Fixed Income

In Section I, we review the three possible economic scenarios over the coming year, and underscore that the “soft landing” scenario remains improbable. A “no landing” scenario could occur, but it would ultimately lead back to the recessionary path and thus is not a basis for investors to maintain pro-risk portfolio positions. US stock prices continue to be buoyed by rate cut expectations, but nonrecessionary cuts still appear to be a long way off. In Section II, we present our best estimate of the inflationary threshold that results in a positive or negative stock price / bond yield (SBY) correlation, and whether investors are likely to approach this level over the coming one-to-two years. US core inflation does not likely need to return to the Fed’s target in order for the SBY correlation to return to positive territory, but a move back to a positive correlation will very likely occur in the context of falling equity prices.

The debt ceiling game’s endpoint will avoid default only if it implies economic pain. For the Republicans, the best strategy is not to lift the debt ceiling unless the Democrats cut spending a lot, or unless the economy starts to tank. Plus: there are signs that the mania in ‘AI’ stocks has gone too far too fast.

China’s recovery is losing steam. Its industrial segments will disappoint, while the pace of consumer spending will be moderate. Overall, the Chinese economic recovery will underwhelm in the months ahead. Odds are that interest rate expectations in China will drop even lower, which will weigh on the RMB.

Investors should expect high volatility and a selloff in US stocks over the short run due to the higher-than-usual risk of technical default. Investors should seek shelter in defensive sectors and large cap stocks. Long-dated Treasuries will see yields fall due to the overall macro and geopolitical context even though short-dated Treasuries will continue to suffer from policy uncertainty.

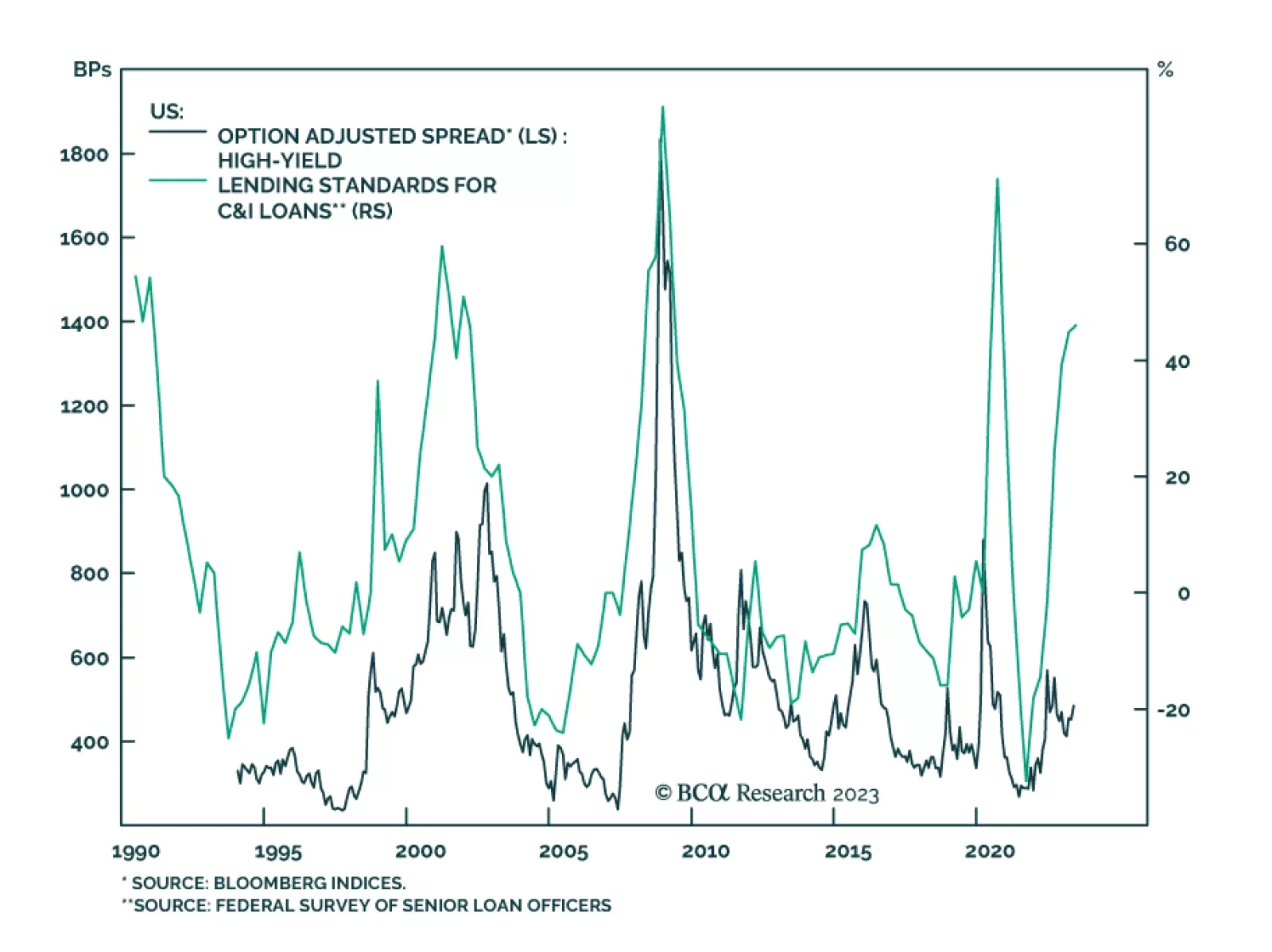

In this US Bond Strategy Insight we discuss the outlook for bank bonds.