Developed Countries

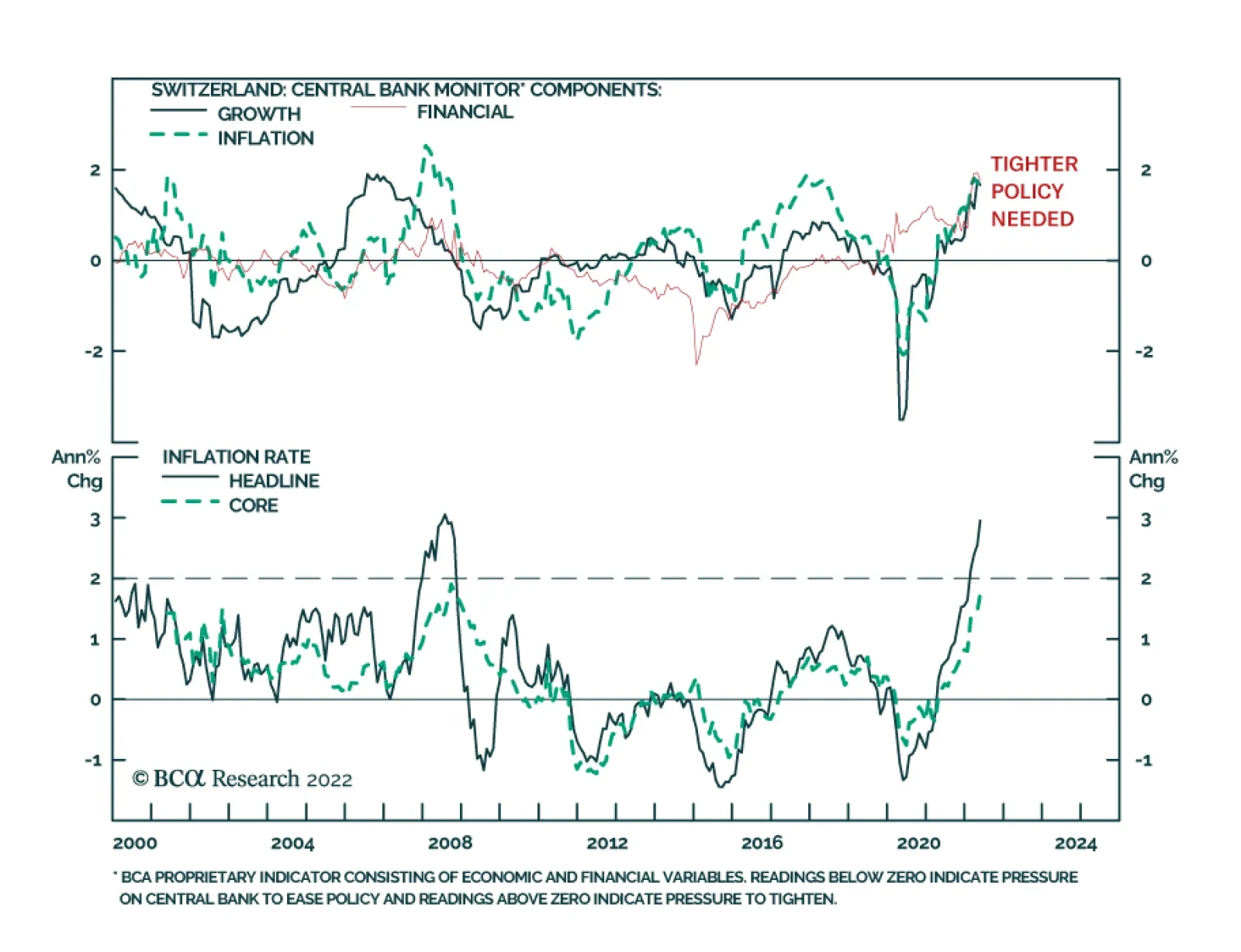

The Swiss National Bank lifted its policy rate by 50bps to -0.25% on Thursday, surprising expectations that it would stand pat and marking its first rate hike in 15 years. In addition, the post-meeting statement noted that “it cannot be ruled out that further…

Executive Summary Was FAANGM A Bubble?

Was FAANGM A Bubble?

Was FAANGM A Bubble?

US inflation has become broad-based, and the labor market is very tight. Wages are a lagging variable, and they will be rising rapidly in the coming months, even as the economy slows. Although US growth will be slowing and global trade will be contracting, the Fed will remain hawkish over the coming months. This is an unprecedented environment and is negative for global and EM risk assets. The US trade-weighted dollar will continue to appreciate as long as the Fed sounds and acts in a hawkish manner and global trade contracts. Consistent with a US dollar overshoot, EM financial markets will undershoot. Even though EM equity and local bond valuations have become attractive, their fundamentals are still negative. A buying opportunity in EM will occur when the Fed makes a dovish pivot and China stimulates more aggressively. We reckon that these conditions will fall into place sometime in H2 this year. Bottom Line: For now, we recommend that investors stay defensive in absolute terms and underweight EM within global equity and credit portfolios. The dollar has more upside in the near term but a major buying opportunity in EM local currency bonds is approaching. Feature Last week, after a two and a half year hiatus, I travelled to Europe to visit clients. I also took the opportunity catch up with Ms. Mea, a global portfolio manager and a long-standing client. Prior to the pandemic, we met regularly to discuss global macro and financial markets. She was happy to resume our in-person meetings, and we met in Amsterdam over dinner last Friday. This report provides the key points of our conversation for the benefit of all clients. Ms. Mea: I am very happy that we are again able to meet in person. Video meetings are good, but in-person meetings are better. One’s body language often gives away their level of confidence regarding investment recommendations. Answer: Agreed. My meetings with clients this week have reminded me of the value of in-person meetings. Chart 1Our Calls On Various EM Asset Classes

Our Calls On Various EM Asset Classes

Our Calls On Various EM Asset Classes

Ms. Mea: Before our meeting I reviewed the evolution of your investment views since the pandemic erupted. Let me try to summarize them, and correct me if I miss something. Even though you upgraded your medium-term view on Chinese growth in May 2020 due to the stimulus, you remained skeptical of the rally in global risk assets. In Q2 2020, you upgraded your stance on EM bonds and in July 2020 you lifted the recommended allocation to EM equities and currencies from underweight to neutral (Chart 1). In the summer and fall of 2020, you were still wary of a deflationary relapse in developed economies. However, since January 2021, your outlook for the US shifted drastically to overheating and inflation. Since then, you have been very vocal about inflation risks in the US. At the same time, you have been warning about a major slowdown in Chinese growth. Regarding financial markets, in March 2021, you downgraded EM stocks and bonds to underweight and recommended shorting select EM currencies versus the US dollar (Chart 1). I should say that your call on US inflation and China’s slowdown have played out very well over the past 18 months. Let’s zero in on US inflation. It was just last year that many investors and analysts claimed that inflation is good for stocks because it helps their top line growth. Why then have global markets panicked? Chart 2Record Wealth Destruction In US Stocks And Bonds

Record Wealth Destruction In US Stocks And Bonds

Record Wealth Destruction In US Stocks And Bonds

Answer: Not many people have a deep understanding of inflation and its impact on financial markets because most investors lack experience in navigating financial markets during an inflation era. In fact, the US equity and bond market selloffs of the past 12 months have wiped out about $12 trillion and $3.5 trillion off their respective market value. This adds up to a combined $15.5 trillion or about 60% of US GDP and already exceeds the wipeouts during the March 2020 crash and all other bear markets (Chart 2). The way we think about macro and markets must change in an inflation regime. In our seminal February 25, 2021 Special Report titled A Paradigm Shift In The Stock-Bond Relationship, we made the case that the US economy and its financial markets were about to enter a new paradigm of higher inflation. We argued that US core CPI would spike well above 2% and US share prices and US government bond yields would become negatively correlated. A similar paradigm shift occurred in 1966 (Chart 3). In short, we argued that the era of low US inflation was over, and as a result, equities and bonds would selloff simultaneously. This will remain the roadmap for investors as long as core inflation is high. Chart 3A Paradigm Shift: US Stock Prices And Bond Yields Correlation Over Decades

