Developed Countries

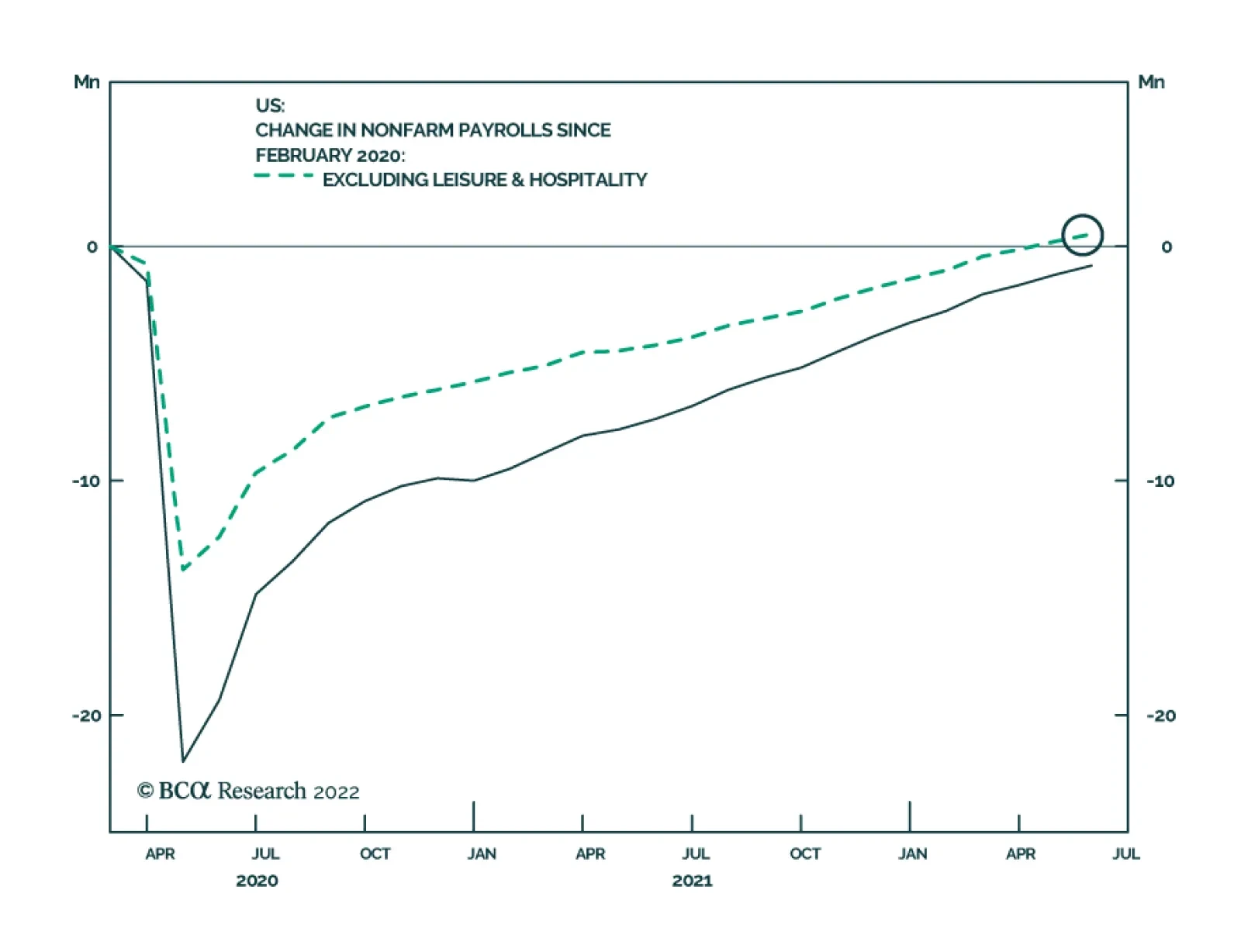

US nonfarm payrolls rose by 390 thousand in May, stronger than expectations of 318 thousand and down from an upwardly revised 436 thousand in April. The leisure and hospitality sector led the May payroll growth. Meanwhile manufacturing added 18 thousand jobs,…

Several ECB hawks – Robert Holzmann, Martins Kazaks, and Klaas Knot – have recently entertained the possibility of a jumbo 50bp rate hike this year. Data released last week shows that inflationary pressures accelerated in May. CPI inflation rose on a monthly…

The headline ISM Services index eased by 1.2 points in May to 55.9. This latest reading signals the slowest expansion in service sector activity since February 2021 and reflects a 4.6-point decline in the Business Activity component. However, details from…

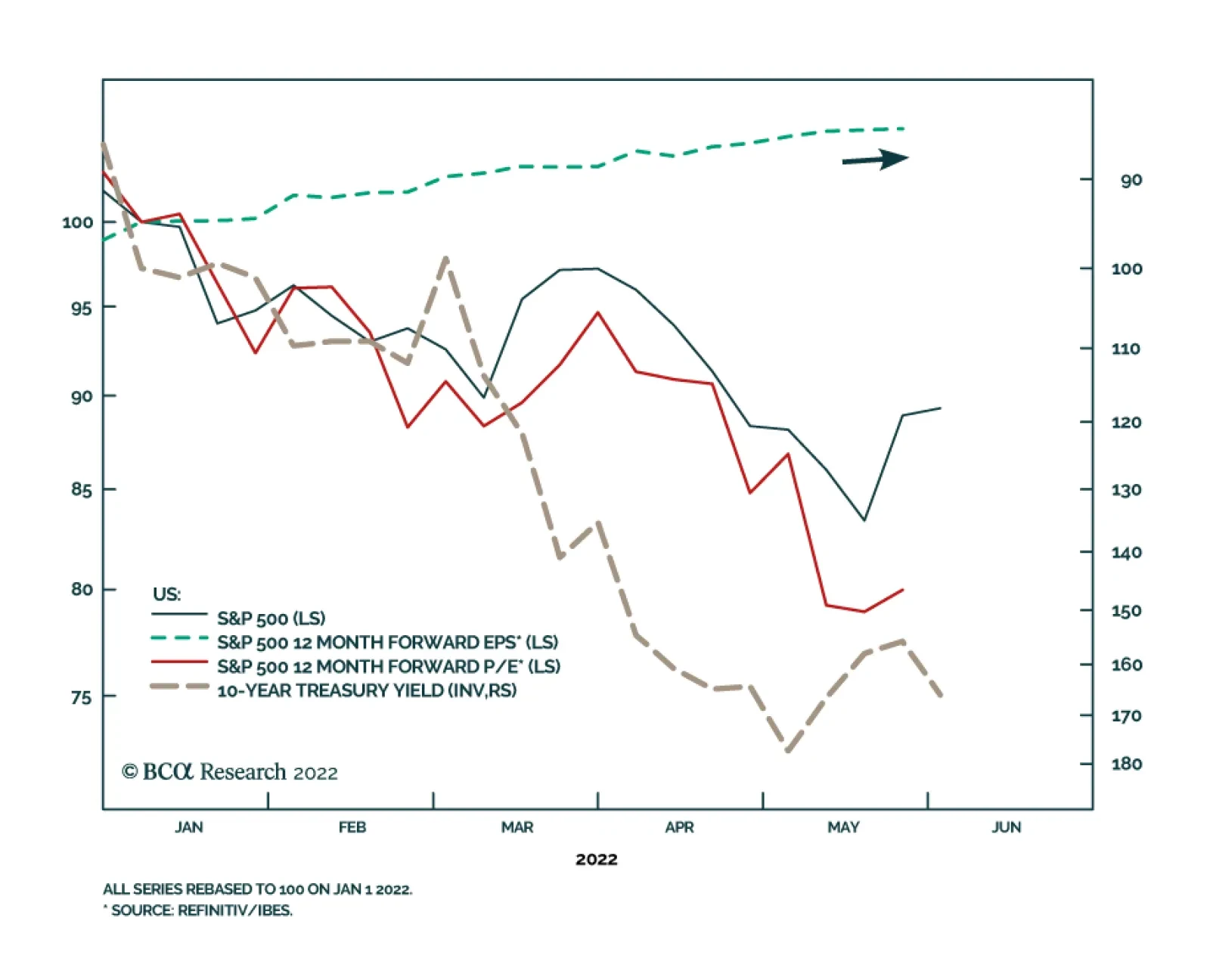

The S&P 500 has shed 13.8% since the beginning of the year on worries of a Fed-induced US recession, accelerating commodity prices and global growth slowdown. The selloff has been entirely valuation-driven. To the extent that Treasury yields provide…

