Equities

We are constructive on equities in 2026, as monetary easing, fiscal support, GenAI-related capex, and strong earnings growth are unequivocally positive for the asset class. Valuations are extended, but concerns about a bubble are overstated. Despite the favorable backdrop, we expect the S&P 500 to return only 5–10%, ending 2026 between 7,200 and 7,500.

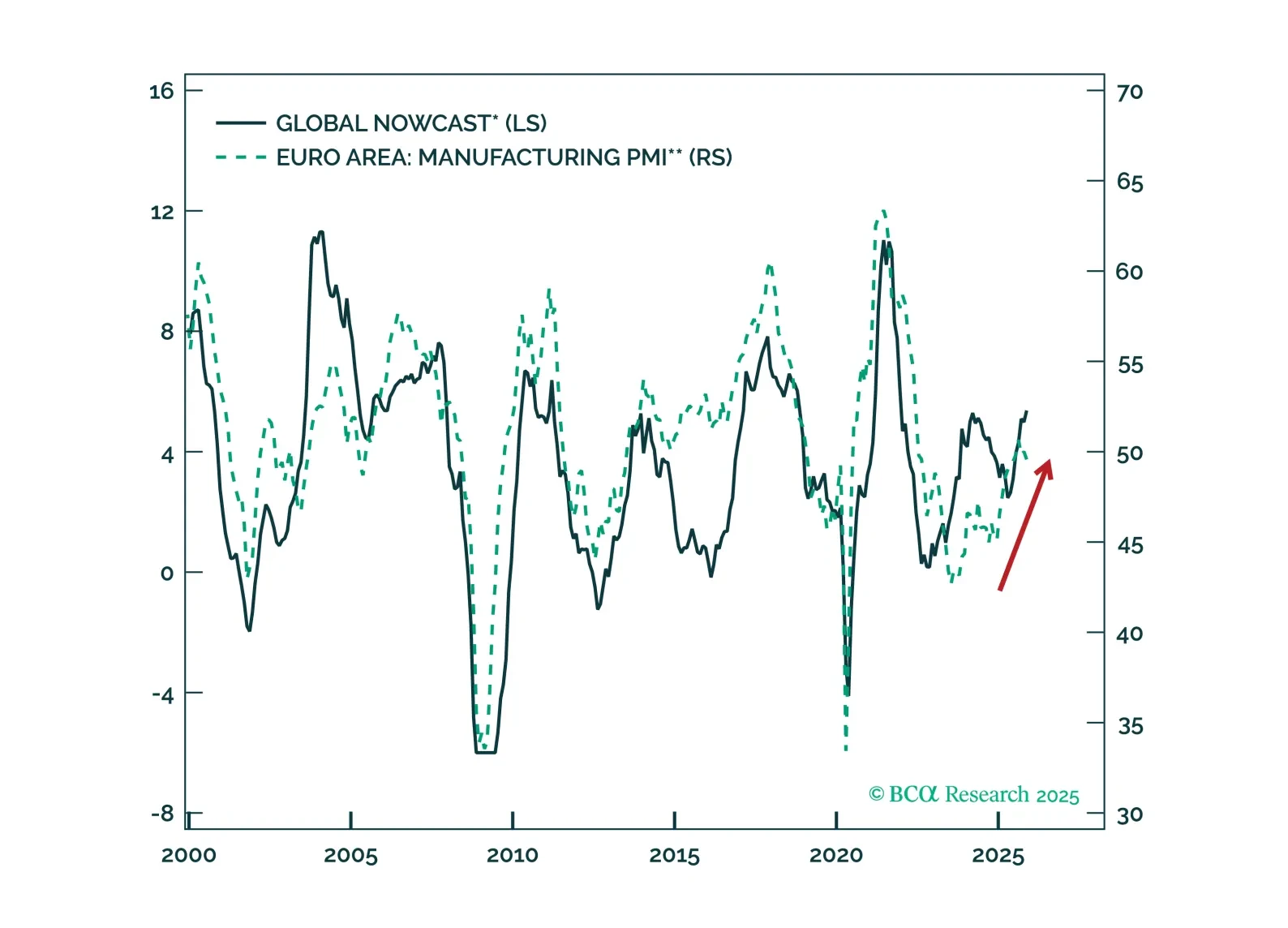

Our 2026 Outlook presents our five key views for Europe’s macro landscape and markets in 2026 —a year poised to reveal the true strength of the recovery.

