Equities

Expectations for oil demand growth through 2023-24 are way too optimistic. Until these expectations fall to -0.5-1 percent, the oil price has further downside. Plus: collapsed complexity confirms that AI is in a mania, while basic materials stocks and ZAR/EUR are rebound candidates.

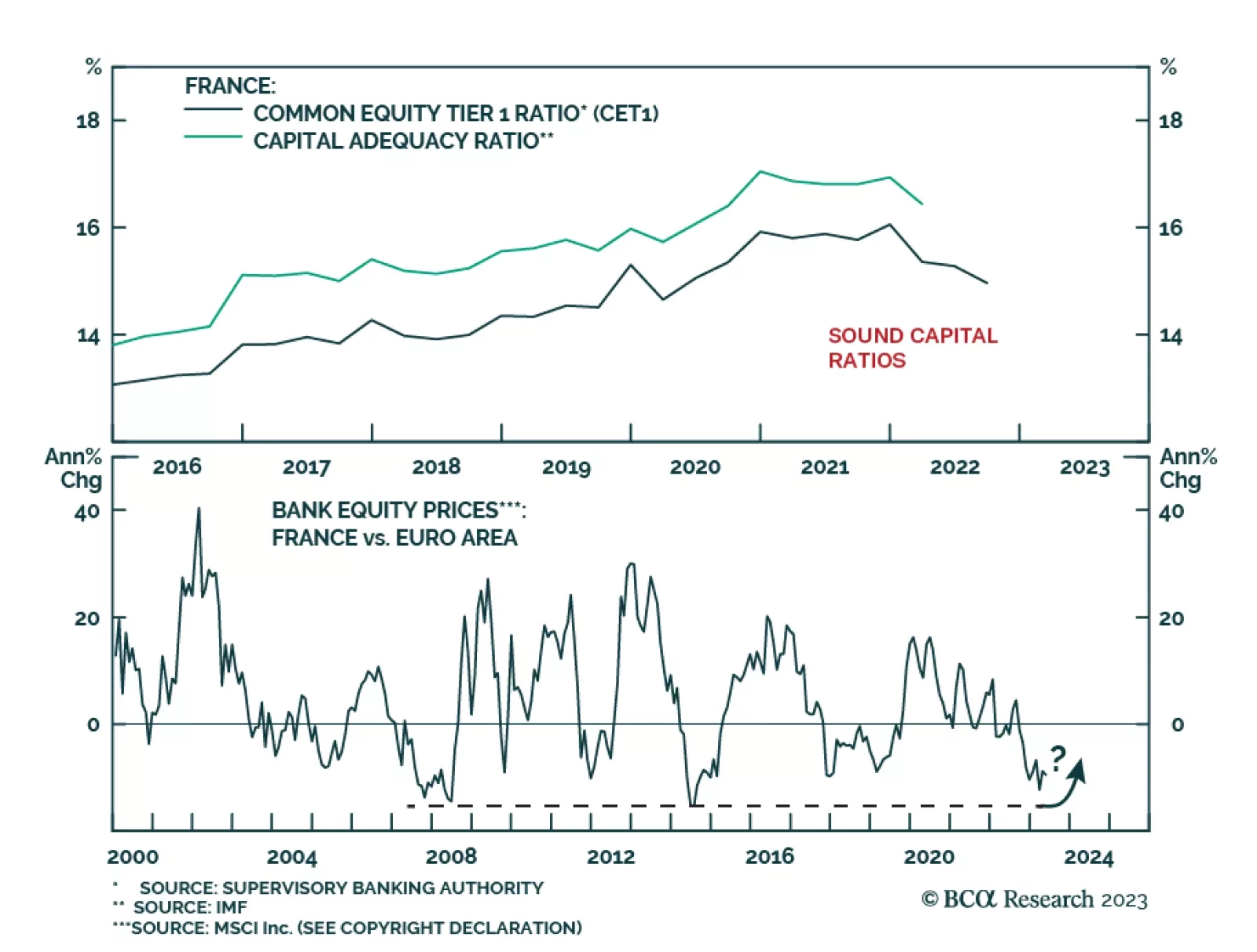

Now that the French pension reforms have been passed, President Macron’s focus will be on the international stage. Where are the risks and opportunities for French assets created by this pivot?

