Financial Markets

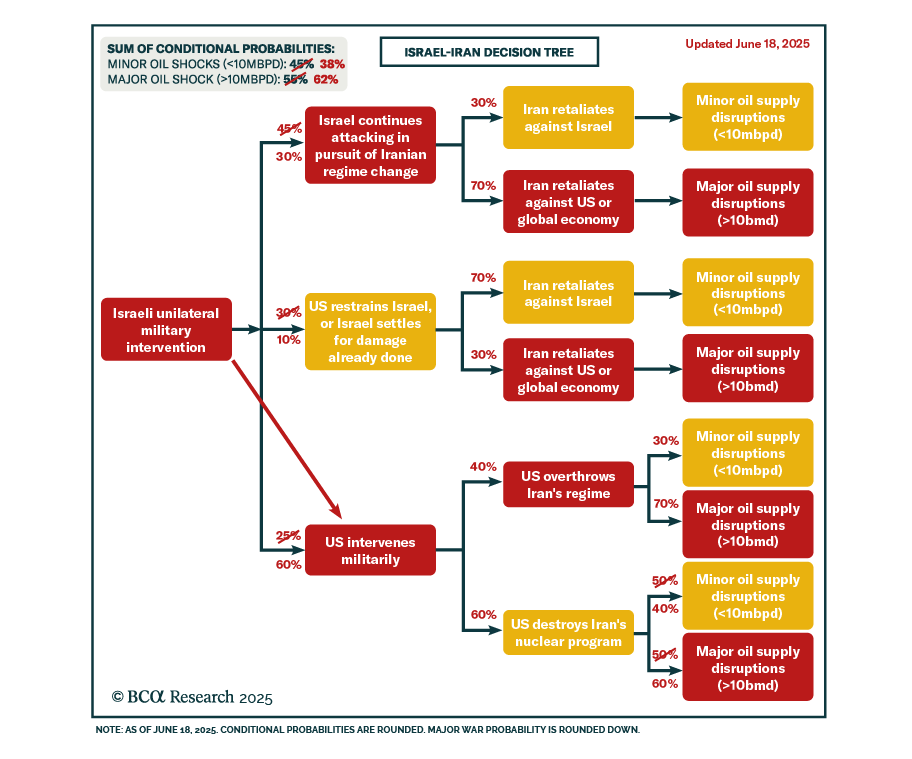

Geopolitical risks and fragile margins reinforce a defensive allocation stance, as oil shocks and high US equity valuations pose growing downside risks. At this month’s Views Meeting, our strategists discussed the potential fallout from an Iran-Israel…