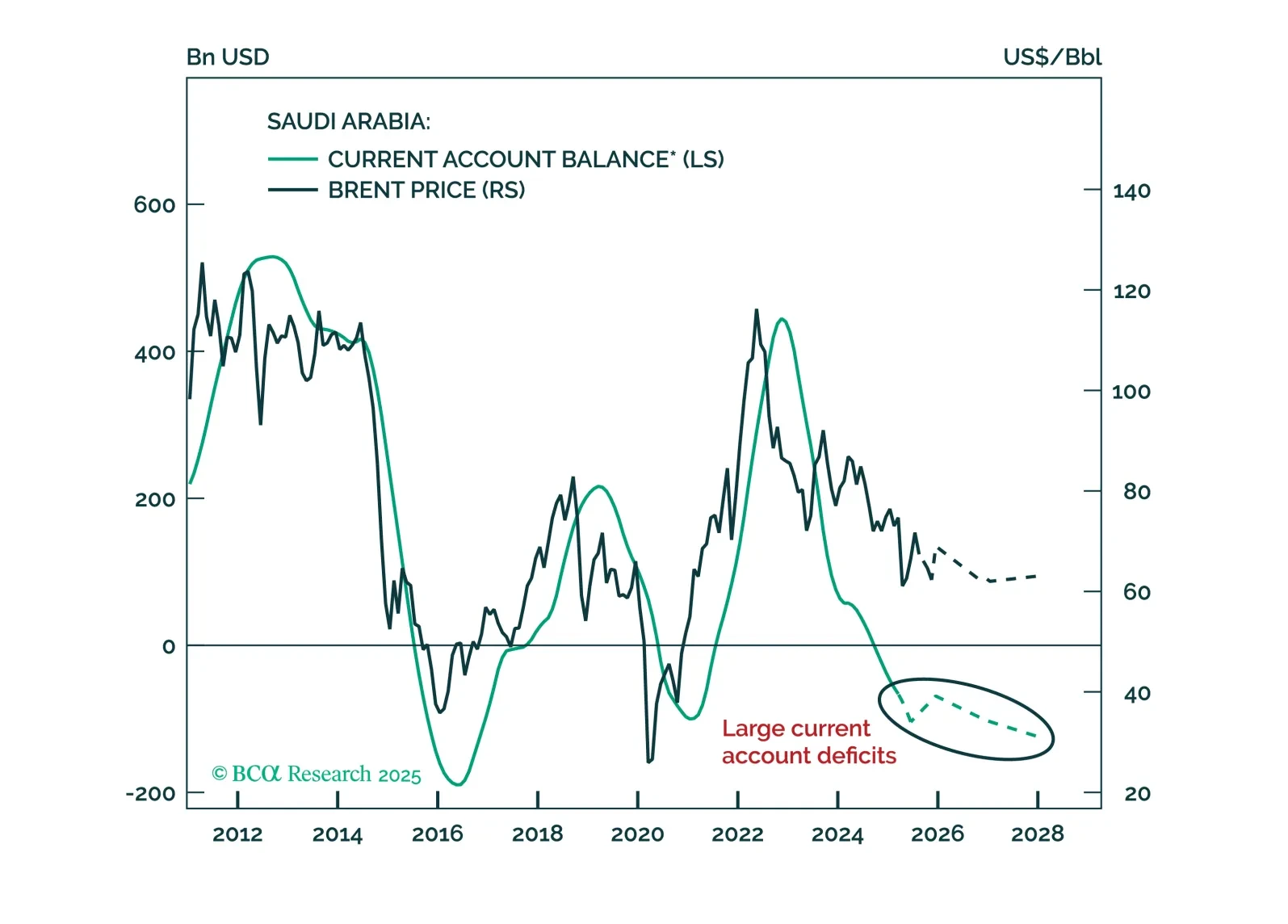

The Kingdom faces a troika of global factors in the next 12-18 months: (1) US policy rates will be cut considerably; (2) the US dollar will depreciate significantly; and (3) crude prices will remain low.

How should investors position themselves in this market?

