Economy

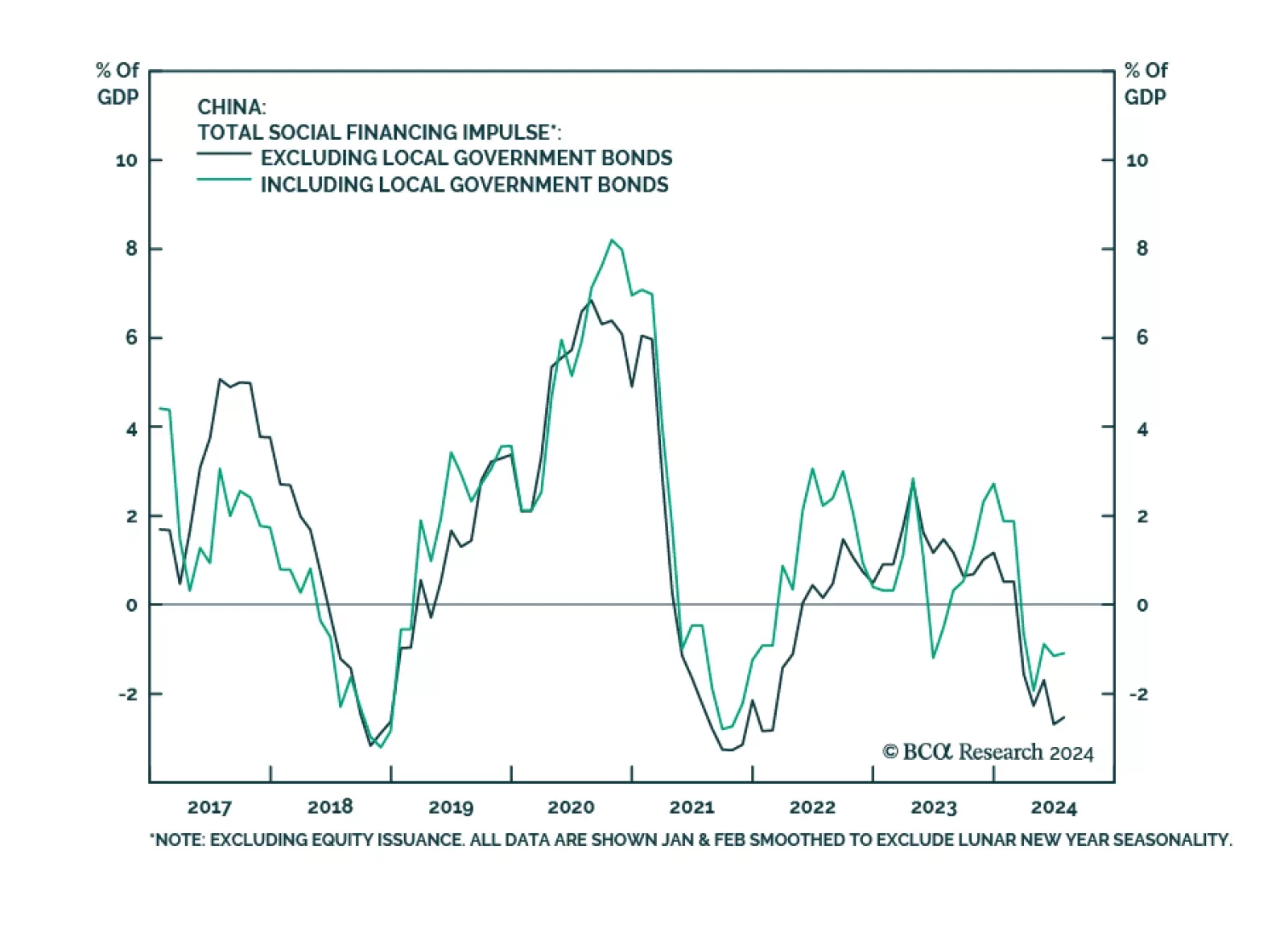

Subdued demand for credit among Chinese private-sector businesses and households persisted through July. Aggregate financing missed expectations, growing CNY 0.8bn to CNY 18.9bn in July on a YTD basis. New loans grew CNY 0.2bn to CNY 13.5bn, below the CNY…

