Emerging Markets

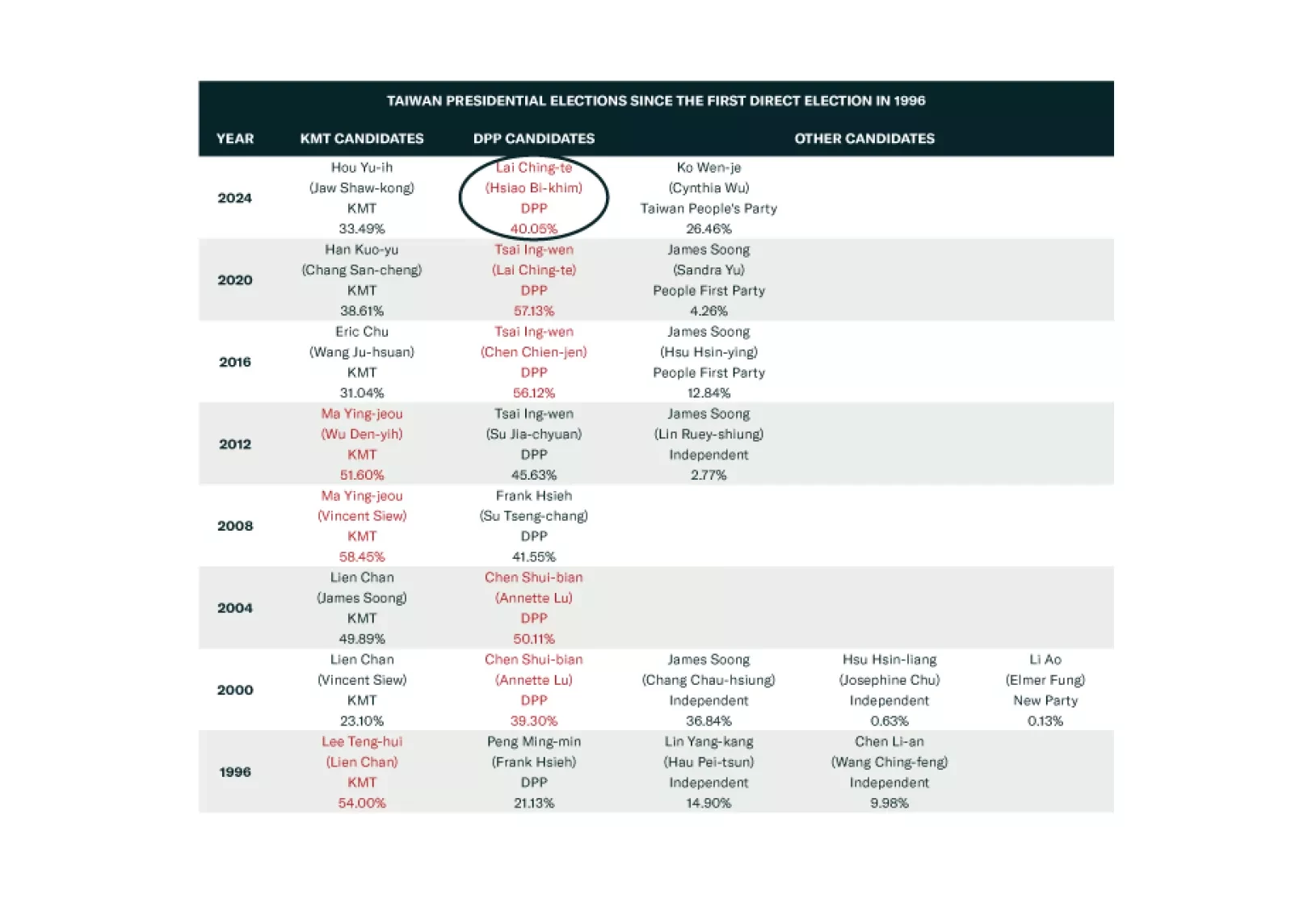

Taiwan’s election will lead to serious Chinese military and economic pressure but not full-scale war. War is a long-term concern. Investors should short TWD-USD.