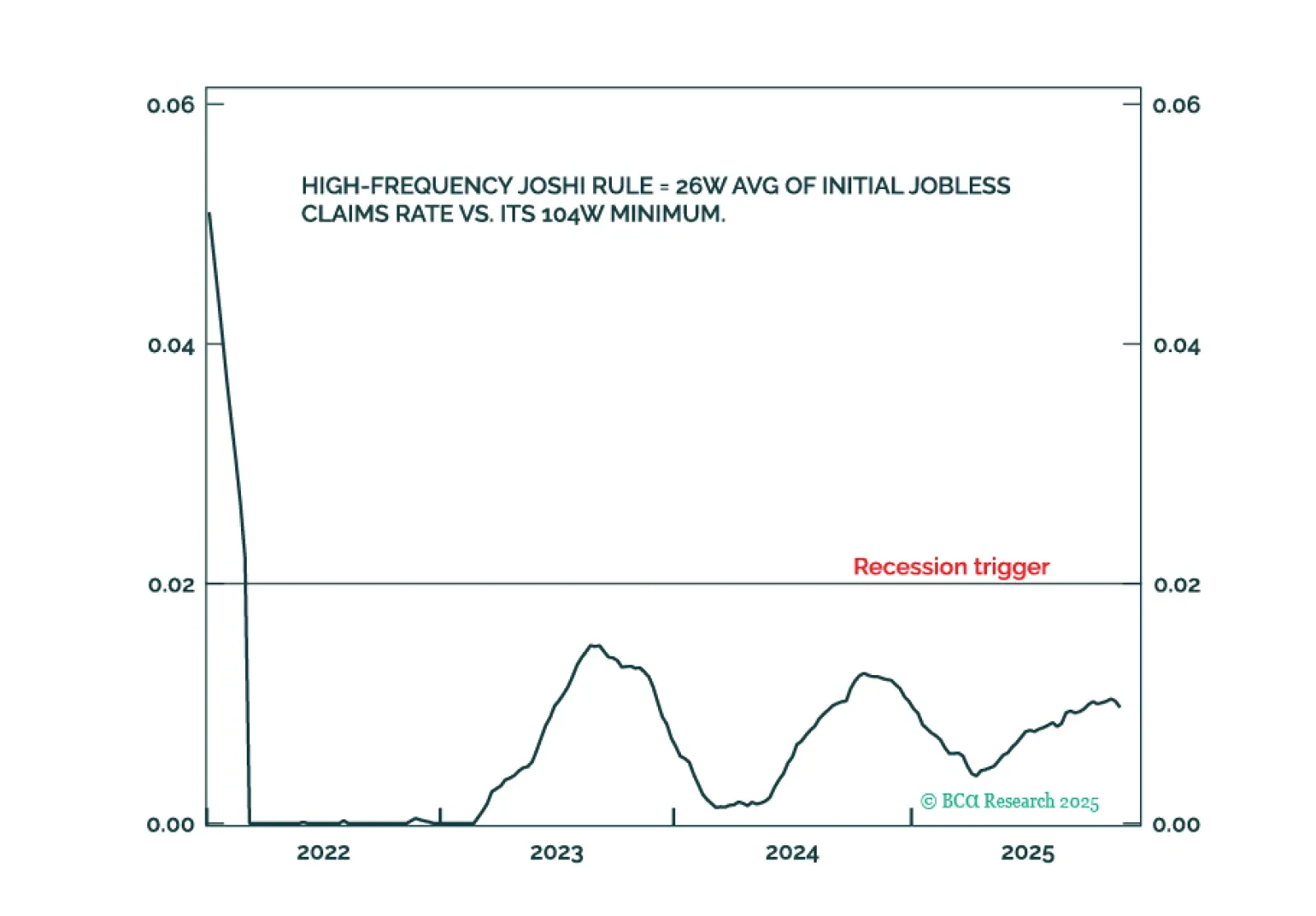

The high-frequency Joshi Rule confirms that the US labour market is holding up. Equity investors should regard 5-10 percent selloffs as tactical buying opportunities. Bond investors should stay underweight US duration. Plus, a new high-conviction trade is to go overweight the 30-year German bund versus the 30-year US T-bond.