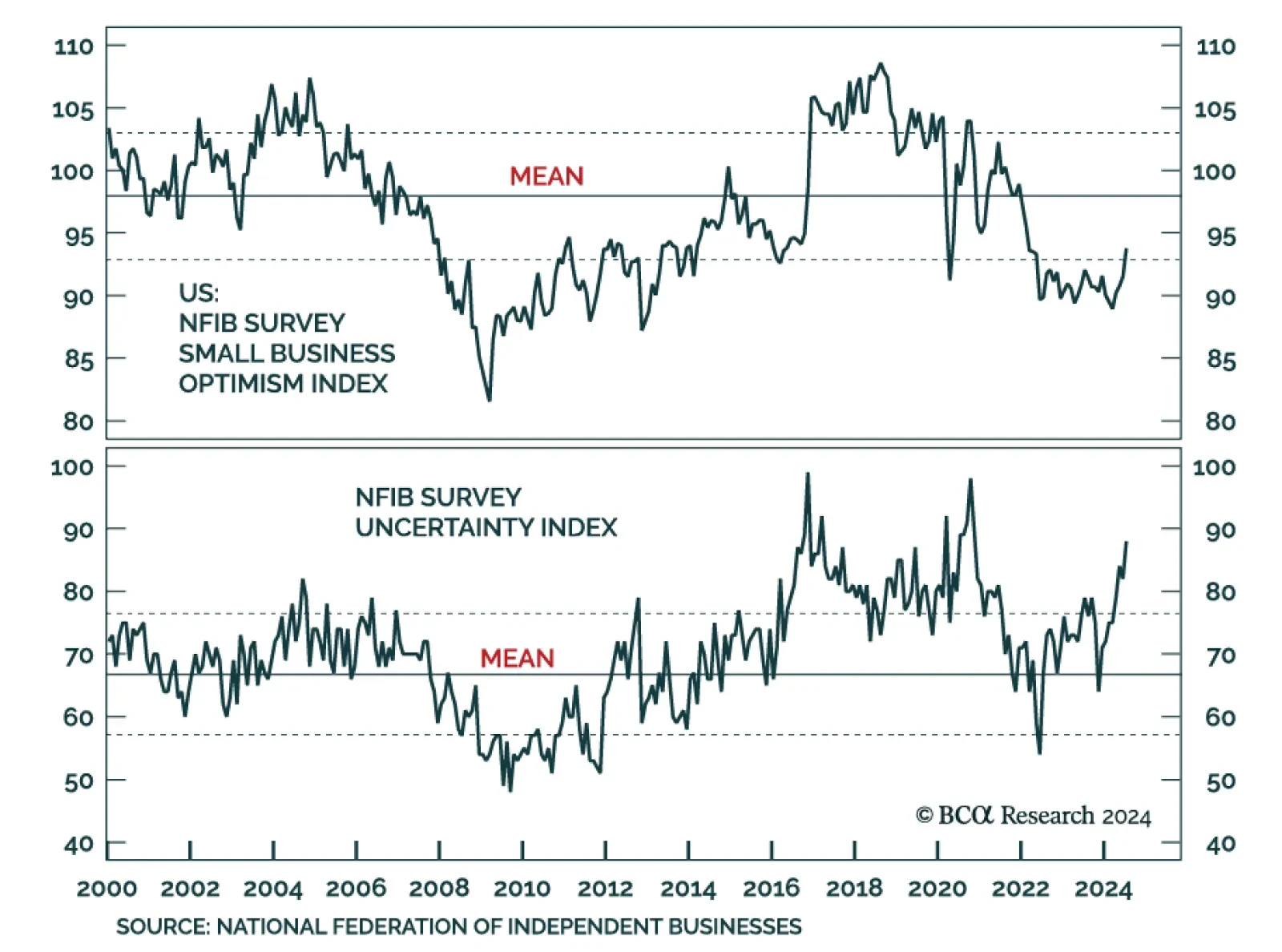

Tuesday morning’s NFIB Small Business Survey release surprised to the upside. The Small Business Optimism Index increased to 93.7 from 91.5, above expectations of remaining flat. The July reading was the highest since February 2022, the last release before…