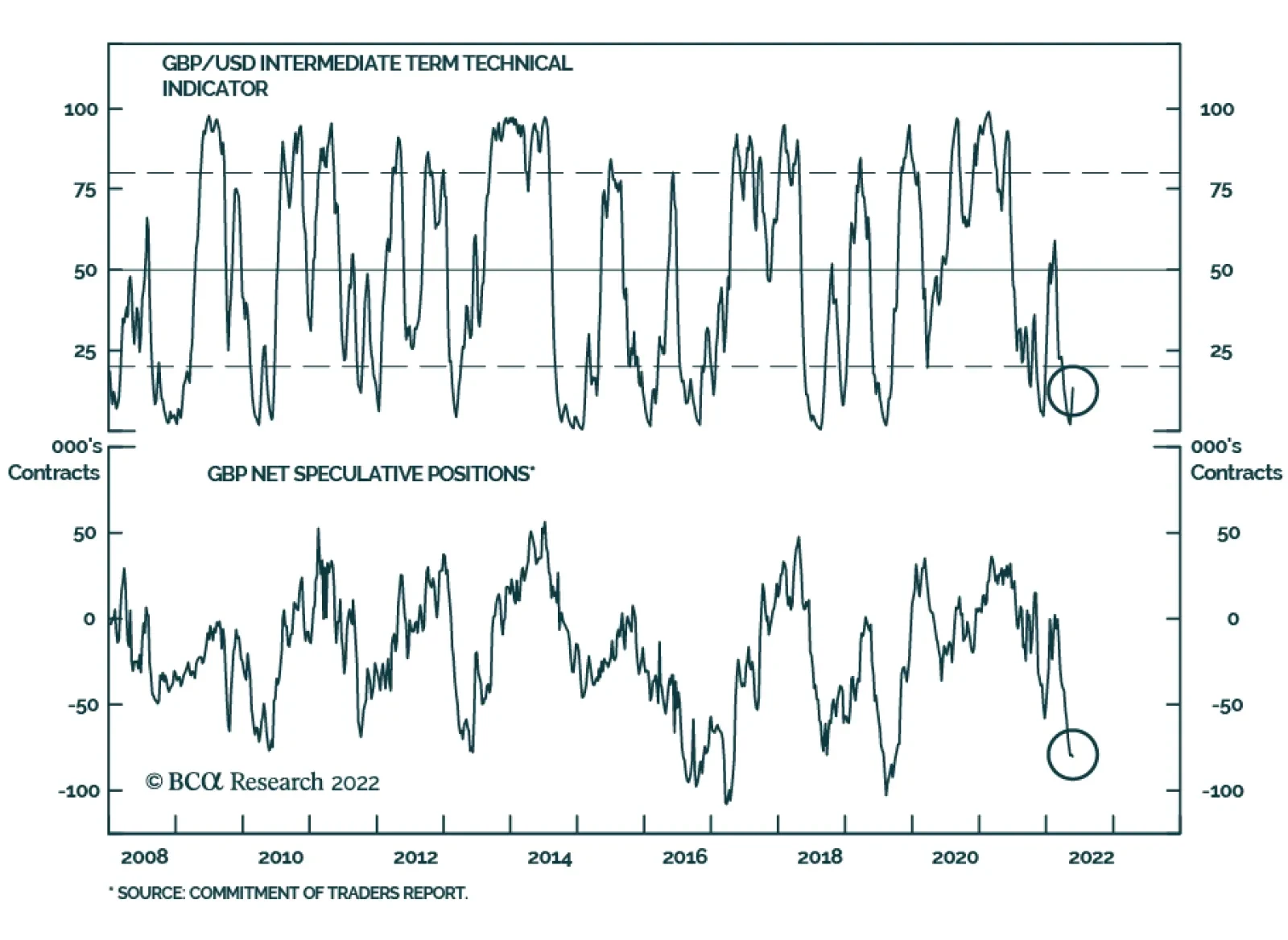

Listen to a short summary of this report. Executive Summary Sentiment On Sterling Is Depressed

Sentiment On Sterling Is Depressed

Sentiment On Sterling Is Depressed

The pound will suffer in the short term, setting the stage for a coiled-spring rebound. Cable is extremely cheap by most measures (Feature chart). The BoE could engineer a soft landing in the UK economy. If successful, it will annihilate sterling vigilantes, in a volte-face of the ERM crisis. We are cognizant of near-term risks. As such, we are long EUR/GBP with a target of 0.90, but will be buyers of cable at 1.20. Ultimately, the pound is undervalued on a longer-term basis. GBP/USD should touch 1.36 over the next 12-18 months. RECOMMENDATIONS INCEPTION LEVEL inception date RETURN long eur/gbp 0.846 2021-10-15 0.27 Bottom Line: The pound will likely face pressure in the near term, but will fare well over a cyclical horizon. Our 12-month target is 1.36. This target is based on a modest reversion towards PPP fair value, and some erosion in the “crisis” discount. Admittedly, sentiment on the pound is very depressed, and we could be wrong in our near-term assessment and cable has indeed bottomed. Feature Chart 1A Play On Cable Downside

A Play On Cable Downside

A Play On Cable Downside

There has been much discussion around the premise that the pound could enter a capitulation phase, akin to an emerging market-style currency crisis. With inflation sitting at 9%, well above the Bank of England’s 2% target, the narrative is that interest rates need to rise substantially but will, at the same time, kill any recovery. The result will be a sharp fall in the pound. We began to highlight the near-term risks to cable in October of last year, going long EUR/GBP in the process, as a way to play sterling downside (Chart 1). That said, our longer-term view on the pound remained positive. In this report, we review what has changed since, and if a negative longer-term view is now warranted. UK Balance Of Payments Almost all currency crises are rooted in a deterioration of the external balance, and this is certainly true for the UK. The trade deficit sits at 7.9% of GDP, the worst among G10 countries (Chart 2). As a result, the current account is also in deficit. That said, there are reasons for optimism. Related Report Foreign Exchange StrategyAn Update On Sterling The Office for National Statistics (ONS) suggests that a change in methodology in January 2022 could be exarcebating the deterioration in the latest release of the trade balance. In our view, there are two key reasons why the UK’s balance of trade is worsening. The first is the oil shock – fuels constitute 11% of UK imports. Second, unprecedented fiscal stimulus led to an overshoot in goods imports. These negative forces are likely cyclical in nature, rather than structural. It is also noteworthy that most of the goods imported into the UK are machinery and transport equipment, which could go a long way in improving its productive capacity (Chart 3). Chart 2The UK Trade Balance Has Deteriorated

The UK Trade Balance Has Deteriorated

The UK Trade Balance Has Deteriorated

Chart 3Goods Imports Have Been A Hit To The UK Trade Balance

Goods Imports Have Been A Hit To The UK Trade Balance

Goods Imports Have Been A Hit To The UK Trade Balance

In parallel, there has been a structural improvement in the UK’s current account balance. This has mostly been driven by a rising primary income balance. In short, investments abroad are earning more, relative to domestic liabilities (Chart 4). The UK runs a large negative international investment position. Despite this, it has maintained the ability to issue debt bought by foreigners, while investing in high-return assets abroad. Secondary income has admittedly been in a structural deficit, but a falloff in transfer payments under the Brexit agreement will significantly improve this balance (Chart 5). Chart 4The UK Current Account Is Improving

The UK Current Account Is Improving

The UK Current Account Is Improving

Chart 5A Fall In Brexit Payments Will Mend Secondary Income

Is Sterling Facing Another Crisis?

Is Sterling Facing Another Crisis?

Finally, the pound’s share of global foreign exchange turnover is 12.8%, just behind the dollar, euro, and yen. That said, London dwarfs New York, Hong Kong, and Tokyo as a hub for foreign exchange trading (Chart 6). The pound also very much remains among the most desirable global currencies. Global allocation of FX reserves in sterling have been rising over the last decade (Chart 7). It currently stand at 4.8%, higher than the RMB at 2.8%, and all other emerging market currencies combined. Chart 6London Remains An Important Financial Center

Is Sterling Facing Another Crisis?

Is Sterling Facing Another Crisis?

Chart 7The Pound Is Still A Reserve Currency

The Pound Is Still A Reserve Currency

The Pound Is Still A Reserve Currency

It is noteworthy to revisit the period the pound experienced an EM-style crisis – under the European Exchange Rate Mechanism (ERM), when cable was effectively pegged to the German mark at an expensive level. At the time, UK inflation was running hot, while German inflation was more subdued. By importing monetary policy from the Bundesbank, the BoE was able to tame inflation, but at a high cost to growth. In Germany, the reunification boom warranted much higher interest rates, which was not appropriate for the UK . Cable eventually collapsed by 32.9% peak-to-trough, as the UK ran out of foreign currency reserves. Chart 8Cable Is Very Cheap

Cable Is Very Cheap

Cable Is Very Cheap

There are three key differences between that episode and today: The pound is freely floating. Foreign exchange markets are extremely fluid and adjust to expectations quite quickly. A collapse in the pound seems unlikely, unless the UK faces a new large exogenous shock. Inflation is running hot in many countries, not just the UK. The pound is extremely cheap, and stimulative for the economy. On a real effective exchange rate basis, the pound is at record lows (Chart 8). Will The BoE Make A Policy Mistake? Sterling is pricing in a policy mistake by the BoE. First, inflation is well above its 2% target. Second, the labor market has tightened significantly. The unemployment rate hit a 47-year low of 3.7%, and job vacancies are low, pushing wages higher. As such, either the BoE allows inflation expectations to become unmoored, destroying the purchasing power of the pound, or kills the recovery to maintain credibility (Chart 9). Chart 9The UK Labor Market Is Tight

The UK Labor Market Is Tight

The UK Labor Market Is Tight

While difficult, there are reasons to believe the BoE can achieve a soft landing. According to an in-house study, only one-third of the rise in UK inflation has been driven by demand-side pull, with the balance related to supply factors.1 The latter have been the usual suspects – rising energy costs, supply shortages, and even legacies of the Brexit shock (Chart 10). UK electricity prices have cratered since the opening of the 1,400MW undersea cable with Norway (Chart 11). Chart 10Most Of The Increase To UK Prices Is Supply-Driven

Is Sterling Facing Another Crisis?