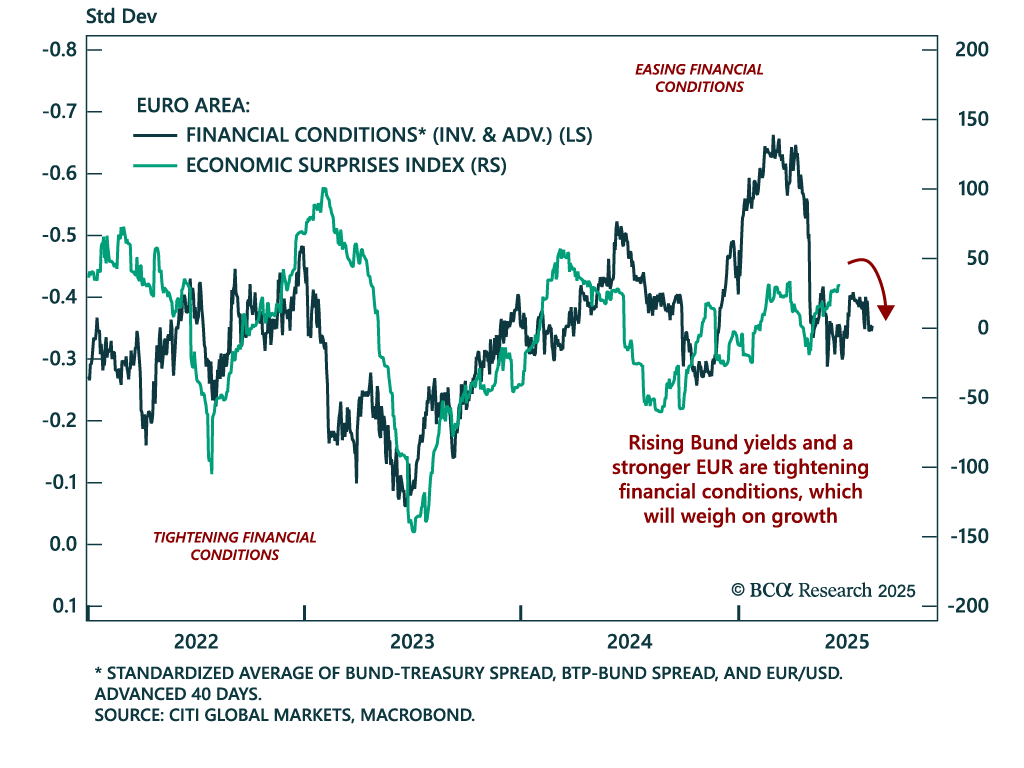

Tightening financial conditions, deflationary headwinds, and rising geopolitical risks argue for short-term caution on European assets. European equities have outperformed in 2025, with the EURO STOXX 50 beating the S&P 500 and EUR/USD moving higher. This…

Our Geopolitical strategists expect US involvement in Israel’s military campaign against Iran, raising near-term risks to oil supply and market stability. Iran is likely to retaliate by targeting regional oil production and transport infrastructure,…

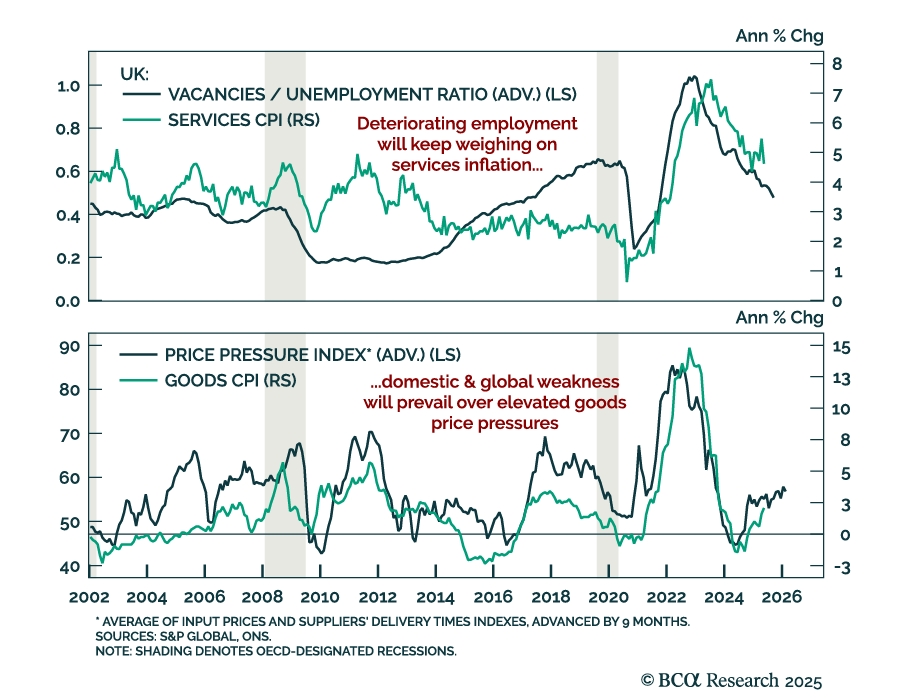

UK disinflation and labor market softening support our overweight in Gilts and short GBP trade. UK CPI came in slightly hotter than expected in May, with headline inflation at 3.4% y/y (vs. 3.5% in April) and core CPI meeting expectations at 3.5%, down from…