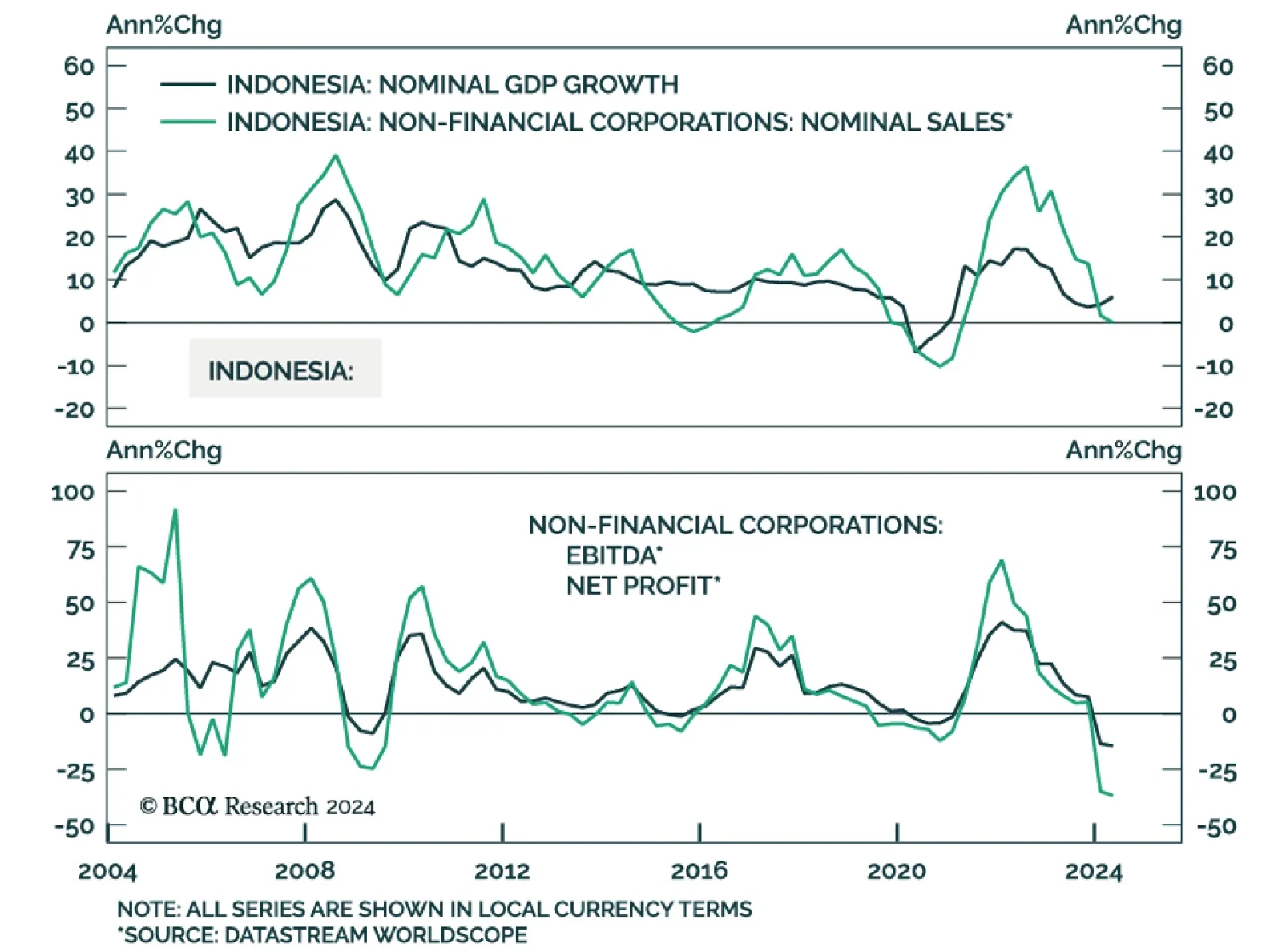

Indonesian stocks have sold off sharply and underperformed their EM and emerging Asian peers – both in local currency and in common currency terms – despite the nation’s 5.1% real GDP growth rate (the highest rate among G-20 countries, second only to India).…