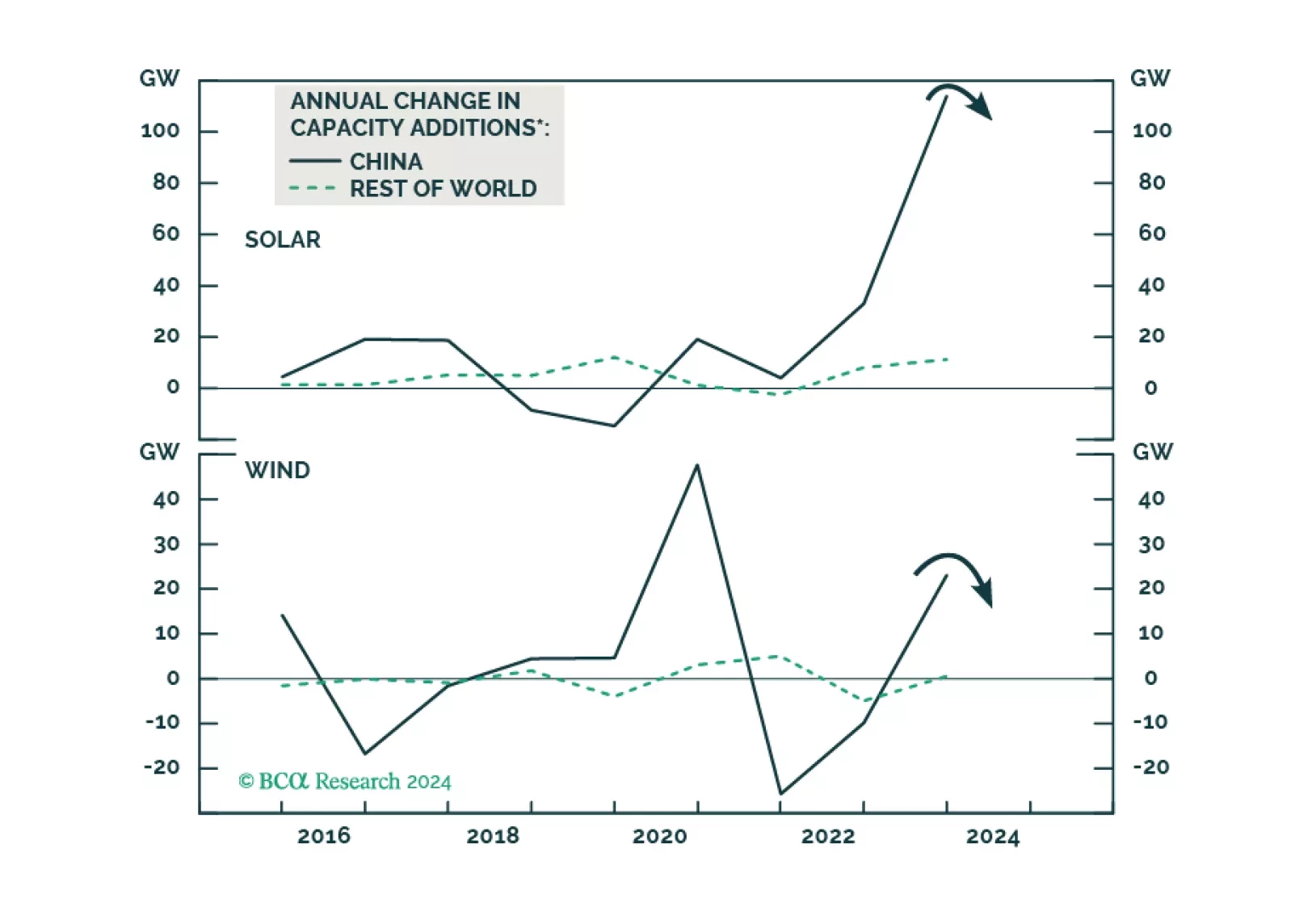

The global green energy rush faces mounting headwinds. Additional global solar and wind capacity installations will have considerable growth reduction this year. Copper prices did not drop much in 2023 due to surging demand from green power build-up. Green power will be less positive for copper demand in 2024 than in 2023. We expect more downside in global renewable energy stocks.

We share the edited transcript of a webinar we participated in discussing global trade, trade wars and tariffs, as well as de-risking strategies.

In this brief Insight we examine the expanding Middle East conflict and update the situation in the Taiwan Strait on the eve of elections. The Houthis are a distraction and China is not likely to invade Taiwan in the near term, but both situations support our overweight of US equities relative to global. Global growth is likely to slow while commodities are likely to see at least minor supply shocks.

