more ambitious approach: that of declaring China’s arrival as a major power and leveraging its economic and military heft to pursue foreign policy and commercial interests aggressively. Xi’s reassertion of Communist rule and state-guided technological acquisition is the biggest factor behind the new U.S. political consensus – entirely aside from Trump – that China is foe rather than friend. There are several empirical reasons to think that Xi might overplay his hand: Xi failed to make substantive concessions with President Barack Obama’s administration on North Korea, the South China Sea, and cyber security, resulting in Obama’s decision to harden U.S. policy toward both China and North Korea in 2015 – a trend that predates Trump. Xi formally removed presidential term limits from China’s constitution even though he could have attracted less negative attention from the West by ruling from behind the scenes after his term in office, like Deng Xiaoping or Jiang Zemin. China has mostly played for time in negotiations with the Trump administration, as mentioned, and this aggravated tensions. Deep revisions to the draft agreement, and the extent of tariff rollback which was supposedly 90% complete, broke the negotiations in May, sparking this summer’s standoff. Aggressive policies in territorial disputes have alienated even China’s potential allies. This includes regional states whose current ruling parties have courted China in recent years, in some cases obsequiously – South Korea, the Philippines, and Vietnam. The East and South China Seas remain a genuine source of “black swans” – unpredictable, low-probability, high-impact events – due to their status as critical sea lanes for the major Asian economies. China continues to militarize the islands there and aggressively prosecute its maritime-territorial disputes. We calculate that $6.4 trillion worth of goods flowed through this bottleneck in the year ending April 2019, 8% of which consists of energy goods from the Middle East that are vital to China and its East Asian neighbors, none of whom can stomach Chinese domination of this geographic space (Diagram II-1). Even if Washington abandoned the region, Japan, South Korea, and Taiwan would see Chinese control as a threat to their security. Ultimately, however, China’s adventures in its neighboring seas are a matter of choice. Not so for Greater China – in Hong Kong and Taiwan, political risk is rapidly mounting in a way that enflames the U.S.-China strategic distrust and threatens to prevent a trade agreement.

Chart II-

Hong Kong: The Dust Has Not Settled Mass protests in Hong Kong have lost some momentum, based on the size of the largest rally in August versus June. But do not be fooled: the political crisis is deepening. A plurality of Hong Kongers now harbors negative feelings toward mainland Chinese people as well as the government in Beijing – a trend that is spiking amid today’s protests but began with the Great Recession and has roots in the deeper socioeconomic malaise of this capitalist enclave (Chart II-12A & II-12B).

Chart II-12

Chart II-12

A majority also lacks confidence in the political arrangement that ensures some autonomy from Beijing – known as “One Country, Two Systems” (Chart II-13). This is a particularly worrisome sign since this is the fundamental basis for stable political relations with Beijing.

Chart II-13

With clashes continuing between protesters and police, students calling for a boycott of school this fall, and Beijing rotating troops into the city and openly drilling its security forces in Shenzhen for a potential intervention, Hong Kong’s unrest is not yet laid to rest and could flare up again ahead of China’s sensitive National Day celebration. U.S. tariffs and sanctions are already in effect, reducing the ability of the U.S. to deter China from using force if it believes instability has gone too far. And as President Trump has warned – and would be true of any U.S. administration – a violent crackdown on civilian demonstrators would greatly reduce the political viability of a trade deal in the United States. Taiwan: The Black Swan Arrives Since Taiwan’s 2016 election, we have argued that it is a potential source of “black swans.” Mass protests in Hong Kong may have taken the cake. But these protests are now affecting the Taiwanese election dynamic and potentially the U.S.-China trade talks. Chart II-14U.S. Approves Big New Arms Sale To Taiwan

U.S. Approves Big New Arms Sale To Taiwan

U.S. Approves Big New Arms Sale To Taiwan

On August 20, the United States Department of Defense informed Congress that it is proceeding with an $8 billion sale of F-16 fighter jets and other military arms and equipment to Taiwan – the largest sale in 22 years and the largest aircraft sale since 1992 (Chart II-14). This sale is not yet complete and delivered, but ultimately will be – the question is the timing. Arms sales to Taiwan are a perennial source of tension between the United States and China – and China is increasingly assertive in using economic sanctions to get its way over such issues, as it showed in the lead up to South Korea’s election in 2017. This sale is not a military “game changer” – the U.S. did not send over fifth-generation F-35s, for instance – but China will respond vehemently. It is threatening to impose sanctions on American companies like Lockheed Martin and General Electric for their part in the deal. The sale does not in itself preclude the chance of a trade agreement but it contributes to a rise in strategic tensions that ultimately could. Chart II-15A 'Fourth Taiwan Strait Crisis' Would Have A Seismic Equity Impact