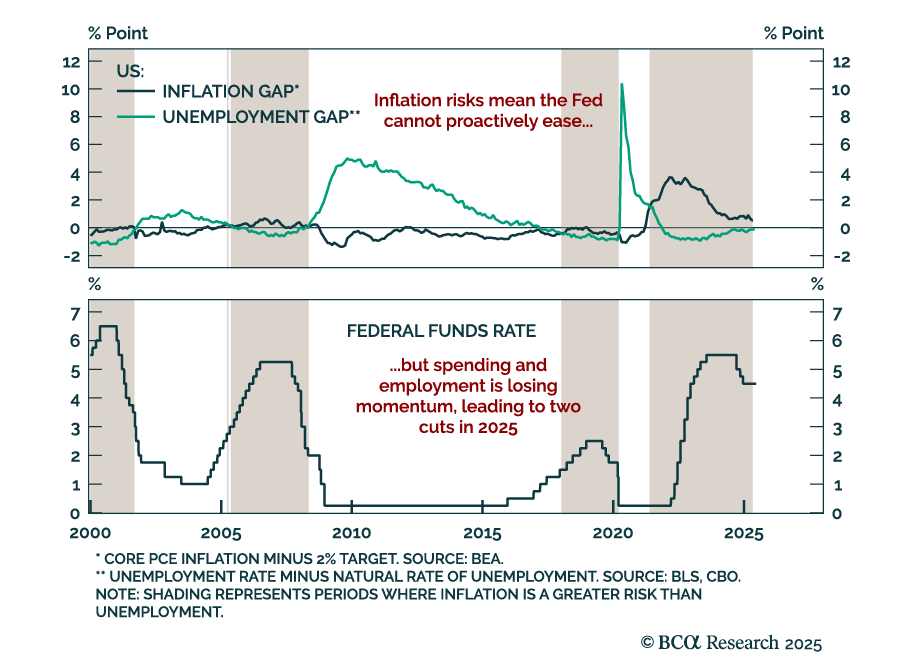

The Fed held rates steady between 4.25% to 4.5% and maintained a hawkish tilt despite soft data, reinforcing our long-duration and steepener trades. The updated dot plot showed upward revisions to both inflation and unemployment projections, as well as to…

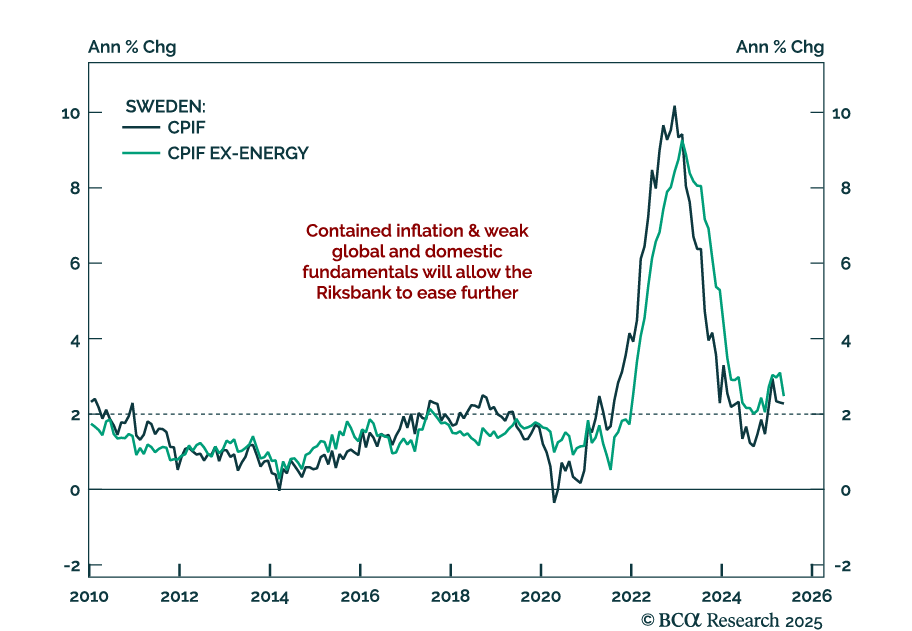

Sweden’s economic fragility and disinflation support further easing, reinforcing our long SEK rates and NOK/SEK trades. The Riksbank cut rates by 25 bps to 2.0% and projected an additional cut, consistent with prior OIS pricing. Forecasts for both headline…

