Developed Countries

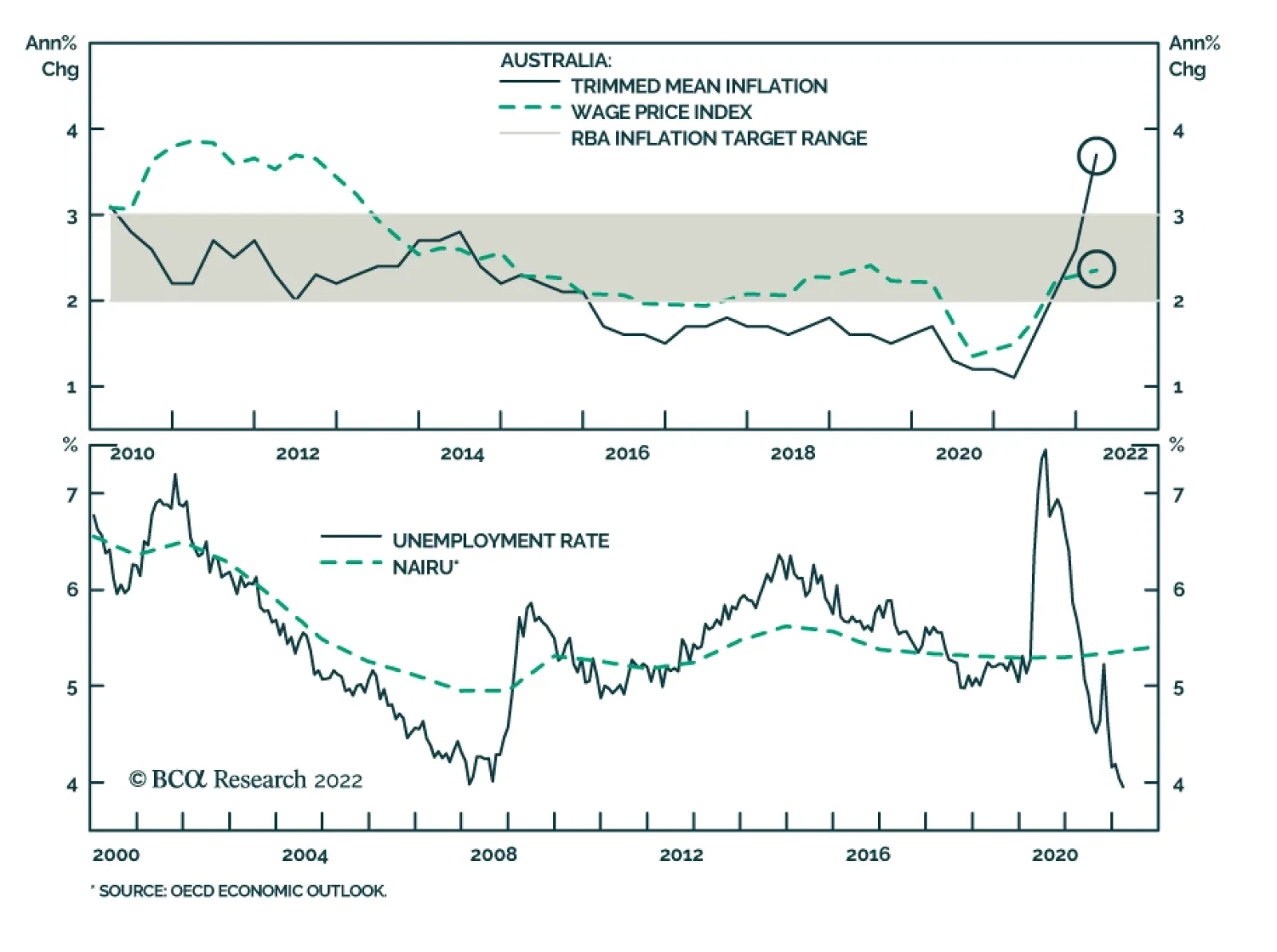

Wages in Australia rose 2.4% y/y (0.7% q/q) in Q1, slightly below expectations of 2.5% y/y (0.8% q/q). Administrative & support services, education & training as well as arts & recreational services industries drove wage growth over the quarter.…