A 'Fourth Taiwan Strait Crisis' Would Have A Seismic Equity Impact

A 'Fourth Taiwan Strait Crisis' Would Have A Seismic Equity Impact

The context is Taiwan’s hugely important election in January. Four years ago, President Tsai Ing-wen and her pro-independence Democratic Progressive Party swept to power on the back of a popular protest movement – the “Sunflower Movement” – that opposed deeper cross-strait economic integration. It dangerously resembled the kind of anti-Communist “color revolutions” that motivate Xi Jinping’s hardline policies. Tsai shocked the world when she called Trump personally to congratulate him after his election, which violated diplomatic protocol given that Taiwan is a territory of China and not an independent nation-state. Since then Trump has largely avoided provoking the Taiwan issue so as not to strike at a core Chinese interest and obliterate the chance of a trade deal. But the U.S. has always argued that the provision of defensive arms to Taiwan is a condition of the U.S.-China détente – and Trump is so far moving forward with the sale. How will Xi Jinping react if the sale goes through? In 1995-96, China’s use of missile tests to try to intimidate Taiwan produced the opposite effect – driving voters into the arms of Lee Teng-hui, the candidate Beijing opposed. This was the occasion of the Third Taiwan Strait Crisis, in which U.S. President Bill Clinton sent two aircraft carriers to the region, one that sailed through the Taiwan Strait. The negative effect on markets at that time was local, whereas anything resembling this level of tensions would today be a seismic global risk-off (Chart II-15). Since the 1990s, leaders in Beijing have avoided direct military coercion ahead of elections. But Xi Jinping has hardened his stance on Taiwan throughout his term. He has dabbled with such coercion in his use of military drills that encircle Taiwan in recent years. While one must assume that he will use economic sanctions rather than outright military threats – as he did with South Korea – saber-rattling cannot be ruled out. The pressure on him is rising. Prior to the Hong Kong unrest, Taiwan’s elections looked likely to return the pro-mainland Kuomintang (KMT) to power and remove the incumbent President Tsai – a boon for Beijing. That outlook has changed and Tsai now has a fighting chance of staying in power (Chart II-16). The prospect of four more years of Tsai would not be too problematic for Beijing if not for the fact that the U.S. political establishment is now firmly in agreement on challenging China. But even if Tsai loses, Taiwan’s outlook is troublesome. And this makes Xi’s decision-making harder to predict. Taiwan has a lot more dry powder for a political crisis in the long run than Hong Kong. It is not that Tsai or her party will necessarily prevail. The manufacturing slowdown will take a toll and third-party candidates, particularly Ko Wen-je, would likely split Tsai’s vote. Moreover her Democratic Progressives still tie the KMT in opinion polling (Chart II-17). The Taiwanese people are primarily concerned about maintaining the strong economy and cross-strait peace and stability, which her reelection could jeopardize (Chart II-18). Tsai could very well lose, or she could be a lame duck presiding over the KMT in the legislature.

Chart II-16

Chart II-17

Rather, the problem for Xi Jinping is that the Taiwanese people clearly sympathize with the protesters in Hong Kong (Chart II-19). They fear that their own governance system faces the same fate as Hong Kong’s, with the Communist Party encroaching on traditional political liberties over time.

Chart II-18

Chart II-19

While Hong Kong ultimately has zero choice as to whether to accept Beijing’s supremacy, Taiwan has much greater autonomy – and the military support of outside forces. It is not a foregone conclusion that Taiwan must suffer the same political dependency as Hong Kong. Indeed, Taiwan has a long history of exercising the democratic vote and has even dabbled into the realm of popular referendums. In short, Taiwan has a lot more dry powder for a political crisis in the long run than Hong Kong. But the Hong Kong events have accentuated this fact, for two key reasons: First, Taiwanese people identify increasingly as exclusively Taiwanese, rather than as both Taiwanese and Chinese (Chart II-20). The incidents in Hong Kong reveal that this sentiment is tied to immediate political relations and therefore deterioration would encourage further alienation from the mainland. Second, while a strong majority of Taiwanese wish to maintain the political status quo to avoid conflict with the mainland, a substantial subset – approaching one-fourth – supports eventual or immediate independence (Chart II-21).

