Developed Countries

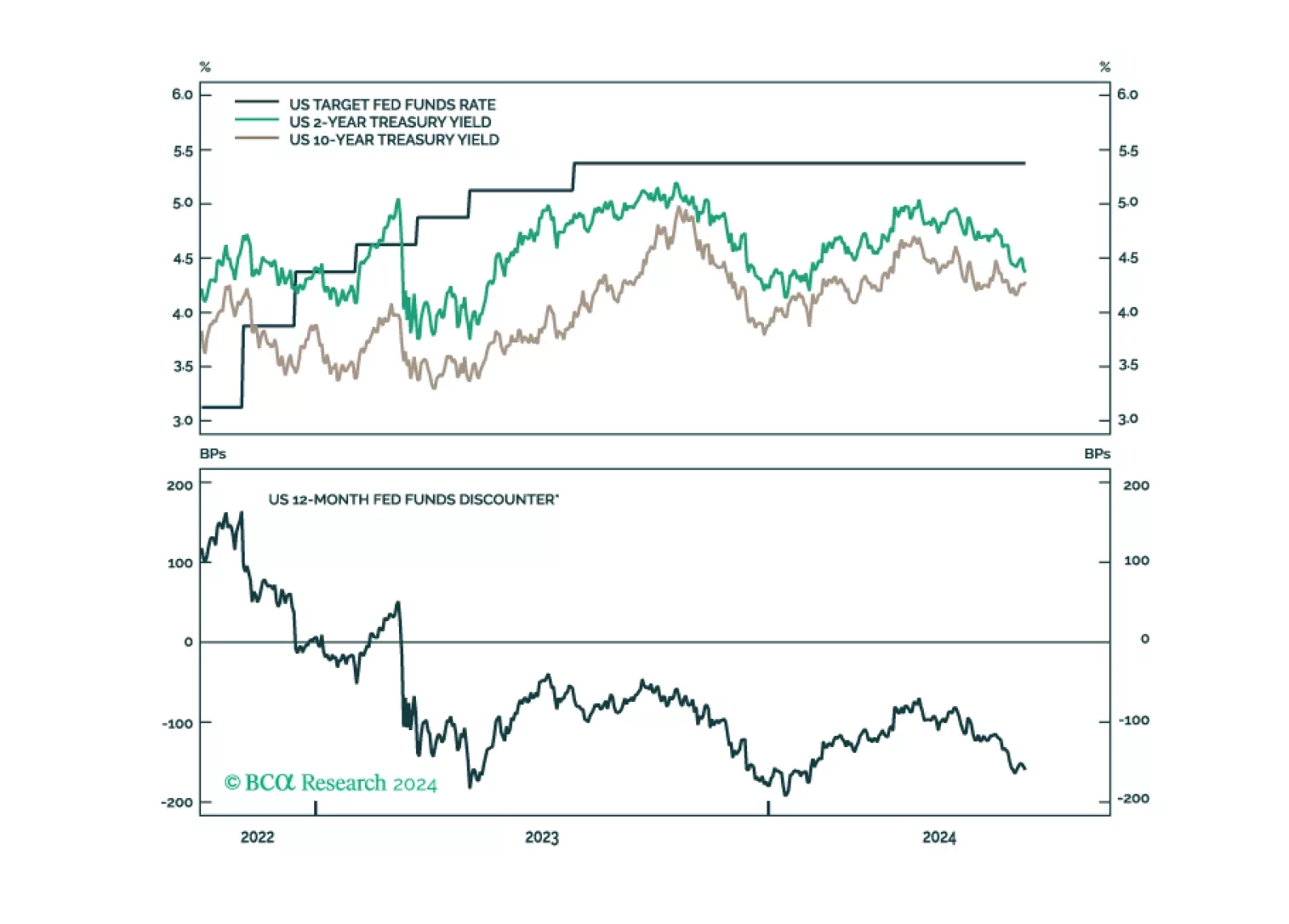

According to BCA Research’s US Bond Strategy service, it is time to increase portfolio duration from “at benchmark” to “above benchmark” on a 6-12 month horizon. Since February, our colleagues have been closely tracking three labor market indicators: the…

After this morning’s jobless claims number, we have now seen enough deterioration in our preferred labor market indicators to increase portfolio duration from “at benchmark” to “above benchmark”.