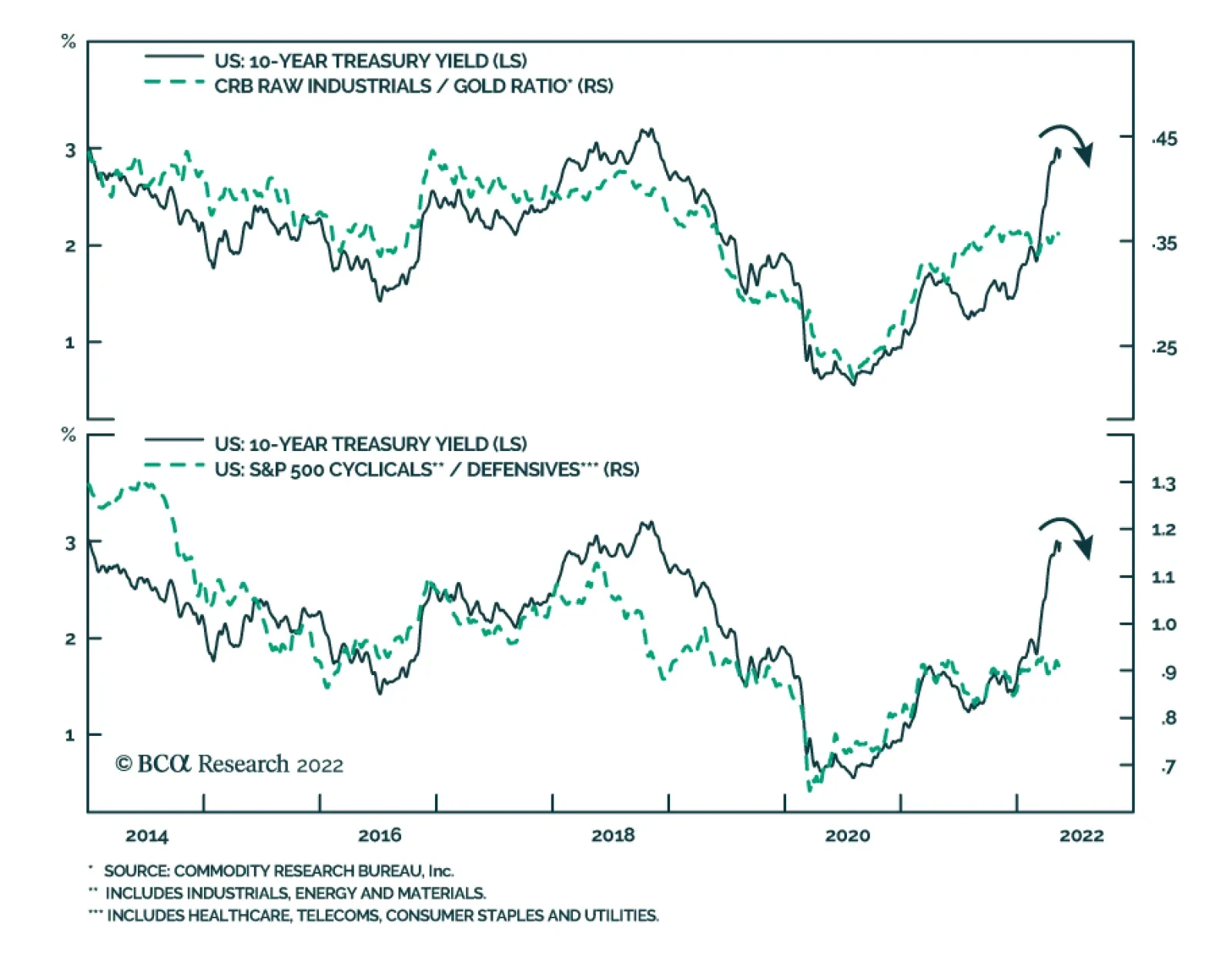

The 10-year Treasury yield briefly broke above the key psychological 3% level earlier this month. It last reached this level back in 2018, towards the end of the prior tightening cycle. A key difference, this time around is that the inflation component has…