Is Sterling Facing Another Crisis?

Chart 11A Sharp Drop In Electricity Prices

A Sharp Drop In Electricity Prices

A Sharp Drop In Electricity Prices

Second, it is likely that the neutral rate of interest in the UK is lower in a post-Brexit, post-COVID-19 world. This is visible in trend productivity growth, but even the size of the labor force has shrunk significantly. The UK workforce is down by 560,000 people since the start of the pandemic. This has been partly due to less immigration and more retirees, but the vast majority has been due to health side-effects from the pandemic, and delays in getting adequate medical care. As a result, there has barely been a recovery in the UK participation rate (Chart 12). Chart 12AThe Participation Rate In The UK Is Below Trend

The Participation Rate In The UK Is Below Trend

The Participation Rate In The UK Is Below Trend

Chart 12BA Low Participation Rate Across Many Regions

A Low Participation Rate Across Many Regions

A Low Participation Rate Across Many Regions

In hindsight, a least-regrets strategy to policy tightening – lift rates faster now, and then back off if financial conditions tighten sufficiently – seems appropriate. Frontloading the pace of tightening will flatten the UK gilts curve further. With most borrowing costs in the UK tied to the longer end of the curve, refinancing costs might not edge up that much, while inflation expectations will be well contained. The real canaries in the coal mine from this strategy are the economies of Australia, New Zealand, and Canada, where household debt is much more elevated (Chart 13), and the percentage of variable rate mortgages are higher. Chart 13Household Debt Is Not Alarming In The UK

Household Debt Is Not Alarming In The UK

Household Debt Is Not Alarming In The UK

Larger fiscal stimulus will partially offset the near-term hit from tighter monetary policy. The additional £15 billion cost-of-living package announced last month is quite substantial at 0.7% of GDP. This gives the BoE breathing room to tighten policy in the near term. The redistributionist nature of the plan – taxing windfall profits from large energy companies, and using that to subsidize consumers most in need – could be what is required to achieve a soft landing, if the energy shock is temporary. Our Global Fixed Income colleagues upgraded UK gilts to overweight last month, on the basis that market pricing further out the SONIA curve was too aggressive. In our prior report on sterling, we also suggested that market expectations for interest rate increases may have overshot. Money markets are discounting a peak in the bank rate at 2.8%. The BoE’s new Market Participants survey suggests it will peak at 1.75%. While the BoE will deliver sufficient monetary tightening to lean against near-term inflationary pressures, it will be very wary to overdo it. This is especially true if the neutral rate in the economy is much lower. What Next For The Pound? Our view is that the pound faces near-term risks but is a buy longer term. There is an old adage that credibility is hard to earn, but easy to lose. For the UK in particular, this hits the mark. The Bank of England is the oldest central bank in the world, after the Riksbank. Yes, the BoE can make a policy mistake (as it has in the past), but treating the pound as an emerging market asset is a stretch (Chart 14). That said, our Chief European Strategist, Mathieu Savary, believes stagflation is not fully priced into UK assets. In the near term, he might be right. The UK’s large trade deficit puts the onus on foreigners to dictate movements in the pound. The pound does well when animal spirits are fervent. So far, markets have bid up a substantial safe-haven premium into the dollar (Chart 15). As a proxy, the pound has been sold. Northern Ireland could also return as a thorn in the side of sterling. Chart 14The Pound Is A Risk-On Currency Cable And EM Stocks

The Pound Is A Risk-On Currency Cable And EM Stocks

The Pound Is A Risk-On Currency Cable And EM Stocks

Chart 15The Dollar Has A Hefty Safe-Haven Premium

The Dollar Has A Hefty Safe-Haven Premium

The Dollar Has A Hefty Safe-Haven Premium

From a bird’s eye view, three factors tend to drive currencies – the macroeconomic environment, valuation, and sentiment. For now, markets have latched on to the GBP’s vulnerability to an EM-style crisis. That said, cable is very cheap, even accounting for elevated UK inflation. Our in-house PPP model suggests the pound could appreciate by 4% per year, over the next 10 years, just to revert to fair value (Chart 16). Chart 16Cable Is Cheap

Cable Is Cheap

Cable Is Cheap

Admittedly, the UK desperately needs an improvement in productivity growth for further currency gains. To encourage capital inflows that the pound depends on, the UK needs to be at the forefront of disruptive technologies such as electric cars, digital currencies, 3D printing, and even innovations in gene therapy. High finance and fashion will remain relevant for London, but the need for innovation is high. Investment Conclusions Chart 17Sentiment On Sterling Is Depressed

Sentiment On Sterling Is Depressed

Sentiment On Sterling Is Depressed

The pound will likely face pressure in the near term, but will fare well over a cyclical horizon. Our 12-month target is 1.36. This target is based on a modest reversion towards PPP fair value, and some erosion in the “crisis” discount. Admittedly, sentiment on the pound is very depressed, and we could be wrong in our near-term assessment if cable has indeed bottomed. Our intermediate-term timing model suggests that GBP is undervalued and has bottomed. Technical indicators also warn that cable is ripe for a fervent rebound (Chart 17). Particularly, our intermediate-term technical indicator is rebounding from oversold levels. The Aussie would outperform the pound in the long term, but AUD/GBP is vulnerable to a commodity relapse in the shorter term. Housekeeping We were stopped out of our short EUR/JPY trade for a loss of -2.78%, as oil prices and bond yields rebounded. This trade is a hedge to our pro-cyclical portfolio, so we will look to reenter it at more attractive levels. We are also lowering the stop-loss on our short RUB trade. This is a speculative bet many clients will not be able to play, but we expect it to payoff over the longer term. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Michael Saunders, "The route back to 2% inflation," (Speech given at the Resolution Foundation), May 9, 2022. Trades & Forecasts Strategic View Cyclical Holdings (6-18 months) Tactical Holdings (0-6 months) Limit Orders Forecast Summary

Executive Summary Crude Oil Prices Will Remain High

Crude Oil Prices Will Remain High

Crude Oil Prices Will Remain High

The EU embargo on Russian seaborne oil imports will tighten global crude oil and refined-product markets further. Pipeline imports are due to phase out by year-end. This will translate to a 90% decrease in Russian crude and product exports to the EU, representing ~ 3mm b/d of lost sales. Russian crude oil production will fall to 7-8mm b/d by year-end 2023, unless the state pre-emptively cuts output before that. This would push crude oil above $140/bbl. We expect Russia to reduce natural gas exports to the EU in the wake of the oil embargo. Refined-product markets will remain tight, given refining capacity losses, tight crude oil markets and still-strong gasoline and diesel demand. OPEC 2.0 is expected to maintain its policy to nominally increase oil supply by 432k b/d at its meeting this week. Actual oil output returned to the market by the coalition is ~ 1.5mm – 1.7mm b/d below nominal levels. Bottom Line: Oil markets will continue to tighten in the wake of the EU’s embargo on Russian imports this week. Refined-product markets will remain well bid, with prices of gasoline, jet and diesel fuel close to or above record levels. We remain long oil producers and refiners via the XOP and CRAK ETFs, along with the S&P GSCI and COMT ETF, to retain exposure to higher commodity prices and backwardation. Feature Global refined-product markets are tight and getting tighter. Related Report Commodity & Energy StrategyOil, Natgas Prices Set To Surge As the Northern Hemisphere driving season gets underway, gasoline and diesel prices in the US are at record levels – up 56.55% and 70.17% respectively yoy. So are jet-fuel prices, which are up 107.97% yoy in the US. Prices are similarly robust ex-US and trading at or close to record levels. During the COVID-19 pandemic, the US permanently lost ~ 5% of total refining capacity. Currently, three of the largest refineries in the US are working on replenishing less than half of that loss by end-2023, which will take total US refining capacity to under 18.5mm b/d. US gasoline stocks are low for this time of the year. Markets expect higher demand this driving season, which unofficially ends in early September with the Labor Day weekend in the US. The US went into the Memorial Day Weekend – the start of the summer driving season – with record high motor gas prices (Chart 1). Gasoline stocks normally build in the off-season winter months. However, this year inventories are depleted (Chart 2) because of relatively high distillate “crack spreads” – gross refining margins – which incentivized refiners to produce more diesel, jet and marine fuels.1 This meant gasoline output was sacrificed in the process, which left markets tight going into the summer driving season.2 Chart 1High Gas Prices Bring In US Driving Season