Chart II-20

Chart II-21

This means that relations with the mainland will eventually deteriorate even if the KMT wins the election. The KMT itself must respond to popular demand not to cozy up too much with Beijing, which is how it fell from power in 2016. Meanwhile, under KMT rule, Taiwan’s progressive-leaning youth are likely to set about reviving their protest movement in the subsequent years and imitating their Hong Kong peers, especially if the KMT warms up relations too fast with the mainland. Ultimately these points suggest that Xi Jinping will strive to avoid a violent crackdown in Hong Kong. A crackdown would be the surest way for him to harm the KMT in the Taiwanese election and to hasten the rebuilding of U.S.-Taiwan security ties. Call The President The best argument for Xi to lie low and avoid a larger crisis in Greater China is that it would unify the West and its allies against China. So far Xi’s foreign policy has not been so aggressive as to lead to diplomatic isolation. Europe is maintaining a studied neutrality due to its own differences with the United States; Asian neighbors are wary of provoking Chinese sanctions or military threats. A humanitarian crisis in Hong Kong or a “Fourth Taiwan Strait Crisis” would change that. For markets, the best-case scenario is that Xi Jinping exercises restraint. This would help Hong Kong protests lose steam, North Korean diplomacy get back on track, and Taiwanese independence sentiment simmer down. China would be more likely to halt U.S. tariffs and tech sanctions, settle a short-term trade agreement, and delay the upgrade in U.S.-Taiwan defense relations. China would still face adverse long-term political trends in both the U.S. and Taiwan, but an immediate crisis would be averted. The worst-case scenario is that Xi indulges his ambition. Hong Kong protests could explode, relations with Taiwan would deteriorate, and U.S.-China relations would move more rapidly in their downward spiral. Trade talks could collapse. Xi Jinping would face the possibility of a unified Western front, instability within Greater China, and a global recession. This might get rid of Donald Trump, but it would not get rid of the U.S. Congress, Navy, or Department of Defense. The choice seems pretty clear. Xi, like Trump, faces constraints that should motivate a tactical retreat from confrontation, at least after October 1. While this does not necessarily mean a settled trade agreement, it does suggest at least a ceasefire or truce. Our GeoRisk indicators show that market-based political risk in Taiwan – and less so South Korea – moves in keeping with global economic policy uncertainty. The underlying U.S.-China strategic confrontation and trade war are driving both (Chart II-22). A deterioration in this region has global consequences. Chart II-22U.S.-China Strategic Conflict Fuels Global Economic Uncertainty And Taiwanese Geopolitical Risk In Tandem

U.S.-China Strategic Conflict Fuels Global Economic Uncertainty And Taiwanese Geopolitical Risk In Tandem

U.S.-China Strategic Conflict Fuels Global Economic Uncertainty And Taiwanese Geopolitical Risk In Tandem

Xi is a markedly aggressive “strongman” Chinese leader who has not been afraid to model his leadership on that of Chairman Mao. He could still overplay his hand. This is why we maintain that the odds of a U.S.-China trade agreement remain 40%, though we are prepared to upgrade that probability if Trump and Xi make pro-market decisions. Investment Implications On the three-month tactical horizon, BCA’s Geopolitical Strategy is paring back our tactical safe-haven trades: we are closing our “Doomsday Basket” of long gold and Swiss bonds for a gain of 13.6%, while maintaining our simple gold portfolio hedge going forward. Trump has not yet decisively staged his tactical retreat on trade policy, while rising political risk in Greater China increases uncertainty over Xi Jinping’s next moves. On the cyclical horizon, the above suggests that there is a light at the end of the tunnel – if both Trump and Xi recognize their political constraints. This means that there is still a political and geopolitical basis to reinforce BCA’s House View to remain optimistic on global and U.S. equities over the next 12 months, with the potential for non-U.S. equities to recover and bond yields to reverse their deep dive. Matt Gertken Vice President Geopolitical Strategy Footnotes 1 Negotiations between Trump and Xi are slated for September in Washington. There is a prospect for Trump to hold another summit with Communist Party General Secretary Xi Jinping on the sidelines of the United Nations General Assembly in New York in late September and at the APEC summit in Chile in mid-November. 2 Hong Kong is a Special Administrative Region of the People’s Republic of China, while Taiwan is recognized as a province or territory.