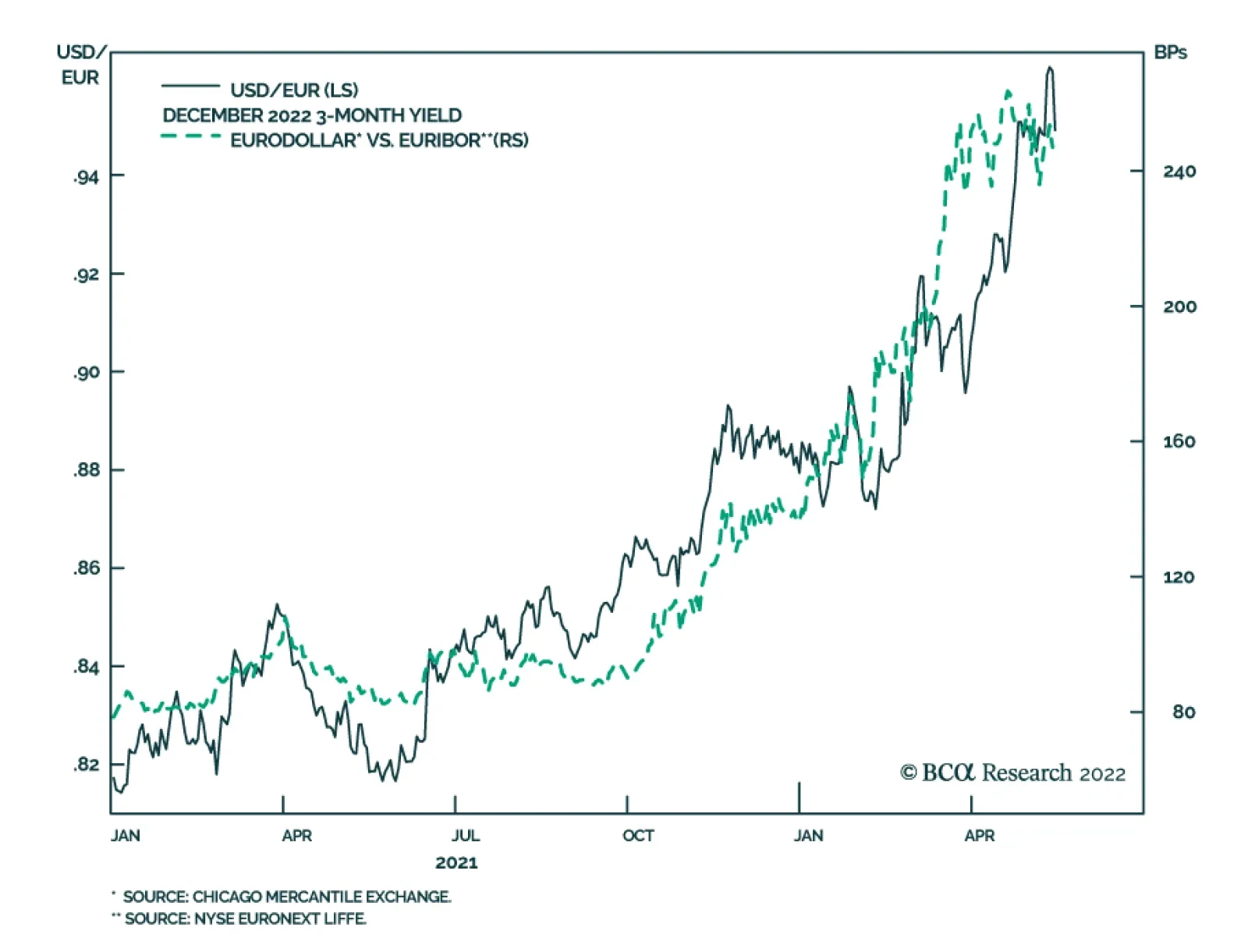

After breaking below 1.05 last week, EUR/USD has recently been strengthening. Interestingly, this recovery is occurring amid heightened geopolitical tensions and growth concerns. The odds of an EU embargo on Russian oil have increased and Sweden and Finland…

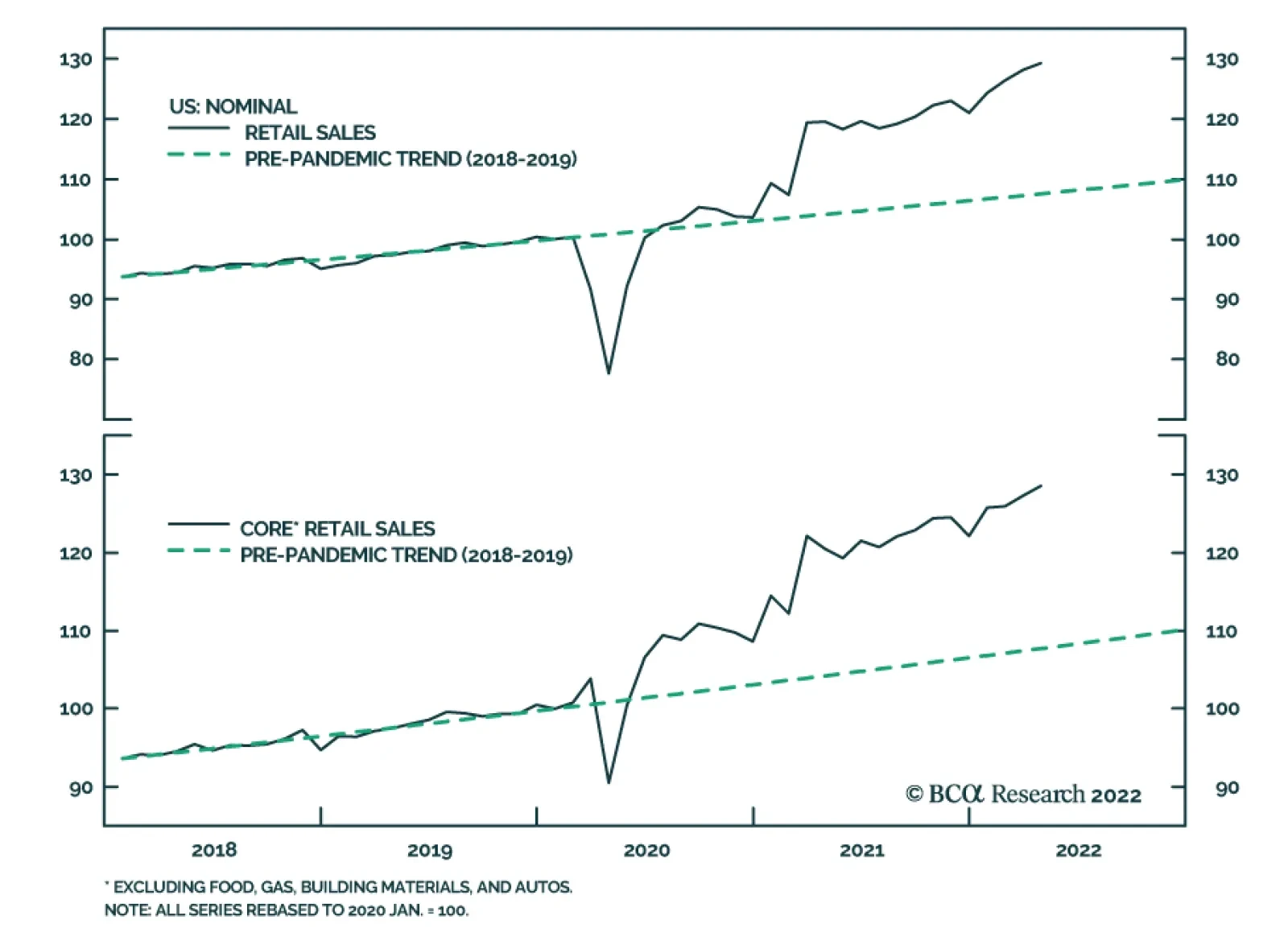

Retail sales and industrial production figures for April suggest that underlying economic fundamentals remain resilient in the US. Overall retail sales increased 0.9% m/m in April, following an upwardly revised 1.4% (from 0.5%) surge in March. Miscellaneous…