A Paradigm Shift: US Stock Prices And Bond Yields Correlation Over Decades

A Paradigm Shift: US Stock Prices And Bond Yields Correlation Over Decades

Ms. Mea: Do you think the Fed is behind the curve? Answer: Yes, the Fed has fallen behind the curve, and, as we have repeatedly argued over the past 12 months, the US inflation genie is out of the bottle. There is a lot of confusion in the global investment community about how we should think about inflation, and about how and when the various measures of inflation matter. As consumers, we care about headline inflation because it affects our purchasing power. So, changes in all goods and service prices, including energy and food, matter to consumers. However, this does not mean that central banks should target and set policy based on headline inflation. Rather, central banks should target genuine broad-based inflation in the economy before it becomes entrenched. Ms. Mea: Can you explain why in certain cases a surge in energy, food and other prices leads to entrenched inflation but in other cases it does not? Answer: Let me give you an example. When consumers experience rapidly rising food and energy prices, they will likely demand faster wage growth from their employers. If businesses are enjoying strong demand for their goods/services and facing a tight labor market, they might have little choice but to agree to pay raises to sustain their business. Companies will then attempt to protect their profit margins by hiking their selling prices. Households may accept higher prices given their incomes are rising. This dynamic could cause inflation to become broad-based and entrenched. In this case, central banks should lift rates to slow the economy materially and cool off the labor market to end the wage-price spiral. If employees fail to negotiate hefty pay raises, odds are that inflation will not become broad-based. The more households spend on energy and food, the less income they will have to spend on other items, causing their discretionary spending to contract. In this case, there is no rush for central banks to tighten policy. If monetary authorities tighten materially, the economy will experience a full-fledged recession. In short, wage dynamics will determine whether inflation becomes broad-based. Labor market conditions will ultimately dictate this outcome. Ms. Mea: But why are wages more important than the price of fuel or food in determining whether inflation becomes broad-based? Answer: To be technically correct, unit labor costs, not wages, are key to inflation dynamics. Unit labor cost = (wage per hour) / (productivity). Productivity is output per hour. Given that labor is the largest cost component of US businesses, unit labor costs will swell and profit margins will shrink when salaries rise faster than productivity. CEOs and business owners always do their best to protect the their profit margins. Thus, accelerating unit labor costs will lead them to raise their selling prices. In the wake of wage gains, consumers might accept higher goods and service prices. If they do and go on to demand even higher wages, the economy will enter a wage-price spiral. This is why wage costs, more specifically unit labor costs, are the most important variable to monitor. If high energy and food prices lead employees to demand faster wage growth from their employers, and if they are granted wage increases above and beyond their productivity advances, inflation will become more broad-based and genuine. If consumers push back against higher prices, i.e., reduce their spending, corporate profits will plunge, and companies will freeze investment and lay off employees. Wages will slow and inflation will wane. Ms. Mea: Are all economies currently experiencing a wage-price spiral? Answer: The US and some other countries have been experiencing a wage-price spiral over the past 12 months. In other countries, including many developing economies, a wage-price spiral is currently absent. In the US, labor demand exceeds supply by the widest margin since 1950 (Chart 4). The upshot is that wages will continue to rise in response to persistently high inflation (Chart 5). Chart 4US Labor Demand Is Exceeding Labor Supply By The Widest Margin Since 1950

US Labor Demand Is Exceeding Labor Supply By The Widest Margin Since 1950

US Labor Demand Is Exceeding Labor Supply By The Widest Margin Since 1950

Chart 5US Wage Growth Is Already Very High

US Wage Growth Is Already Very High

US Wage Growth Is Already Very High

Wages in the US are currently rising at a rate of 6-6.5% or so. US productivity growth is around 1.5%. As a result, unit labor costs are rising at a 4.5-5% annual rate, the fastest rate for corporate America in the past 40 years (Chart 6). As Chart 6 demonstrates, unit labor costs have been instrumental in defining core CPI fluctuations over the past 70 years in the US. Chart 6US Unit Labor Costs Are Rising At The Fastest Rate Since 1982

US Unit Labor Costs Are Rising At The Fastest Rate Since 1982

US Unit Labor Costs Are Rising At The Fastest Rate Since 1982

Chart 7US Core Of Core Inflation Is High And Not Falling

US Core Of Core Inflation Is High And Not Falling

US Core Of Core Inflation Is High And Not Falling

In short, both surging unit labor costs and the acceleration of super core CPI measures like trimmed-mean CPI and median CPI suggest that US inflation has become broad-based and a wage-inflation spiral has taken hold in the US (Chart 7). Critically, wages are a lagging variable and are not reset all at once for all employees. American employees will continue to demand substantial wage hikes both to offset the last 12 months of lost purchasing power and to protect their purchasing power for the next 12 months. Hence, we will be witnessing faster wage growth in the coming months even as the economy slows. For many continental European economies and for several EM economies, wage growth is still weak. Chart 8 illustrates that nominal wage growth in India, Indonesia, China and Mexico are very subdued. Sluggish wage gains in emerging economies are consistent with the profile of their domestic demand. Domestic demand in these large developing economies remains extremely weak. In many cases, the level of domestic demand in real terms is still below its pre-pandemic level (Chart 9). Chart 8EM Wages Are Very Tame

EM Wages Are Very Tame

EM Wages Are Very Tame

Chart 9EM Domestic Demand Is Depressed

EM Domestic Demand Is Depressed

EM Domestic Demand Is Depressed

In China, deflation, rather than inflation, is the main economic threat. Headline and core inflation are within a 1-2% range (Chart 10), domestic demand is very weak, and the unemployment rate has risen in the past 12 months. Chart 10China's Inflation Is Subdued

China's Inflation Is Subdued

China's Inflation Is Subdued

Ms. Mea: Do you expect the US economy to contract? Answer: US growth will decelerate substantially, and certain segments of the economy could shrink for a couple of quarters. My expectation is that US corporate profits will contract materially. Slowing top line growth, narrowing profit margins, shrinking global trade and a strong dollar are all major headwinds for the S&P 500 EPS. EM EPS are also heading towards a major contraction. This is why I view EM fundamentals as negative even though EM valuations have become attractive. Ms. Mea: You have recently written that global trade volumes are about to contract. What is your rationale and is there any evidence that this is already happening? Answer: US and EU demand for consumer goods ex-autos has been booming over the past two years. Households have overspent on goods ex-autos (Chart 11). Given that their disposable income is contracting in real terms and a preference to spend on services, households will markedly curtail their purchases of consumer goods in the coming months. This will hurt global manufacturing in general, and emerging Asia in particular. Some forward-looking indicators are already signaling a contraction in global trade: US retail inventories (in real terms) have swelled (Chart 12, top panel). US retailers will dramatically reduce their orders. Chart 11Global Trade Volumes Will Shrink In H2 2022

Global Trade Volumes Will Shrink In H2 2022

Global Trade Volumes Will Shrink In H2 2022

Chart 12US Import Volumes Are Set To Contract

US Import Volumes Are Set To Contract

US Import Volumes Are Set To Contract

Besides, US railroad carload is already shrinking, signaling reduced goods shipments (Chart 12, bottom panel). Taiwanese shipments to China lead global trade and they point to an impending slump (Chart 13, top panel). Also, the Taiwanese manufacturing shipments-to-inventory ratio has dropped below 1 (Chart 13, bottom panel). Finally, industrial metal prices are breaking down despite easing lockdowns in China and continued sanctions on Russia (Chart 14). This is a sign of downshifting global manufacturing. Chart 13A Red Flag For Global Trade

A Red Flag For Global Trade

A Red Flag For Global Trade

Chart 14Industrial Metal Prices Are Breaking Down

Industrial Metal Prices Are Breaking Down

Industrial Metal Prices Are Breaking Down

Ms. Mea: Won’t a global trade contraction push down goods prices and help US inflation? Answer: Correct, it will bring down US goods inflation but not services inflation. Importantly, as we discussed above, US inflation has already spilled into wages and has become broad-based. Plus, it is hovering well above the Fed’s target. Hence, the Fed cannot dial down its hawkishness now, even if goods price inflation drops significantly. In brief, even though US growth will be slowing and global trade will be contracting over the coming months, the Fed is likely to remain hawkish. This is an unprecedented environment and is negative for global and EM risk assets. Ms. Mea: What are the financial market implications of entrenched inflation in the US and the lack of genuine inflationary pressures in many emerging economies? Answer: As long as the Fed sounds and acts in a hawkish manner and/or global trade contracts, the US trade-weighted dollar will continue to appreciate. The greenback is a countercyclical currency and rallies when global trade slumps. On the whole, the USD will likely overshoot in the near run. Consistent with a US dollar overshoot, EM financial markets will undershoot. Even though investor sentiment on EM equities and USD bonds is very low (Chart 15), a final capitulation selloff is still likely. In short, EM valuation and positioning are positive for future potential returns yet their fundamentals (business cycle, profits, return on capital, etc.) are still negative. A buying opportunity in EM will emerge when the Fed makes a dovish pivot, China stimulates more aggressively, and EM equity and bond valuations improve further. We reckon that these conditions will fall into place sometime in H2 this year. If the Fed turns dovish early without taming US inflation, it will fall behind the inflation curve and the US dollar will begin its bear market. Investors will respond by embracing EM financial assets. EM local currency bonds in particular offer value (Chart 16). Prudent macro policies and the lack of wage pressures entail a good medium-to-long term opportunity in EM local currency bonds. Chart 15Investor Sentiment On EM Stocks And USD Bonds Is Low

Investor Sentiment On EM Stocks And USD Bonds Is Low

Investor Sentiment On EM Stocks And USD Bonds Is Low

Chart 16US TIPS Yields Should Roll Over For EM Local Bond Yields To Decline

US TIPS Yields Should Roll Over For EM Local Bond Yields To Decline

US TIPS Yields Should Roll Over For EM Local Bond Yields To Decline

As EM currencies put in a bottom, local yields will come down. This will help their equity markets. Ms. Mea: Speaking of a capitulation selloff, how far can it go? Both for EM stocks as well as the S&P 500? Chart 17S&P500: Where Is Technical Support Line?

