Equities

Does the incipient slowdown in European data herald a soft landing and a goldilocks period for equities? We have our doubts.

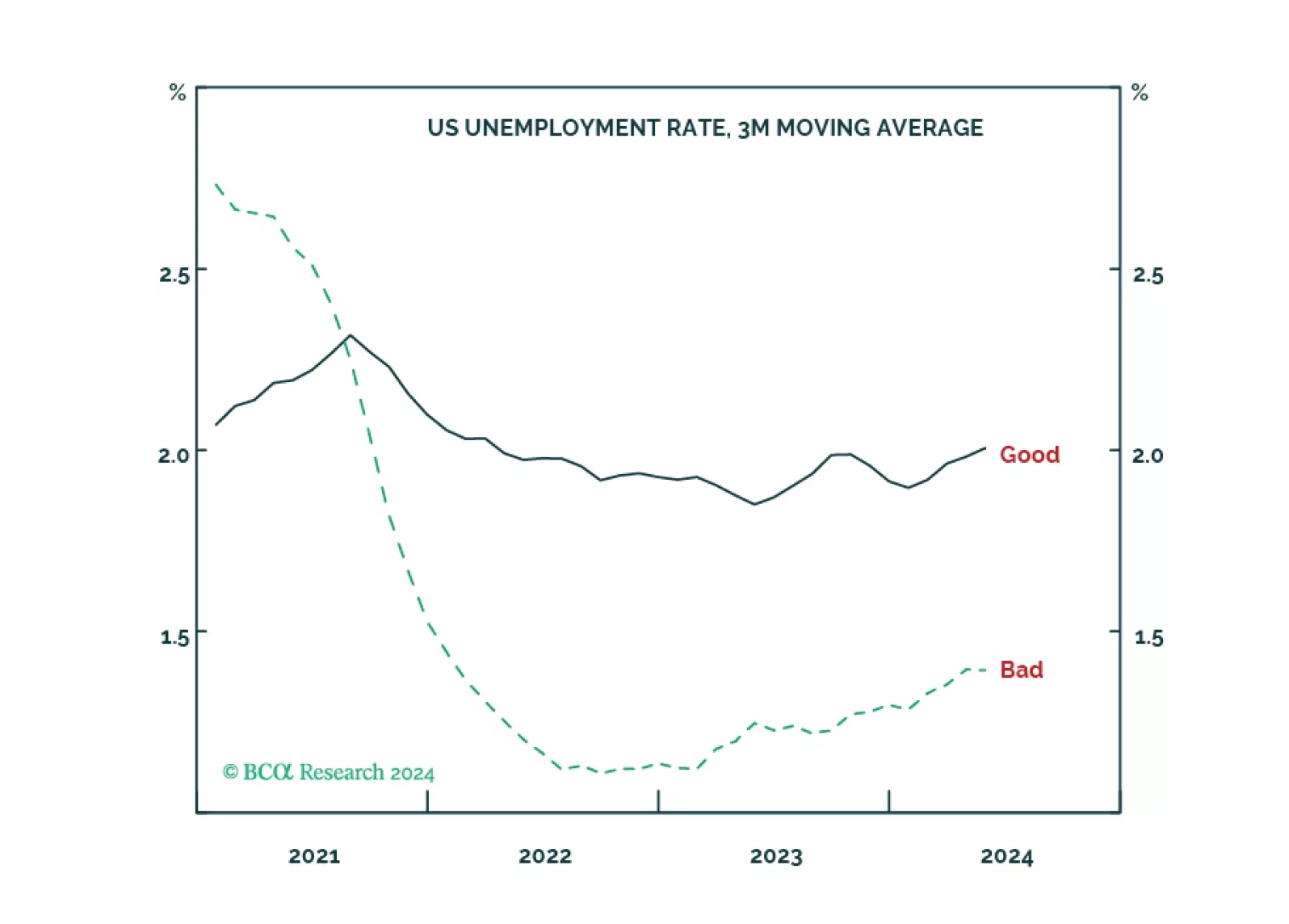

We explain how to distinguish between ‘good’, ‘bad’ and ‘ugly’ unemployment, why bad unemployment is a much better gauge of the jobs market than headline unemployment, and what this means for the tactical positioning in bonds and stocks. Plus: base metals (XBM) have already sold off sharply, so take profits in the short position and open a tactical overweight in global materials (MXI).