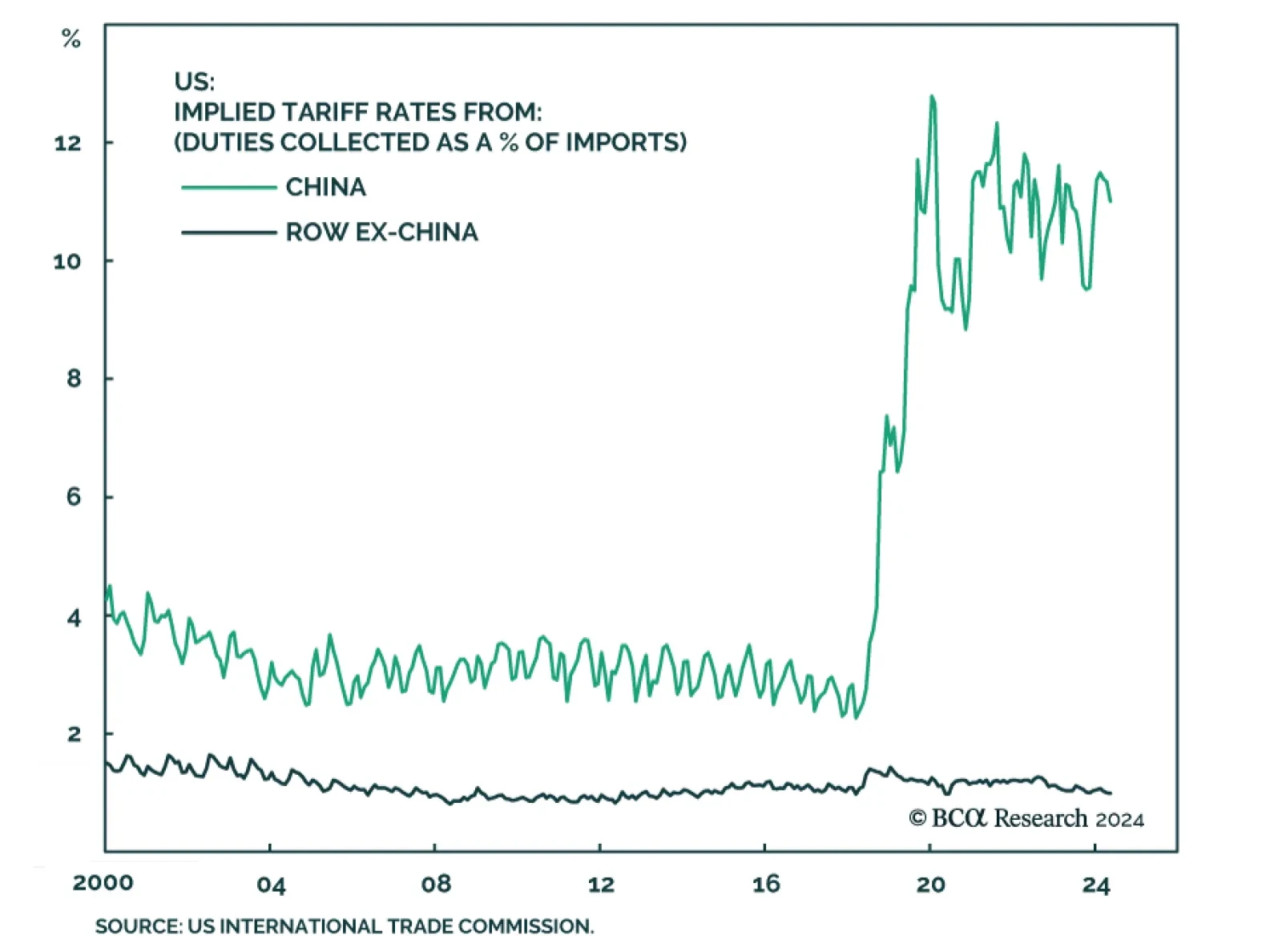

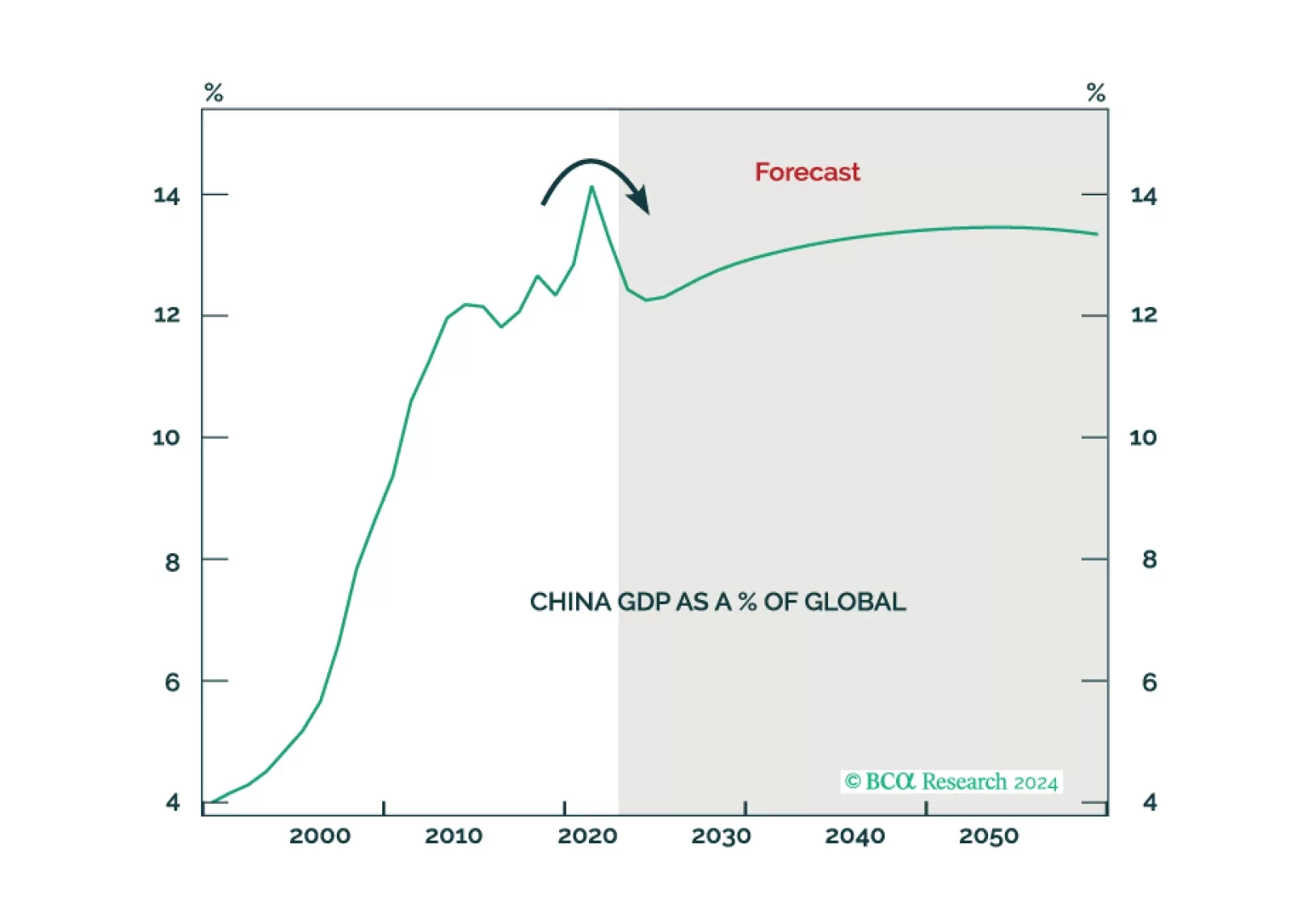

According to BCA Research’s Geopolitical Strategy service, Trump’s brand, legacy, and populist movement are based on the popular demand for a more hawkish US policy on trade and immigration. China has been the chief target. Investors have every reason to plan…

China missed the chance to change course on economic policy and now it faces rising social instability and western protectionism. This policy approach implies it is not afraid of escalating strategic conflicts in East Asia. Investors should continue to underweight Greater Chinese assets. Any US-China détente will come later rather than sooner.

Regular readers are familiar with our expectation that the stabilization in global growth this year will be fleeting. The US has been the main source of demand in this cycle. We view the latest string of US employment data as further evidence the US…