S&P500: Where Is Technical Support Line?

S&P500: Where Is Technical Support Line?

Answer: As long as US bond yields and oil prices do not start falling on a consistent basis, the S&P 500 will remain under selling pressure. Technicals can help us gauge the likely magnitude of the move. The S&P 500 has dropped to a major technical support, but it will likely be broken. The next support is around 3100-3200 (Chart 17). The EM equity index is sitting on a technical support now (Chart 18). The next support level is 15-17% below the current one. Chart 18EM Stocks in USD Terms Could Drop Another 15%

EM Stocks in USD Terms Could Drop Another 15%

EM Stocks in USD Terms Could Drop Another 15%

Critically, US equity investors should also consider whether the US equity bull market that has been in place since 2009 is over. If it is, then the S&P 500 bear market could last long, and prices could drop significantly. Chart 19Was FAANGM A Bubble?

Was FAANGM A Bubble?

Was FAANGM A Bubble?

A few observations that investors should keep in mind: First, over the past 12 years, FAANGM stocks have followed the profile of the Nasdaq 100 (Chart 19). In short, FAANGM stocks have risen as much as the Nasdaq 100 index did in the 1990s. Second, when retail investors rush into an asset class, it often signals the final phase of the bull market. Once the bull market ends, the ensuing bear market is vicious. The behavior of tech/internet stocks and the broader S&P 500 fits this profile extremely well. For several years after the Lehman crash, individual investors were hesitant to buy US stocks. However, the resilience of US equities led to a buy the dip mentality in 2019-20. Retail investors joined the equity party en masse in early 2020. The post retail frenzy hangover is usually very painful and prolonged. Based on this roadmap, it seems that the 2020-21 retail-driven rally was the final upleg in the S&P 500 bull market. By extension, we have entered a bear market that could be vicious and extended. All the excesses of the 10-year FAANGM and S&P500 bull markets will need to be worked out before a new bull market emerges. Finally, a high inflation regime raises the bar for the Fed to rescue the stock market. This also entails lower equity multiples than we have in the S&P500 now. Ms. Mea: What do you make of EM’s recent outperformance versus DM stocks? When will you upgrade EM versus DM? Answer: Indeed, EM stocks have recently outperformed DM stocks. We might be witnessing a major transition in global equity market leadership. We have held for some time that an equity leadership change from the US to the rest of the world and from TMT stocks to other segments of the global equity market would likely take place during or following a major market selloff. The ongoing equity bear market seems to be exactly that catalyst. Chart 20For EM Equities To Outperform, USD Needs To Weaken

For EM Equities To Outperform, USD Needs To Weaken

For EM Equities To Outperform, USD Needs To Weaken

If the S&P 500 bull market is over, the global equity leadership will also change away from US and TMT stocks to other stock markets and sectors. That said, to upgrade EM stocks, we need to change our view on the USD because EM relative equity performance versus DM closely tracks the inverted trade-weighted US dollar (Chart 20). In the near term, we believe the greenback has more upside potential. In particular, Asian currencies and equity markets cannot outperform when the Fed is hawkish and global trade is contracting. Latin American currencies have benefited since early this year from the spike in commodity prices. However, worries about a US recession, a strong dollar and a lack of strong recovery in the Chinese economy will push industrial metal prices lower. As shown in Chart 14 above, industrial metal prices are breaking down. This is a bad omen for Latin American markets. On the whole, we will likely be upgrading EM versus DM later this year. For now, we recommend that investors stay defensive and underweight EM within global equity and credit portfolios. We also continue to short the following currencies versus the USD: ZAR, COP, PEN, PLN, PHP and IDR; as well as HUF vs. CZK, and KRW vs. JPY. A major buying opportunity in local currency bonds is approaching. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com

Executive Summary

Does Powell Need To Channel His Inner Volcker?

Does Powell Need To Channel His Inner Volcker?