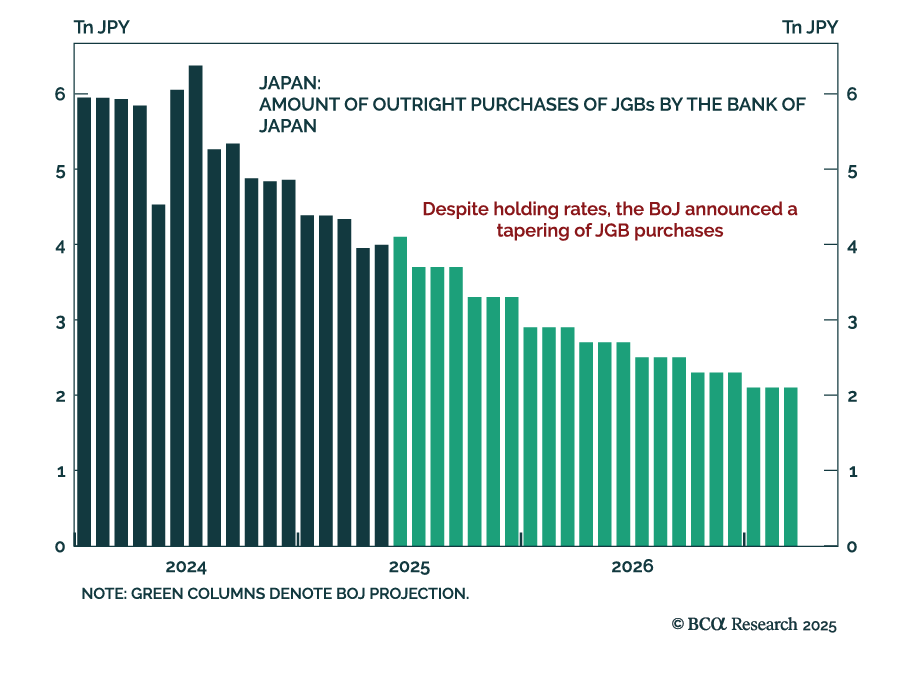

The BoJ’s decision to keep rates unchanged while announcing a tapering of bond purchases reinforces our underweight stance on JGBs and long bias on the yen. While the decision was broadly neutral, the reduction in asset purchases adds a hawkish undertone,…

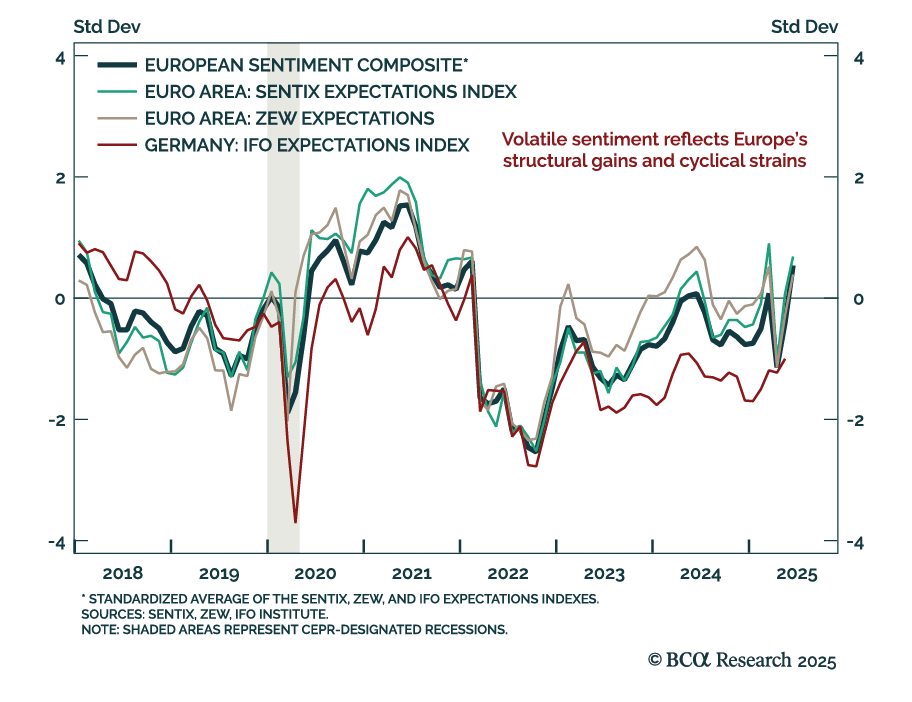

ZEW expectations jumped in May, but underlying macro fragility supports a cautious stance on eurozone assets. The ZEW expectations index for the euro area rose to 35.3 from 11.6, with Germany also beating expectations. The current situation component improved…