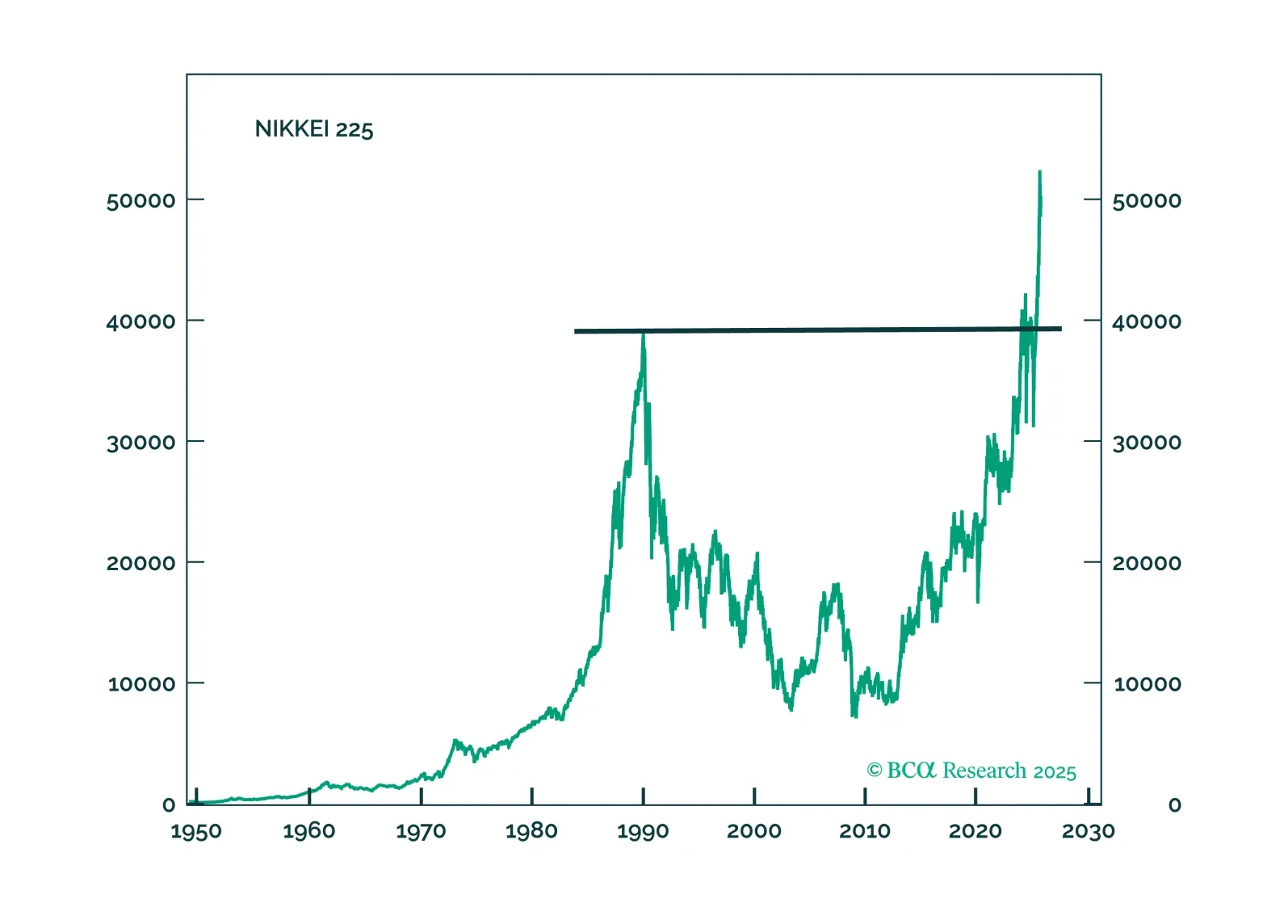

Japanese financial assets will finally have unfettered access to outsized returns. This performance will come in fits and starts, but we are comfortable laying our cards down on buying the yen, and Japanese industrial stocks.