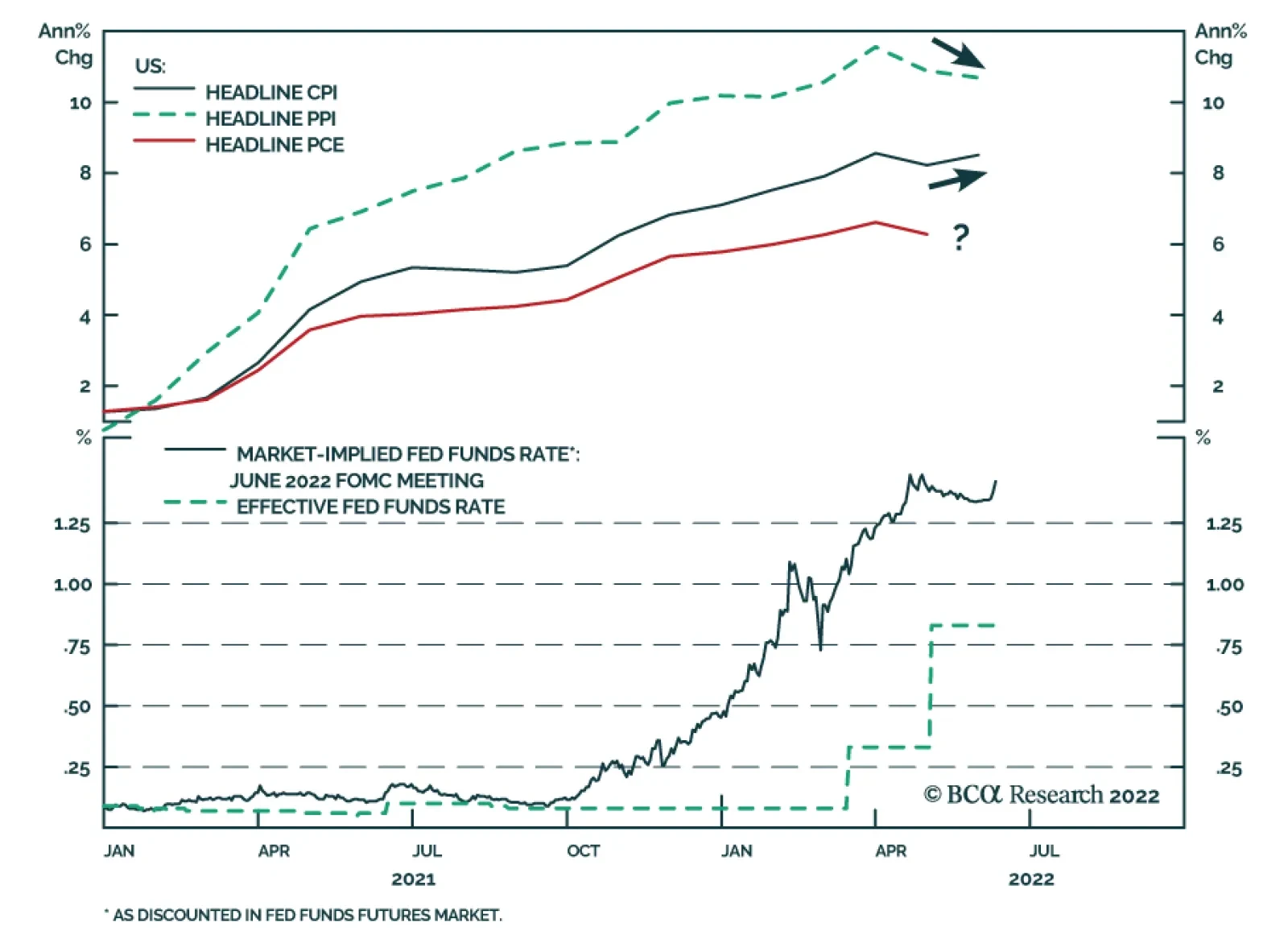

Economic growth is now a casualty, and not a driver, of monetary policy choices. Inflation is dictating where central banks are taking interest rates. Our baseline view remains that core US inflation will cool by enough on its own without the need for the Fed to deliver a policy-induced recession. However, the odds of the latter have increased after the upside surprise in the May US CPI report. The ECB has been dragged into the same morass as other major central banks – tightening policy because of soaring inflation, despite broad-based signs of sluggish economic growth. We still see the pricing of cumulative rate hikes in the euro area as being too aggressive, even after last week’s clear announcement from the ECB that a string of future rate hikes was coming. With the ECB also announcing an end to its QE program, but offering no details on a replacement, markets have been given the green light to push Italian yields/spreads higher (and the euro lower) until there is an ECB response to market fragmentation in European sovereign debt. Bottom Line: The Fed is still more likely than the ECB to follow through on rate hikes discounted in US and European interest rate curves - position for renewed widening of the Treasury-Bund spread. Italian bond yields will remain under upward pressure until the contours of an ECB plan to stabilize Peripheral Spreads alongside rate hikes are revealed – tactically position for a wider BTP-Bund spread. Central Bankers Cannot Worry About Growth … Or Your Investment Portfolio The US consumer price index (CPI) report for May was yet another bond-bearish shock in a year full of them. With US headline US inflation hitting an 41-year high of 8.6%, the Treasury market adjusted bond yields upward to reflect both higher inflation expectations and even more aggressive Fed tightening. Coming only a day after the June European Central Bank (ECB) meeting that provided guidance that a series of rate hikes would begin in July, that could include a 50bp hike at the September meeting, financial markets worldwide moved to price in the risk that policy-induced recessions were the only way to bring down soaring global inflation. The result: global bond yields soared to new highs for the year, while risk assets of all shapes and sizes were hammered. We have our doubts that today’s class of policymakers – especially the Fed - has the stomach to repeat the actions of former Fed Chair Paul Volcker, who famously pushed US interest rates above the double-digit inflation rates of the late 1970s to engineer a deep recession to crush inflation. The starting point of the current tightening cycle is even further behind the curve than during the Volcker era, in terms of “realized” real interest rates, with the 10-year US Treasury yield now over five percentage points below headline US CPI inflation (Chart 1). Related Report Global Fixed Income StrategyAssessing The Risks To Our Main Views Central bankers are now faced with the no-win scenario of pushing nominal policy rates higher to chase soaring inflation in a bid to maintain inflation fighting credibility, regardless of the spillover effects on financial market stability or economic growth expectations. More worryingly, the rate hikes needed to establish that credibility are not only becoming more frequent but larger. 50bps has become the “standard” size for developed market rate hikes. The Fed may have upped the ante with the 75bp hike at yesterday's FOMC meeting. Such is the reality of a funds rate still only at 1.75% but with US inflation pushing toward 9%. The timing of the latest hawkish shifts from the Fed, ECB and others is surprising, looking purely from a growth perspective. The OECD leading economic indicators for the US, euro area and China are slowing, alongside depressed consumer confidence and deteriorating business sentiment (Chart 2). Similar readings are evident in comparable measures in other major economies, both in developed and emerging economies. This would normally be the type of backdrop that would entice central banks to consider easing monetary policy - IF inflation was subdued, which is clearly not the case today. Chart 1Does Powell Need To Channel His Inner Volcker?

Does Powell Need To Channel His Inner Volcker?

Does Powell Need To Channel His Inner Volcker?

In fact, high inflation is the reason why economic sentiment has worsened. Chart 2Worrying Signs For Global Growth

Worrying Signs For Global Growth

Worrying Signs For Global Growth

Consumers see income growth that is lagging inflation, especially for everyday items like gasoline and food. Businesses are seeing input costs rising, especially for labor in an environment of tight job markets. Inflation has become broad-based, across goods, services and wages. This is true for countries that are more advanced in their monetary tightening cycles - the US, Canada and the UK - where inflation rates are remarkably similar (Chart 3). But it is also now true in countries with lower (but still accelerating) inflation rates and where central banks have been slower to tighten monetary conditions, like the euro area and Australia (Chart 4). Chart 3Inflation Turning More 'Domestic' (Services / Wages) Here

Inflation Turning More 'Domestic' (Services / Wages) Here

Inflation Turning More 'Domestic' (Services / Wages) Here

Chart 4Still No Major Services/Wage Inflation Overshoots Here

Still No Major Services/Wage Inflation Overshoots Here

Still No Major Services/Wage Inflation Overshoots Here

For the Fed, assessing the underlying momentum of US inflation, and setting monetary policy accordingly, has become a bit trickier. While headline inflation continues to accelerate in response to rising energy and food prices, core inflation ticked lower in both April and May and now sits at 6.1%, down from 6.5% in March. Longer-term survey-based measures of inflation expectations have been moving steadily higher, with the University of Michigan 5-10 year consumer inflation expectations survey now up to a 14-year high of 3.3% (Chart 5). Yet longer-term market-based inflation expectations have been more stable, with the 10-year TIPS breakeven now at 2.66%, down from the late April peak of 3.02%. There are also some mixed signals visible within the US inflation data. Core goods CPI inflation clocked in at 8.5% in May, down from the recent peak of 12.4% in February 2022, while core services CPI inflation accelerated to a 14-year high of 5.2% in May (Chart 6). A similar divergence can be seen when looking at the Atlanta Fed’s measures of “sticky” and “flexible” price inflation. Core flexible CPI inflation – measuring prices that adjust more rapidly – has fallen from a peak of 19% to 12.3% in May. At the same time, core sticky CPI inflation for prices that are slower to adjust sped up to an 31-year high of 5% in May. Chart 5Some Mixed Inflation Messages For The Fed

Some Mixed Inflation Messages For The Fed

Some Mixed Inflation Messages For The Fed

Chart 6US Inflation Will Eventually Be Lower, But 'Stickier'

US Inflation Will Eventually Be Lower, But 'Stickier'

US Inflation Will Eventually Be Lower, But 'Stickier'

Chart 7Stick With UST-Bund Spread Widening Trades

Stick With UST-Bund Spread Widening Trades

Stick With UST-Bund Spread Widening Trades

In terms of the Fed’s next policy moves, the acceleration of core services (and sticky) inflation means underlying inflation momentum remains strong enough to make it difficult for the Fed to tighten by less than markets are discounting over the next year. Yet the deceleration of core goods (and flexible) inflation, if it continues, can lead to an eventual peak in overall US inflation. This would ease pressure on the Fed to tighten policy more aggressively than markets are expecting to slam the brakes on US economic growth. For nervous markets worried about Fed-induced recession risks, the clear peak in US inflation that we had been expecting has likely been pushed out further into the latter half of 2022. Thus, a significant fall in US Treasury yields that would provide relief to stressed risk assets is unlikely in the near term. Our preferred way to play that upward pressure on US Treasury yields is through an underweight stance on US Treasuries in global bond portfolios, rather than a below-benchmark duration stance. That is particularly true versus German Bunds - the 10-year UST-Bund yield spread is now well below the fair value level from our fundamental valuation model (Chart 7). Bottom Line: It is not clear that the Fed needs to “pull a Volcker” and generate a policy-induced recession to cool off US inflation. However, the Fed is far more likely to hike rates in line with market expectations than the ECB over the next 6-12 months. Stay underweight US Treasuries versus core Europe in global bond portfolios. The ECB Takes The Patient Off Life Support The ECB is finally coming to grips with surging European inflation. At last week’s policy meeting, the ECB Governing Council voted to end new bond buying via the Asset Purchase Program, while also signaling that a 25bp rate hike was on the way in July, with more hikes to follow – perhaps as much as 50bps in September if inflation remains elevated. Chart 8Markets Pricing In A Highly Aggressive ECB

Markets Pricing In A Highly Aggressive ECB

Markets Pricing In A Highly Aggressive ECB

The central bank provided a new set of quarterly economic projections that, unsurprisingly, included significant upward revisions to the inflation forecasts. The 2022 headline HICP inflation forecast was bumped from 5.1% to 6.8%, the 2023 forecast from 2.1% to 3.5% and the 2024 forecast was nudged higher from 1.9% to 2.1%. The projections for core HICP inflation were also increased to 3.3% for 2022, 2.8% for 2023 and 2.3% for 2024. The central bank now expects euro area inflation to stay above its 2% inflation target throughout its forecast period – even with a 20% decline in oil prices, and 36% fall in natural gas prices, built into the projection between 2022 and 2024. A move towards tighter monetary policy has been heralded by our ECB Monitor, which remains elevated largely due to its inflation component (Chart 8). By contrast, the growth component of the Monitor has rolled over and is now at levels consistent with unchanged monetary policy. Yet in the current environment of very elevated inflation, concerns about the economy are taking a back seat to maintaining the ECB’s inflation-fighting credibility. In the relatively young history of the ECB, dating back to the inception of the euro in 1998, there have only been three true hiking cycles that involved multiple interest rate increases: 2000, 2006-08 and 2011. In each case, both growth and inflation were accelerating in a broad-based way across the majority of euro area countries. Today, inflation is surging, with the headline HICP inflation rate hitting 8.1% in May, while core inflation (ex energy and food) is a more subdued but still high 4.4%. Economic growth is decelerating, however, with leading economic indicators now slowing in a majority of euro area countries (Chart 9). Chart 9Coming Up: An Unusual ECB Tightening Cycle That Ignores Growth

