Fixed Income

The Eurozone’s inflation will continue to slow over the coming months. While this trend will help Bund prices, will it boost the appeal of European equities?

We consider several uncertainties in this week’s report, from the interest rate outlook to the source of the mountain of cash households have amassed since the pandemic began. We have not adjusted our tactical asset-allocation recommendations but will do so soon to align with the defensive cast of our cyclical recommendations.

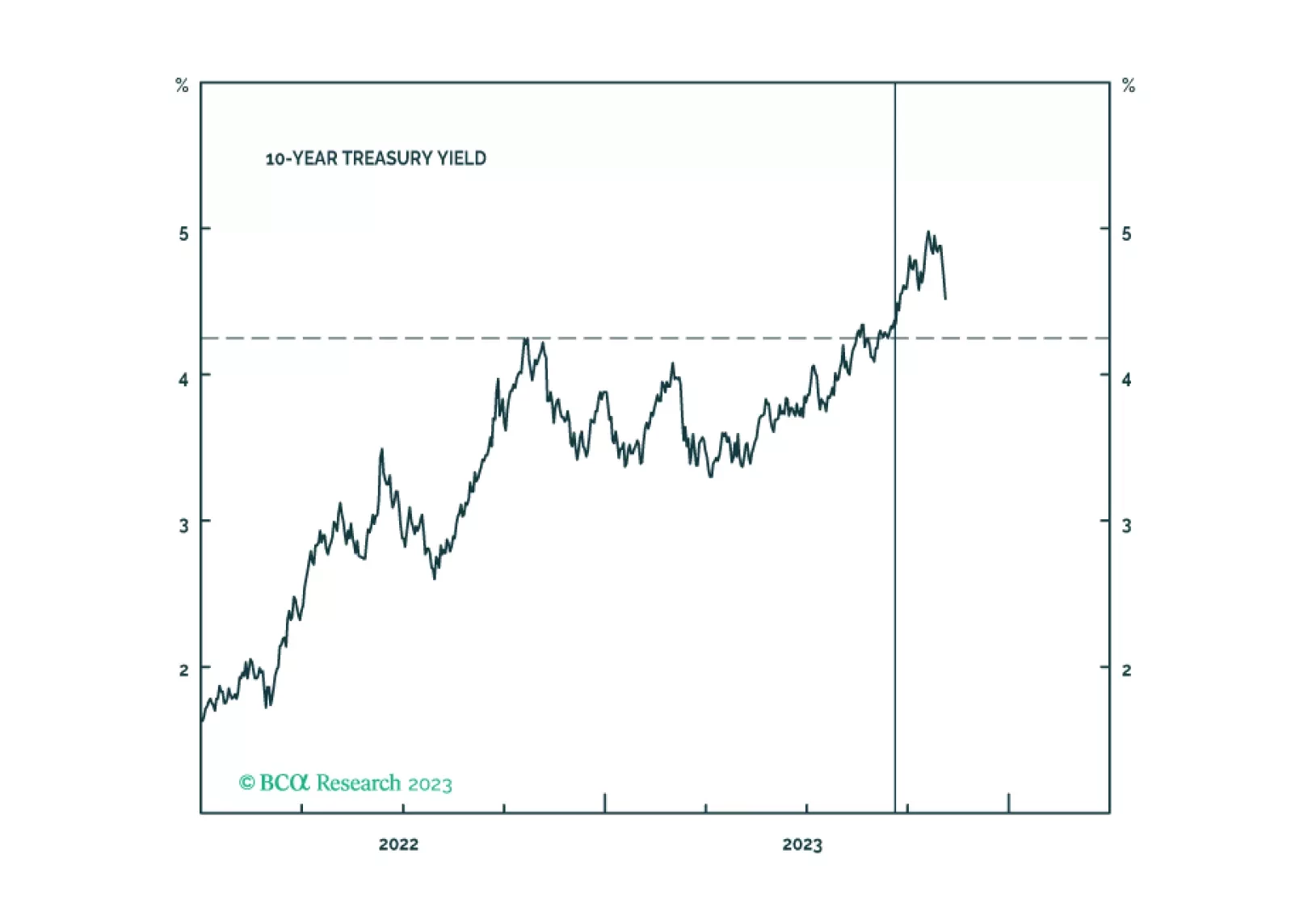

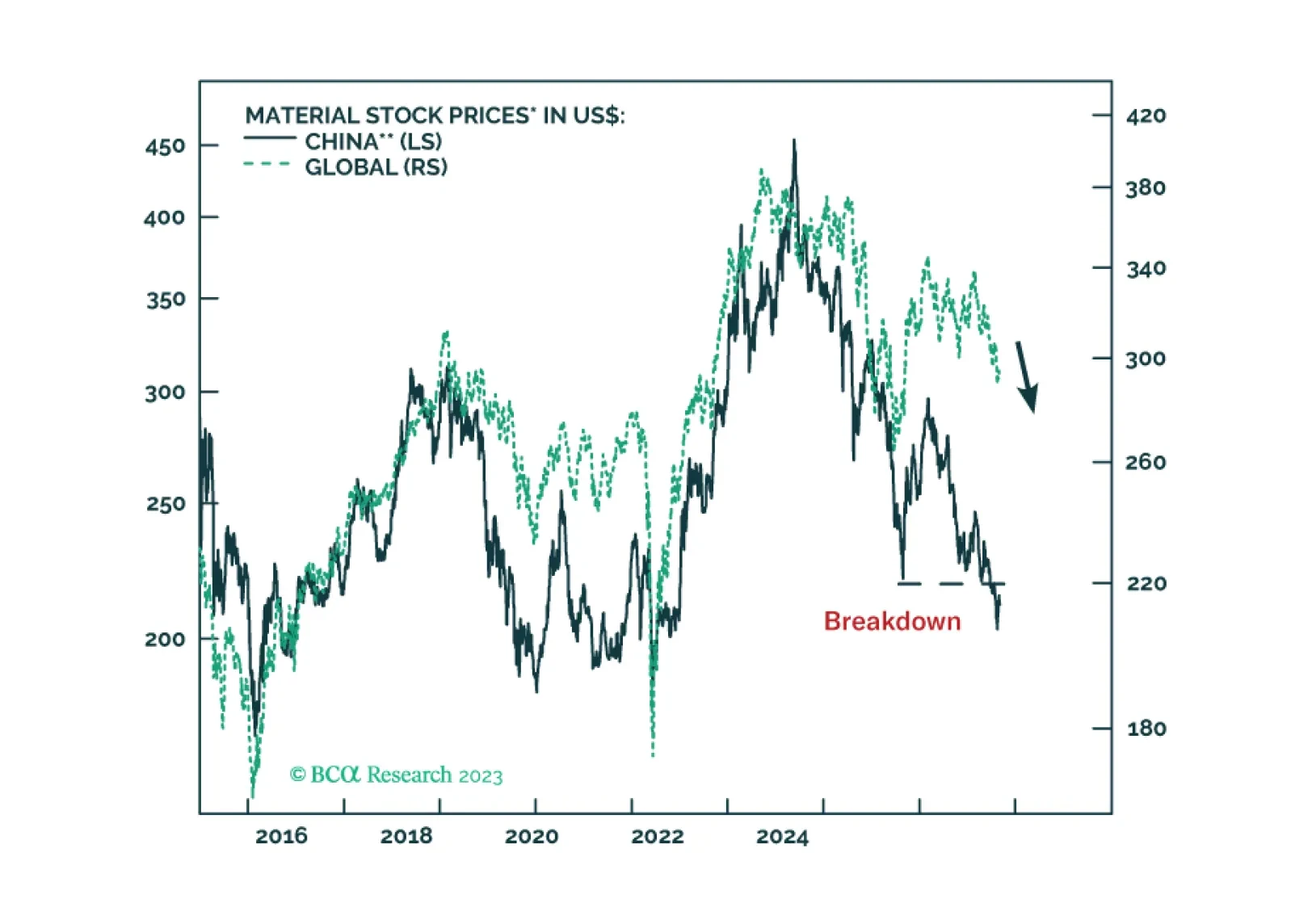

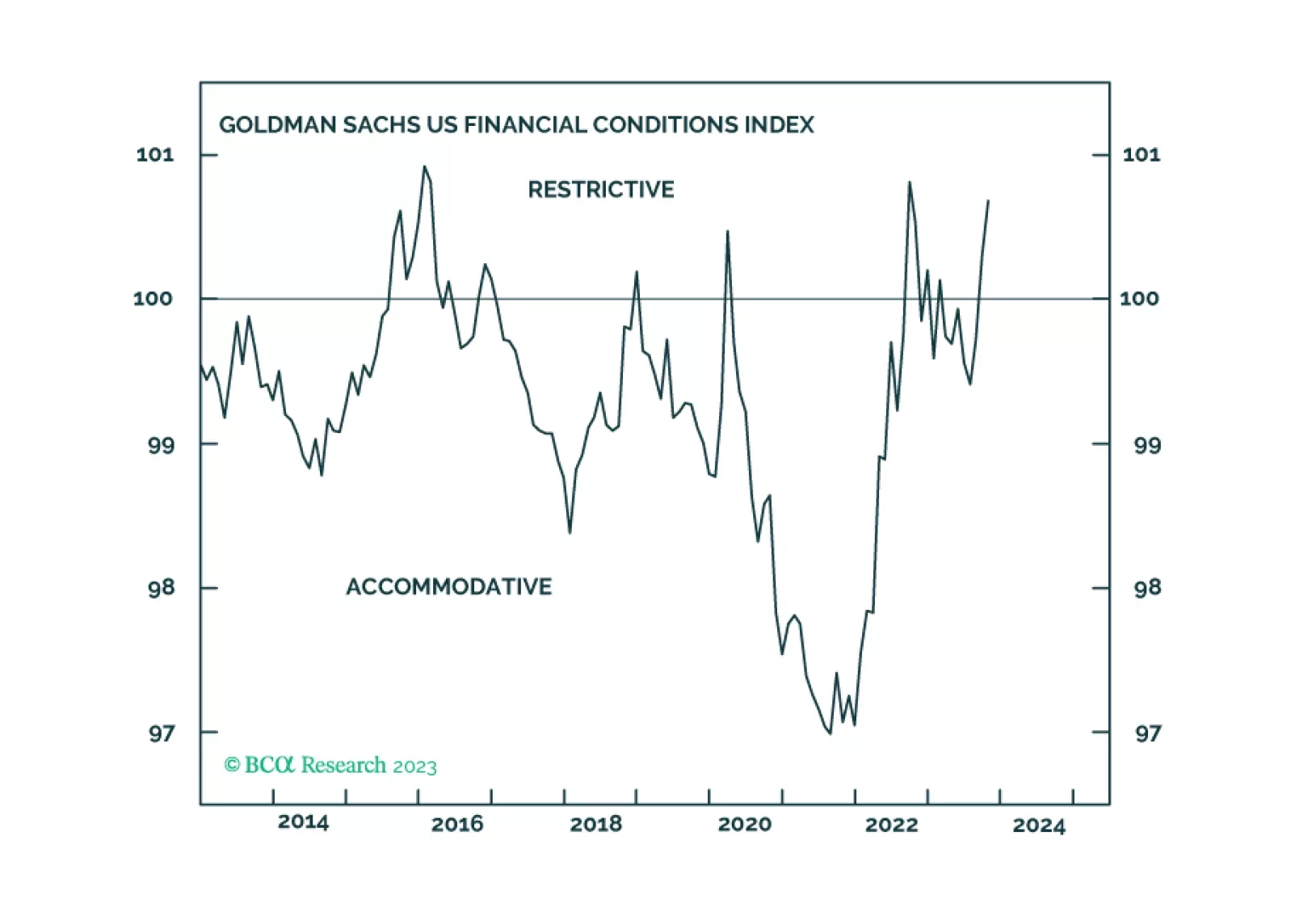

In financial systems, cracks typically begin on the periphery and then expand to the center. Hence, the ruptures on the fringes often act as an early warning. These fissures tend to widen and spread to the core, causing a breakdown in the S&P 500. Investors should consider buying US Treasurys aggressively when the S&P 500 slips below 4,000.

Our reaction to today’s FOMC meeting and the Treasury’s Quarterly Refunding Announcement.