At a Tuesday appearance at a Wall Street Journal event, Fed Chair Jay Powell stated that the central bank will increase interest rates until “we feel we’re at a place where … we see inflation coming down.” He also noted that “if that involves moving past…

The NAHB Housing Market Index suggests that US homebuilder sentiment deteriorated sharply in May. The headline index dropped eight points to 69, the lowest level since June 2020. Notably, all three components of the index declined sharply. According to the…

Executive Summary Global inflation will peak sometime in the next few months, a process that has likely already begun in the US. This will give policymakers some breathing room to turn less hawkish, a more credible stance given softening global growth momentum and increased financial market volatility. Our Global Golden Rule of Bond Investing suggests that overall government bond returns should turn positive over the next year, but with widening divergences across countries for our base case scenarios. Projected government bond return expectations over the next 12 months look most attractive in Australia, Germany and the UK – where far too many rate hikes are priced in – compared to the US, where the Fed is more likely to follow through on most, but not all, discounted rate increases. Japan has the lowest expected returns, and the defensive properties of “low-beta” JGBs will be less necessary with global yield momentum set to peak in the latter half of 2022. Our Global Golden Rule Base Case Scenarios For The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Bottom Line: The return expectations over the next year stemming from our Global Golden Rule suggest the following country allocation recommendations in global government bond portfolios: maintain overweights in Australia, Germany and the UK, stay underweight the US and neutral Canada, but downgrade Japan to underweight. Feature Chart 1A Pause In The Global Bond Bear Market

A Pause In The Global Bond Bear Market

A Pause In The Global Bond Bear Market

Global bond markets may finally be showing signs of settling down after a painful period of rising yields and high volatility. Government bond yields across the developed economies have fallen substantially over the past week as equity and credit markets have sold off, in a typical risk-off response to increased concerns over global growth momentum. For example, benchmark 10-year government yields have fallen by -32bps both the US and UK, -25bps in Germany and -22bps in Canada since the cyclical intraday high was reached on May 9. These moves are modest in the context of the cyclical bond bear market, with the Bloomberg Global Treasury index still down -12.1% year-to-date and -14.4% on a year-over-year basis (Chart 1). That painful selloff has been driven by expectations of intense monetary tightening in response to surging global inflation. However, last week’s release of US Consumer Price Index data for April confirmed that US goods inflation has peaked, a trend that we expect to follow suit in other countries (Chart 2). That will leave inflation momentum, and eventual interest rate hikes, to be driven more by domestic services inflation that will prove to be less correlated across countries over the next 6-12 months (Chart 3). Chart 2Inflation & Rate Hike Expectations Have Become Correlated. . .

Inflation & Rate Hike Expectations Have Become Correlated. . .

Inflation & Rate Hike Expectations Have Become Correlated. . .