Coming Up: An Unusual ECB Tightening Cycle That Ignores Growth

Coming Up: An Unusual ECB Tightening Cycle That Ignores Growth

The ECB’s updated economic growth forecasts were downgraded for this year and next, with real GDP growth now expected to reach 2.8% in 2022 and 2.1% in both 2023 and 2024. Cutting growth forecasts for the current year was inevitable given the uncertainties stemming from the Ukraine war and soaring European energy prices. However, the projected growth rates do seem optimistic in the face of deeply depressed readings on economic sentiment from reliable measures like the ZEW index or the European Commission consumer confidence index, both of which have fallen sharply to levels last seen during the 2020 pandemic shock (Chart 10). Demand for European exports is also sluggish, particularly exports to China which are now flat in year-over-year terms. A similar pattern can be seen in the ECB’s inflation forecasts, which seem too optimistic in projecting lower wage growth and core inflation through 2024, even with the euro area unemployment rate forecasted to stay below 7% - under the OECD’s full employment estimate of 7.7% over the same period (Chart 11). Chart 10Overly Optimistic ECB Growth Forecasts

Overly Optimistic ECB Growth Forecasts

Overly Optimistic ECB Growth Forecasts

Chart 11Overly Optimistic ECB Inflation Forecasts?

Overly Optimistic ECB Inflation Forecasts?

Overly Optimistic ECB Inflation Forecasts?

The ECB is facing the same communications problem as other central banks at the moment. There is a fear of forecasting a major growth slowdown that would scare financial markets, even though that is a necessary condition to help bring down elevated inflation. At the same time, projections of a big decline in inflation that would limit the need for economy-crushing monetary tightening are not credible in the current environment of historically elevated headline inflation with very low unemployment rates. Interest rate markets understand the bind that the ECB finds itself in, and have moved to price in a very rapid jump in policy rates over the next 1-2 years. The 1-month OIS rate, 2-years forward is now at 2.5%, a high level compared to estimates of the neutral ECB policy rate, which lies between 1-1.5%. Core European bond yields have moved up alongside those rising rate expectations, with the 10-year German bund yield now at 1.64%, a far cry from the -0.18% yield at the start of 2022. Additional German yield increases will prove to be more difficult in the months ahead. There has already been a major upward adjustment in the inflation expectations component of yields, with the 10-year euro CPI swap rate now up to 2.6% compared to 2% at the start of this year (Chart 12). Importantly, those inflation expectations have stabilized of late, even in the face of high oil prices. Meanwhile, real bond yields, while still negative, have also moved up substantially and are now back to levels that prevailed before the ECB introduced negative policy rates in 2014 (bottom panel). With so much bond-bearish news now priced into core European bond yields, additional yield increases from here would require a more fundamental driver – an upward repricing of terminal interest rate expectations. On that note, the German yield curve is signaling that the terminal rate in the euro area is not much above 1.75%, as that is where bond yield forwards have converged to for both long and short maturity bonds (Chart 13). Chart 12How Much Higher Can Bund Yields Realistically Go?

How Much Higher Can Bund Yields Realistically Go?

How Much Higher Can Bund Yields Realistically Go?

Chart 13Markets Signaling A 1.75% Terminal Rate

Markets Signaling A 1.75% Terminal Rate

Markets Signaling A 1.75% Terminal Rate

Given our view that the neutral rate in Europe is, at best, no more than 1.5%, ECB rate hikes much beyond that level would likely invert a Bund curve that is priced for only a 1.75% terminal rate. An inverted Bund curve would also raise the odds that Europe enters a policy-induced recession – turning a bond bearish outcome into a bond bullish one. Even with the relatively aggressive policy expectations priced into European bond yields, it is still too soon to raise European duration exposure with inflation still accelerating. We prefer maintaining a neutral duration stance until there is a clear peak in realized European inflation – an outcome that would also favor a shift into Bund curve steepeners as the markets price out rate hikes and, potentially, begin to discount future rate cuts. Does The ECB Even Have A Plan For Italian Debt? The ECB seems to have a clear near-term plan on the timing, and even the potential size, of rate hikes. There is far less clarity on how it will deal with stabilizing sovereign bond yields post-APP in the countries that benefitted from ECB asset purchases, most notably Italy. By offering no details on a replacement to APP buying of riskier European debt at last week’s policy meeting, markets were given the green light to test the ECB’s resolve by pushing Italian bond yields higher (and the euro lower). Volatility in both markets will continue until there is a credible ECB response to so-called “market fragmentation” in European sovereign debt (i.e. higher yields and wider spreads versus Bunds in the Periphery). With the benchmark 10-year Italian BTP yield pushing above 4%, the ECB tried to calm markets yesterday by announcing an emergency meeting of the Governing Council to discuss “anti-fragmentation” policy options. The announcement triggered a relief rally in BTP prices, likely fueled by short covering. But the ECB statement was again light on concrete details, only noting that: a) reinvestments from maturing bonds from the now-completed Pandemic Emergency Purchase Program (PEPP) could be used “flexibly” to support stressed parts of the European bond market b) the timeline for ECB researchers to prepare proposals for a “new anti-fragmentation instrument” would be accelerated. We expect the ECB to eventually produce a credible bond buying plan to support Peripheral European bond markets – but only after an “iterative” trial-and-error process where trial balloon proposals are floated and skeptical financial markets respond. Chart 14Stay Cautious On Italian Government Bonds

