Developed Countries

The latest release of the Canadian Labour Force Survey indicated further softening of the labor market in the Great White North. The economy experienced a net loss in total employment, shedding 1,400 jobs compared to market expectations of a net creation of…

ed on Thursday. The month-on-month contraction deepened to 1.6% in June from a contraction of 0.6% in May, revised down from the previously reported 0.2%, well below expectations of a modest 0.5% expansion. Indeed, Germany confronts material headwinds. …

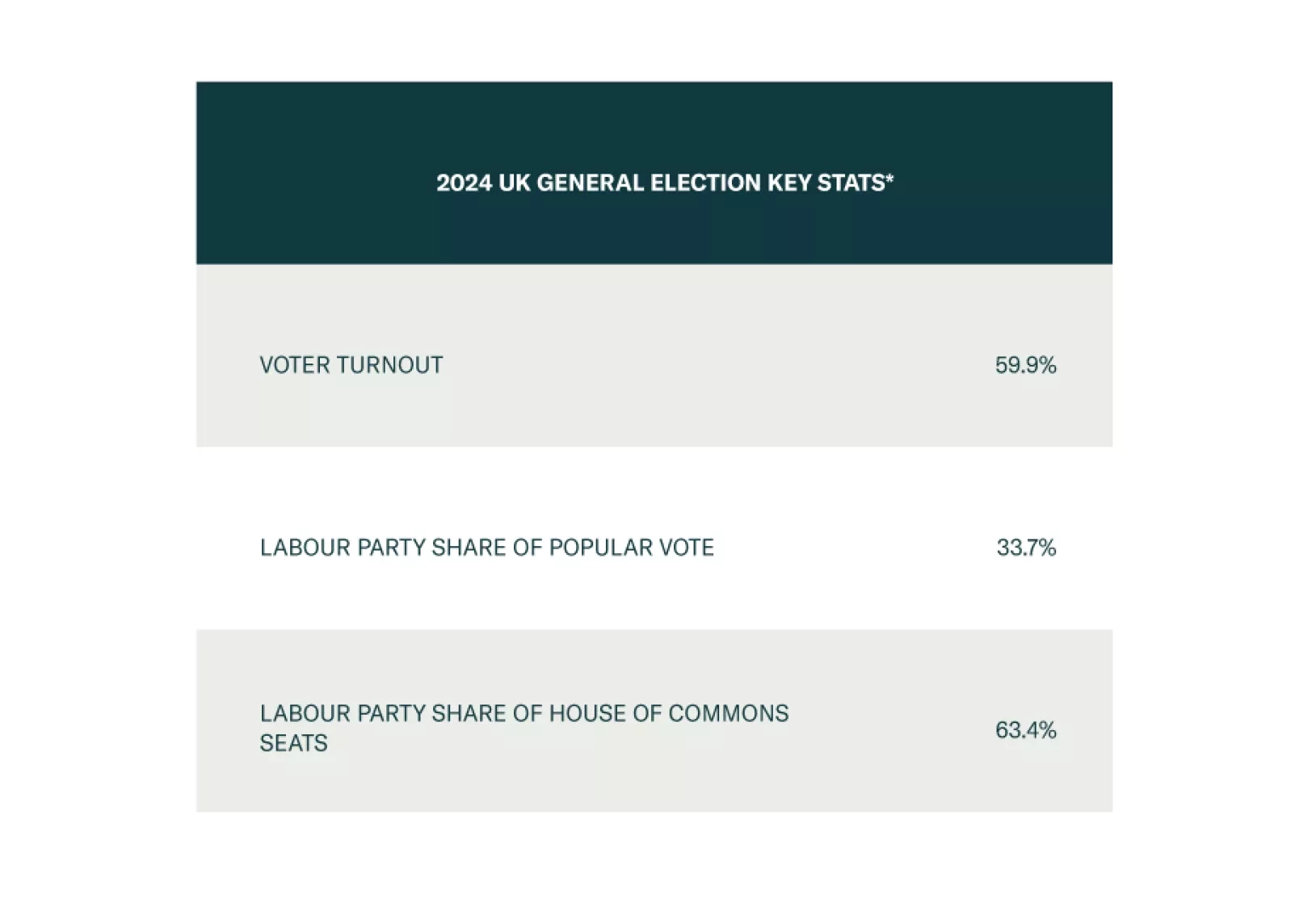

The Labour Party won the UK election, just as BCA Research’s Geopolitical Strategy service predicted back in 2022. However, this win is unlikely to rock the proverbial geopolitical boat. Popular enthusiasm for Sir Keir Starmer and his party is muted, and…

In this week's report, we review the impact of political developments, as well as incoming fundamental data, on our positioning.

Our labor market indicators have softened meaningfully during the past month but aren’t yet signaling an imminent recession. That said, the Fed can no longer ignore the labor market with the unemployment rate above 4% and rising.

The new Labour government will have flexibility to respond to macro shocks, which is positive for the UK in general, namely GBP-EUR, and also gilts in absolute terms. But over the long run, tax hikes will likely surprise to the upside, which poses a risk to corporate earnings.

Eurozone headline inflation slowed from 2.6% y/y to 2.5% in June. Germany, its largest economy, saw price pressures ease from 2.4% to 2.2%, below expectations of 2.3% (or from 2.8% to 2.5% on an EU-Harmonized basis). However, Euro Area core inflation…

The stabilization in global growth continued in June. The JPM Global Manufacturing PMI came in at 50.9, nearly in line with May’s 22-month high. However, international trade flows deteriorated notably. The new export orders component started contracting in…

The US unemployment rate stands at just 4.0% today following 27 consecutive sub-4% readings. Does this low unemployment rate guarantee a soft landing in the US economy? Our Global Investment Strategy (GIS) team’s base case is that the US economy will fall…

The US conventional 30-year mortgage rate climbed back above 7% in late June and drove a 2.6% weekly contraction in mortgage applications. The fixed-rate home affordability index sank to a nearly four-decade low. Housing is one of the most interest-rate…