Highlights The U.S.-Sino trade war is taking a dangerous turn, but the U.S. should avoid a recession until 2022. Global growth will bottom in early 2020. The Fed is set to cut rates two to three times in the next year. Safe-haven bonds have more tactical upside, but will perform poorly on a cyclical basis. Long-term investors should use the next six to nine months to offload their corporate bonds. Equities will be volatile for the rest of 2019; a breakout is forecast for 2020. Long-term investors should favor stocks over bonds, and international stocks over U.S. ones. Feature The yield curve has become the punch line of late-night shows, triggered by the 2-/10-year yield curve inversion in early August. Recession fears have hit the front page. There are good reasons for the mounting concern. Historically, yield curve inversions have done an excellent job forecasting recession. The trade war between the U.S. and China is intensifying at an alarming speed. Moreover, global government bond yields are dipping to all-time lows. Additionally, the global ZEW and PMIs are depressed, while the global production of capital goods and machinery is contracting (Chart I-1). Despite this backdrop, the odds of a U.S. recession are overstated. Consumers in the U.S. and other advanced economies are healthy, the U.S. Federal Reserve and other major central banks are easing, and global financial conditions are supporting growth. We expect stocks to break out of their volatile period of consolidation early next year. Bond yields should rise later this year, but it is too early to stand in front of their downward trend. Finally, long-term investors should use any additional narrowing in credit spreads to lighten their exposure to corporates. U.S. Recession Odds Are Low The yield curve signal is not as dire as the headlines suggest. The inversion is incomplete; the curve is inverted up to the five-year mark and beyond that point, it steepens again. If the yield curve foreshadows a recession, then its slope would be negative across all maturities (Chart I-2). Chart I-1The List Of Worries Is Long

The List Of Worries Is Long

The List Of Worries Is Long

Chart I-2

The consumer sector is doing well despite the global growth slowdown. Real retail sales, excluding motor vehicles, are growing at 4.4% and have quickly recovered from this past winter’s government shutdown. Meanwhile, retailers such as Walmart, Target, Home Depot and Lowe’s are reporting strong numbers. Three factors insulate consumer spending from global woes. First, household disposable income is expanding at a healthy 4.7% pace, courtesy of a tight labor market. Secondly, household balance sheets are robust. Household debt-servicing costs only represent 9.9% of disposable income, the lowest reading in more than four decades (Chart I-3, first panel). According to a December BIS paper, debt-servicing costs are one of the best forecasters of recessions.1 Additionally, household debt relative to GDP and to household assets is at 16- and 34-year lows, respectively (Chart I-3, second and third panel). Thirdly, the U.S. savings rate, which stands at 8.1%, already offers a cushion against adverse shocks and has limited upside. The corporate sector also displays some easily overlooked positives. So far, the PMIs and capex growth are still in mid-cycle slowdown territory. Meanwhile, debt loads have never provided an accurate recessionary signal. Since the end of the gold standard, recessions have always materialized after debt-servicing costs as a share of EBITDA rose two to four percentage points above their five-year moving average. We are nowhere near there (Chart I-4). Chart I-3Consumer Balance Sheets Are Very Robust

Consumer Balance Sheets Are Very Robust

Consumer Balance Sheets Are Very Robust

Chart I-4Corporate Debt Is Not In Recessionary Territory

Corporate Debt Is Not In Recessionary Territory

Corporate Debt Is Not In Recessionary Territory

Nevertheless, we will remain vigilant on the capex trend. Corporate investment may not indicate a recession, but the escalating trade war with China will hurt capex intentions. Even if capex contracts, as in 2016, the economy can still avoid a recession. The factors that prompted slowdowns in global trade and manufacturing provide a mixed message. Housing is showing some positive signs after subtracting from GDP in the past six quarters. The NAHB Housing Market Index is recovering smartly from its plunge last year and homebuilder stocks have been outperforming the S&P 500 since October 2018 (Chart I-5). Meanwhile, the 139-basis point collapse in mortgage rates since November 2018 is finally impacting the economy. Mortgage demand is surging, according to the Fed’s Senior Loan Officers Survey. The MBA mortgage applications data corroborate this observation. As a result, both existing home sales and residential investment are trying to bottom (Chart I-6). Chart I-5Leading Indicators Of Residential Activity Are Improving

Leading Indicators Of Residential Activity Are Improving

Leading Indicators Of Residential Activity Are Improving

Chart I-6Positive Signs For Residential Activity

Positive Signs For Residential Activity

Positive Signs For Residential Activity

The liquidity of the U.S. private sector is also strengthening. Deposit growth has reaccelerated after falling to near recessionary levels (Chart I-7) and the non-financial, private sector’s cash holdings are again increasing faster than debt. Furthermore, bank credit is expanding. Chart I-7The Private Sector Is Accumulating Liquidity