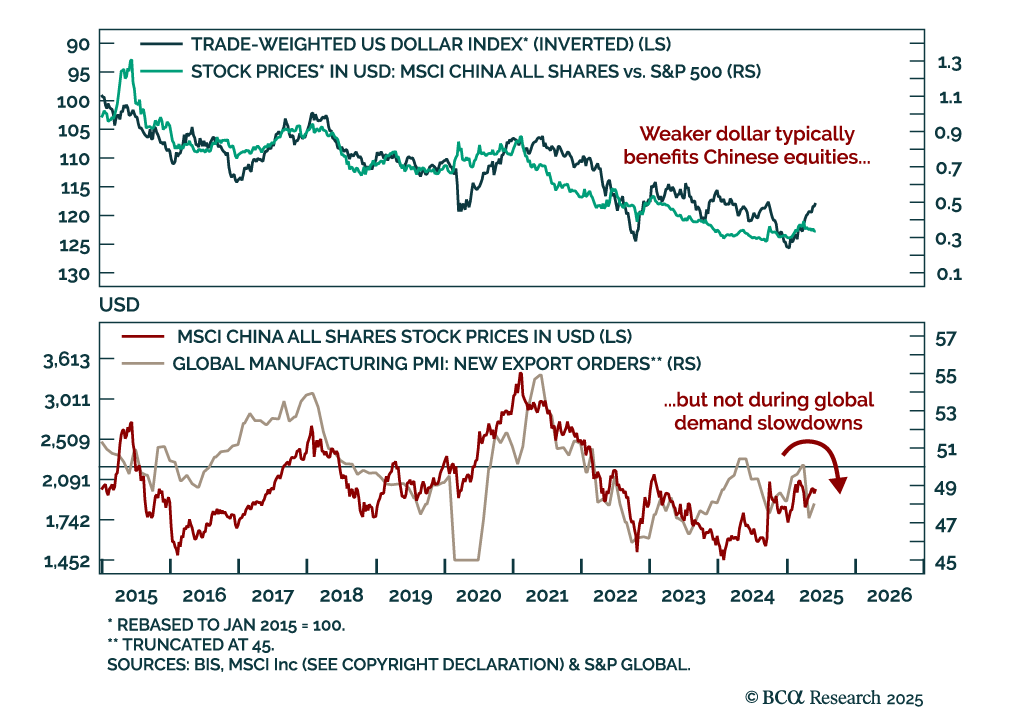

BCA’s China Investment strategists see limited upside for Chinese equities and favor bonds, as trade tensions ease but domestic headwinds persist. This week’s US-China trade talks in London lowered the risk of near-term escalation or new retaliatory tariffs,…