President Erdogan and the Justice and Development Party emerged as the winner of the Turkish general election which was concluded yesterday. This victory means that their expansive policies of the past decade will continue, and Turkish assets will suffer. Across the Aegean, the Greeks voted to reelect the New Democrats under the leadership of Prime Minister Mitsotakis. Their fiscal prudence and structural reforms will be continued as voters had rewarded them with another term in office. Go long Greek versus Turkish equities.

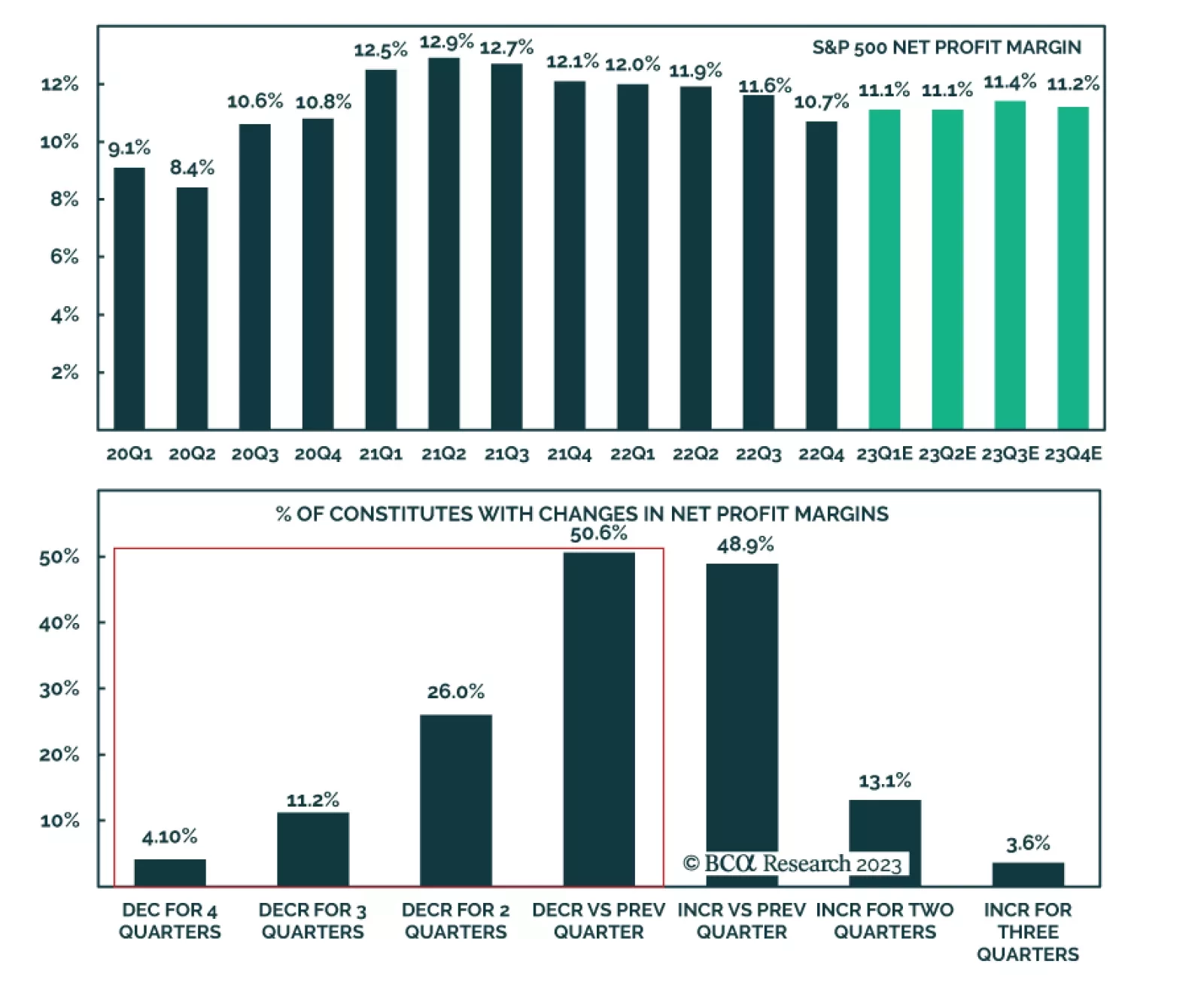

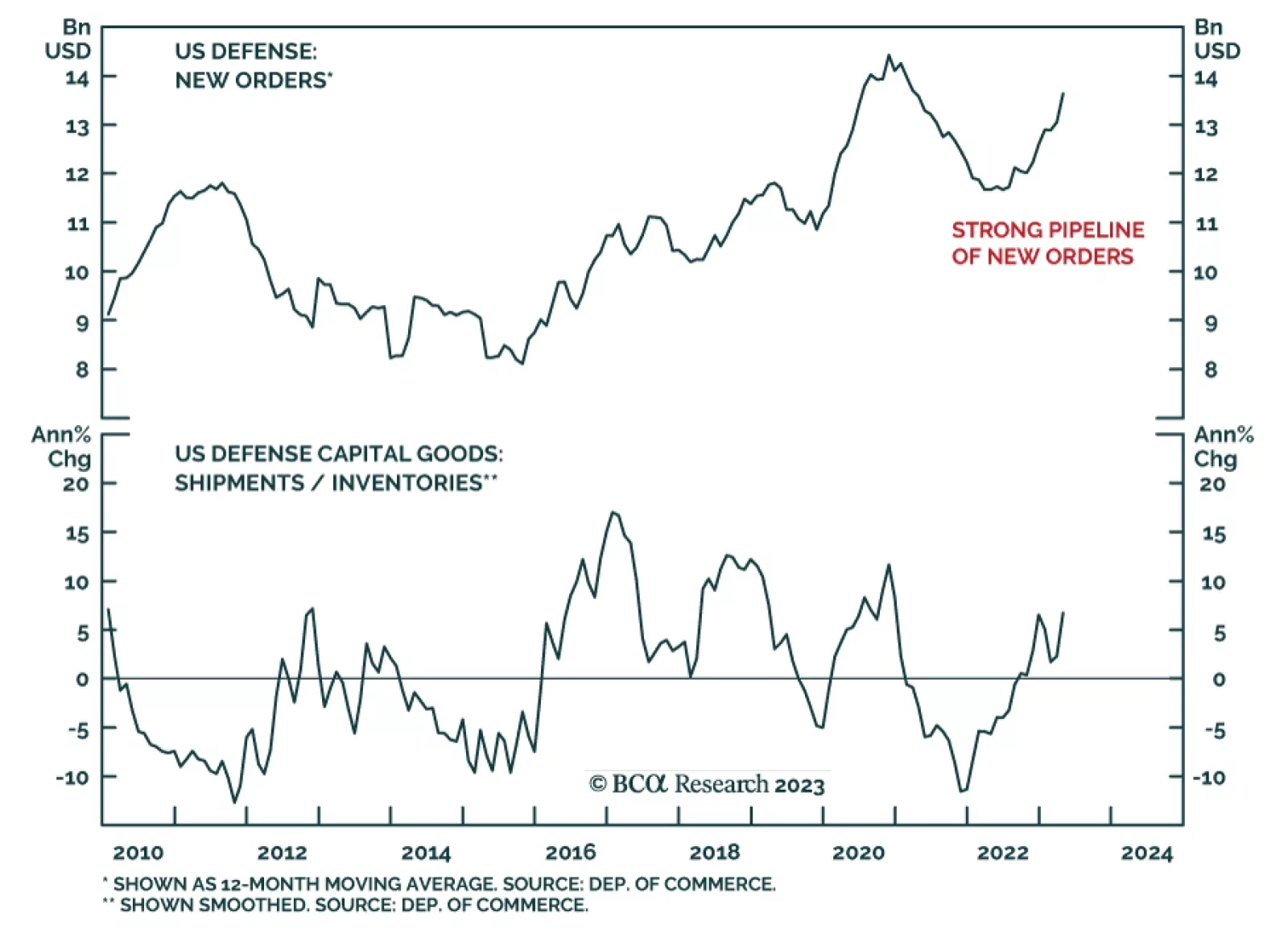

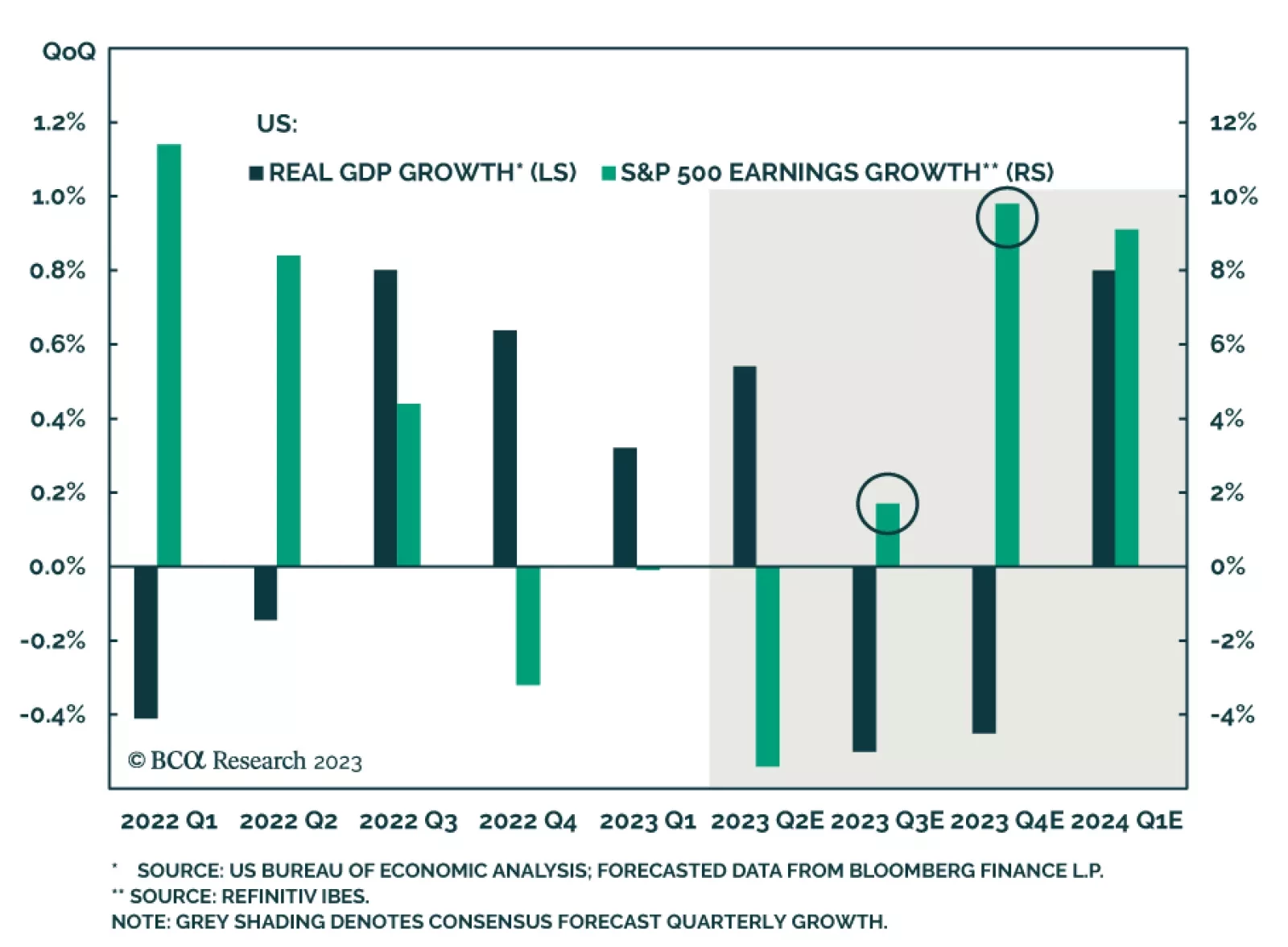

Once the debt ceiling soap opera ends, investors will likely turn their attention to some of the tailwinds supporting stocks. These include stronger earnings growth, diminished bank stresses, better housing data, early signs of an upleg in the manufacturing cycle, the prospects of an AI-driven productivity boom, and the fact that labor slack has managed to increase without rising unemployment. Investors should resist turning bearish on stocks for now but look to become more defensive later this year.