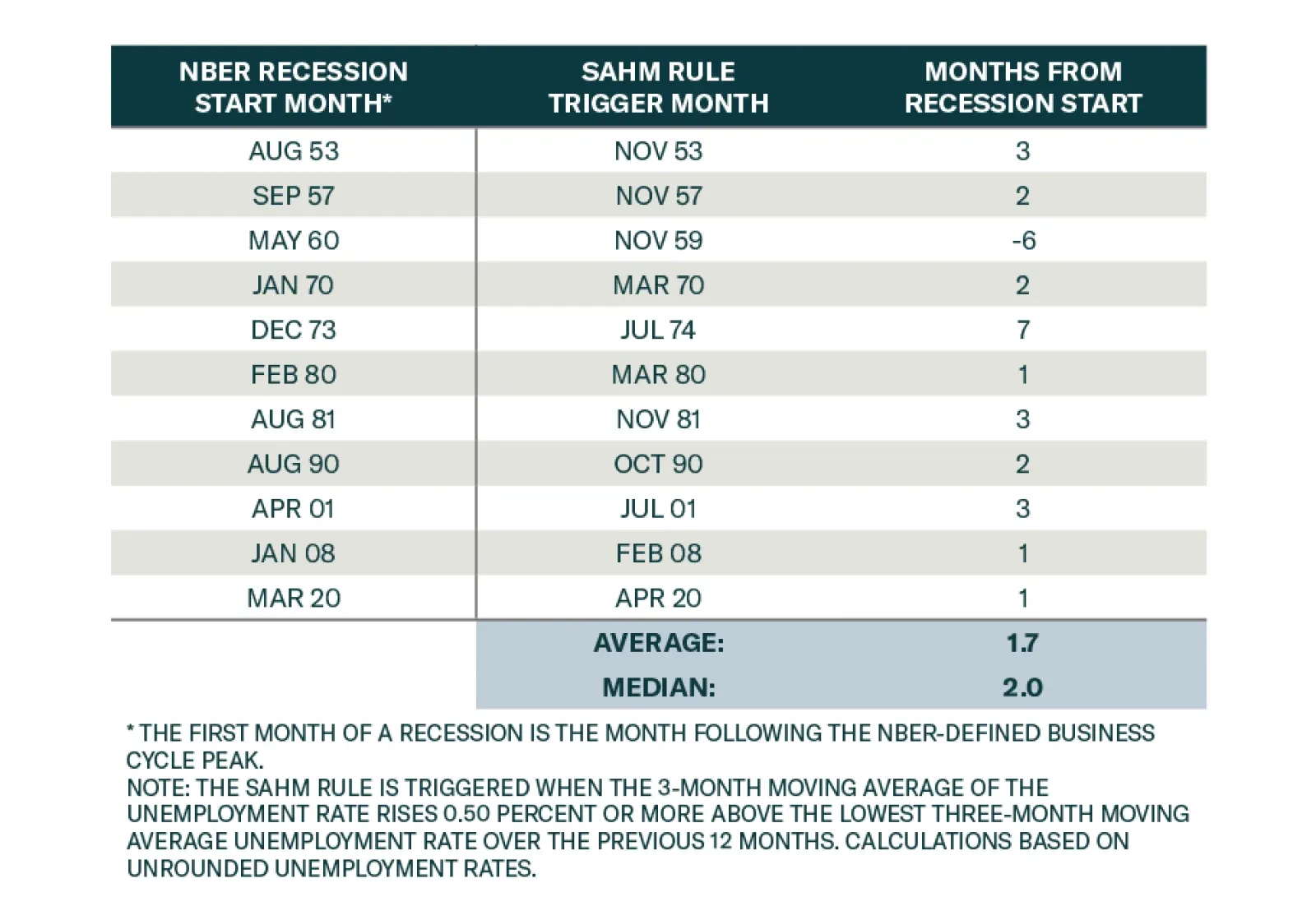

Market and economic observers have devoted a lot of attention to the Sahm Rule following July’s employment report, and whether or not it has been triggered. BCA’s analysis has highlighted that the overall direction of the labor market is far more important…

