Economy

Recent data releases have painted a mixed picture of US housing market dynamics. On the one hand, housing starts and building permits unexpectedly increased on a month-on-month basis in October. After falling in 2022, housing starts have somewhat…

Global market sentiment has improved notably since late-October. In the equity space, DM and EM stocks have gained 8.5% and 7.8% respectively since October 26. Regarding currencies, the counter-cyclical DXY index has lost 2.2% so far in November. And as we…

Oil prices have relapsed despite the supply cuts and the geopolitical volatility stemming from the Middle East. Odds are that global oil demand is downshifting. The chart above illustrates that there is a tight relationship between crude oil prices and the…

BCA Research's US Bond Strategy service continues to recommend a neutral allocation to TIPS for now, but with a bias to turn underweight. The team calculates a forecasted range for headline CPI inflation of 0.9% to 2.9% over the next 12 months. For core…

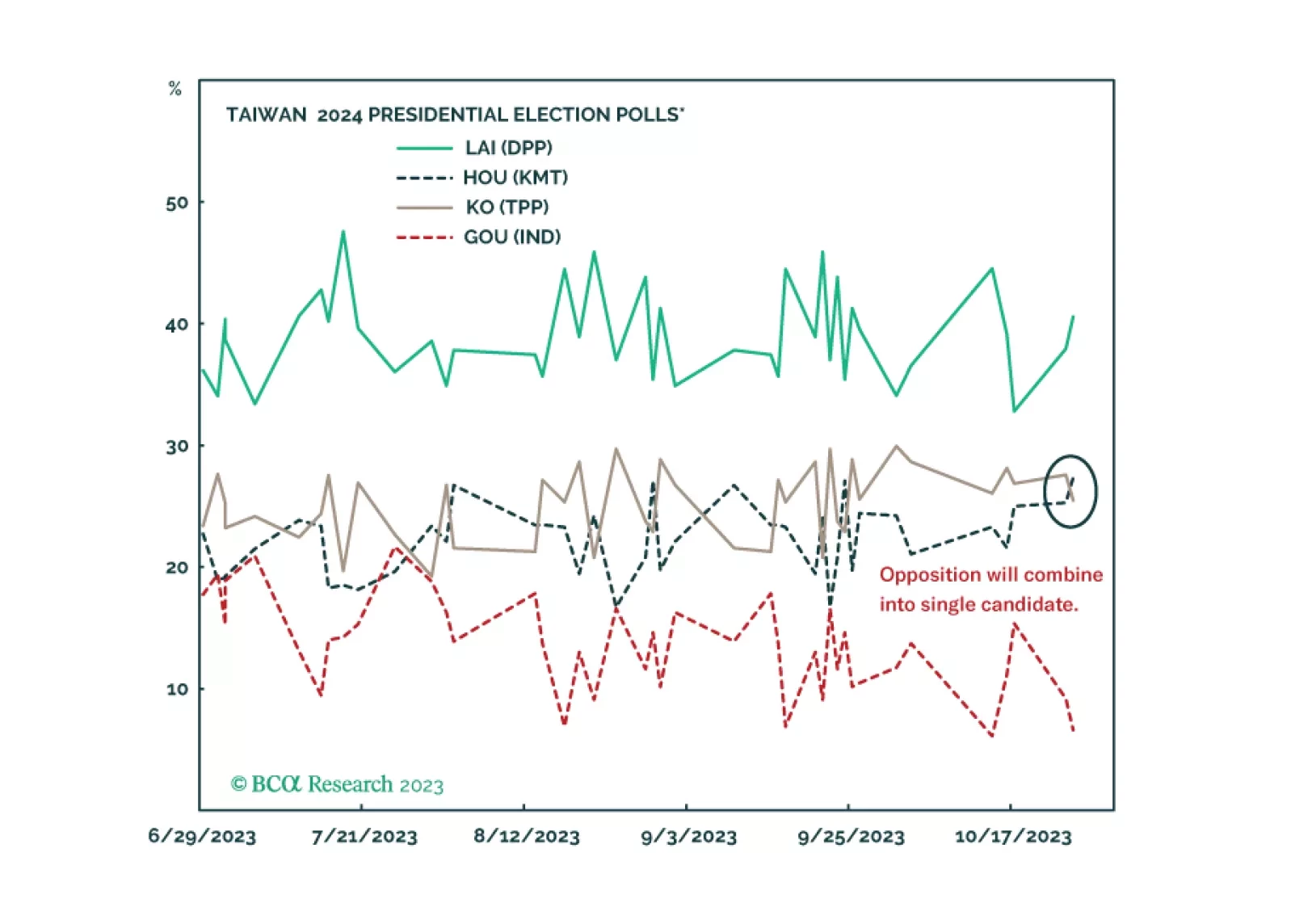

Watch Taiwan, Not US-China, For Détente

Investors should not get their hopes up about the Biden-Xi summit. Wait to see if a new ruling party is elected in Taiwan before downgrading geopolitical risk in the Taiwan Strait. US-China strategic détente is possible but neither the geopolitics nor the macro backdrop warrant a risk-on position next year.