Chart 3. . .Making Our Global Golden Rule All About Inflation

. . .Making Our Global Golden Rule All About Inflation

. . .Making Our Global Golden Rule All About Inflation

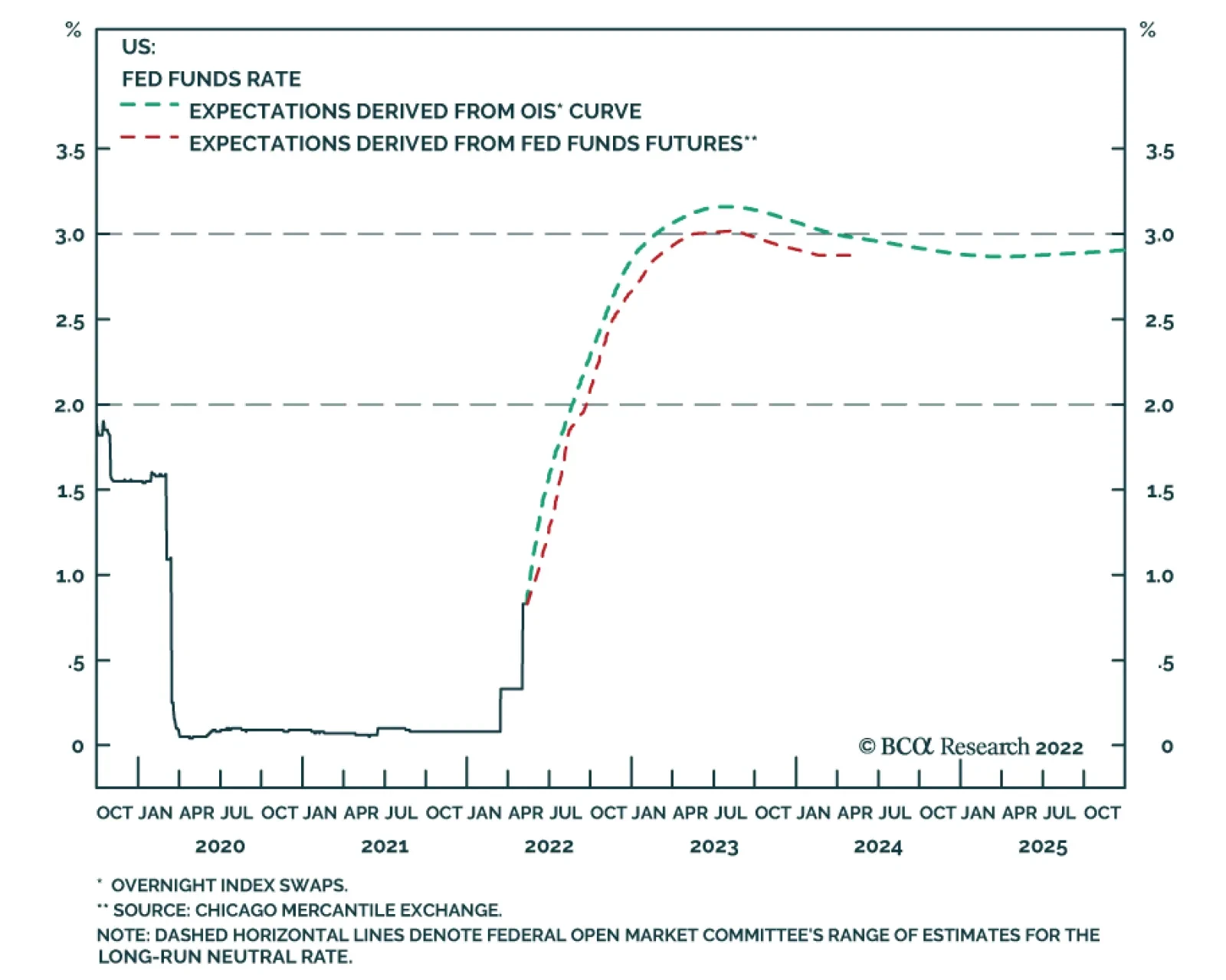

With that in mind, we revisit our framework for linking government bond returns to monetary policy outcomes versus expectations, the Global Golden Rule of Bond Investing. A Brief Overview Of The Global Golden Rule In September 2018, we published a Special Report introducing a government bond return forecasting methodology called the “Global Golden Rule.” This was an extension of a framework introduced by our sister service, US Bond Strategy, that links US Treasury returns (versus cash) to changes in the fed funds rate that were not already discounted in the US Overnight Index Swap (OIS) curve.1 The historical results convincingly showed that investors who "get the Fed right" by making correct bets on changes in the funds rate versus expectations were very likely to make the right call on the direction of Treasury yields and Treasury returns. Related Report Global Fixed Income StrategyRevisiting Our Global Golden Rule Of Bond Investing We discovered that relationship also held in other developed market countries. This gave us a framework to help project expected global bond returns simply based on a view for future central bank interest rate moves versus market expectations.2 Specific details on the calculation of the Global Golden Rule can be found in those original 2018 papers. In the following pages, we present the latest results of the Global Golden Rule for the US, Canada, Australia, the UK, the euro area and Japan. The set-up for the chart shown for each country is the same. We show the 12-month policy rate “surprise”, defined as the actual change in the central bank policy rate over the preceding 12-months versus the expected 12-month change in the policy rate from a year earlier extracted from OIS curves (a.k.a. our 12-month discounters). We then compare the 12-month policy rate surprise to the annual excess return over cash (treasury bills) of the Bloomberg government bond index for each country. We also show the 12-month policy rate surprise versus the 12-month change in the government bond index yield. The very strong historical correlation between those latter two series is the backbone of the Global Golden Rule framework. After that, we present tables showing expected yield changes and excess returns for various maturity points, as well as the overall government bond index, derived from the Global Golden Rule regressions. The expected change in yield is derived from regressions on the policy rate surprises, with different estimations done for each maturity point. In the tables, we show the results for different scenarios for changes in policy rates. For example, the row in the return tables labeled “+25bps” would show the expected yield changes and excess returns if the central bank for that particular country lifts the policy interest rate by +25bps over the next 12 months. Showing these scenarios allows us to pick the one that most closely correlates to our own expectation for central bank actions, translating that into government bond return expectations. Global Golden Rule: US Chart 4Risk/Reward Favors Less UST-Bearish Fed'Surprises'

Risk/Reward Favors Less UST-Bearish Fed'Surprises'

Risk/Reward Favors Less UST-Bearish Fed'Surprises'

US Treasuries have delivered a painful loss of -7.8% versus cash over 12 months. Bearish outcomes of such magnitude were last seen during 1994 and 1999 when the Fed was aggressively lifting the funds rate. The Fed delivered a smaller hawkish surprise over the past year than those 1990s episodes, with a trailing 12-month policy rate surprise of -72bps. Thus, the Golden Rule underestimated losses realized by US Treasuries, as US bond yields moved to price in far more Fed tightening than what was expected one year ago. The US OIS curve now discounts +229bps of rate hikes over the next 12 months, taking the fed funds rate to 3.3% (Chart 4). That is a more aggressive profile than was laid out in the March 2022 Fed “dots”, where the median FOMC member projection called for the funds rate to climb to 2.8% in 2023. That means there is less scope for Fed rate hikes to surprise versus market expectations that are already very hawkish, at a time when US growth and inflation momentum is rolling over. Our base case calls for the Fed to deliver +200bps of rate increases over the next year, +50bps at the next two policy meetings followed by +25bps at the subsequent four meetings. That outcome produces a Golden Rule forecast of the overall US Treasury index yield falling -13bps, generating a total return of +3.73% (Tables 1 & 2). Table 1US: Government Bond Index Total Return Forecasts Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Table 2US: Expected Changes In Treasury Yields Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Global Golden Rule: Canada Chart 5Canadian Bonds Selloff After A Hawkish BoC