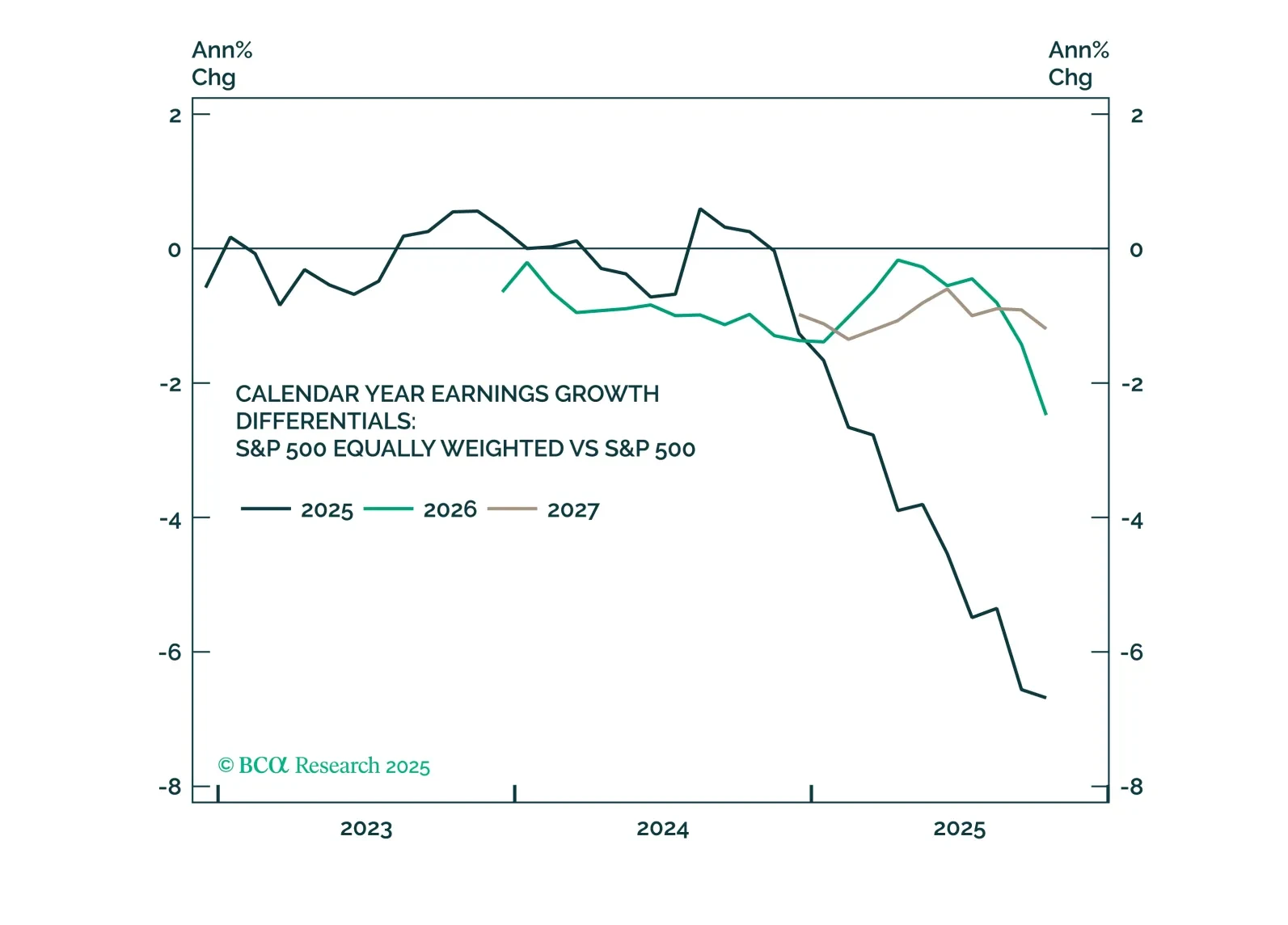

The outperformance of the S&P 500 relative to the S&P 500 EW index is likely to continue over the next year, supported by stronger earnings growth. However, extreme levels of market concentration will ultimately halt the outperformance of the mega-caps.