US jobless claims have been trending higher in recent weeks, confirming that labor market conditions are deteriorating. Initial claims came in slightly above consensus estimates on Thursday, increasing by 231 thousand versus expectations of a 220 thousand…

The latest house price data indicate that China's housing market remains weak. The prices of newly built homes across 70 medium and large Chinese cities declined by 0.4% m/m in October – a faster pace of decline than the 0.3% m/m drop registered in September…

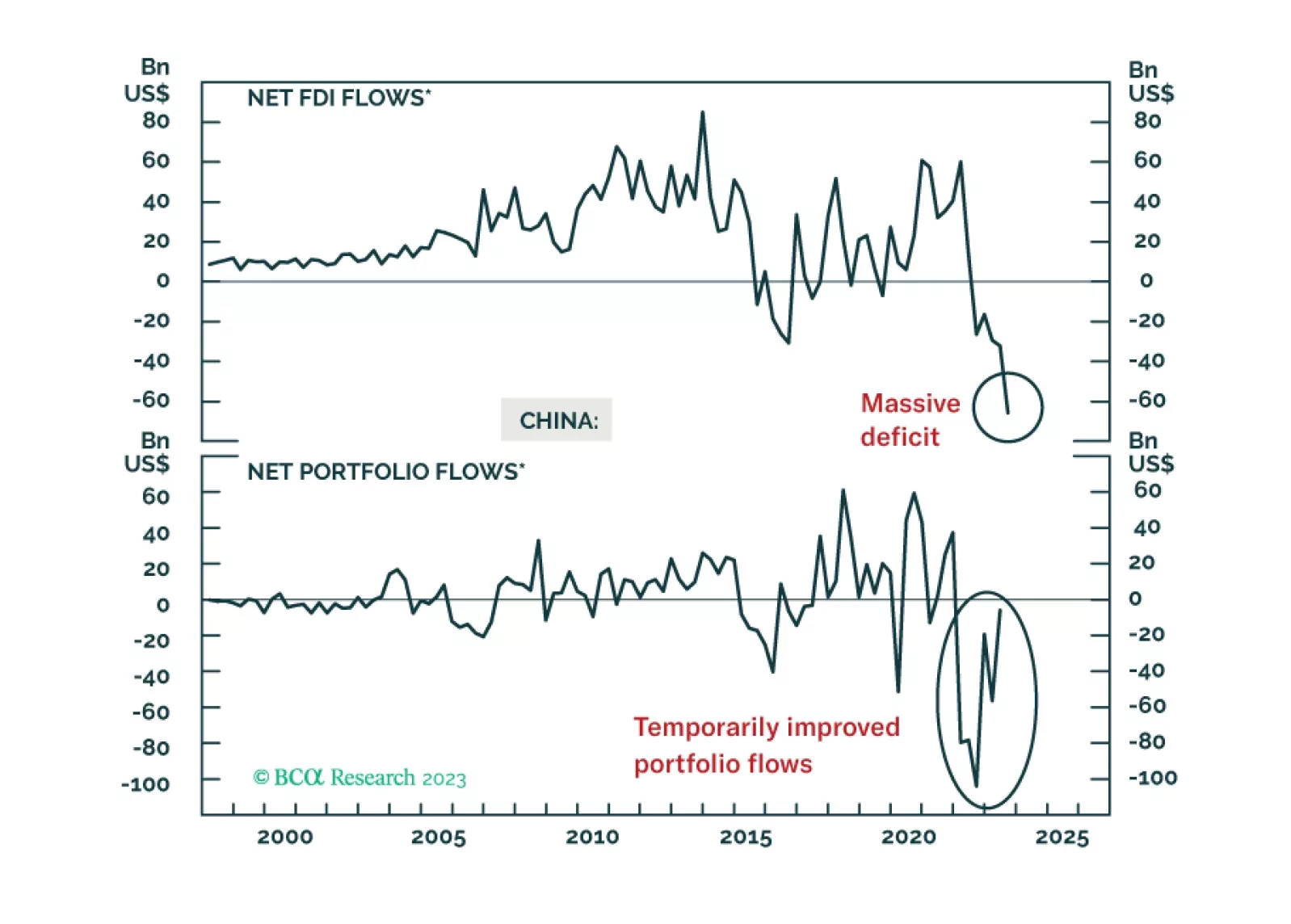

China’s capital outflows will likely remain substantial at least through the next few quarters. This wave of capital outflows will likely be more chronic, albeit less acute than the 2015-16 episode. Persistent capital outflows will exert downward pressure on the RMB.

The US retail sales release delivered a mixed signal about US consumption. Although the headline figure contracted by 0.1% m/m in October, it was better than expectations of a 0.3% m/m decline. Moreover, the September increase was revised up from 0.7% m/m to…

On the surface, the acceleration in Chinese retail sales and industrial production growth in October suggests that the economy is holding up. Retail sales expanded by 7.6% y/y last month – beating expectations of 7.0% y/y following a 5.5% y/y increase in…