Canadian Bonds Selloff After A Hawkish BoC

Canadian Bonds Selloff After A Hawkish BoC

Canadian government bonds have sold off hard over the past 12 months, delivering an excess return over cash of -7.5% (Chart 5). That loss reflects the Bank of Canada’s (BoC) hawkish turn, but is a less severe outcome compared to other developed economy government bond markets that saw a major repricing of rate hike expectations like the US and Australia. Losses in the Canadian government bond market were consistent with the +34bps of hawkish surprises delivered by the BoC, which tightened by +75bps on a 12-month basis versus the +41bps expected by markets in May 2021. Rate expectations are highly aggressive on a forward basis. The Canadian OIS curve now discounts 210bps of interest rate increases over the next 12 months. However, high household debt in Canada, fueled by a relentlessly expanding housing bubble, will limit the ability of the BoC to match the Fed’s rate hikes over the next 6-12 months. Higher debt levels also imply a lower nominal neutral rate of interest, as the BoC has less room to hike before debt servicing costs become overly burdensome for overleveraged Canadian consumers. Our base case is that the BoC will deliver +150bps of tightening over the next 12 months. This produces a Golden Rule forecast of a decline in the overall Canadian government bond index yield of -17bps, delivering a projected total return of 4.52% (Tables 3 & 4). Table 3Canada: Government Bond Index Total Return Forecasts Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Table 4Canada: Expected Changes In Government Bond Yields Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Global Golden Rule: Australia Chart 6Aggressive Rate Hike Expectations On A Forward Basis For Australia

Aggressive Rate Hike Expectations On A Forward Basis For Australia

Aggressive Rate Hike Expectations On A Forward Basis For Australia

Australian government bonds have delivered a negative excess return over cash of -9.6% over the past year (Chart 6). This is the biggest sell-off among all the countries covered in our Global Golden Rule framework. The magnitude of those realized losses far exceeded what would have been predicted by the Golden Rule a year ago, with the Reserve Bank of Australia (RBA) delivering only a modest hawkish surprise. An unexpectedly high Australian headline inflation print of 5.1% in Q1 of this year led the RBA to deliver a surprise +25bps rate hike in April. This created a mild hawkish policy rate surprise of -17bps over the past 12 months, as only +8bps of tightening had been discounted in the Australian OIS curve in May 2021. The Australian OIS curve is now discounting 292bps of rate hikes over the next year, taking the cash rate to just over 3% - a level last seen in 2013 when the neutral rate in Australia was much higher by the RBA’s own reckoning. The RBA appears confident in the Australian economy, forecasting the unemployment rate to reach a 50-year low around 3.5% in 2023. However, we believe the RBA will be more measured in its pace of rate increases over the next year than markets expect, as global traded goods inflation cools and Australian wages are still not overheating. According to the Golden Rule projections, our base case of +150bps of tightening will produce a decline in Australian government bond index yield of -92bps, delivering a projected total return of 9.29% (Tables 5 & 6). Table 5Australia: Government Bond Index Total Return Forecasts Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Table 6Australia: Expected Changes In Government Bond Yields Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Global Golden Rule: UK Chart 7The BoE Will Hike Less Than Markets Expect

The BoE Will Hike Less Than Markets Expect

The BoE Will Hike Less Than Markets Expect

UK government bonds have gotten hit hard over the past year, delivering a negative excess return over cash of -7.9% - one of the worst performances seen over the past quarter century (Chart 7). The size of that loss was in line with the Global Golden Rule forecasts, given the magnitude of the rate shock seen in the UK. The Bank of England (BoE) hiked rates by 90bps over the past 12 months, which was a hawkish surprise of -79bps compared to what was discounted one year earlier. The UK OIS curve is now priced for another +139bps of rate hikes over the next year. This would take the BoE’s Bank Rate to 2.4%, a level that would push the UK unemployment rate up by two percentage points and lower UK inflation to below 2% within the next 2-3 years, according to the BoE’s own forecasting models. As we discussed in our report last week, where we upgraded our stance on UK Gilts to overweight, the neutral level of UK policy rates is between 1.5-2%, at best, with UK potential growth barely above 1%. Thus, markets are already pricing in a very restrictive monetary policy stance from the BoE that is unlikely to be fully delivered before UK growth and inflation decline sharply. Our base case calls for the BoE to deliver only another +75bps of hikes over the next year, which will produce a fall in the UK government bond index yield of -21bps and a total return of 4.12% (Tables 7 & 8). Table 7UK: Government Bond Index Total Return Forecasts Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Table 8UK: Expected Changes In Gilt Yields Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Global Golden Rule: Germany Chart 8German Bunds Stand To Gain From An ECB Dovish Surprise