High Gas Prices Bring In US Driving Season

High Gas Prices Bring In US Driving Season

US distillate crack spreads are at record highs, after stocks hit a 14-year low last month (Chart 3). Reduced oil refinery capacity will constrict future supply, keeping prices elevated, which will feed into inflation. Demand destruction will be required to balance markets and bring prices lower. Chart 2Depleted Stocks Due To Low Gasoline Margins

Higher Gasoline, Diesel Prices Ahead

Higher Gasoline, Diesel Prices Ahead

Chart 3Low Distillate Stocks Produce Record Cracks

Higher Gasoline, Diesel Prices Ahead

Higher Gasoline, Diesel Prices Ahead

Tight Supply-Demand Fundamentals, High Prices US refined-product prices have been strengthening since 2021 due to high crude oil prices, rising demand and lower refinery capacity and utilization rates. This keeps the level of demand for refined products consistently above the level of supply, which forces refiners to pull down inventories or increase imports to cover the supply-demand gaps. Higher refined-product prices ensue as inventories fell. As a result, crack spreads were pushed higher to encourage higher output, which remains problematic because of supply-side pressure in global crude-oil markets (Chart 4). Crude oil prices account for 60% of gasoline and 49% of diesel costs, respectively.3 Last year OPEC 2.0’s production-management strategy kept the level of crude oil supply below demand, but this year additional forces are constraining output. Supply disruptions following Russia’s invasion of Ukraine, lower OPEC 2.0 production, and non-OPEC capital discipline, particularly from US shale-oil producers, have combined to constrain crude-oil production. We expect continued production restraint by core OPEC 2.0 (Saudi Arabia and the UAE); lower output from the rest of the coalition; falling Russian supply due to sanctions and an EU embargo on Russian oil imports; and continued capital discipline by shale producers. These factors will offset weaker global oil demand resulting from slower GDP growth in the EU and China. Chart 4Supply Will Barely Rise Despite High Margins

Higher Gasoline, Diesel Prices Ahead

Higher Gasoline, Diesel Prices Ahead

Volatile supply-demand dynamics will keep crude oil prices elevated this year and next (Chart 5).4 The EU’s embargo on Russian oil, in particular, will raise oil-price volatility, and leave prices upwardly biased. Lastly, we do not expect the US and Iran to renew the Joint Comprehensive Plan of Action (JCPOA), which would allow ~ 1mm b/d of Iranian exports to return to the market. Chart 5Crude Oil Prices Will Remain High

Crude Oil Prices Will Remain High

Crude Oil Prices Will Remain High

Tighter Product Markets Will Persist Refined-product stocks in the US and the rest of the world were low prior to Russia’s invasion of Ukraine, owing to strong demand growth and weak crude-oil supply growth last year, along with lower global refining capacity. US refinery utilization rates last year and earlier this year fell as refiners undertook heavier-than-usual maintenance, which was deferred during the pandemic (Chart 6). Refiners also closed ~ 1mm b/d in 2020 during the COVID-19 pandemic, which resulted in ~ 5% of US refining capacity being shut-in at the start of 2021.5 Global refining capacity has fallen by more than 2mm b/d since the COVID-19 pandemic.6 As midterm elections approach, the Biden administration has been urging refiners to restart idle capacity to little or no avail, and has threatened to re-introduce export restrictions on crude oil in an attempt to hold down gasoline and diesel prices. Chart 6US Refiners Were Shut-In For Maintenance

Higher Gasoline, Diesel Prices Ahead

Higher Gasoline, Diesel Prices Ahead

Gasoline markets are going into their first summer without COVID-19 restrictions since 2020. While US data for the first 3 months of 2022 suggest Americans’ gasoline consumption was more price-inelastic than in the past (Chart 7), a series of record-breaking gasoline prices recently may have been enough to start curbing US gasoline demand (Chart 8). All the same, US consumers appear to be willing to pay up for holiday breaks and get-aways, which will keep pressure on inventories during the summer driving season. Chart 7US Gasoline Demand Price Inelastic In Q1…

Higher Gasoline, Diesel Prices Ahead

Higher Gasoline, Diesel Prices Ahead

Chart 8…But Record Breaking Prices May Change That

Higher Gasoline, Diesel Prices Ahead

Higher Gasoline, Diesel Prices Ahead

Jet, Diesel Remain Tight, Especially In Europe The approval of an embargo on Russian oil imports into the EU earlier this week means member states on the continent that rely heavily on Russian distillate exports will remain exposed to higher refined-product prices (Chart 9).7 This will keep European diesel prices and crack spreads elevated this year and next (Chart 10). Chart 9EU Dependent On Russia For Diesel

Higher Gasoline, Diesel Prices Ahead

Higher Gasoline, Diesel Prices Ahead

Chart 10Europe Refining Margins Will Remain Elevated

Higher Gasoline, Diesel Prices Ahead

Higher Gasoline, Diesel Prices Ahead

Shipping markets also will continue to feel the pressure of higher prices, particularly for marine diesel fuel. Russia’s invasion of Ukraine forced insurance rates higher, which propelled shipping-rates higher in Europe and Russia (Chart 11). The EU is now slapping sanctions on insurers. In addition, the Ukraine war forced a re-routing of ships and port congestion, which led to massive supply-chain disruptions due to closures and blockades.8 High refined-product prices partly is the result of European refineries either permanently shutting in production or switching to renewable energy production when faced with low Covid-19-induced demand in 2020. In the first half of 2021, as product demand started to rise, the parabolic increase in prices of natgas – used as a fuel by refiners – was an additional headwind to refining margins. Chart 11Cost Of Shipping Crude, Products Surges

Higher Gasoline, Diesel Prices Ahead

Higher Gasoline, Diesel Prices Ahead

As of last December, more than 800 kb/d – or 5% of the continent’s refining capacity – was permanently taken offline during the pandemic.9 As a result, OECD Europe’s refining capacity for 2022 will be 11.4 mmb/d, ~ 0.8 mmb/d below pre-pandemic levels.10 Europe will need to look elsewhere for distillates. Attempting to substitute refined products in such tight energy markets will not be cheap. Sourcing imports from other states will tighten exporters’ domestic refined product markets and dislocate distillate supply to their traditional importers, which will tighten those states’ domestic markets as well. This could lead to something similar to what we are currently witnessing in LNG markets between Europe and Asia. The US, despite having its own tight refined products market, likely will step up as an alternate supplier to fill the Russian distillate supply void for states reliant on Russian diesel, jet and marine fuels. This can be seen in the 32-month high in Gulf Coast diesel exports from the US, which are the result of stronger imports by Europe and LatAm.11 Investment Implications The EU embargo on Russian oil imports will tighten global refined-product markets. If Russia retaliates by pre-emptively cutting crude oil production by 20-30%, prices would significantly exceed our forecast of $113/bbl this year and $122/bbl next year – reaching or surpassing $140/bbl. Refined-product markets will remain well bid, with prices of gasoline, jet and diesel fuel close to or above record levels. We remain long oil producers and refiners via the XOP and CRAK ETFs, along with the S&P GSCI and COMT ETF, to retain exposure to higher commodity prices and backwardation. Ashwin Shyam Research Analyst Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Paula Struk Research Associate Commodity & Energy Strategy paula.struk@bcaresearch.com Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Commodities Round-Up Energy: Bullish We continue to expect Russia to cut off natural gas exports to the EU in retaliation for the embargo on EU oil imports from Russia agreed this week. The timing of this cut-off is uncertain, however. As our colleague Matt Gertken notes in this week’s Geopolitical Strategy, Russia and the EU both would benefit if exports were maintained as long as possible and phased down slowly. This would provide Russia with revenues to wage war in Ukraine, while allowing Europe to avoid recession as it phases out Russian gas. This is not an equilibrium, however, as it leaves both sides exposed to a sudden reversal of the tacit understanding. In equilibrium – i.e., the strategies that guarantee the EU and Russia lose the least – both states reduce their energy trade immediately. Russia needs to show strength in the face of the EU’s embargo, and Europe needs to cut the revenues fueling Russia’s war in Ukraine, which also will deter similar aggression against member states in the future. As soon as the EU weans itself off Russian natgas, Russia’s leverage disappears. If Europe does not diversify immediately, Russia can punish it severely by cutting off energy before it is prepared. (Chart 12). In the meantime, the EU is moving heaven and earth to fill its natgas storage as quickly as possible (Chart 13). According to the GIE AGSI, the percent-full level was 46.68% as of May 30, 2022. Precious Metals: Bullish Gold prices pared losses last Wednesday after the Federal Open Market Committee’s (FOMC) minutes of the May meeting indicated the Fed will not raise rates by more than the half percentage points markets had priced in for June and July. Recent weakness in gold prices despite heightened geopolitical uncertainty can be attributed to the Fed’s tightening cycle. Rate hikes will increase real interest rates, the opportunity cost of holding non-yielding bullion and strengthen the USD, which competes directly with gold for safe-haven demand, and will also raise the price of gold in local currencies. Base Metals: Bullish Chile’s National Institute of Statistics reported the country’s Mining Production Index fell 10.6% year-over-year (y-o-y) in April, dragging the country’s overall Industrial Production Index lower by 3.6% y-o-y. The drop in mining was due to a 9.8% fall in copper production y-o-y. The contraction in mined copper output this month follows y-o-y contractions of 15%, 7% and 7.2% in January, February and March respectively this year. Chart 12