The Private Sector Is Accumulating Liquidity

The Private Sector Is Accumulating Liquidity

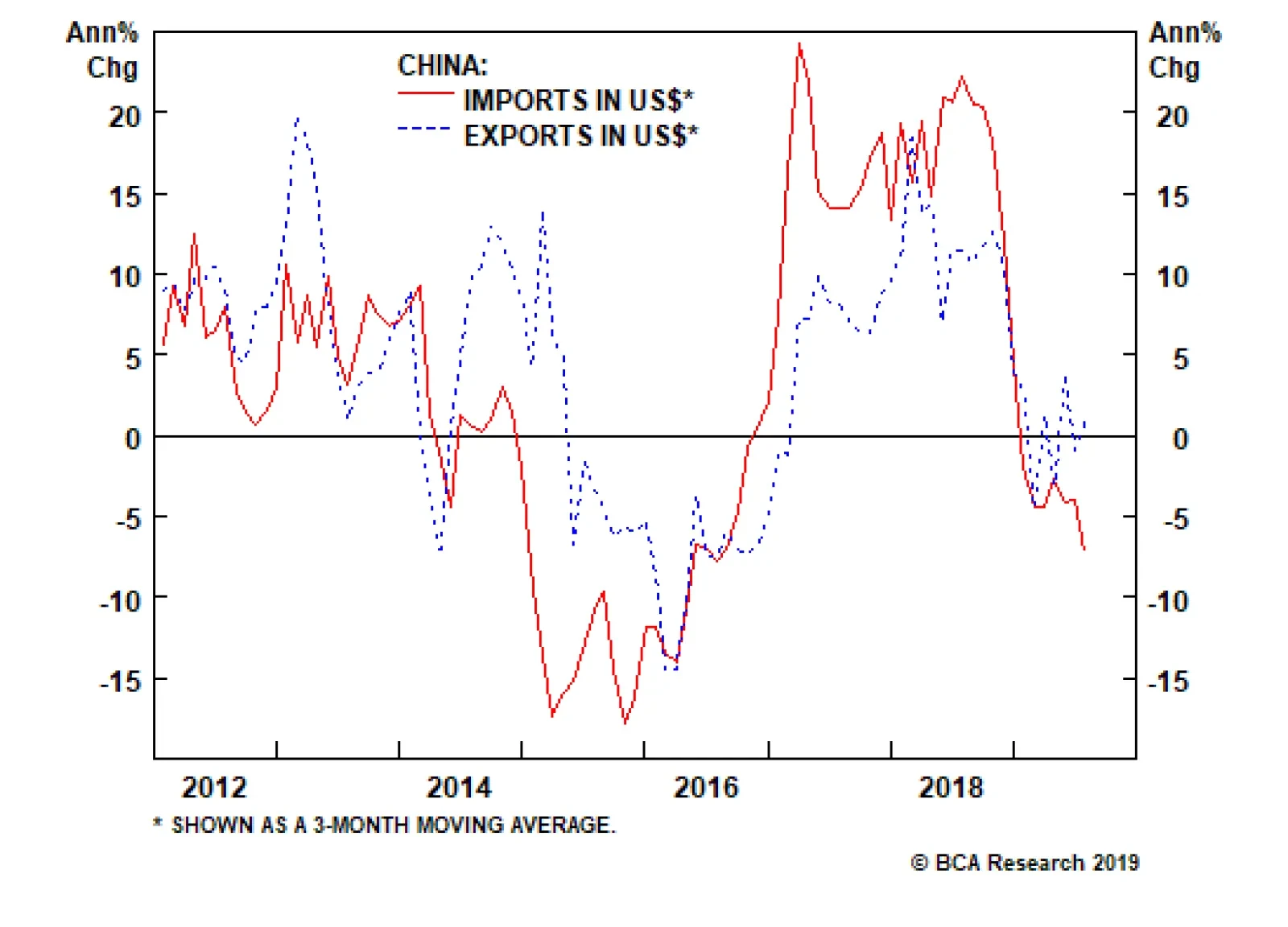

Waiting For The Global Economy To Bottom Global growth should bottom by early 2020. Thus, while the U.S. economy should avoid a recession, any distinct re-acceleration will wait until next year. The factors that prompted slowdowns in global trade and manufacturing provide a mixed message. The trade war between the U.S. and China is intensifying. Chinese activity has not yet bottomed but policymakers will be increasingly forced to react. However, the global inventory down cycle is advanced, and in Europe, domestic activity indicators are holding up despite the continued deterioration in external and industrial conditions. Trade War The uncertainty created by the Sino-U.S. trade war is hurting global growth. On August 1, U.S. President Donald Trump announced a 10% tariff on the remaining $300 billion of Chinese exports to the U.S. The tariffs are phased in: $112 billions of goods will be taxed on September 1 while $160 billion will be hit on December 15. Unsurprisingly, a vicious circle of retaliation has been unleashed as China imposed a tariff ranging from 5% to 10% on U.S. goods last Friday, to which Trump immediately responded with a tariff hike from 25% to 30% on the $250 billion batch of goods and from 10% to 15% on the $300 billion batch slated to come into place September 1 and December 1. To bring back hedged foreign buying of Treasurys, the Fed will have to engineer a steeper yield curve and lower FX hedging costs. A resumption in talks between Beijing and Washington in September will offer little solace to investors. Even if President Trump is pressured by the stock market and the U.S. electoral calendar to settle for what Beijing is offering, it is not clear that President Xi Jinping will accept a deal. As BCA’s Chief Geopolitical Strategist Matt Gertken discusses in Section II, the two superpowers are locked in a multi-decade geopolitical rivalry and the Hong Kong protests and tensions over Taiwan could move the talks off track. China’s Challenges China’s economy has yet to bottom convincingly. So far, Chinese reflation has been weaker than anticipated. Given that stimulus has not been forceful, the uncertainty produced by the trade war and the illiquidity created by bloated balance sheets is still dragging down China’s marginal propensity to consume (Chart I-8). However, this propensity to spend has little downside, if the past 10 years are any indication. Chinese infrastructure and equipment investment needs to be revived. They are shouldering the bulk of the decline in economic activity and have slowed to an annual pace of 2.8% and -2.1%, respectively. Residential investment is expanding at a 9.4% annual rate (Chart I-9), but according to Arthur Budaghyan, BCA’s Chief Emerging Markets Strategist, even this sector’s strength could be an illusion. Chinese property developers are starting projects to raise funds via pre-sales. However, they are not completing nearly as many projects as they have started.2 Chart I-8A Falling Marginal Propensity To Spend Means More Stimulus Is Needed