German Bunds Stand To Gain From An ECB Dovish Surprise

German Bunds Stand To Gain From An ECB Dovish Surprise

German government bonds suffered major losses over the past year, underperforming cash by -8.5% over the past year. We saw no policy surprise from the European Central Bank (ECB) over that time relative to market expectations (Chart 8). The dramatic sell-off instead reflected surging expectations of future tightening as the euro area faces an energy-driven inflation spike. The trailing 12-month policy rate surprise for Germany (and the overall euro area) remains stuck near zero. However, markets now expect a very aggressive move by the ECB, discounting a full +156bps of tightening over the next 12 months. This would push the ECB’s main refinancing rate to levels last seen in the disastrous tightening cycle during the 2011 European debt crisis. As argued by our colleagues at BCA Research European Investment Strategy, the euro area is heading into a growth slowdown and energy inflation looks set to peak. Even if the hawks are able to sway the ECB Governing Council to begin hiking rates this summer, the slowing trajectory of growth and inflation make it highly unlikely that the ECB will deliver the full amount of tightening currently discounted. Our base case is that the ECB will deliver only +50bps of tightening over the next 12 months, enough to push the deposit rate out of negative territory to 0%. As shown in Tables 9 & 10, this is consistent with the Germany government bond index yield falling -55bps, delivering an index return of 5.07% over a 12-month horizon. Table 9Germany: Government Bond Index Total Return Forecasts Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Table 10Germany: Expected Changes In Bund Yields Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Global Golden Rule: Japan Chart 9The Upside On A BoJ Dovish Surprise Is Limited

The Upside On A BoJ Dovish Surprise Is Limited

The Upside On A BoJ Dovish Surprise Is Limited

Japanese government bonds (JGBs) have delivered an excess return versus cash of -1.8% over the past twelve months (Chart 9). The policy rate surprise was flat as the Bank of Japan (BoJ) kept the policy rate unchanged at -0.1%. Admittedly, the Golden Rule framework is poorly suited to project Japanese bond returns. The BoJ has been unable to lift policy rates for many years, while instituting yield curve control on 10-year JGBs since 2016 to anchor yields near zero. With no variability on policy rates or bond yields, a methodology that links bond returns to unexpected policy interest rate changes will have poor predictive power. However, rates traders are making some attempt to challenge the BoJ’s ultra-dovish posture. The Japan OIS curve now discounts +9bps of tightening, approximately enough to push the policy rate to zero, over the next 12 months. With the yen weakening rapidly and the cost of imported energy elevated, consumer price inflation in Tokyo (excluding fresh food) hit the BoJ’s 2% target in April. However, as evidenced in the minutes of the March BoJ meeting, policymakers see a sustainable inflation overshoot as unlikely. Our base case is the “Flat” scenarios shown in Tables 11 & 12, with the BoJ keeping policy rates unchanged for the next twelve months and delivering a slight dovish surprise. That generates a Golden Rule forecast of a -6bps fall in the Japanese government bond index yield, with a total return projection of 0.87%. Table 11Japan: Government Bond Index Total Return Forecasts Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Table 12Japan: Expected Changes In JGB Yields Over The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Investment Implications Of The Global Golden Rule Projections For all the countries discussed above, our base case calls for the respective central banks to deliver less tightening than markets are discounting over the next year. This suggests that government bonds should be expected to deliver positive returns versus cash, even as we expect multiple rate increases from all central banks except the BoJ. While this could argue for an above-benchmark duration stance at the overall global level, we prefer to translate the Global Golden Rule results via country allocations – as we have greater conviction on relative central bank moves in the current high inflation environment – while keeping overall global duration exposure at neutral. The return outcomes for our base case scenarios for the six countries in our Global Golden Rule framework are presented in Table 13. We show the expected returns both in local currency and hedged into US dollars, the latter allowing a comparison in common currency terms. In our base case scenarios, we expect Australian and German government bonds to deliver the strongest performance over the next year, followed by the UK, Canada, the US and Japan. Table 13Our Global Golden Rule Base Case Scenarios For The Next 12 Months

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Chart 10Downgrade 'Defensive' Low-Yield-Beta JGBs To Underweight

Downgrade 'Defensive' Low-Yield-Beta JGBs To Underweight

Downgrade 'Defensive' Low-Yield-Beta JGBs To Underweight

Our UK upgrade to overweight last week was a change to our strategic call on Gilts. Based on the results from our Global Golden Rule update, increased exposure to UK Gilts should be “funded” in a global bond portfolio by reducing exposure to Japan, with JGBs expected to deliver the weakest returns. Cutting JGB exposure also fits with the signal from our Global Duration Indicator, which is heralding a peak in global bond yield momentum in the latter half of 2022 (Chart 10). JGBs are typically a good “defensive” overweight country allocation in an environment of rising global bond yields. Persistently low Japanese inflation prevents the BoJ from credibly signaling rate hikes when other central banks like the Fed are lifting rates in response to stronger growth or overshooting inflation as is currently the case. The relative performance of Japan versus the Bloomberg Global Treasury benchmark index (in USD-hedged terms) is highly correlated to the year-over-year momentum of the overall level of global bond yields. With our Duration Indicator signaling a peak in yield momentum, we expect JGBs, which continue to exhibit a very low “beta” to changes in global bond yields, to underperform. Thus, this week we are downgrading our strategic allocation to Japan from overweight (4 out of 5) to underweight (2 out of 5). We view this as an offsetting recommendation to our UK upgrade from last week, while leaving our other country allocations unchanged. The result is that our country recommendations now line up with the expected returns from our Global Golden Rule, as can be seen in Table 13. That includes leaving the recommended US Treasury exposure at underweight, as we expect the Fed to deliver the smallest dovish surprise out of the central banks discussed in this report. We are adding both of the view changes made over the past two weeks, upgrading the UK and downgrading Japan, to our model bond portfolio as seen on pages 20-21. Bottom Line: Our Global Golden Rule suggests that developed market government bonds are expected to deliver positive returns over the next year as softening inflation momentum leads central banks to not fully deliver discounted rate hikes. Return expectations look most attractive in Australia, Germany and the UK, especially compared to the US and Japan. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Shakti Sharma Senior Analyst ShaktiS@bcaresearch.com Deborah Acri Research Associate deborah.acri@bcaresearch.com Footnotes 1 Please see BCA Research US Bond Strategy Special Report, "The Golden Rule Of Bond Investing", dated July 24, 2018, available at usbs.bcarearch.com. 2 Please see BCA Research Global Fixed Income Strategy Special Report, "The Global Golden Rule Of Bond Investing", dated September 25, 2018, available at gfis.bcaresearch.com. GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index Global Fixed Income - Strategic Recommendations* Cyclical Recommendations (6-18 Months)