Higher Gasoline, Diesel Prices Ahead

Higher Gasoline, Diesel Prices Ahead

Chart 13

Higher Gasoline, Diesel Prices Ahead

Higher Gasoline, Diesel Prices Ahead

Footnotes 1 The “crack spread” (or “cracks”) is an industry term for gross margins. It derives its name from the literal cracking of the bonds holding the hydrocarbon molecules of crude oil together under intense heat and pressure, and reforming them into refined products like gasoline and diesel fuel and other liquids and gases. The crack spread is the difference between the price of a refined product and crude oil in USD/bbl. 2 In this report, we focus on diesel fuel and gasoline. Low stocks, high prices and high crack spreads are a feature of jet-fuel markets as well. 3 Please see the US EIA’s May 2022 Gasoline and Fuel Update. 4 Please see Oil, Natgas Prices Set To Surge published on May 19, 2022 for our latest balances and price forecasts. 5 Please see the U.S. EIA’s 30 June, 2021 edition of This Week In Petroleum. 6 Please see White House Eyes Restarting Idle Refineries, published by ttnews.com on May 26, 2022. 7 Please see Breakingviews: Oil embargo will hurt Putin more than EU, published by reuters.com on May 31, 2022. 8 For more on this, please refer to High Food Prices Drive EM Inflation, which we published on May 12, 2022. 9 Please see Viewpoint: European refiners cautious on cusp of 2022, published by Argus Media on December 30, 2021. 10 Please see the IEA’s January 2022 Oil Market Report. 11 Please see to PADD 3 diesel exports reach 32 month high as the competition for the non-Russian molecule begins, published by Vortexa on May 4, 2022. Investment Views and Themes Strategic Recommendations Tactical Trades Trades Closed in 2022

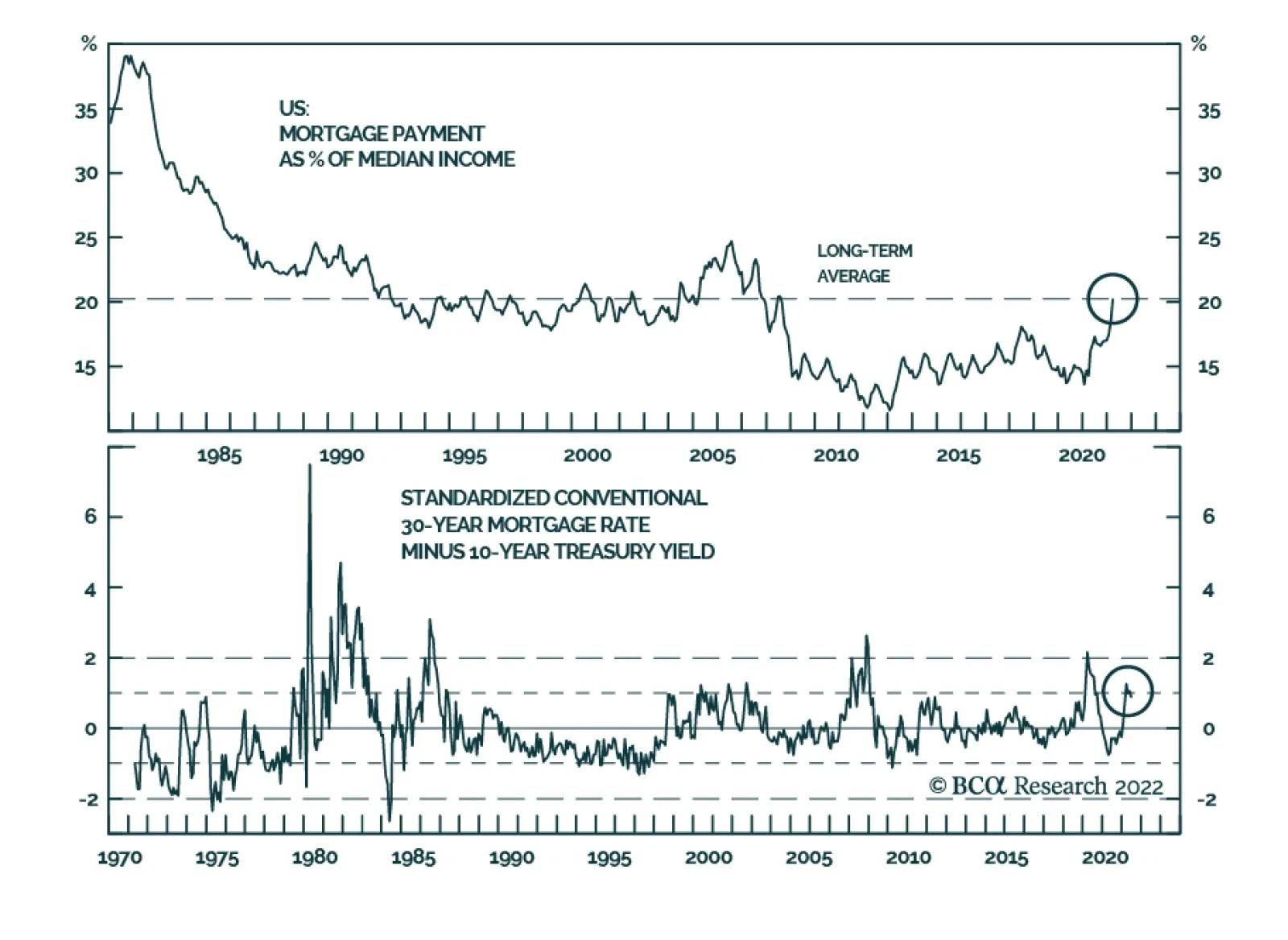

US housing, one of the most interest-rate sensitive sectors of the economy, has cooled in line with the two-percentage point rise in mortgage rates. Housing market dynamics affect aggregate growth via the wealth effect it exerts on consumption as well as…

GBP/USD has been strengthening over the past three weeks after hitting a two-year low of 1.22 on May 12. Does this mark the beginning of a more sustainable rally? Cable faces crosscurrents over the near term. On the one hand, the BoE’s recent messaging…

Executive Summary Return Of The 'Pocketbook Voter'

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

President Biden’s pledge to fight inflation ahead of the midterm elections got a boost with the Gulf Arab states pledging to increase oil production in July and August. Yet OPEC’s action should not be overrated. The Saudis are not clearly bailing out Biden … at least not yet. Biden’s other inflation-fighting tools are also limited. The Fed will hike rates, which will weigh on inflation, at least in the short run. A short-term moderation in inflation will cause big shifts in financial markets. It will not save the midterms for Democrats, but gridlock is disinflationary so the effect is the same. Inflation risks will persist over the long run. Recommendation (Cyclical) Inception Level Inception Date Return Small Vs. Large Cap Energy 0.6485 26-JAN-22 14.2% Oil And Gas Transportation And Storage Vs. S&P 500 0.0527 30-MAR-22 16.5% Bottom Line: Expect inflation to moderate in the short run. Oil prices will be volatile. Book a 14% profit on small cap versus large cap energy stocks and a 16.5% profit on the oil and gas transportation sub-sector relative to the broad market. Feature President Biden kicked off the summer – and the midterm election campaign – by defending his record thus far and pledging a three-pronged strategy to fight inflation. His options are limited but he received a boost from OPEC right off the bat. The bottom line is that disinflationary pressures are emerging. These include congressional gridlock, which is likely to return in January 2023. Biden’s policies will not save his party from a defeat in the midterms but moderating inflation will have huge investment consequences. Biden’s Three-Pronged Plan Consumer confidence is hurting while inflation eats away at real wage growth for Americans (Chart 1). Confidence is 14% higher than when Biden took office but 17.5% lower than when it peaked in June 2021. The latest survey from the Conference Board showed another decrease in May. This is foul weather for a ruling party that already stands to suffer a major check on its power when voters go to the polls in the fall. Biden’s approval rating is likely to stabilize but only at the current low level of 41.4%. Voters are focusing on the economy more than other issues like health care, the environment, or foreign affairs (Chart 2). Chart 1Consumer Confidence And Real Wages Tumble