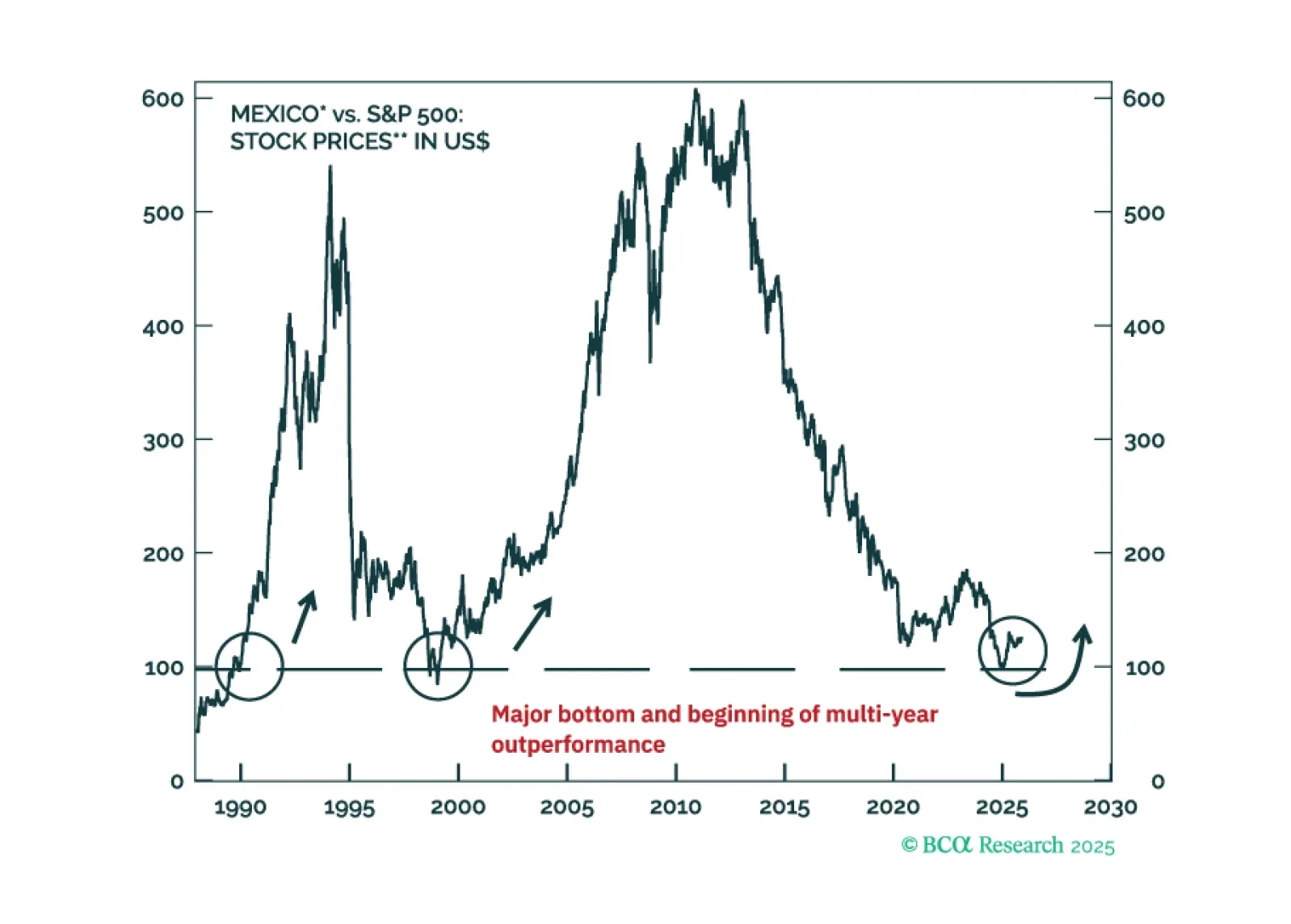

Mexican equity and fixed-income markets will continue outperforming their EM counterparts, regardless of whether global risk assets sell off or not. Also, we recommend a new trade: long Mexican stocks / short the S&P 500.

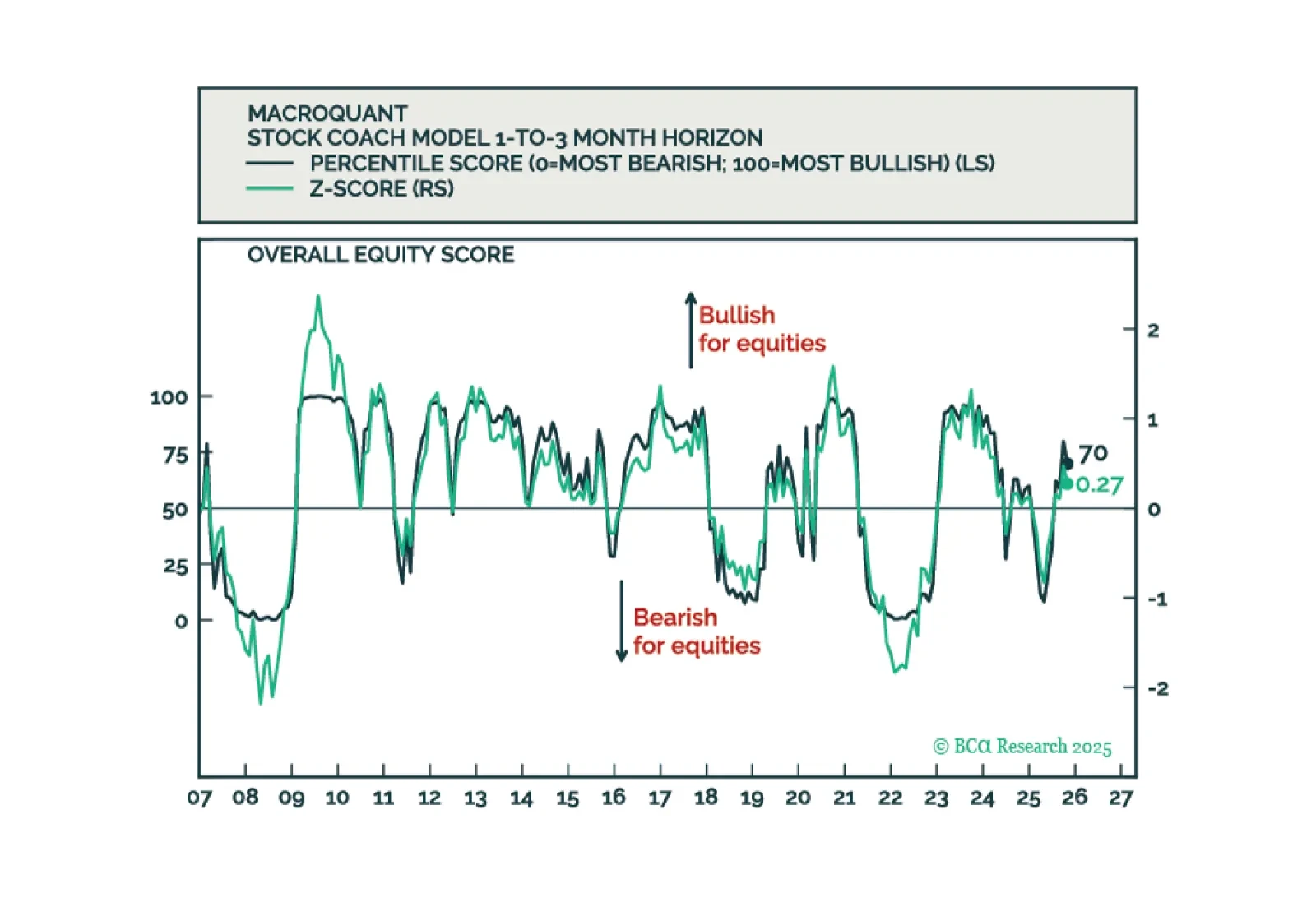

MacroQuant remains tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold.