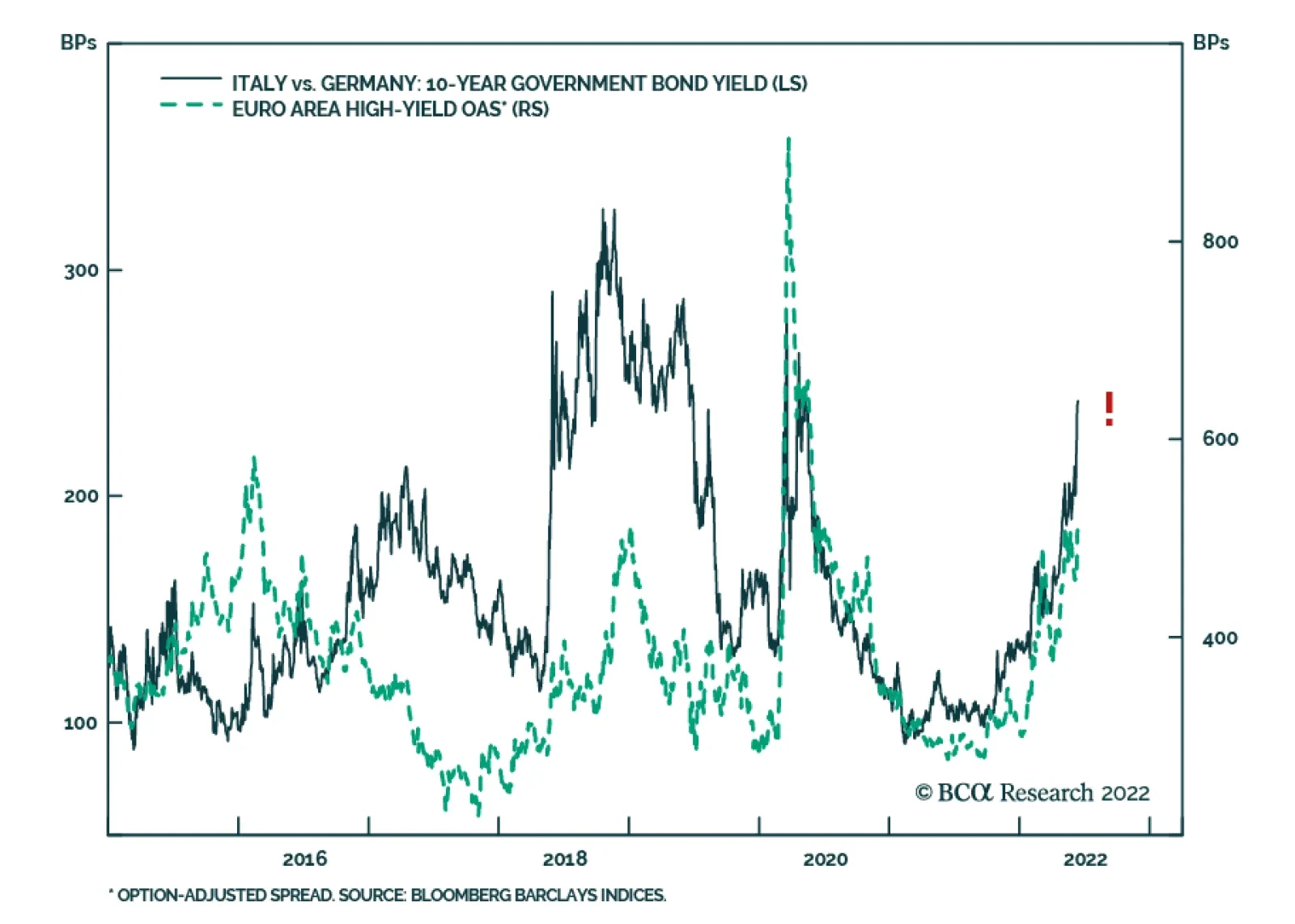

Stay Cautious On Italian Government Bonds

Stay Cautious On Italian Government Bonds

There is almost certainly some serious horse trading going on within the ECB Governing Council, with inflation hawks demanding more rate hikes in exchange for their support of new plans to deal with market fragmentation. Details such as the size of any new program, the conditions under which it would be activated, and country purchase limits (if any) will need to be ironed out. Internal ECB debates will prolong that trial-and-error process with financial markets, keeping yield/spread/FX volatility elevated in the short-term. On a strategic (6-18 month) time horizon, we see a neutral allocation to Italy in global bond portfolios as appropriate, given the tradeoff between increasingly attractive yields and the uncertain timing of effective ECB market stabilization proposals. On a more tactical horizon (0-6 months), we expect Italian yields and spreads versus Germany to remain under upward pressure until a viable anti-fragmentation program is announced (Chart 14). To play for that move, we are introducing a new position in our Tactical Overlay Trade portfolio, selling 10-year Italy futures and buying 10-year German Bund futures. The details of the new trade, including the specific futures contracts and weightings for the two legs of the trade to make it duration-neutral, can be found in the Tactical Trade table on page 18. As we monitor and discuss this trade in future reports, we will refer to the well-followed 10-year Italy-Germany spread (currently 225bps) to determine targets and stop levels of this bond futures spread trade. We are setting a stop-out on this trade if the 10-year Italy-Germany spread has a one-day close below 200bps, while targeting a potential widening to 275-300bps (the 2018 peak in that spread). Bottom Line: The ECB’s lack of conviction on designing a plan to support Peripheral bond markets during the upcoming period of interest rate hikes will keep upward pressure on Peripheral yields/spreads over the next few months. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

Volcker's Ghost

Volcker's Ghost

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index Global Fixed Income - Strategic Recommendations*

Volcker's Ghost

Volcker's Ghost

Tactical Overlay Trades

In lieu of next week’s report, I will host a Webcast on Monday, June 27 to explain the recent market turmoil and how to navigate it through the second half of 2022. Please mark the date, and I do hope you can join. Executive Summary The recent sharp underperformance of the HR and employment services sector presages an imminent rise in the US unemployment rate. Central banks have decided that a recession is a price worth paying to slay inflation. In this sense, the current setup rhymes with 1981-82, when the Paul Volcker Fed made the same decision. The correct investment strategy for stocks, bonds, sectors and FX is to follow the template of 1981-82. In a nutshell, an imminent recession will require a defensive strategy for most of 2022, before a strong recovery in markets unfolds in 2023. Go long the December 2023 Eurodollar (or SOFR) futures contract. While interest rates are likely to overshoot in the near term, the pain that they will unleash will require a commensurate undershoot in 2023-24. Cryptocurrencies will rally strongly once the Nasdaq reaches a near-term bottom, which in turn will depend on a peak in long bond yields. Fractal trading watchlist: Czechia versus Poland, German telecoms, Japanese telecoms, and US utilities. The Underperformance Of Human Resources Warns That The US Jobs Market Is Rolling Over

The Underperformance Of Human Resources Warns That The US Jobs Market Is Rolling Over

The Underperformance Of Human Resources Warns That The US Jobs Market Is Rolling Over

Bottom Line: An imminent recession will require a defensive strategy for most of 2022, before a strong recovery in markets unfolds in 2023. Feature Financial markets have collapsed in 2022, but jobs markets have held firm, at least so far. For example, the US economy has added an average of 500 thousand jobs per month1, and the unemployment rate, at 3.6 percent, remains close to a historic low. But now, an excellent real-time indicator warns that cracks are appearing in the US jobs market. The excellent real-time indicator of the jobs market is the performance of the human resources (HR) and employment services sector. After all, with its role to place and support workers in their jobs, what better pulse for the jobs market could there be than HR? What better pulse for the jobs market could there be than the human resources sector? Worryingly, the recent sharp underperformance of the HR and employment services sector warns that the pulse of the jobs market is weakening, and that consumers will soon be reporting that jobs are becoming less ‘plentiful’ (Chart I-1). In turn, consumers reporting that jobs are becoming less plentiful presages an imminent rise in the unemployment rate (Chart I-2). Chart I-1The Underperformance Of Human Resources Warns That The US Jobs Market Is Rolling Over

The Underperformance Of Human Resources Warns That The US Jobs Market Is Rolling Over

The Underperformance Of Human Resources Warns That The US Jobs Market Is Rolling Over

Chart I-2Jobs Becoming Less 'Plentiful' Presages Higher Unemployment

Jobs Becoming Less 'Plentiful' Presages Higher Unemployment

Jobs Becoming Less 'Plentiful' Presages Higher Unemployment

2 Percent Inflation Will Require A Sharp Rise In Unemployment The health of the jobs market has a huge bearing on the big issue du jour – inflation. Specifically, in the US, the unemployment rate (inversely) drives the inflation of rent and owners’ equivalent rent (OER) because, to put it simply, you need a steady job to pay the rent. Furthermore, with rent and OER comprising almost half of the core CPI basket, the ‘rent of shelter’ component is by far the most important long-term driver of core inflation.2 Shelter inflation at 3.5 percent equates to core inflation at 2 percent. For the past couple of decades, full employment has been consistent with rent of shelter inflation running at 3.5 percent, which itself has been consistent with core inflation running at 2 percent (Chart I-3). Hence, the Fed could achieve the Holy Grail of full employment combined with inflation running close to 2 percent. Chart I-3Core Inflation At 2 Percent = Shelter Inflation At 3.5 Percent...

Core Inflation At 2 Percent = Shelter Inflation At 3.5 Percent...

Core Inflation At 2 Percent = Shelter Inflation At 3.5 Percent...

But here’s the Fed’s problem. In recent months, there has been a major disconnect between the jobs market and rent of shelter inflation. The current state of full employment equates to rent of shelter inflation running not at 3.5 percent, but at 5.5 percent (Chart I-4). Chart I-4...But Full Employment Now = Shelter Inflation At 5.5 Percent

...But Full Employment Now = Shelter Inflation At 5.5 Percent

...But Full Employment Now = Shelter Inflation At 5.5 Percent

This means that to bring rent of shelter and core inflation back to 3.5 percent and 2 percent respectively, the unemployment rate will have to rise by 2 percent. In other words, to achieve its inflation goal, the Fed will have to sacrifice its full employment goal. Put more bluntly, if the Fed wants to reach 2 percent inflation quickly, it will have to take the economy into recession. The cracks appearing in the HR and employment services sector suggest this process is already underway. There Are Two ‘Neutral Rates Of Interest’. Which One Will Central Banks Choose? The ‘neutral rate of interest rate’, also known as the long-run equilibrium interest rate, the natural rate and, to insiders, r-star or r*, is the short-term interest rate that is consistent with the economy at full employment and stable inflation: the rate at which monetary policy is neither contractionary nor expansionary. But here’s the subtle point that many people miss. The neutral rate is defined in terms of stable inflation without stating what that stable rate of inflation is. Therein lies the Fed’s problem. The near-term neutral rate that is consistent with inflation at 2 percent is much higher than the near-term neutral rate that is consistent with full employment. The near-term neutral rate that is consistent with inflation at 2 percent is much higher than the near-term neutral rate that is consistent with full employment. Now let’s add a third goal of ‘financial stability’, and the message from the ongoing crash in stock, bond, and credit markets is crystal clear. The near-term neutral rate that is consistent with inflation at 2 percent is also much higher than the near-term neutral rate that is consistent with financial stability (Chart I-5 and Chart I-6). Chart I-5Markets Have Crashed Because Valuations Have Crashed. Profits Have Held Up… So Far