A Falling Marginal Propensity To Spend Means More Stimulus Is Needed

A Falling Marginal Propensity To Spend Means More Stimulus Is Needed

Chart I-9

We are not yet ready to give up on Chinese stimulus as the economy is on the verge of a deflationary spiral that could push debt-to-GDP abruptly higher. The following developments support this view: The statement following the July Politburo meeting showed a greater willingness to stimulate economic activity, as long as it does not add to the property bubble. Producer prices are again deflating. Contracting PPIs often unleash vicious circles as they push real rates higher and hurt investment, which foments additional price declines. Retail sales are slowing and the employment components of the manufacturing and non-manufacturing PMIs have fallen to 47.1 and 48.7, respectively. China’s economy needs to be insulated from the intensifying trade war with the U.S. or the deteriorating labor market will dampen consumer spending even more. We expect more tax cuts, more credit growth, and more issuance of local government special bonds to finance government spending, following China’s 70th anniversary celebrations on October 1. As Chart I-10 illustrates, an acceleration in total social financing will ultimately lift EM PMIs as well as Asian and European exports. Inventory Cycle The inventory cycle is very advanced. Inventories in the U.S., China and euro area are depleting (Chart I-11). Inventories cannot fall forever, especially when global monetary policy is increasingly accommodative and fiscal policy is loosened. Chart I-10More Chinese Stimulus Will Eventually Support Global Growth

More Chinese Stimulus Will Eventually Support Global Growth

More Chinese Stimulus Will Eventually Support Global Growth

Chart I-11The Inventory Purge Is Advanced

The Inventory Purge Is Advanced

The Inventory Purge Is Advanced

Global activity can rebound if the inventory adjustment ends. Inventory fluctuations help drive the Kitchin cycle, a 36-40 month oscillation in activity. According to BCA’s Chief Global Strategist, Peter Berezin, the current slowdown is nearing 18 months, the typical length of a down oscillation in these cycles (Chart I-12).3 Europe The manufacturing-heavy euro area will benefit when the global industrial cycle bottoms, but domestic tailwinds are also emerging. European deposits accumulation is quickening, driven by households (Chart I-13, top panel). Meanwhile, the European credit impulse has recovered thanks to the fall in both non-performing loans and borrowing costs (Chart I-13, bottom panel). Moreover, consumer spending is healthy as household balance sheets are improving and wage growth is accelerating to a 3.2% annual pace. Finally, last month we highlighted that the euro area fiscal thrust is set to increase by 0.7% of GDP this year.4 Fiscal easing appears set to expand as Germany and Italy study support packages. Finally, the Italian political uncertainty is receding as the Five Star Movement and the Democratic Party have agreed to form a coalition government. Chart I-12The Three-Year Cycle Is Also Advanced