The Bank of Canada (BoC) reduced its policy rate by 25bps for the second meeting in a row on Wednesday. We highlighted in a recent Insight that the soft June inflation print and weakening labor market increased the odds of more aggressive BoC easing. …

According to BCA Research’s Emerging Markets Strategy service, there is little firepower left to sustain the US equity rally much further. The ratio of aggregate investable funds of US households and investment organizations/firms is at a record…

UK’s CPI growth stands right on the Bank of England’s (BoE) 2% target. However, services inflation remains sticky, growing at a constant 5.7% y/y in June. Moreover, the deceleration in wage growth remains insufficient to temper inflationary pressures in the…

The US economy has clearly cooled from its above-trend pace of growth in 2023. The consensus view among BCA Research’s strategists project that this deceleration will eventually culminate in a recession by year-end or early 2025. Our US Investment…

Total consumer credit rose by USD 11.4 billion in May (to USD 5,065 billion outstanding) from a slightly upwardly revised USD 6.5 billion increase in April, surpassing expectations of a smaller increase. Notably, revolving credit (which includes credit cards)…

The S&P 600 and Russell 2000 have outperformed the S&P 500 by close to 10% since July 9. Small caps typically outperform in the early stages of economic expansions when growth is accelerating, demand-driven inflation is rising and lending standards…

According to BCA Research’s European Investment Strategy service, the impact on global trade from another round of tariffs under a potential Trump administration is an emerging risk to Europe. The underperformance of European equities relative to US ones…

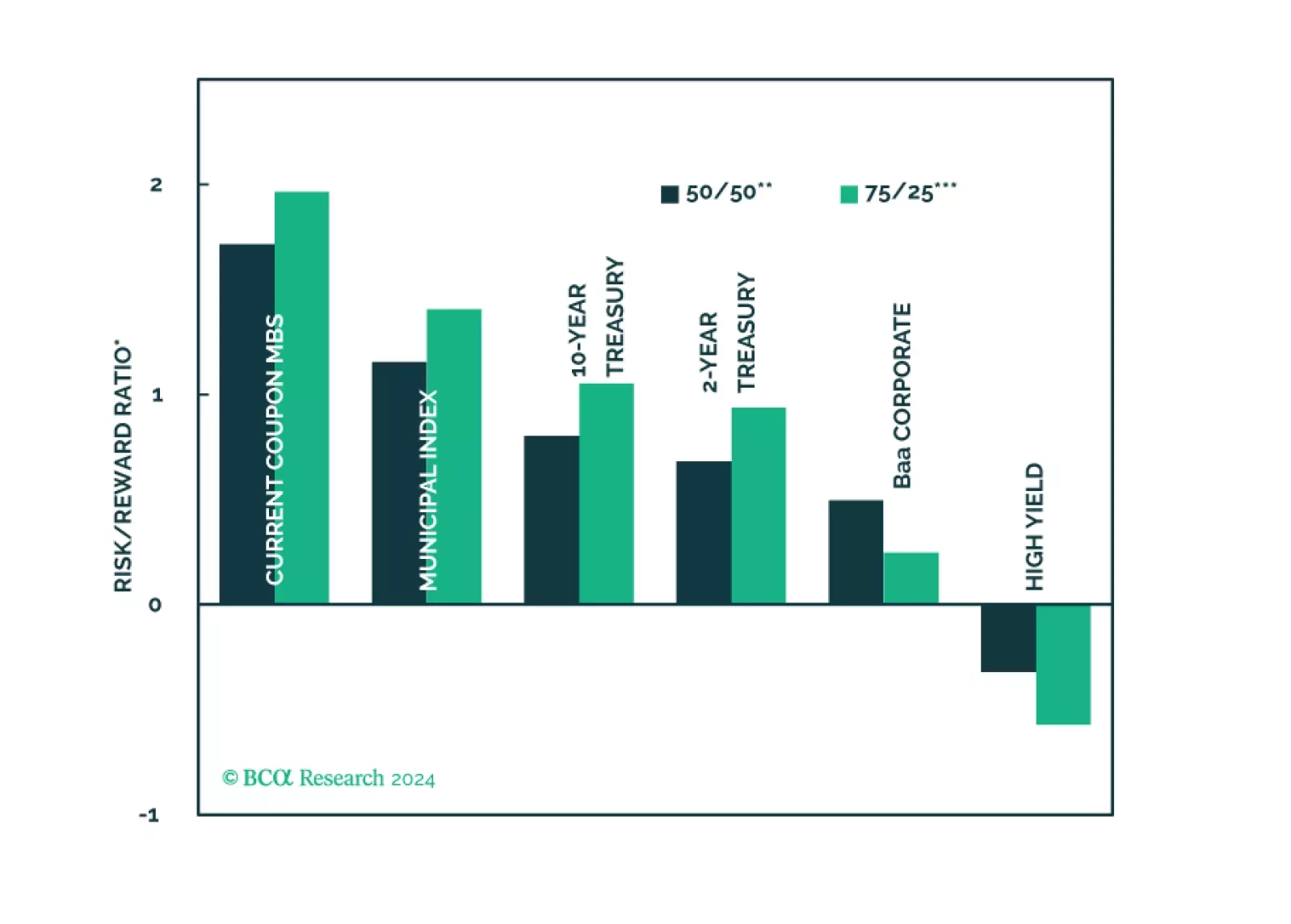

We calculate expected returns for several different US fixed income sectors with a focus on how municipal bonds stack up against the investment alternatives.