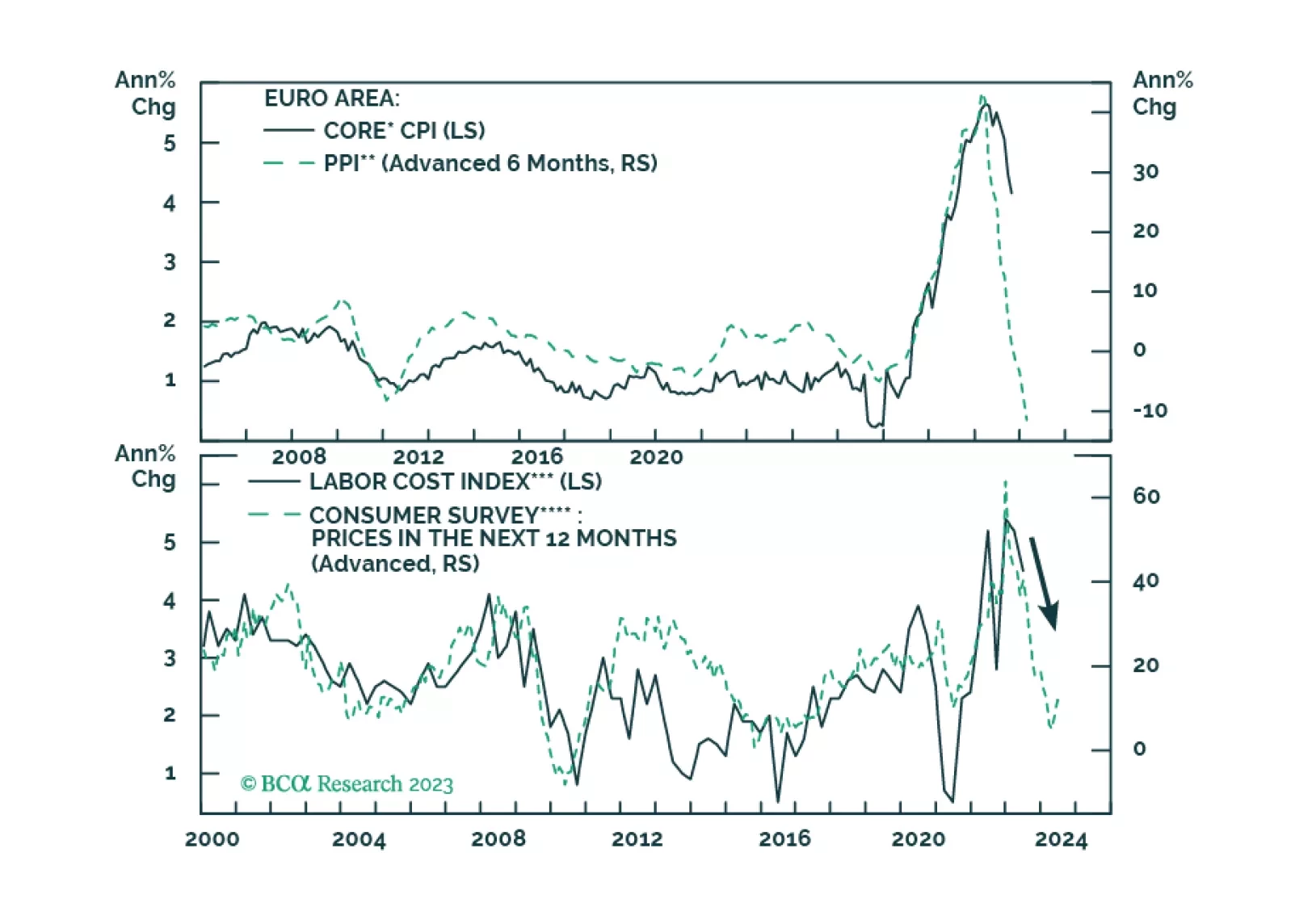

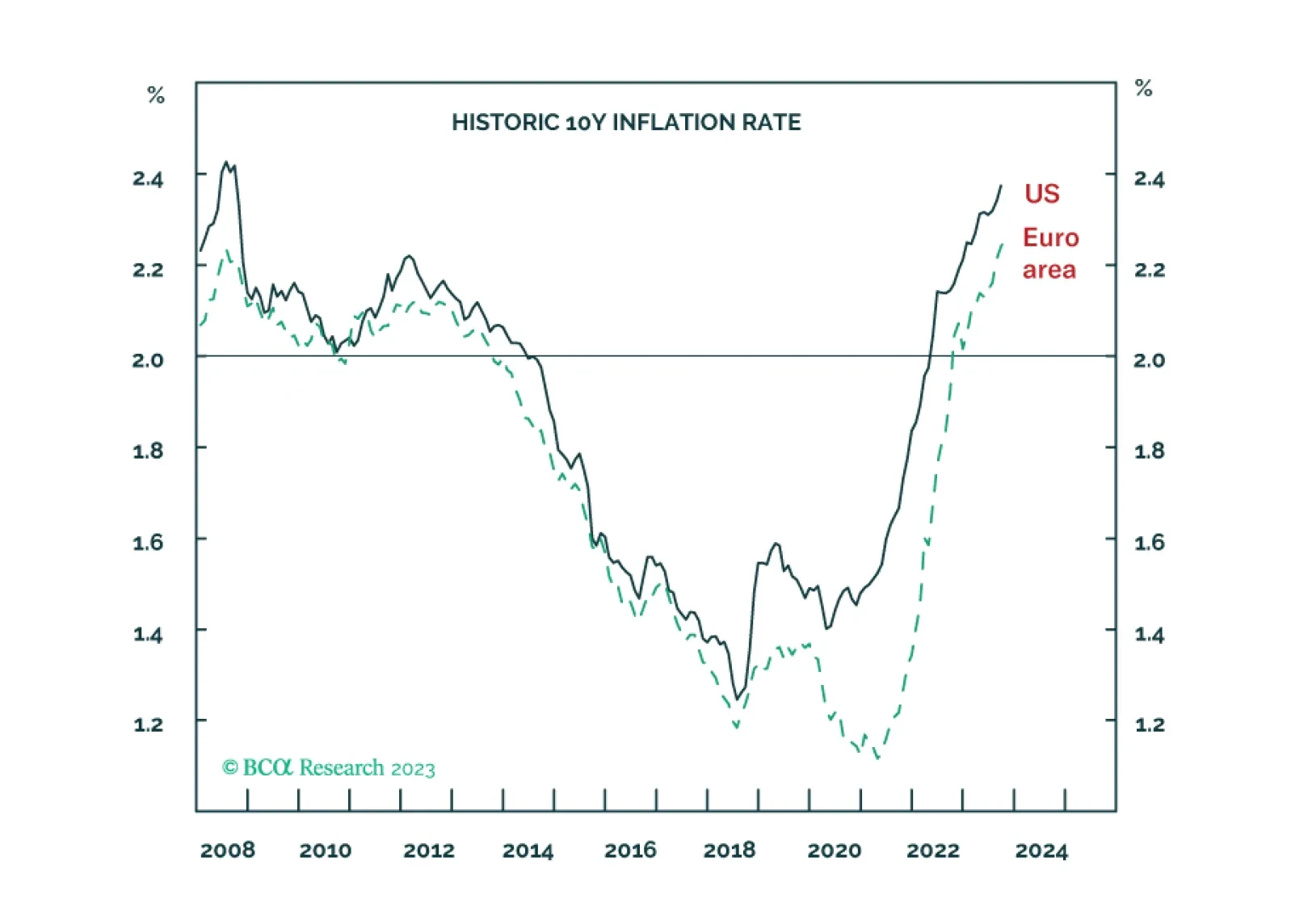

The fundamental component of long-term inflation expectations has climbed to its highest level since 2008 in both the US and the euro area. This means that both the Fed and the ECB will need to engineer inflation to undershoot 2 percent for an extended period if they are to maintain their 2 percent inflation targets. We explain what this means for investment strategy over the coming 6-12 months. Plus, we pinpoint what to focus on in this Friday’s US jobs report. And we identify food and beverages (PBJ) and the Indonesian rupiah (IDR/USD) as excellent rebound candidates.