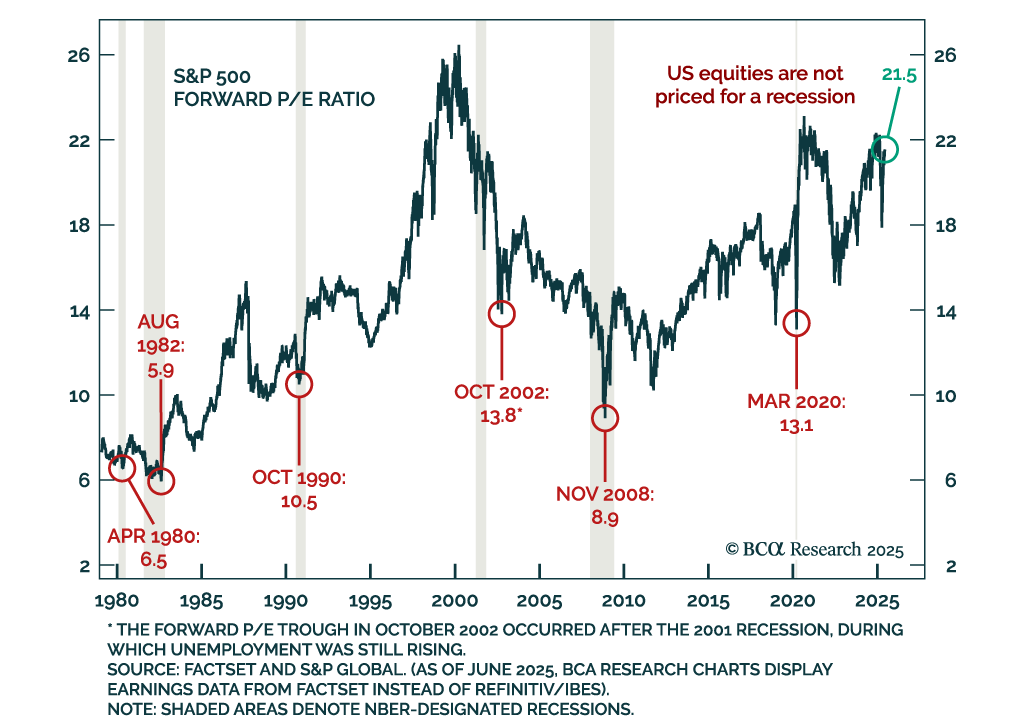

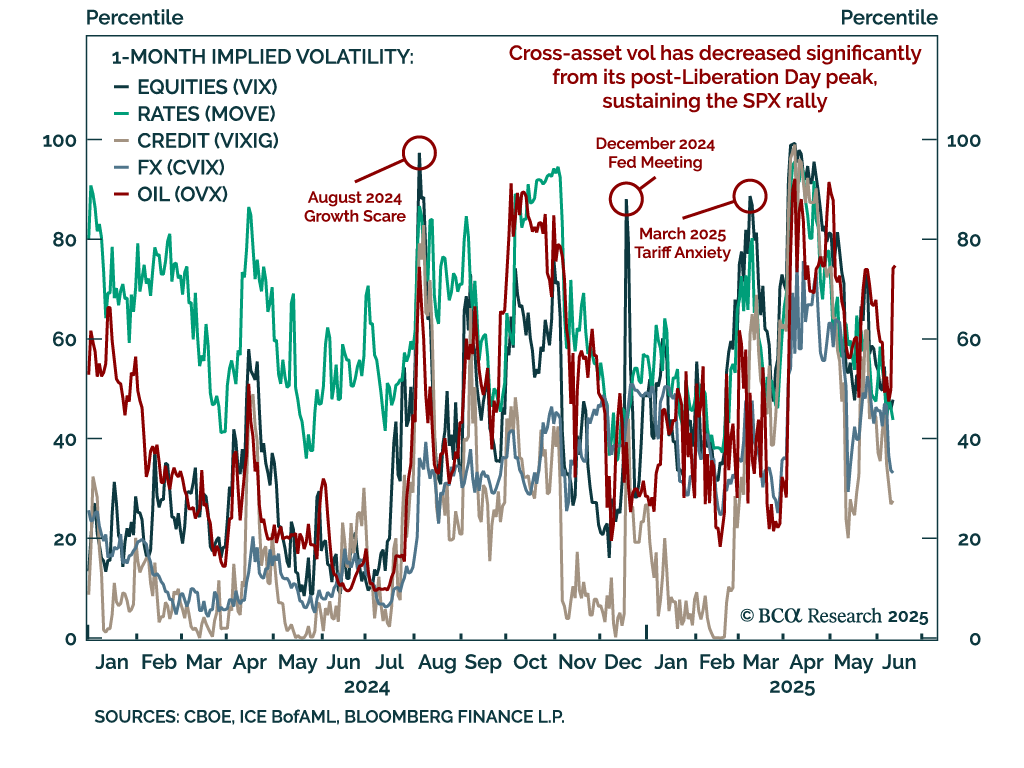

The S&P 500 has breached 6000 and may retest all-time highs, but we would not recommend chasing the rally. Risk assets have shrugged off recession fears, with stress indicators like the VIX, SKEW, and VVIX still subdued, signaling limited demand for…