5. Markets Have Crashed Because Valuations Have Crashed. Profits Have Held Up... So Far

5. Markets Have Crashed Because Valuations Have Crashed. Profits Have Held Up... So Far

Chart I-6When The Mortgage Rate Exceeds The Rental Yield, It Spells Trouble For House Prices

When The Mortgage Rate Exceeds The Rental Yield, It Spells Trouble For House Prices

When The Mortgage Rate Exceeds The Rental Yield, It Spells Trouble For House Prices

This leaves the Fed, and other central banks, with a major dilemma. Which neutral rate goal to pursue – full employment and financial stability, or inflation at 2 percent? In the near term, the answer seems to be inflation at 2 percent. This is because the lifeblood of central banks is their credibility. With their credibility as inflation fighters in tatters, this may be the last chance to repair it before it is shredded forever. Taking this long-term existential view, central banks have decided that a recession is a price worth paying to slay inflation and repair their credibility. In this important sense, the current setup rhymes with 1981-82 when the Paul Volcker Fed made the same decision. Therefore, the correct investment strategy for stocks, bonds, sectors and FX is to follow the template of 1981-82, which we detailed in More On 2022-2023 = 1981-82, And The Danger Ahead. In a nutshell, an imminent recession will require a defensive strategy for most of 2022, before a strong recovery in markets unfolds in 2023. Eventually, the central banks’ major dilemma between inflation and growth will resolve itself. The triple whammy of a recession in asset prices, profits, and jobs will unleash a strong disinflationary – or even outright deflationary – impulse, causing inflation to collapse to well below 2 percent in 2023-24. And suddenly, there will be no conflict between the neutral rate that is consistent with full employment and financial stability, and that which is consistent with inflation at 2 percent. Both neutral rates will be ultra-low. Hence, while interest rates are likely to overshoot in the near term, the pain that they will cause will require a commensurate undershoot in 2023-24. On this basis, go long the December 2023 Eurodollar (or SOFR) futures contract (Chart I-7). Chart I-7Go Long The Dec 2023 Eurodollar (Or SOFR) Future

Go Long The Dec 2023 Eurodollar (Or SOFR) Future

Go Long The Dec 2023 Eurodollar (Or SOFR) Future

Cryptos Will Bottom When The Nasdaq Bottoms The turmoil across financial markets has naturally engulfed cryptocurrencies, and this has generated the usual Schadenfreude among the crypto-doubters. But in the short-term, cryptocurrencies just behave like leveraged tech stocks, meaning that as the Nasdaq has fallen sharply, cryptos have fallen even more sharply (Chart I-8). Chart I-8In the Short Term, Cryptos = A Leveraged Nasdaq

In the Short Term, Cryptos = A Leveraged Nasdaq

In the Short Term, Cryptos = A Leveraged Nasdaq

Most cryptocurrencies are just the tokens that secure their underlying blockchains, so their long-term value hinges on whether their underlying blockchain technologies will succeed in displacing the current ‘trusted third party’ model of intermediation. In this sense, blockchain tokens are the ultimate long-duration growth stocks, whose present values are highly sensitive to the performance of the blockchain technology sector, which in turn is highly sensitive to the long-duration bond yield. Hence, while the bear markets in bonds, Nasdaq, and cryptos appear to be separate stories, they are just one massive correlated trade! Given that nothing fundamental has changed in the outlook for blockchains, long-term investors should treat this crypto crash, just like all the previous crypto crashes, as a buying opportunity. Cryptos will rally strongly once the Nasdaq reaches a near-term bottom, which in turn will depend on a peak in long bond yields. Fractal Trading Watchlist Amazingly, while most markets have crashed, the financial-heavy Czech stock market is up by 20 percent this year, in sharp contrast to its neighbouring Polish stock market which is down by 25 percent. In fact, over the last year, Czechia has outperformed Poland by 100 percent. From both a fundamental and technical perspective, this outperformance is now vulnerable to reversal (Chart I-9). Accordingly, a recommended trade is to underweight Czechia versus Poland, setting the profit target and stop-loss at 15 percent. Elsewhere, the outperformances of German telecoms, Japanese telecoms, and US utilities are all at, or close, to points of fractal fragilities which make them vulnerable to reversals. As such, these have entered out watchlist. The full watchlist of 27 investments that are at, or approaching turning points, is available on our website: cpt.bcaresearch.com Chart I-9Czechia's Spectacular Outperformance Is Vulnerable To Reversal

Czechia's Spectacular Outperformance Is Vulnerable To Reversal

Czechia's Spectacular Outperformance Is Vulnerable To Reversal

Fractal Trading Watchlist: New Additions German Telecom Outperformance Vulnerable To Reversal

German Telecom Outperformance Vulnerable To Reversal

German Telecom Outperformance Vulnerable To Reversal

Japanese Telecom Outperformance Vulnerable To Reversal

Japanese Telecom Outperformance Vulnerable To Reversal

Japanese Telecom Outperformance Vulnerable To Reversal

US Utilities Outperformance Vulnerable To Reversal

US Utilities Outperformance Vulnerable To Reversal

US Utilities Outperformance Vulnerable To Reversal

Chart 1BRL/NZD At A Resistance Point

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 2Homebuilders Versus Healthcare Services Has Turned

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 3CNY/USD At A Potential Turning Point

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 4US REITS Are Oversold Versus Utilities

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 5CAD/SEK Is Vulnerable To Reversal

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 6Financials Versus Industrials Has Reversed

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 7The Outperformance Of Resources Versus Biotech Has Ended

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 8The Outperformance Of Resources Versus Healthcare Has Ended

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 9FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable To Reversal

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 10Netherlands' Underperformance Vs. Switzerland Is Ending

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 11The Sell-Off In The 30-Year T-Bond At Fractal Fragility

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 12The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 13Food And Beverage Outperformance Is Exhausted

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 14German Telecom Outperformance Vulnerable To Reversal

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 15Japanese Telecom Outperformance Vulnerable To Reversal

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 16The Strong Downtrend In The 18-Month-Out US Interest Rate Future Is Fragile

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 17The Strong Downtrend In The 3 Year T-Bond Is Fragile

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 18A Potential Switching Point From Tobacco Into Cannabis

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 19Biotech Is A Major Buy

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 20Norway's Outperformance Has Ended

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 21Cotton Versus Platinum Is At Risk Of Reversal

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 22Switzerland's Outperformance Vs. Germany Has Ended

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 23USD/EUR Is Vulnerable To Reversal

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 24The Outperformance Of MSCI Hong Kong Versus China Has Ended

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 25A Potential New Entry Point Into Petcare

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 26GBP/USD At A Potential Turning Point

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Chart 27US Utilities Outperformance Vulnerable To Reversal

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 Based on the nonfarm payrolls. 2 Rent of shelter also includes lodging away from home, but the two dominant components are rent of primary residence and owners’ equivalent rent of residences. Fractal Trading System Fractal Trades