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart 2Return Of The 'Pocketbook Voter'

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

In the Wall Street Journal Biden laid out his party’s election pitch.1 First, he argued that the US economy is transitioning from rapid recovery to stable growth – i.e. that it is not going into recession. That would be good, but a recession is possible and the slowdown is politically deadly: Household Savings: Aggregate household savings have risen from $1Tn in 2019 to $3.9Tn today, which Biden cited as evidence of improving financial security. The problem is that inequality skews the picture and the average American is unlikely to feel secure. Low and middle income earners have depleted their savings or seen only a small increase (Chart 3). The Biden administration failed to improve inequality as promised while the uneven economic recovery means that lower-paid Americans do not have as much ability to buffer spending as the aggregate savings imply. They will be unhappy in November. Chart 3Normal Households No Longer Flush With Savings

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Jobs And Wages: Biden highlighted the role of his economic stimulus in lowering unemployment and argued that Americans have better paying jobs. But inflation has eroded real wages and incomes, as highlighted in Chart 1 above. Business Investment: Biden argued that business investment is brisk. But sentiment is turning. New orders of core capital goods have rolled over and capex intentions are falling (Chart 4). Manufacturing Comeback: Biden also touted the US manufacturing comeback, claiming that factory jobs are growing at fastest rate in 30 years. But again the tide is shifting against him, with the employment component of manufacturing purchasing manager indexes now signaling contraction (Chart 5). Biden, like Presidents Trump and Obama, has invested heavily in the “Buy America” re-industrialization narrative, so this trend is threatening. Chart 4Business Investment Setback

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart 5Manufacturing Employment Weakening

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

A recession may indeed be avoided but the risk will not go away in time for the election. A recent study showed that at today’s extremely high level of inflation and extremely low level of unemployment, the odds of recession range from 60%-70% over the next 12-24 months.2 Second, Biden promised voters that he will fight inflation with all the powers of the White House. He laid out a three-pronged approach. However, his options are fairly limited and voters will not change their minds easily over the next five months: The Fed will hike rates: Biden argued that it is the Fed’s job to fight inflation and he will not interfere with rate hikes. While Biden offered admirable verbal support for an independent and non-partisan central bank, the truth is that real interest rates have not been this low since the highly politicized Fed chairmanship of Arthur Burns (Chart 6). While Biden has no reason to discourage rate hikes at the moment, he may change his tune as rates rise, growth slows, and the presidential election approaches. So may Powell, but by then it may be too late. In short, the Fed will hike, which will weigh on inflation, but it will not help Biden win voters this fall or avoid a recession by 2024. Congress will expand capacity: Biden argued that the bipartisan infrastructure bill that he signed into law and his other legislative proposals will boost the supply side of the economy. We are moderately optimistic about Congress’s ability to pass a party-line reconciliation bill that provides subsidies for the energy sector. This could pass under the consensus-building rubric of fighting Russia and climate change at the same time. But this measure, along with Biden’s Housing Supply Action Plan, child care and elderly care subsidies, and other proposals often look more like demand-side stimulus than supply-side reforms. They would fan inflation by increasing government spending and budget deficits. Moreover the administration cannot fix broken supply chains while China remains subject to strict Covid-19 lockdowns (Chart 7). In short, Congress may pass a reconciliation bill but it would be mildly stimulating for the economy (i.e. inflationary) and none of the supply-side improvements would reduce inflation in time for the midterms. Chart 6Biden Doesn't Need To Interfere With The Fed

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart 7Supply Snarls Will Continue While China Struggles With Covid

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

The budget deficit will fall: Biden argued that budget consolidation will reduce inflation, pointing to this year’s estimated $1.7 trillion drop in the budget deficit and arguing that the deficit is falling lower than pre-pandemic levels. He also argued that robust tax revenues from the economic recovery justified his previous fiscal stimulus (the American Rescue Plan Act). However, the budget is merely normalizing from extreme pandemic heights – there have obviously not been any long-term fiscal reforms (Chart 8). If Congress passes a reconciliation bill then Biden may succeed at passing a minimum corporate tax, which would mark an important success. But while the fiscal drag is negative for inflation, it is also negative for the economy this year and for Biden’s party in the midterms, and long-term budget trends are inflationary. Chart 8No Sign Of Budget Control Over Long Run – Budget Deficits Are Inflationary

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

The takeaway is that the Fed’s actions are disinflationary. Congress may or may not pass a climate bill before the election, but if it does, the budget deficit will be the same or larger and the economy will be the same or slightly stimulated. In brief Biden’s anti-inflation plan is to avoid interfering at the Fed. Extremely low unemployment will not save Biden and the Democrats this election season, any more than it saved Trump and the Republicans in 2018 (Chart 9). The Fed will rein in inflation at least in the short run. The election will lead to gridlock, which will freeze fiscal policy. Bottom Line: Inflation expectations will moderate but not because of any supply-side reform or fiscal consolidation coming from the Biden administration this year. Chart 9Low Unemployment Will Not Save Democrats

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Will Biden Ease Russian Energy Tensions? No. Biden’s other avenues for reducing inflation – not addressed in his editorial – lie in the foreign policy realm. The Biden administration is turning toward foreign policy as gridlock settles over Capitol Hill. Biden’s foreign policy will be insular, reactive, and focused on the midterm elections. Could Biden facilitate ceasefire talks in Ukraine so as to ease energy pressures stemming from Russia? The short answer is no. Biden imposed an oil embargo on Russia and ultimately agreed to the EU’s embargo. Biden can afford to run large risks with Russia this year because a larger confrontation or crisis with Russia would not hurt the Democrats in the midterm elections. Indeed the best hope for the Democrats is to recreate the 1962 congressional election, when John F. Kennedy stared down Soviet leader Nikita Krushchev in the Cuban Missile Crisis in October just before the election. Kennedy’s Democrats lost four seats in the House, gained four in the Senate, and kept control of both. Biden’s approval rating is nowhere near Kennedy’s but his party’s outlook is bad enough that he may be willing to run the risk of a crisis that could lead to a favorable rally-around-the-flag effect in the fall (Chart 10). Biden’s clearance this week of the highly mobile artillery rocket system for Ukraine – despite the risk that Ukrainians would launch attacks into Russian territory – underscores this point. Bottom Line: Biden will not ease tensions with Russia ahead of the midterm to try to reduce energy prices. Chart 10Biden Can Risk A Bigger Russia Crisis

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Will Biden Lower China Tariffs? No. What about China – will Biden ease the Trump administration’s tariffs on China to reduce inflation before the midterm election? Treasury Secretary Janet Yellen has repeatedly signaled support for this idea. The Trump administration marked a historic increase in US tariffs and the Biden administration has so far offered relief only for US allies (Chart 11). Again the short answer is no. Protectionist sentiment will prevail during midterm election season and US voters have turned decisively unfavorable toward China in recent years (Chart 12). The China tariffs have not been the driver for US inflation so tariff relief would bring minimal price relief while exacting a high political cost of making Biden look weak, wishy-washy on his pro-democracy values, and (according to Republicans) corrupt. Biden would be offering unilateral benefits to China without gaining Chinese trade concessions. Chart 11Biden Keeps Trump's Tariffs On China

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart 12Protectionist Sentiment To Prevail Amid Midterms

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Recently the Biden administration gave some indications of where it stands on China policy. Biden visited US allies in Asia Pacific and provoked China over the Taiwan Strait. Secretary of State Antony Blinken unveiled the administration’s comprehensive China policy and declared that the US would remain focused on China as the “most serious long-term challenge” despite Russia’s open belligerence in Europe.3 On paper, US-China trade relations do not look that bad. While China is falling short of its Phase One trade deal import promises, the truth is that a global recession intervened – and those promises were made under duress when the US slapped sweeping sanctions on Chinese exports. The commodity trade is booming, as is to be expected amid global energy shortages (Chart 13). The problem is that neither the US nor China has the domestic political capital to offer structural concessions in the short run, while both sides are girding for a century-long power struggle over the long run. Supply insecurity will result in the commodity trade suffering as a vast global substitution effect takes place. This is due to Russia’s energy breakup with Europe, growing Russia-China trade linkages, and ongoing US-China tensions. Global trade and US-China trade are set to slow, while China’s surge in energy imports from the US will abate for reasons of state security. Chart 13US-China Trade Faces Strategic Limits