Concerns about the global economy have shifted from sticky inflation to faltering growth. Tight monetary policy is finally starting to bite. We suggest increasing portfolio defensiveness.

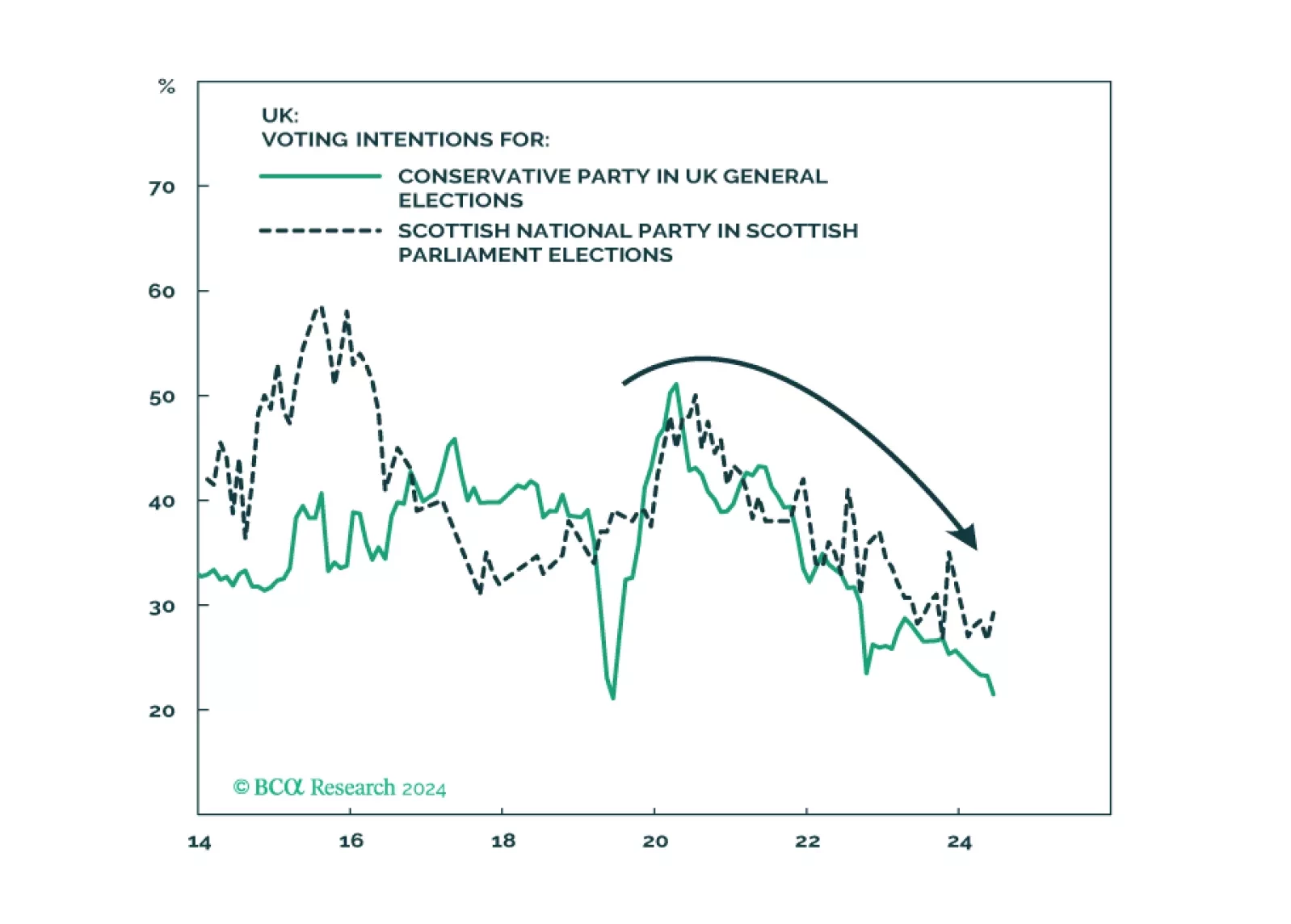

The Labour Party’s comeback in the UK is widely expected and will lead to fiscal stimulus consisting of increased public spending with minimal tax hikes. But a sweeping single-party majority will reduce social unrest only at the cost of higher taxes over the medium term. The paradigm has shifted away from the Thatcherite low-tax regime of the now-discredited Tories. v