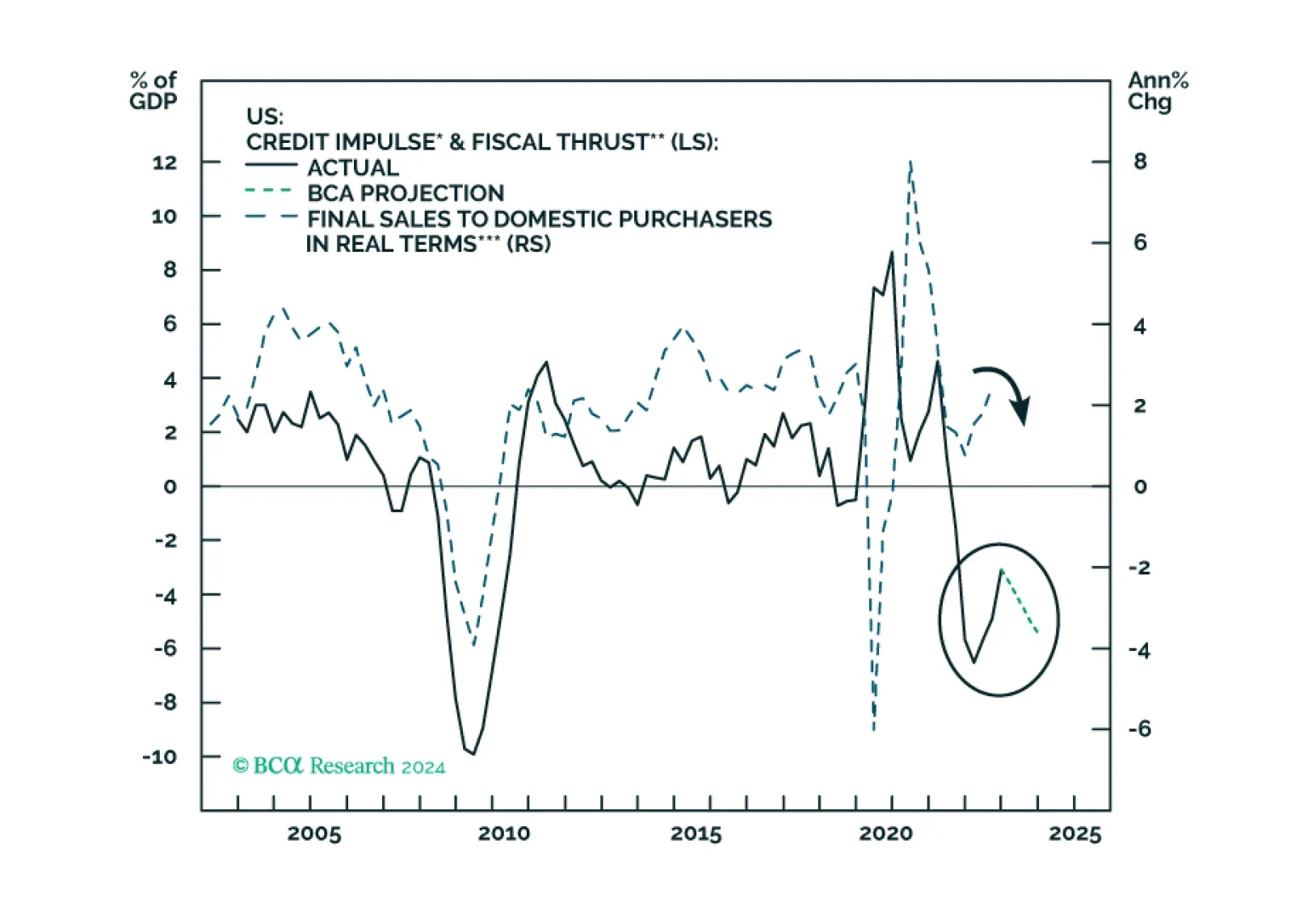

The combined US credit impulse and fiscal thrust indicator will likely relapse in 2024, heralding growth weakness. Stalling US sales volume and falling inflation, combined with sticky labor costs, will herald a non-trivial profit margin compression. The recent increase in Asian exports will likely prove to be a mid-cycle improvement rather than a cyclical recovery.

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.