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Bottom Line: No reduction in US tariffs on China is likely. Any reduction will have minimal macroeconomic effects and will be replaced by other punitive measures, given the underlying strategic competition and protectionist election politics. Meanwhile China’s “Zero Covid” policy will weigh on trade ties and sustain price pressures in the short run, as mentioned. Will Biden Lift Iran Sanctions? Probably Not. What about the Middle East? Can Biden convince the core OPEC states to pump more oil in lieu of Russian production? Or can Biden lift sanctions on Iran to undercut soaring gasoline prices? On this front Biden received welcome news on June 2 when Gulf Arab states promised to increase production by 638,000 barrels per day in July and August, up from an expected 430,000. At the same time news broke that Biden will visit Saudi Arabia, including potentially Crown Prince Mohammed bin Salman (MBS), and other Gulf partners sometime in June. There is not yet a clear understanding between Biden and MBS but it is possible that one will develop. The trigger for OPEC’s declaration is the EU oil embargo on Russia. EU is finalizing an embargo on 90% of oil imports – everything except the oil flowing through the Southern Druzhba pipeline to land-locked eastern European states. The embargo will impair Russian energy production: it could fall by as much as 2-3 million barrels per day, distribution interruptions will occur as Russia transitions to Asian buyers, and Russia’s long-term production capacity could be damaged. The result could be a destabilizing price spike. While the core OPEC states have just enough spare capacity to cover that gap in theory (Chart 14), they will not want to commit all spare capacity at once. Chart 14OPEC Spare Capacity

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

There is still a lot of uncertainty about how rapidly the embargo will be enforced, how much Russian production will suffer, whether the OPEC states will meet these new production increases (all except Saudi have been falling short), and what will be the OPEC policy beyond August. But for now it is clear that the Gulf Arab states are helping the US and EU by signaling some extra supplies at a critical time. The Gulf Arabs benefit from high oil prices and have previously ignored the G7’s pleas to increase production. But they also need to prolong the business cycle – a cycle-killing price shock from Russia is not in their interest. They are interested in keeping up revenues, maintaining domestic stability, and maintaining their position as the gatekeepers of the global oil supply and price. Secondarily, they are interested in maintaining close relations with the US, which guarantees their national security. OPEC supply easing at this juncture is obviously beneficial to Biden ahead of the US midterm election in November. But there is not yet an understanding on this front because the US is also negotiating to rejoin the 2015 nuclear agreement with Iran, which Saudi Arabia and the Gulf states oppose. Biden’s trip to the Gulf suggests that nothing is settled yet. The OPEC production increase is not proof alone that the US is breaking off talks with Iran. If the Gulf states thought the US were going to strike a deal with Iran, they might produce more oil to preempt the deal and grab more market share, which is what they did in 2014 in advance of the original 2015 US-Iran nuclear deal. The Saudis do not want US shale producers and Iranian exporters to form an unholy alliance that steals market share and compromises Saudi security. Still, we expect the US-Iran deal to fall apart. The Biden administration does not have a unified international coalition to enforce sanctions on Iran. Nor does it have the political capital or longevity to give Iran credible security guarantees that would convince it to freeze its nuclear program. Recent events support our view. The UN atomic watchdog says that Iran’s stockpile of highly enriched uranium has risen by 30% in three months. Meanwhile the US seized an Iranian tanker off Greece, Iran seized two Greek tankers, and Greece warned about dangers to shipping in the Persian Gulf. To develop a better understanding between Biden and MBS, the US needs to assure the Saudis that it will not renew the deal with Iran. The Saudis will not provide oil at Biden’s whim but they may provide if they have satisfaction that the US will scrap the deal, or otherwise compensate them, such as through increased defense assistance (which Biden threatened to cut off when he entered office). Investors should expect OPEC to fall short of its current promises – and yet to try to provide the minimum production increases necessary to prevent a destabilizing oil spike. OPEC’s interest is to make a windfall for as long as possible, which means not killing the cycle out of greed. This policy could be positive for oil prices after the immediate downward price adjustment. But for now investors should merely expect oil volatility as the EU’s embargo enforcement, Russian retaliation, Russian oil production, OPEC implementation, and US sanctions on Iran are all up in the air. A successful US-Iran deal would deepen the drop in oil prices. But odds are 60/40 that that deal will fail, leading to an escalation of tensions in the Middle East. Biden will have to underscore the US’s red line against Iranian nuclear weaponization. Oil supply disruptions will increase in frequency across the region. Bottom Line: OPEC has given Biden’s anti-inflation campaign a boost but it is too soon to declare that oil prices will substantially abate. The US-Iran deal will likely fail, increasing Middle Eastern instability and supply risks. Investment Takeaways Given that we expect continued volatility in the oil space, we are booking a 14% gain on our long small cap energy versus large cap energy trade. We are also booking a 16.5% gain on our overweight position in the oil and gas transportation and storage sub-sector. We will revisit these trades in future reports. Overall we maintain a defensive portfolio strategy. Biden’s anti-inflation campaign is meeting with some success in the Middle East but the US confrontation with Russia and the likely failure of US-Iran talks suggests that price spikes can still kill more demand and lead to further growth upsets. Matt Gertken Senior Vice President Chief US Political Strategist mattg@bcaresearch.com Footnotes 1 See Joseph R. Biden, Jr, “Joe Biden: My Plan for Fighting Inflation,” Wall Street Journal, May 30, 2022, wsj.com. 2 See Lawrence H. Summers and Alex Domash, “History Suggests a High Chance of Recession over the Next 24 Months,” Harvard Kennedy School, March 15, 2022, www.hks.harvard.edu. 3 See Antony J. Blinken, “The Administration’s Approach to the People’s Republic of China,” US Department of State, May 26, 2022, state.gov. Strategic View Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Table A2Political Risk Matrix

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Table A3US Political Capital Index

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart A1Presidential Election Model

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Chart A2Senate Election Model

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Table A4House Election Model

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Table A5APolitical Capital: White House And Congress

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Table A5BPolitical Capital: Household And Business Sentiment

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Table A5CPolitical Capital: The Economy And Markets

Biden's Anti-Inflation Campaign

Biden's Anti-Inflation Campaign

Executive Summary Investors face a dilemma. The faster that inflation comes down, the better it will be for valuations via a stronger rally in the bond price. But if a collapse in inflation requires a sharp deceleration in growth, the worse it will be for profits. Bond yields are likely in a peaking process, but the sharpest declines may come a few months down the road, after an unambiguous roll-over in food and energy inflation. The stock market’s valuation-driven sell-off is likely over, but the danger is that it morphs into a profits-driven sell-off. As such, the stock market will remain under pressure through 2022, though it is likely to be higher 12 months from now in June 2023. High conviction recommendation: Overweight healthcare versus basic resources. In other words, tilt towards sectors that benefit the most from rising bond prices and that suffer the least from contracting profits. New high conviction recommendation: Go long the Japanese yen. As bond yield differentials re-tighten, the yen will rally. Additionally, the yen will benefit from its haven status in a period of recessionary risk. Fractal trading watchlist: JPY/USD, GBP/USD, and Australian basic resources. If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

Bottom Line: The risk is that the valuation-driven sell-off morphs into a profits-driven sell-off. Feature In May, many stock markets reached the drawdown of 20 percent that defines a technical bear market. Yet what has caught many people off guard is that the bear market in stocks has happened during a bull market in profits. Since the start of 2022, US profits are up by 5 percent.1 The bear market in stocks has happened during a bull market in profits… so far. This shatters the shibboleth that bear markets only happen when there is a profits recession. The 2022 bear market has been a valuation-driven bear market. US profits rose 5 percent, but the multiple paid for those profits collapsed by 25 percent, taking the market into bear territory. None of this should come as any surprise to our regular readers. As we have pointed out many times, a stock market can be likened to a bond with a variable rather than a fixed income. So, just as with a bond, every stock market has a ‘duration’ which establishes which bond it most behaves like. It turns out that that long-duration US stock market has the same duration as a 30-year bond. This means that: The US stock market = (The 30-year T-bond price) multiplied by (US profits) It follows that if the 30-year bond price falls by more than profits rise, then the stock market will sell off. And if the 30-year bond price falls by much more than profits rise, then the stock market will enter a valuation-driven bear market. Therein lies the story of 2022 so far (Chart I-1). Chart I-1The Bear Market Is Valuation-Driven. Profits Are Up... For Now

The Bear Market Is Valuation-Driven. Profits Are Up... For Now

The Bear Market Is Valuation-Driven. Profits Are Up... For Now

Just As In 1981-82, Will The Sell-Off Morph From Valuation-Driven To Profits-Driven? In Markets Echo 1981, When Stagflation Morphed Into Recession, we argued that a good template for what happens to the economy and the markets in 2022-23 is the experience of 1981-82. Does 2022-23 = 1981-82? Then, just as now, the world’s central banks were obsessed with ‘breaking the back’ of inflation, and piloting the economy to a ‘soft landing’. Then, just as now, the central banks were desperate to repair their badly damaged credibility in managing the economy. And then, just as now, an invasion-led war between two major commodity producers – Iran and Iraq – was disrupting commodity supplies and adding to inflationary pressures. In 1981, just as now, the equity market sell-off started as a valuation sell-off, driven by a declining 30-year T-bond price. Profits held up through most of 1981, just as they have so far in 2022. In September 1981, US core inflation finally peaked, with bond yields following soon after. In the current experience, March 2022 appears to have marked the equivalent peak in US core inflation (Chart I-2 and Chart I-3). Chart I-2Does September 1981...