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Updating Our Global Golden Rule Of Bond Investing As Inflation Momentum Peaks

Tactical Overlay Trades

Results from the May New York Fed Empire State Manufacturing Survey sent a warning about the state of the US manufacturing sector. The General Business Conditions index collapsed 36.2 points to -11.6, far below expectations of a more muted deterioration to…

Japanese machine tool orders are an excellent gauge of the state of the global manufacturing and trade cycle. On the surface, the double-digit year-on-year pace of expansion in April suggests that underlying macroeconomic conditions are resilient. However,…

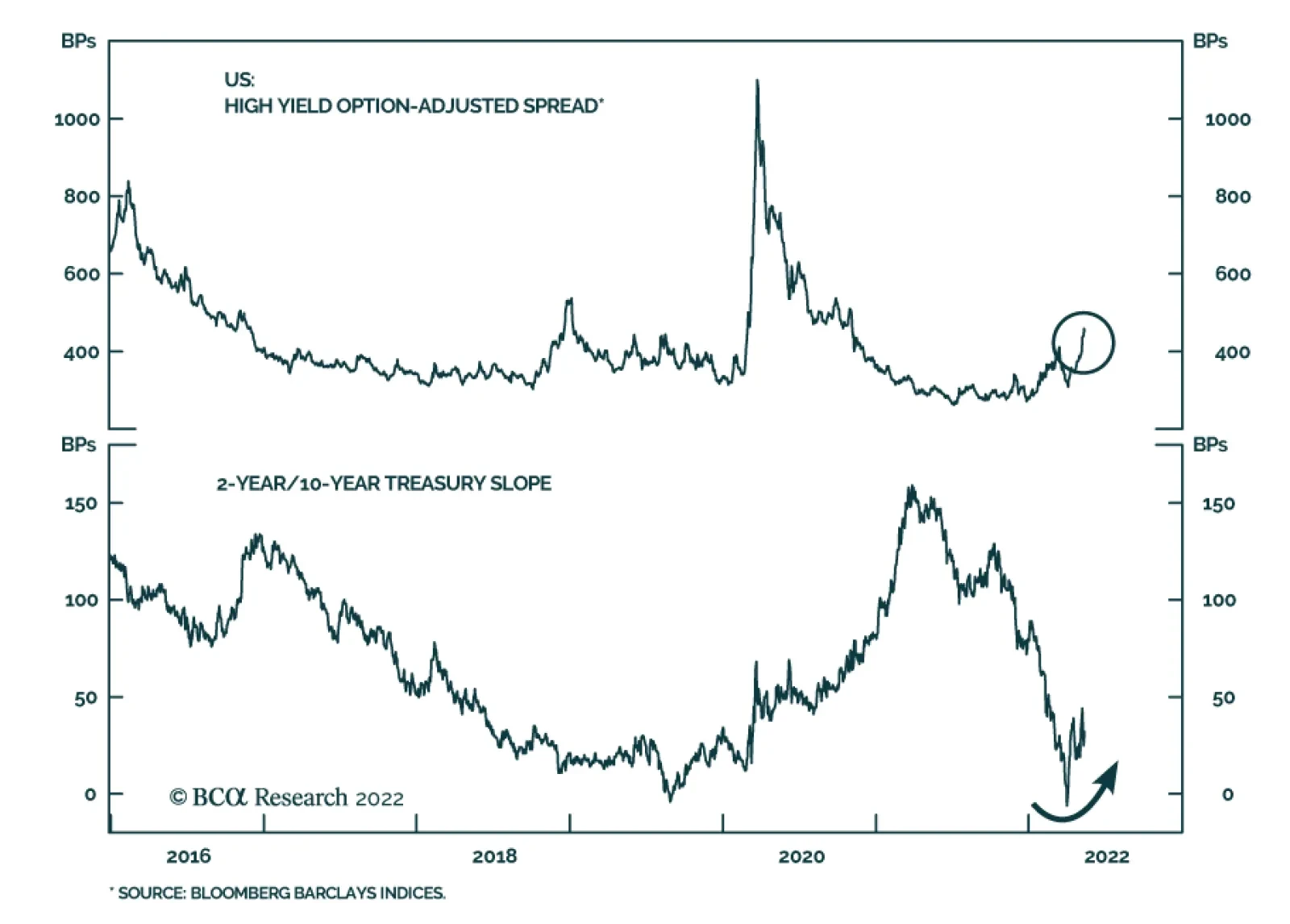

US high-yield corporate bonds have sold off sharply of late. The average index option-adjusted spread widened 50 bps last week to reach 452 bps. The latest move reverses the brief March rally and brings the spread on high-yield bonds to its highest level so…