Equities

The economy remains resilient despite a softening labor market. As the economy shifts from labor toward capital, we may be in the early stages of a “jobless boom.” Our bull case for equities rests on strong earnings growth, accelerating GenAI adoption, monetary easing, and stimulus from OBBBA. Key risks we continue to monitor are rising bond yields and the threat of stagflation.

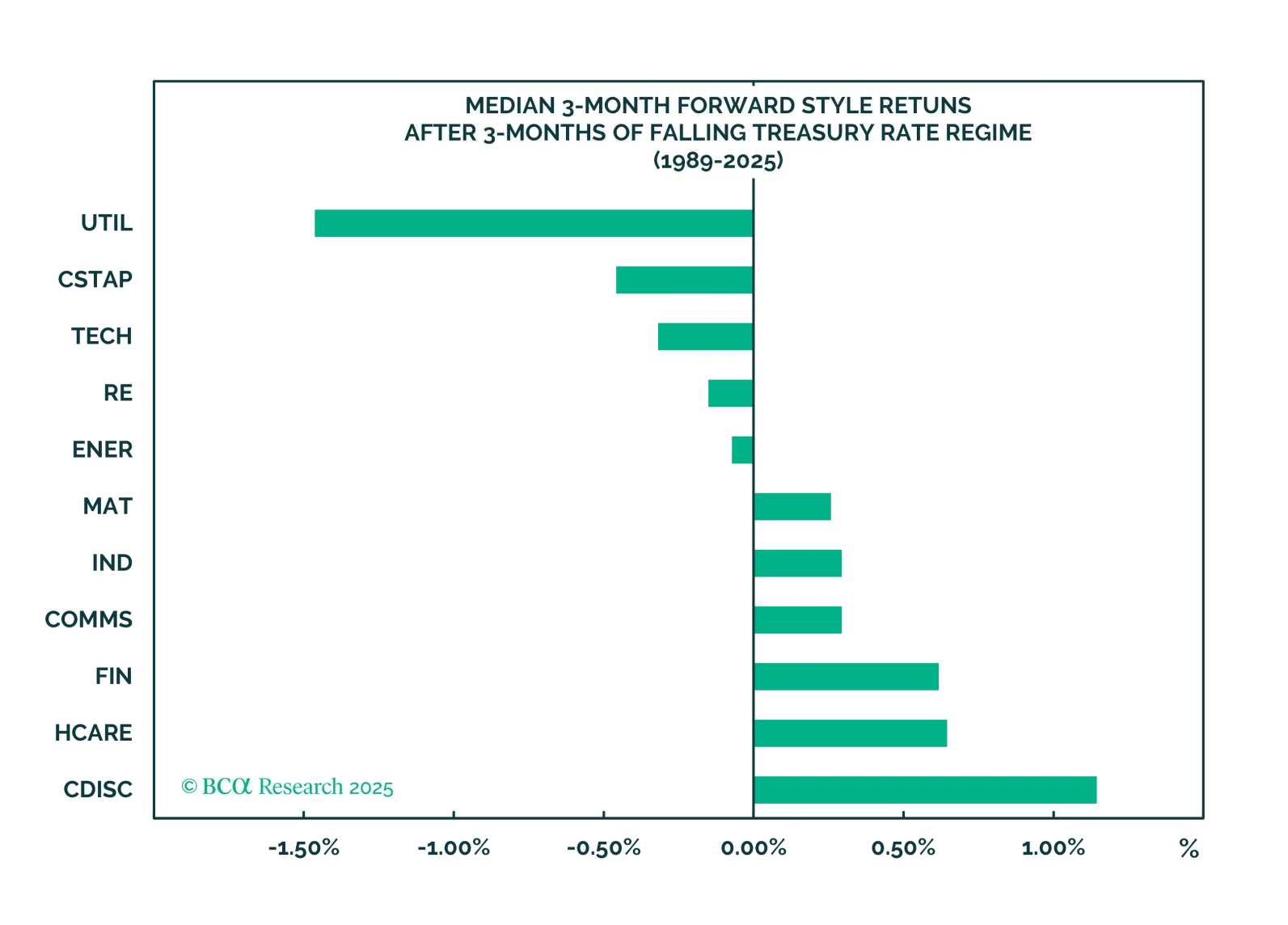

In this update, we apply our Macro Surprises framework to equities for the first time. Overall, the message is broadly consistent with our current equity views: Investors should favor Eurozone equities and continue to overweight cyclical sectors relative to defensive ones.

