Developed Countries

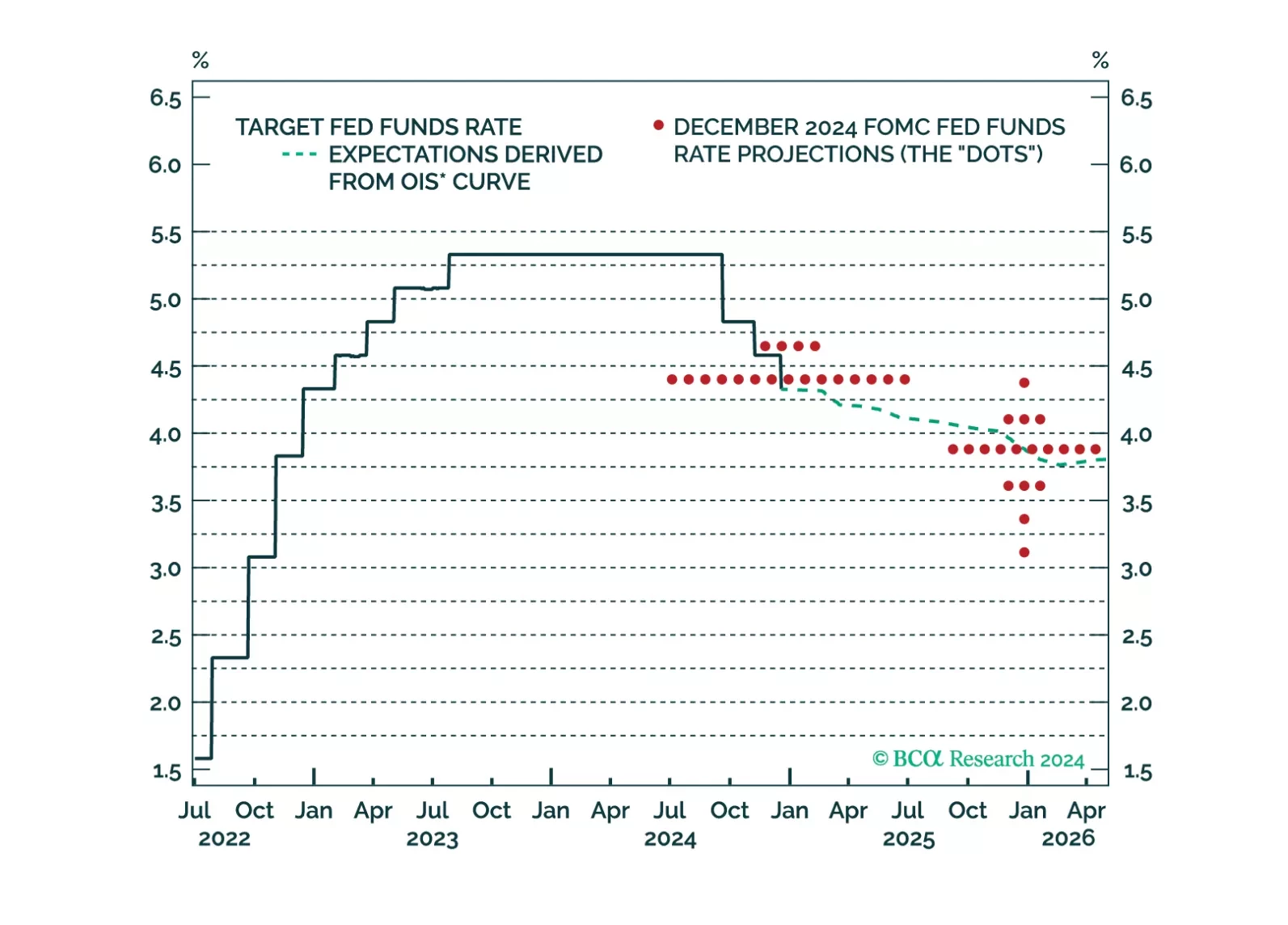

Our thoughts on this afternoon’s Fed decision and the bond market reaction.

November retail sales were roughly in line with expectations, with headline growth at 0.7% m/m vs. 0.4% in October. Vehicle sales were solid. Excluding auto and gas, sales rose a more modest 0.2% m/m, below expectations. The control group grew 0.4% m/m after…

European sentiment data was mixed. The December Ifo Business Climate index for Germany missed estimates and was down 1 point to 84.7 from November. The decrease came from its expectations component, which fell to 84.4 from 87.2. Meanwhile, the December ZEW…

The November Canadian CPI was slightly below estimates, declining to 1.9% y/y from 2.0%, below the BoC’s 2% target but within the 1%-to-3% range. The BoC’s favored core measures, median and trim, were flat at 2.6% and 2.7% respectively after revisions. CPI…

Our European Investment Strategy team published their annual outlook, outlining five key themes that will shape Europe’s economy and markets in 2025. Europe will enter a mild recession in H1 2025, but growth is expected to rebound quickly in the…

December flash PMIs for the core advanced economies showed service sector growth picking up. Manufacturing keeps contracting, and the US continues to outperform its DM peers. The US composite index beat expectations and increased to 56.6 from 54.9.…

The December Empire Manufacturing index missed expectations, slowing to 0.2 from 31.2 in November. Most cyclical components eased, suggesting last month's surge was a post-election blip. The new orders subcomponent decreased, leaving the new…

Our Chart Of The Week comes from Mathieu Savary, Chief Strategist of our European Investment Strategy service. Mathieu sees a dimming outlook for European industrial stocks in the near term.The sector has been one of the strongest performers in Europe this…

The post-COVID US recovery was different from previous cycles. Despite an ebullient economy, US consumers and firms have just not been feeling it, as reflected by the depressed signals from so-called soft, survey-based indicators. The main reason behind this…

Our Global Investment Strategy team released their 2025 outlook, adopting the unique perspective of time-travelers reporting from January 2, 2026. They foresee a challenging 2025, with the global economy slowing sharply and the NBER pinning the start date…