Does September 1981...

Does September 1981...

Chart I-3...Equal March 2022?

...Equal March 2022?

...Equal March 2022?

In late 1981, when the 30-year T-bond price rebounded, the good news was that beaten-down equity valuations also reached their low point. The bad news was that just as the valuation-driven sell-off ended, profits keeled over, and the valuation-driven sell-off morphed into a profits-driven sell-off (Chart I-4). In 2022-23, could history repeat? Chart I-4In September 1981, The Sell-Off Morphed From Valuation-Driven To Profits-Driven

In September 1981, The Sell-Off Morphed From Valuation-Driven To Profits-Driven

In September 1981, The Sell-Off Morphed From Valuation-Driven To Profits-Driven

Recession Or No Recession? That Is Not The Question History rhymes, it rarely repeats exactly. What if the 2022-23 experience can avoid the outright economic recession of the 1981-82 experience? This brings us to another shibboleth that needs to be shattered. You don’t need the economy to go into recession for profits to go into recession. To understand why, we need to visit the concept of operational leverage. Profits is a small number that comes from the difference of two large numbers: sales and the costs of generating those sales. As any company will tell you, sales can be volatile, but costs – which are dominated by wages – are sticky and much slower to change. The upshot is that if sales growth exceeds costs growth, there is a massively leveraged impact on profits growth. This is the magic of operational leverage. But if sales growth falls below sticky cost growth, the magic turns into a curse. The operational leverage goes into reverse, and profits collapse. Using US stock market profits as an example, the magic turns into a curse at real GDP growth of 1.25 percent, above which profits grow at six times the difference, and below which profits shrink at six times the difference (Chart I-5). Chart I-5A Model For US Profits Growth: (Real GDP Growth - 1.25) Times 6

A Model For US Profits Growth: (Real GDP Growth - 1.25) Times 6

A Model For US Profits Growth: (Real GDP Growth - 1.25) Times 6

Strictly speaking, we should compare US profits growth with world GDP growth because multinationals generate their sales globally rather than domestically. But to the extent that the US has both the world’s largest stock market and the world’s largest economy, it is a reasonable comparison. We should also compare both profits and sales in either nominal or real terms, rather than a mixture. But even with these tweaks, we would still find that the dominant driver of profit growth is operational leverage. ‘Recession or no recession?’ is a somewhat moot question, because even non-recessionary low growth is enough to tip profits into contraction. Therefore, the conclusion still stands – ‘recession or no recession?’ is a somewhat moot question, because even non-recessionary low growth is enough to tip profits into contraction. Such a period of low growth is now likely. If 2022-23 = 1981-82, What Happens Next? To repeat: The US stock market = (The 30-year T-bond price) multiplied by (US profits) This means that investors face a dilemma. The faster that inflation comes down, the better it will be for valuations via a stronger rally in the bond price. But if a collapse in inflation requires a sharp deceleration in growth, the worse it will be for profits. This was the precise set-up in December 1981, the equivalent of June 2022 in our historical template. In which case, what can we expect next? 1. Bond yields are likely in a peaking process, but the sharpest declines may come a few months down the road, after an unambiguous roll-over in food and energy inflation (Chart I-6). Chart I-6If 2022-23 = 1981-82, Then This Is What Happens To The Bond Yield

If 2022-23 = 1981-82, Then This Is What Happens To The Bond Yield

If 2022-23 = 1981-82, Then This Is What Happens To The Bond Yield

2. The stock market’s valuation-driven sell-off is likely over, but the danger is that it morphs into a profits-driven sell-off. As such, the stock market will remain under pressure through 2022, though it is likely to be higher 12 months from now in June 2023 (Chart I-7). Chart I-7If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

If 2022-23 = 1981-82, Then This Is What Happens To The Stock Market

3. Long-duration defensive sectors will outperform short-duration cyclical sectors. In other words, tilt towards sectors that benefit the most from rising bond prices and suffer the least from contracting profits. As such, a high conviction recommendation is to overweight healthcare versus basic resources (Chart I-8). Chart I-8If 2022-23 = 1981-82, Then This Is What Happens To Healthcare Versus Resources

If 2022-23 = 1981-82, Then This Is What Happens To Healthcare Versus Resources

If 2022-23 = 1981-82, Then This Is What Happens To Healthcare Versus Resources

4. In foreign exchange, the setup is very bullish for the Japanese yen through the next 12 months. The yen’s recent sell-off is explained by bond yields rising outside Japan. As these bond yield differentials re-tighten, the yen will rally. Additionally, the yen will benefit from its haven status in a period of recessionary risk. A new high conviction recommendation is to go long the Japanese yen (Chart I-9). Chart I-9The Yen's Sell-Off Is Due To Bond Yields Rising Outside Japan

The Yen's Sell-Off Is Due To Bond Yields Rising Outside Japan

The Yen's Sell-Off Is Due To Bond Yields Rising Outside Japan

Fractal Trading Watchlist Supporting our bullish fundamental case for the Japanese yen, the sell-off in JPY/USD has reached the point of fragility on its 260-day fractal structure that marked previous major turning points in 2013 and 2015 (Chart 10). Hence, a first new trade is long JPY/USD, setting the trade length at 6 months, and the profit target and symmetrical stop-loss at 5 percent. Chart I-10The Sell-Off In JPY/USD Has Reached A Potential Turning Point

The Sell-Off In JPY/USD Has Reached A Potential Turning Point

The Sell-Off In JPY/USD Has Reached A Potential Turning Point

Supporting our bearish fundamental case for resources stocks, the outperformance of Australian basic resources has reached the point of fragility on its 130-day fractal structure that marked previous turning points in 2013, 2015, and 2021 (Chart I-11). Hence, a second new trade is short Australian basic resources versus the world market, setting the trade length at 6 months, and the profit target and symmetrical stop-loss at 10 percent. Chart I-11The Australian Basic Resources Sector Is Vulnerable To Reversal

The Australian Basic Resources Sector Is Vulnerable To Reversal

The Australian Basic Resources Sector Is Vulnerable To Reversal

Finally, we are adding GBP/USD to our watchlist, given that its 260-day fractal structure is close to the point of fragility that marked major turns in 2014, 2015, and 2016. Our full watchlist of 29 investments that are at, or approaching turning points, is available on our website: cpt.bcaresearch.com Fractal Trading Watchlist: New Additions GBP/USD At A Turning Point

GBP/USD At A Turning Point

GBP/USD At A Turning Point

Chart 1AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

Chart 2Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Chart 3Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Chart 4US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

Chart 5BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

Chart 6Homebuilders Versus Healthcare Services Has Turned

Homebuilders Versus Healthcare Services Has Turned

Homebuilders Versus Healthcare Services Has Turned

Chart 7CNY/USD Has Reversed

CNY/USD Has Reversed

CNY/USD Has Reversed

Chart 8CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

Chart 9Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Chart 10The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

Chart 11The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

Chart 12FTSE100 Outperformance Vs. Euro Stoxx 50 Is Reversing

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Reversing

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Reversing

Chart 13Netherlands Underperformance Vs. Switzerland Has Been Exhausted

Netherlands Underperformance Vs. Switzerland Has Been Exhausted

Netherlands Underperformance Vs. Switzerland Has Been Exhausted

Chart 14The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

Chart 15The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

Chart 16Food And Beverage Outperformance Has Been Exhausted

Food And Beverage Outperformance Has Been Exhausted

Food And Beverage Outperformance Has Been Exhausted

Chart 17The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

Chart 18The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

Chart 19A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Chart 20Biotech Is A Major Buy

Biotech Is A Major Buy

Biotech Is A Major Buy

Chart 21Norway's Outperformance Could End

Norway's Outperformance Could End

Norway's Outperformance Could End

Chart 22Cotton Versus Platinum Is Reversing

Cotton Versus Platinum Is Reversing

Cotton Versus Platinum Is Reversing

Chart 23Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Chart 24The Rally In USD/EUR Has Ended

The Rally In USD/EUR Has Ended

The Rally In USD/EUR Has Ended

Chart 25The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

Chart 26A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

Chart 27Czech Outperformance Near Exhaustion

Czech Outperformance Near Exhaustion

Czech Outperformance Near Exhaustion

Chart 28US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

Chart 29GBP/USD At A Turning Point

GBP/USD At A Turning Point

GBP/USD At A Turning Point

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 Defined as 12-month forward earnings per share. Fractal Trading System

More On 2022-23 = 1981-82, And The Danger Ahead

More On 2022-23 = 1981-82, And The Danger Ahead

More On 2022-23 = 1981-82, And The Danger Ahead

More On 2022-23 = 1981-82, And The Danger Ahead

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations