Energy

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

The attacks on Red Sea commercial tankers by Iran’s Yemeni proxies, the Houthi movement, are an inflation risk inasmuch as they lengthen voyage times for any shipping forced to avoid the Bab el-Mandeb Strait. The risk of an expansion of these attacks is, in our view, limited, given Iran’s inability to project naval power in the region.

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

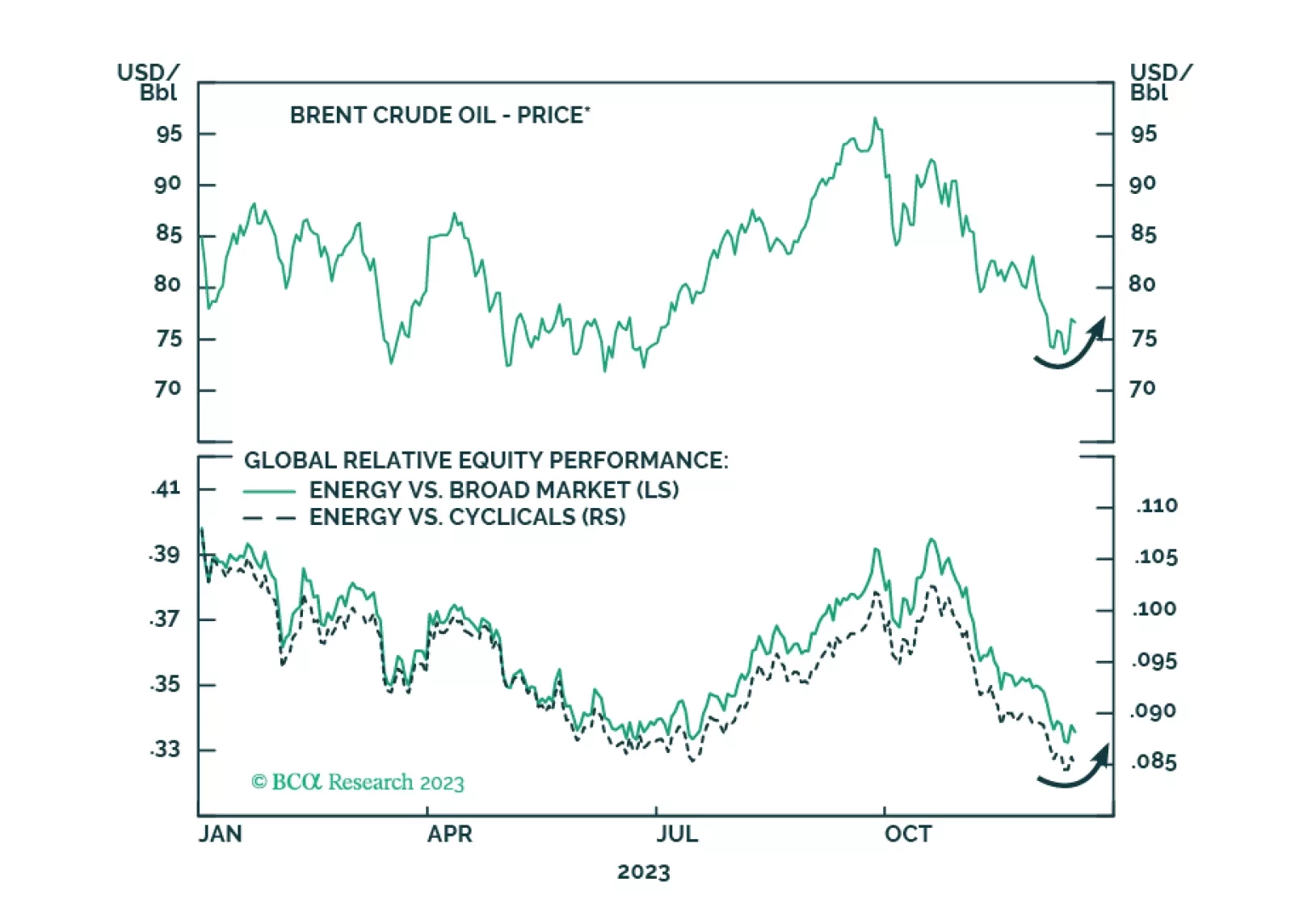

Oil prices will rise tactically due to supply risks. Recent developments indicate escalation of the conflict with Iran in the Middle East and confirm our expectation of energy supply disruptions and oil price spikes in the short run.

Political economy dominates fundamentals going into 2024, as states prepare for war and de-risk supply chains. Asynchronous global growth will elevate commodity-price volatility. We expect oil to trade above $100/bbl in 2024 and continue to favor equity exposure to oil-and-gas producers. Given weak capex, we also favor metals miners and refiners. We remain long the Gold, the XME and COMT ETFs We were stopped out of our XOP ETF with a 12.5% gain; we will re-establish it at tonight’s close.