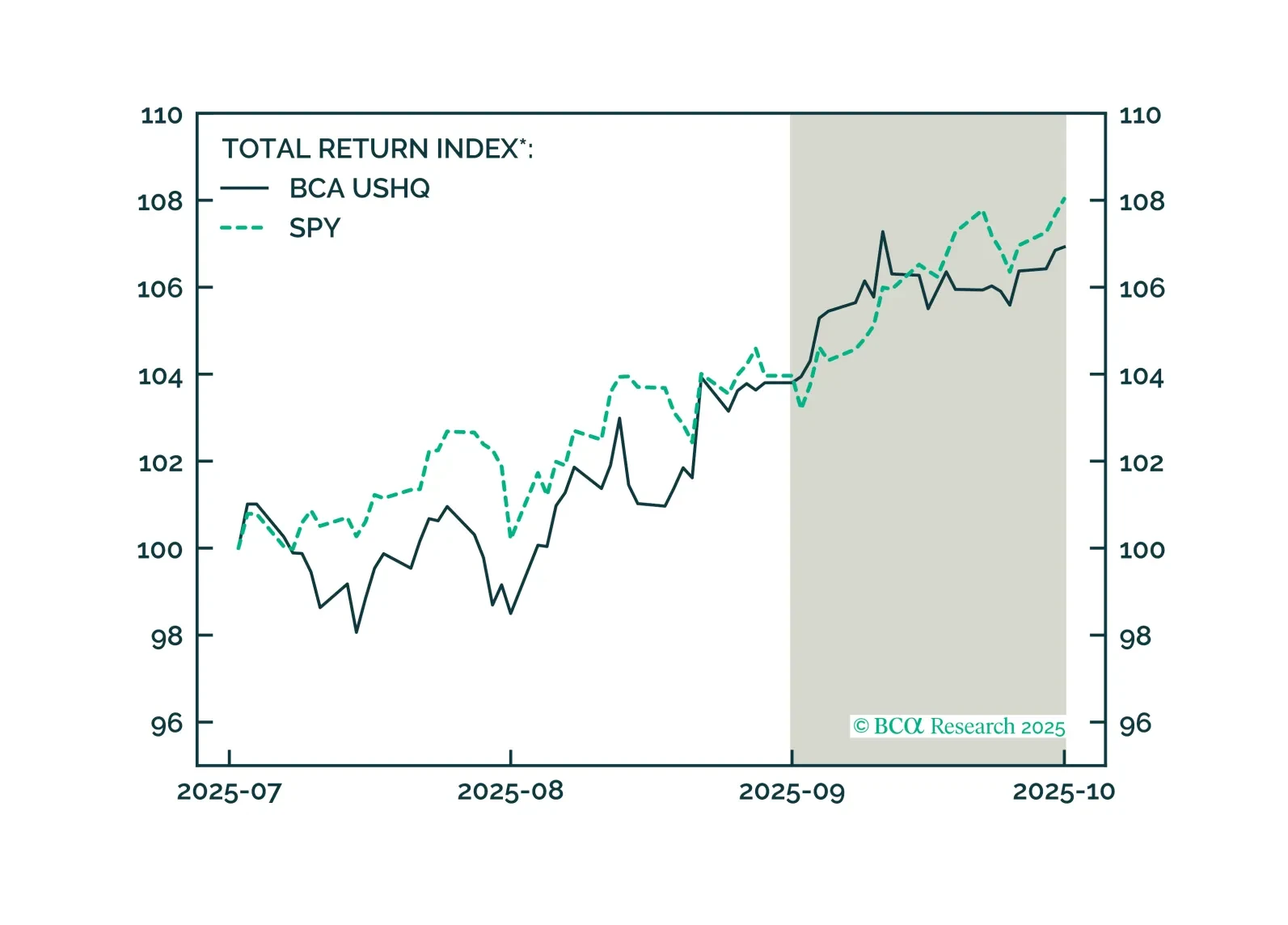

The US High Quality (USHQ) portfolio underperformed its benchmark through September, returning 3.01%, whilst its SPY benchmark returned 3.91%. However, our US High Quality SMID (USHQ SMID) portfolio continues to show strength, with another solid month of performance. The portfolio returned 2.69%, outperforming its MSCI US Mid Cap benchmark by 169bps.