The Three-Year Cycle Is Also Advanced

The Three-Year Cycle Is Also Advanced

Chart I-13Some Ignored Improvements In Europe

Some Ignored Improvements In Europe

Some Ignored Improvements In Europe

At the moment, the biggest risk for Europe is the significant probability of a No-Deal Brexit. After the recent decision to prorogue Parliament, Matt Gertken raised his probability of a No-Deal Brexit to one third from 20%.Such an event would negatively impact Dutch, German and French exports, which could scuttle any improvement in Europe. Adding It Up The combined effects of more Chinese stimulus in the fourth quarter, an impending end to the global inventory drawdown, and an endogenous improvement in Europe, all should ultimately outweigh the negatives created by the U.S.-Sino trade war. Moreover, global financial conditions are easing (Chart I-14). Therefore, the fall in global bond yields should push the G-10 12-month credit impulse higher (Chart I-14, bottom panel). Lower oil prices should also help G-10 consumers. Early indicators support this assessment. BCA’s Global Leading Economic Indicator has been slowly bottoming, and according to its diffusion index, it will soon move higher (Chart I-15, top panel). Moreover, Singapore’s container throughput is tentatively stabilizing, while our Asian EM Diffusion Index is improving, albeit from depressed levels (Chart I-15, second panel). Finally, ethylene and propylene prices are rallying with accelerating momentum (Chart I-15, third and fourth panels). Chart I-14Easier Financial Conditions Favor Credit Growth

Easier Financial Conditions Favor Credit Growth

Easier Financial Conditions Favor Credit Growth

Chart I-15Some Growth Indicators Are Stabilizing

Some Growth Indicators Are Stabilizing

Some Growth Indicators Are Stabilizing

Bottom Line: The U.S. economy will probably slow further in the coming months, but it will not enter into recession anytime soon. Neither debt nor consumers pose problems, the housing sector is turning the corner and the private sector’s liquidity position is strengthening. Meanwhile, global activity is trying to bottom, but any improvement will be delayed by the latest round of trade tensions. However, global policymakers are responding, thus global growth should improve by early 2020. Fed Policy: More Cuts Expected Chart I-16A Liquidity Crunch In The Interbank Market?

A Liquidity Crunch In The Interbank Market?

A Liquidity Crunch In The Interbank Market?

Our base case is that the Fed will cut rates twice more in the coming nine months. In the tails of the probability distribution, three supplementary cuts are more likely than only one additional cut. Paradoxically, liquidity considerations support our Fed view. A recurring theme in our research is the improvement in global liquidity indicators such as excess money, deposit growth and our financial liquidity index.5 However, these indicators are not able to boost growth because of an important technical consideration. What might be classified as excess reserves by the Fed may not be free reserves. Higher Supplementary Leverage Ratios under Basel III rules require commercial banks to hold greater levels of excess reserves to meet their mandatory Tier 1 capital ratios. Since the Fed’s balance sheet runoff results in falling excess reserves, the decline in reserves may have already created some illiquidity in the interbank system. Global central banks have been divesting from the T-bill market, which is worsening the decline in excess reserves. They have parked their short-term funds at the New York Fed’s Foreign Repurchase Agreement Pool (Foreign Repo Pool) which limits the availability of reserves in the banking system (Chart I-16).6 These dynamics increase the cost of hedging the dollar for foreign buyers of U.S. assets. When reserves fall below thresholds implied by Basel III regulations, global banks lose their ability to use their balance sheets to conduct capital market transactions. Without this necessary wiggle room, they cannot arbitrage away wider cross-currency basis swap spreads and deviations of FX forward prices from covered interest rate parity. For foreign investors, the cost of hedging their FX exposure increases. Together with the flatness of the U.S. yield curve, hedged U.S. Treasurys currently yield less than German Bunds or JGBs (Table I-1).

Chart I-

Chart I-17Declining Excess Reserves Hurt Risk Assets And Growth

Declining Excess Reserves Hurt Risk Assets And Growth

Declining Excess Reserves Hurt Risk Assets And Growth

Lower excess reserves and higher hedging costs have been bullish for the USD and negative for the global economy. Instead of buying hedged Treasurys, foreigners purchase U.S. assets unhedged (agency and corporate bonds, not Treasurys). Thus, falling excess reserves have been correlated with a stronger dollar, softer global growth and weaker EM asset and FX prices (Chart I-17). This adverse environment has accentuated the downside in Treasury yields and flattened the yield curve (Chart I-17, bottom panel). Going forward, these problems should intensify. The Treasury will issue over US$800 billion of debt by year-end to replenish its cash balance and finance the bulging U.S. budget deficit. Primary dealers will continue to plug the void left by foreigners and will purchase the expanding issuance (Chart I-18). In the past year, primary dealers have already increased their repo-market borrowing by $300 billion to finance their inventories of securities. They will need to expand these borrowings, which will further lift the cost of hedging U.S. assets. Thus, foreign investors faced with $16 trillion of assets with negative yields will buy more U.S. assets on an unhedged basis. The dollar will rise and global growth conditions will deteriorate. The Fed will have to cut rates two to three more times, otherwise the dangerous feedback loop described above will take hold. These cuts are more than domestic economic conditions warrant. To bring back hedged foreign buying of Treasurys, the Fed will have to engineer a steeper yield curve and lower FX hedging costs. The end of the balance sheet runoff is a step in the right direction, but it will not be enough. The BCA Financial Stress Index and our Fed Monitor are consistent with this view (Chart I-19). Moreover, the intensifying trade war is hurting the outlook for growth, inflation expectations and the stock market. Chart I-18A Large Inventory Build Up By Primary Dealers