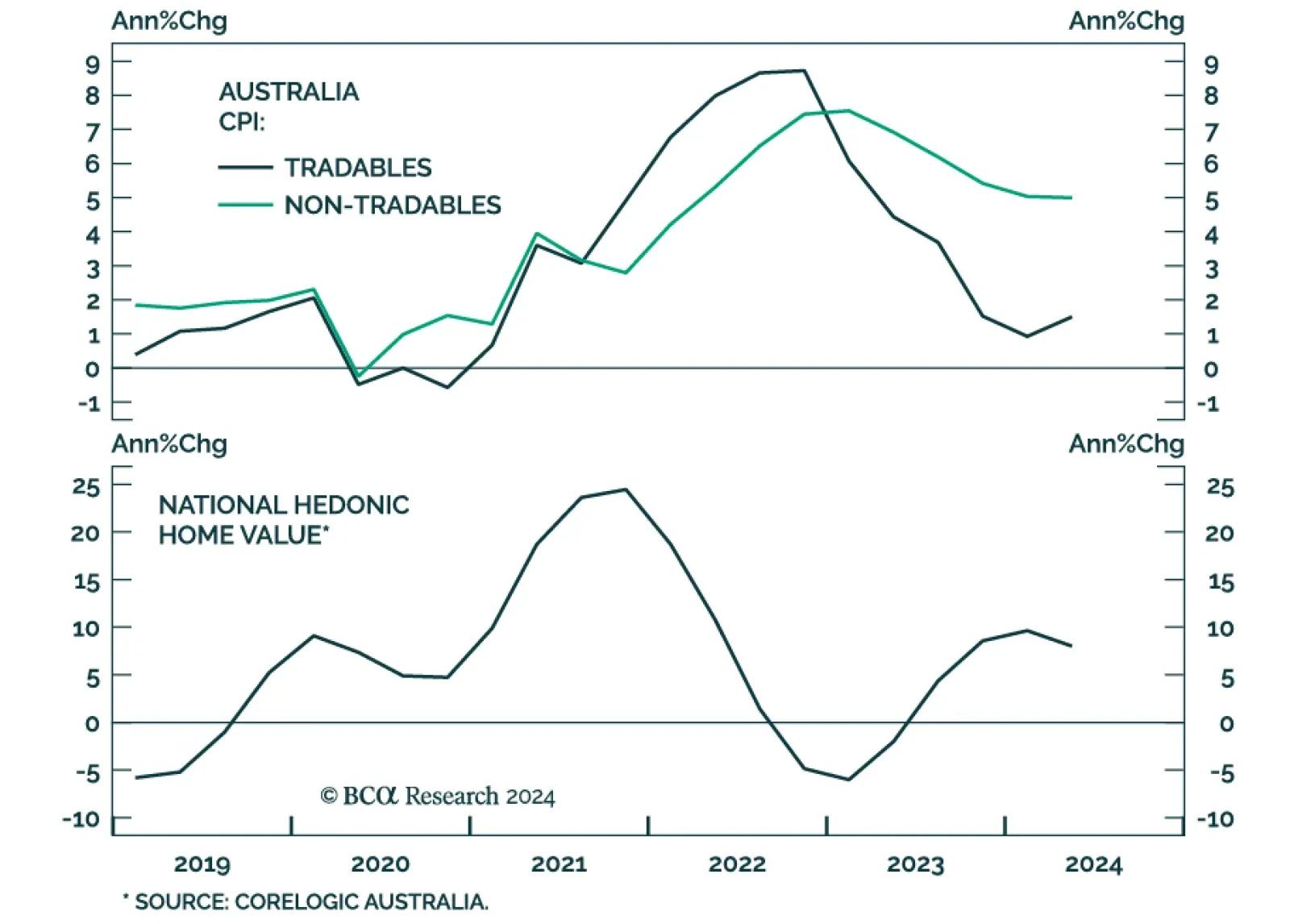

The RBA kept its cash rate unchanged at 4.35% in August, in line with expectations. However, it lifted its trimmed-mean inflation forecast to 3.5% y/y in Q4 2024 and to 2.9% by Q4 2025 (up from 3.4% and 2.8% in its May forecast, respectively). Inflation…

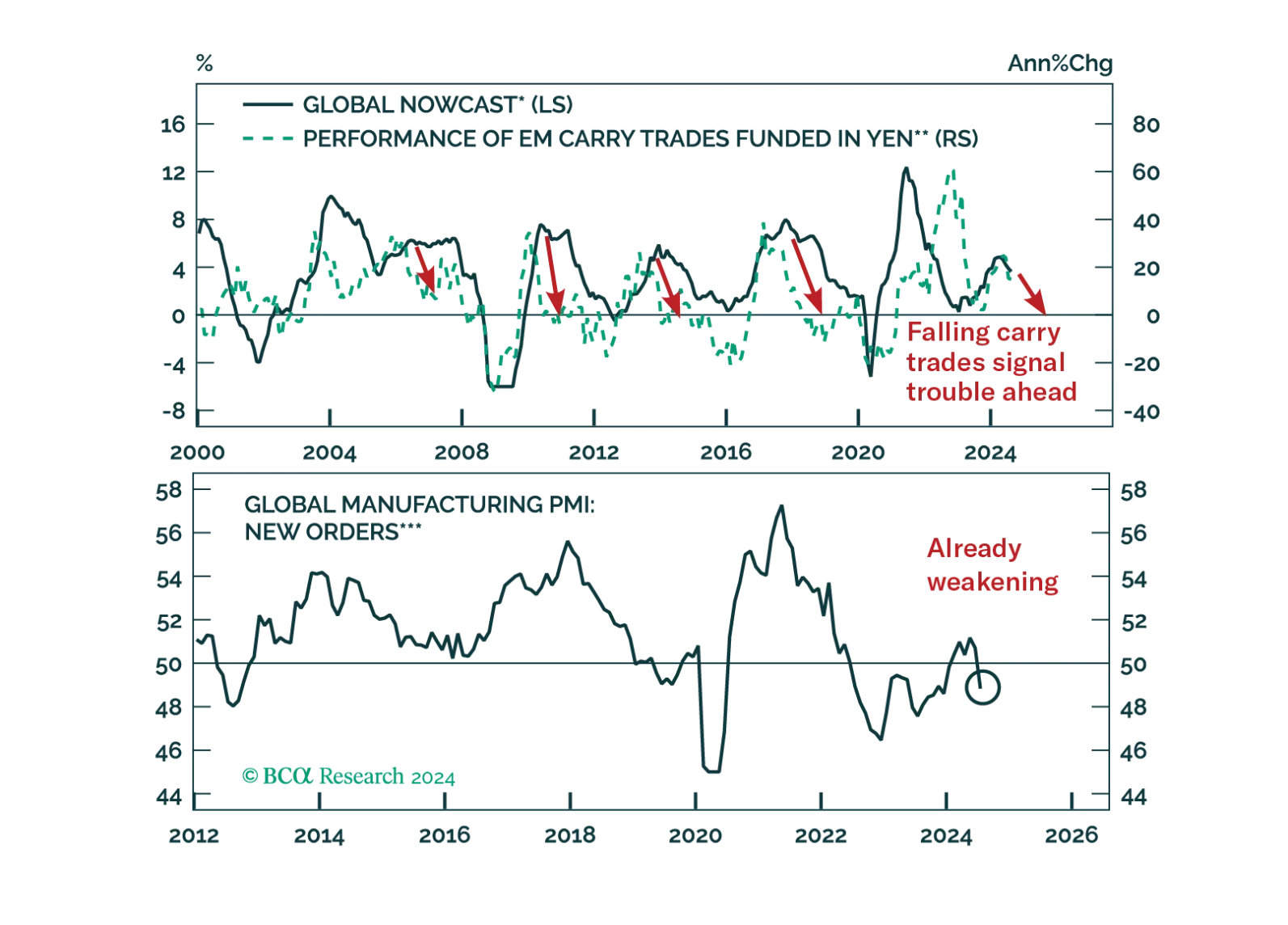

The unwind of yen carry trades caused violent tremors across the globe. Was this shock a one-off event or the prelude to more troubles?