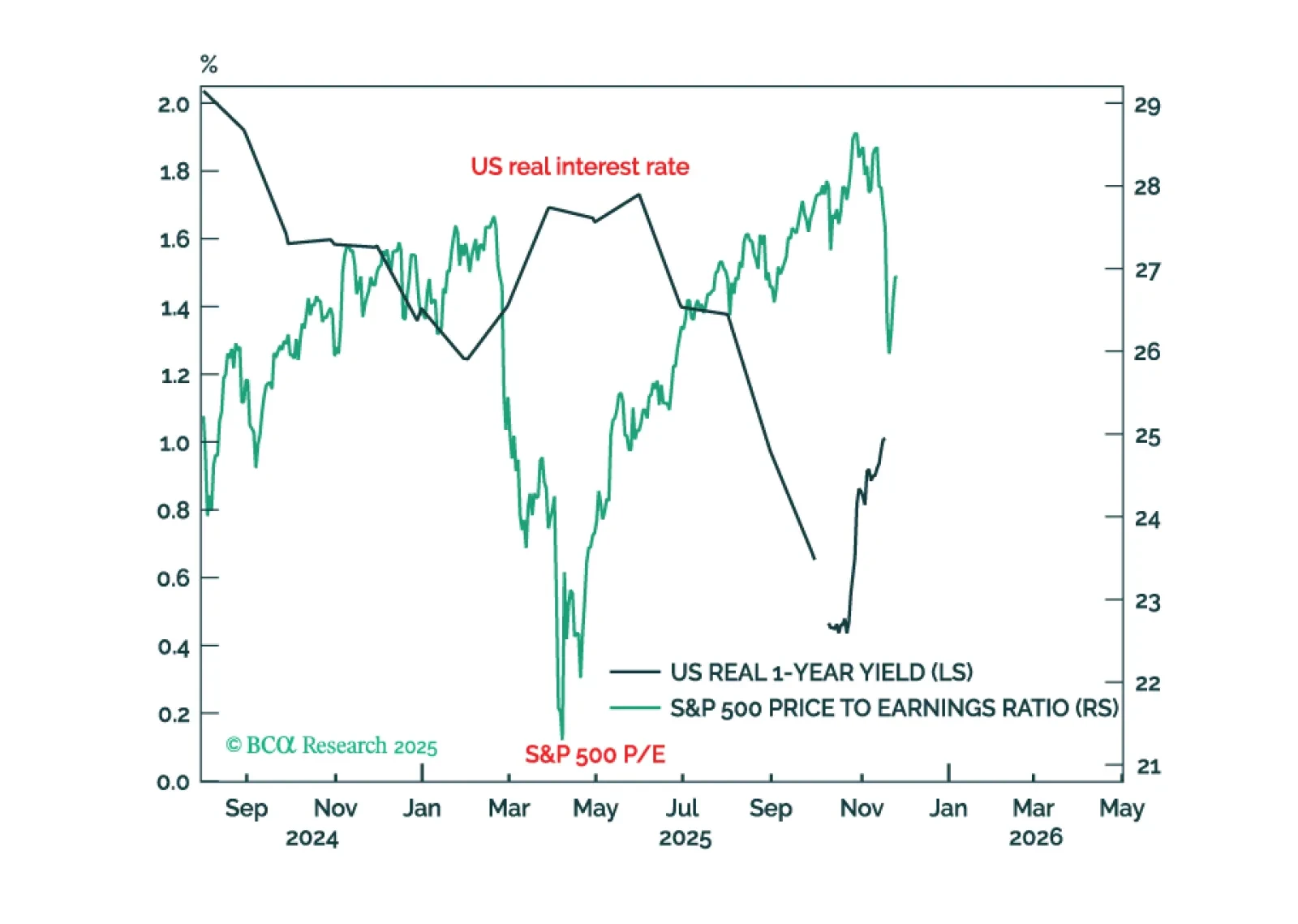

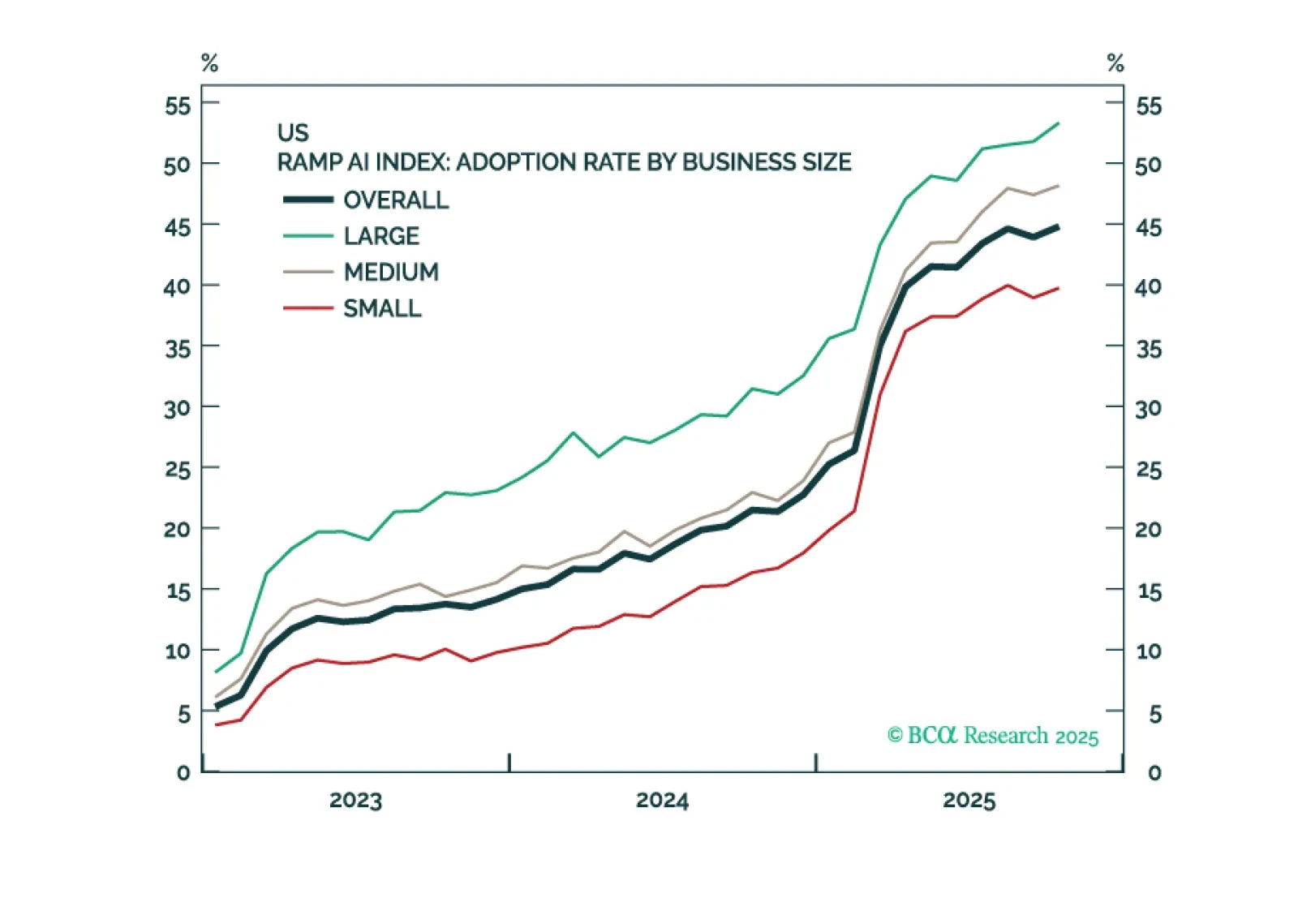

Stock market valuations are moving as a near-perfect mirror image of the US real interest rate, meaning that the Fed is underpinning the stock market. But if the market stopped believing in AI-driven profits growth, valuations would collapse, irrespective of the Fed’s efforts to underpin them. When might this happen? Plus, two new tactical trades are: long BTC versus gold; and overweight industrials.

The odds have risen that we have reached a “Metaverse Moment” – a situation where investors punish AI companies for increasing capex. This warrants greater caution towards AI stocks specifically, and the broader S&P 500 more generally.