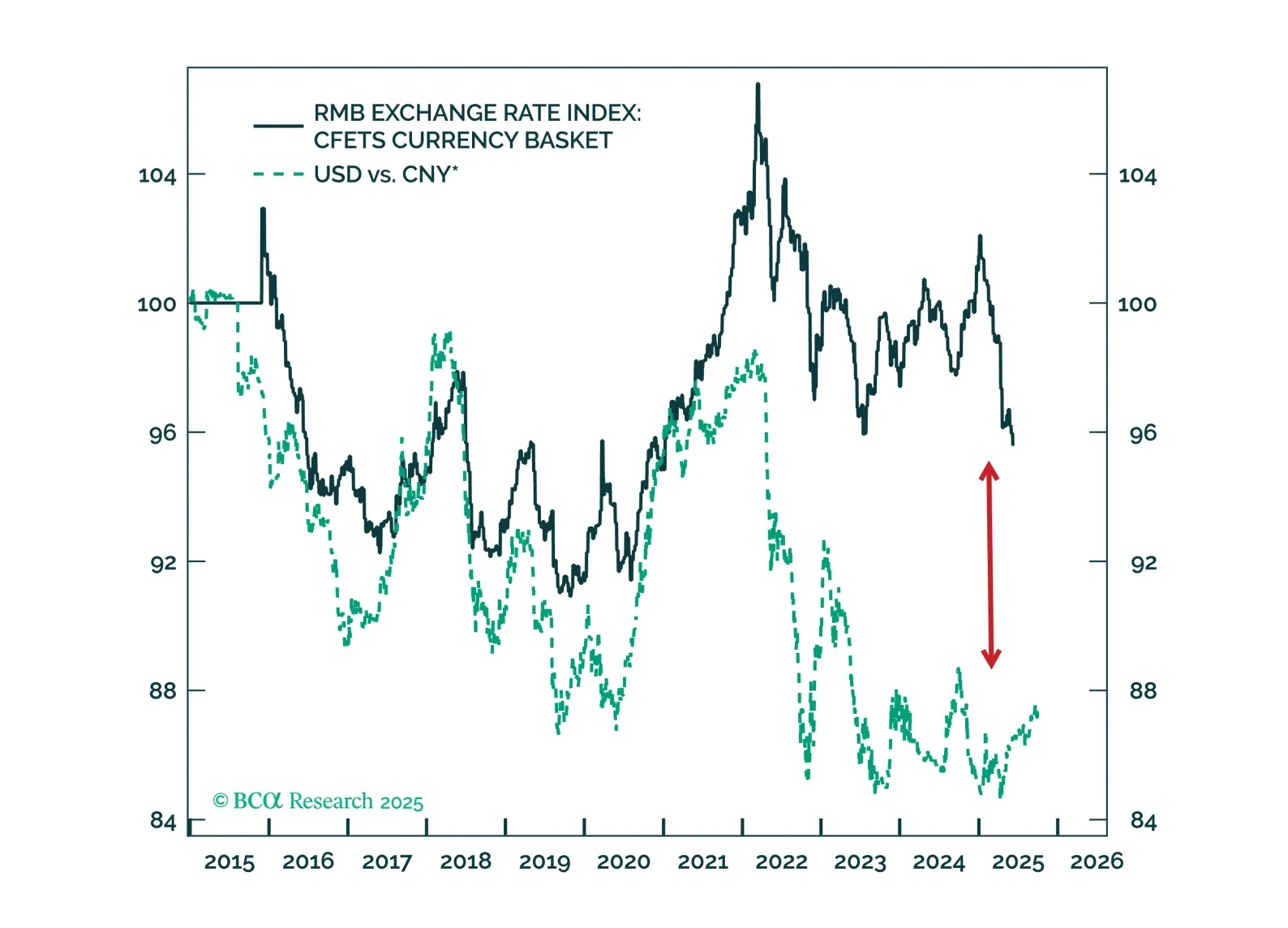

The CNY/USD has room to appreciate both cyclically and structurally, while nominal yields on China’s long-duration government bonds are set to fall. This combination supports Chinese equities.