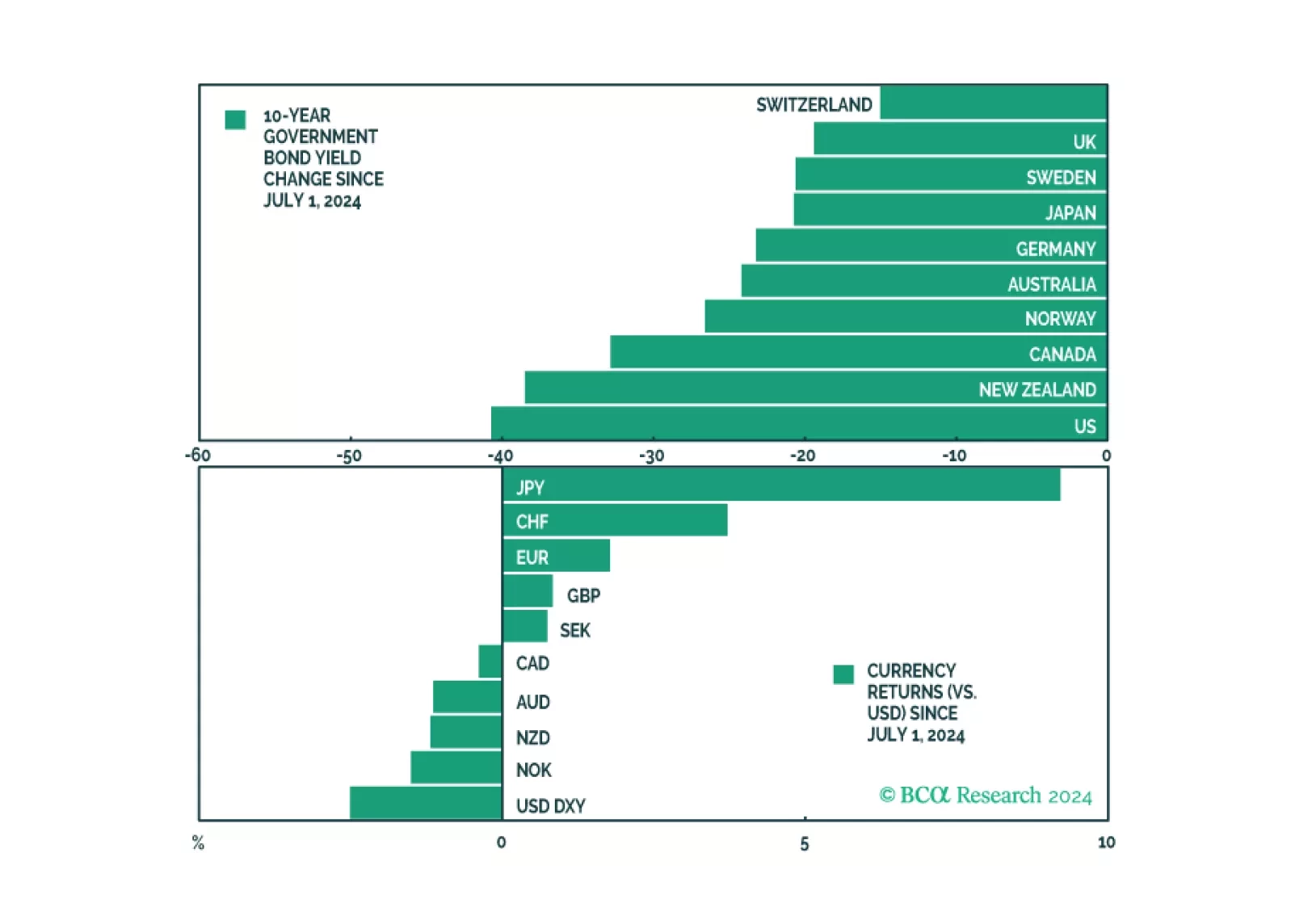

In this monthly review, we give our take on where bond yields and the dollar are headed. This is within the lens of revisiting our fundamental indicators.