A Large Inventory Build Up By Primary Dealers

A Large Inventory Build Up By Primary Dealers

Chart I-19Two To Three More Cuts Are Coming

Two To Three More Cuts Are Coming

Two To Three More Cuts Are Coming

Investment Implications Government Bonds We have revised our position on an imminent end to the bull market. We do expect bond yields to be higher in 12 months, but for now the global economy has too many risks to time a bottom in yields. The cyclical picture for bonds is bearish. Treasurys have outperformed cash by 8% in the past year, a performance normally associated with a fed fund rate that is 200 to 300 basis points below what markets anticipated 12 months ago (Chart I-20). In order for Treasurys to continue outperforming cash, the Fed must cut rates to zero next year. Nonetheless, a U.S. recession is not in the offing and the global economy should perk up by early 2020. At most, the Fed will validate current rate expectations of 96 basis points of cuts. Chart I-20The Fed Must Cut To Zero For Bonds To Further Outperform Cash Next Year

The Fed Must Cut To Zero For Bonds To Further Outperform Cash Next Year

The Fed Must Cut To Zero For Bonds To Further Outperform Cash Next Year

Valuations are also consistent with Treasurys delivering negative returns in the next 12 months. According to the BCA Bond Valuation Index, Treasurys are extremely overvalued. Moreover, real 10-year yields are two standard deviations below the three-year moving average of real GDP growth, a proxy for potential GDP (Chart I-21). Investors should wait to sell bonds until the Fed cuts rates by another 50 basis points, global and U.S. PMIs stabilize, and our cyclical indicator sends a sell signal. Technicals also point to poor 12-month prospective returns. The 13-week and 52-week rates of change in yields are consistent with tops in bond prices (Chart I-22). Positioning is also very stretched, as highlighted by the J.P. Morgan Duration Survey, the Bank of America Merrill Lynch Investors Survey, ETF flows, and government bonds futures and options holdings of asset managers. As a result, our Composite Technical Indicator is very overbought (Chart I-22, bottom panel). Chart I-21U.S. Bonds Are Very Expensive ...

U.S. Bonds Are Very Expensive ...

U.S. Bonds Are Very Expensive ...

Chart I-22... And Very Overbought

... And Very Overbought

... And Very Overbought

The quickening pace of accumulation of securities on bank balance sheets also points to higher yields in 12 months (Chart I-23). As banks stockpile liquid assets, they accumulate more juice to fuel future lending. However, the rising cost of hedging FX exposure is bullish for the dollar. Hence, increasing Treasury holdings will not lift yields until the Fed cuts rates more aggressively. We are reluctant to recommend shorting / underweighting bonds. As Chart I-24 illustrates, mounting uncertainty over economic policy anchors U.S. yields. Last week’s round of tariff increases, along with the Brexit saga, suggests that the uncertainty has not yet peaked. Chart I-23A Coiled Spring

A Coiled Spring

A Coiled Spring

Chart I-24Uncertainty Is Keeping Global Bonds Expensive

Uncertainty Is Keeping Global Bonds Expensive

Uncertainty Is Keeping Global Bonds Expensive

The collapse in German yields is also not finished. The fall in bund yields to -0.7% has dragged down rates worldwide as investors seek positive long-term returns. In response, the U.S. 10-year premium dropped to -1.1%. Historically, bunds end their rally when yields decline 120 basis points below their two-year moving average (Chart I-25). If history is a guide, German yields could bottom toward -1%, which is in line with Swiss 10-year yields. The 1995 experience also argues against an imminent end to the bond rally. In a recent Special Report, BCA’s U.S. Equity Strategy service highlighted the parallels between today’s environment and the aftermath of the December 1994 Tequila Crisis.7 In that episode, global growth troughed and the Fed cut rates three times before the U.S. ISM Manufacturing Index bottomed in January 1996. Only then did Treasury yields turn higher (Chart I-26). A similar scenario could easily unfold. Chart I-25More Downside For German Yields

More Downside For German Yields

More Downside For German Yields

Chart I-26Bottom In Yields: Wait For The ISM To Turn And The Fed To Cut More

Bottom In Yields: Wait For The ISM To Turn And The Fed To Cut More

Bottom In Yields: Wait For The ISM To Turn And The Fed To Cut More