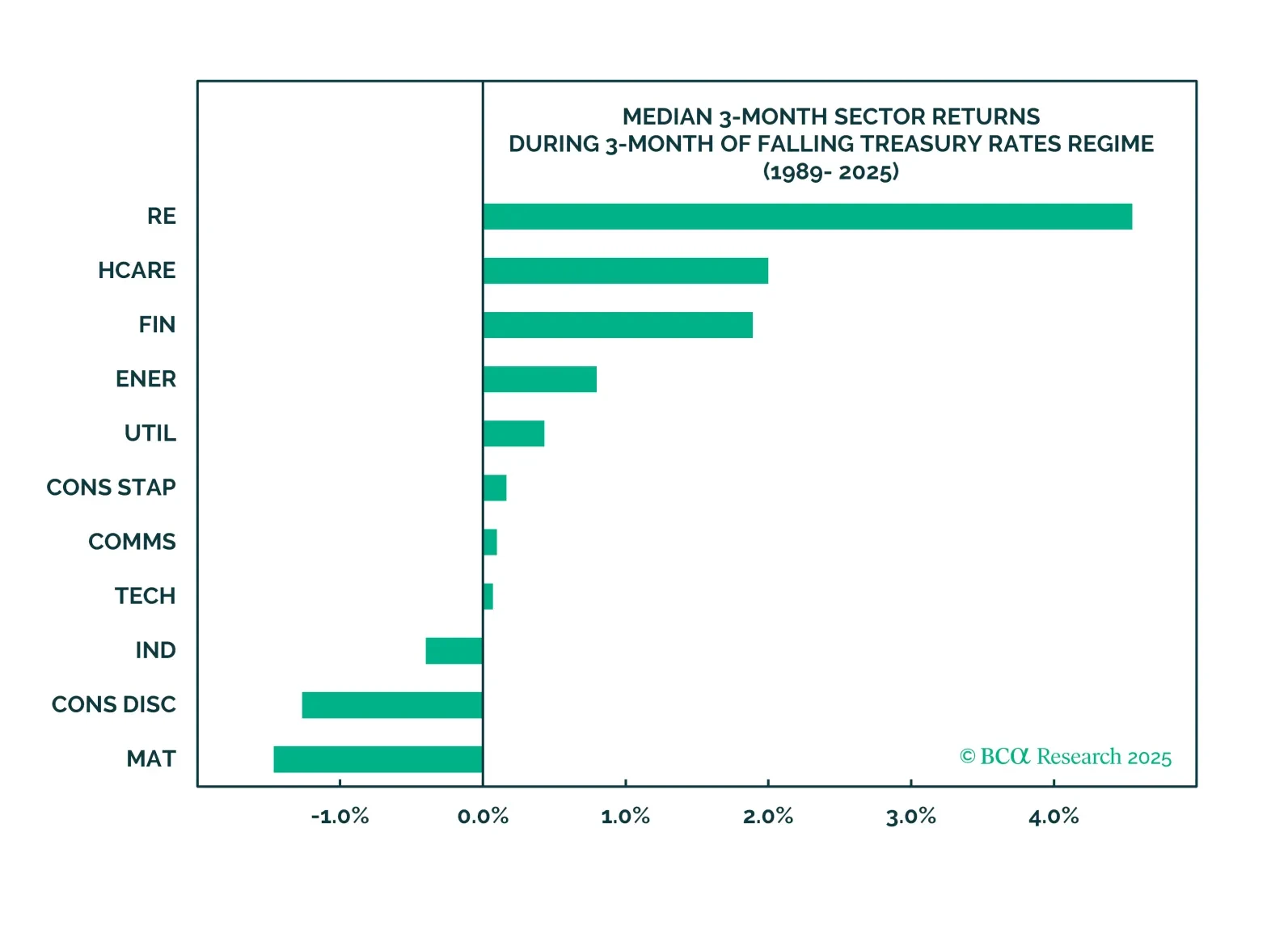

Real Estate performance is contingent upon the Fed rate-cutting cycle. Yet, we worry about a hawkish Fed surprise and are closing our overweight in the sector. We also recommend a granular approach to subsector selection.