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

Higher Unemployment Is Coming, Says This Indicator

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

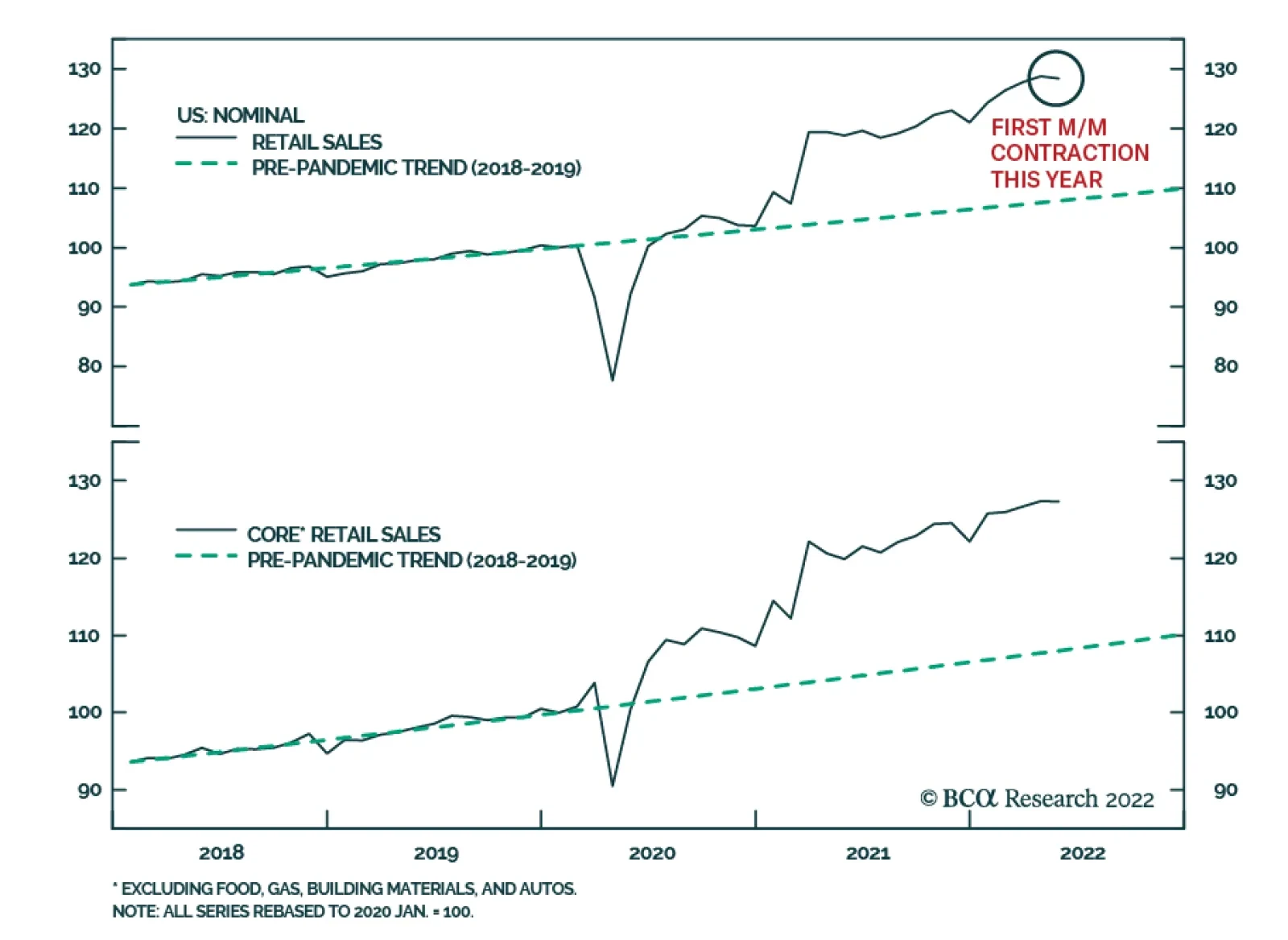

US retail sales contracted 0.3% m/m in May, surprising expectations of a modest 0.1% m/m rise and following a downwardly revised 0.7% m/m increase in April. Sharp declines in vehicles (3.5% m/m), electronics and appliances (1.3% m/m) and home furnishing (0.9%…

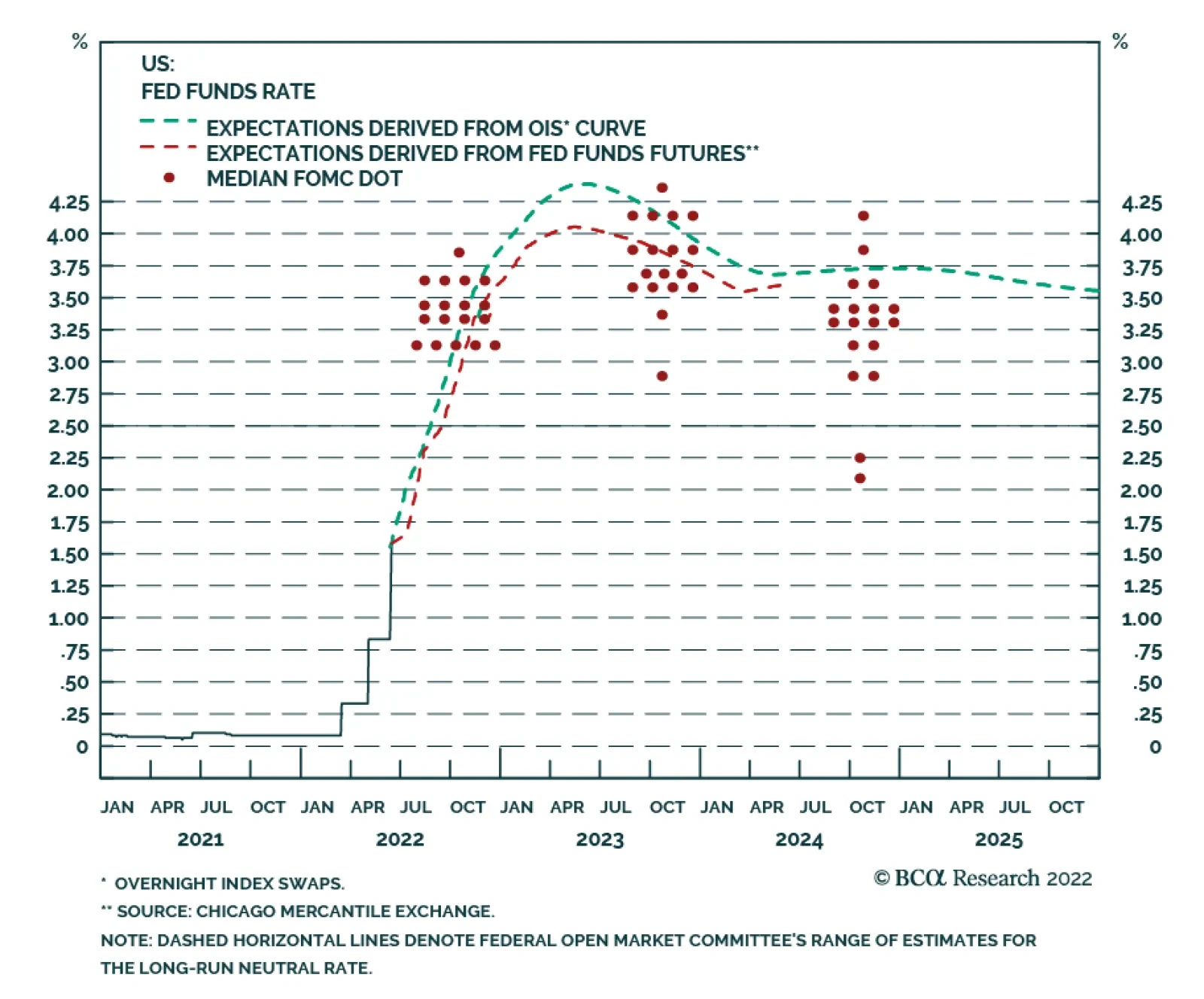

The Fed hiked interest rates by 75bps on Wednesday – above the 50bp rate hike plan it had telegraphed at its previous meeting. Chairman Jay Powell noted that unexpectedly hot inflation and rising long-dated consumer inflation expectations warranted the…

Following an emergency meeting on Wednesday, the ECB pledged to “apply flexibility in reinvesting redemptions coming due in the PEPP portfolio” and “accelerate the completion of the design of a new anti-fragmentation instrument” in order to address the…

Don’t Be A Hero

Don’t Be A Hero

In our recent research, we have been cautioning investors that the market will be “Fat and Flat” over the course of 2022. Our view was that inflation was going to turn down due to the base effect, rather than heroic actions of the Fed. We expected rates stabilization and investors moving on from inflation worries to growth worries. As a result, we hypothesized, that equities will be range-bound, with rallies and pullbacks alternating each other, as better inflation readings would be accompanied by disappointing growth. Friday’s nasty inflation surprise changed this view. There are now three key worries: Inflation is not abating, while growth is slowing. Are we at the gates of stagflation? Will monetary tightening be even more aggressive than expected? The probability of a 75bps rate hike at the coming Fed meeting increased to over 90% from 4% just a week ago (see chart). Are we shifting to a new monetary regime, and the easy money of the past 12 years is a thing of the past? In addition, there may be a greater risk flying under the radar of the equity investors. We learned in our conversations with the hedge fund clients, that there is a dearth of liquidity in the fixed income space. Recent violent moves in equities and bonds could result in a credit/counterparty “black swan” event as there are already liquidity problems in the MBS market. Meanwhile, junk bonds are trading at the March 10, 2020 levels. True, the SPX discounted plenty of negative news now that it is officially in the bear market territory. However, we believe that the S&P 500 is not yet close to the bottom. The market is again pricing in tighter monetary policy. In addition, we are predicting that the next leg of the bear market will come from earnings. An earnings recession is highly likely due to falling growth at home and abroad, and companies’ waning pricing power. Bottom Line: The S&P 500 has not bottomed out. We say: Don't buy the dip, sell the rip. Also, markets will remain volatile - "don't be a hero” and keep sector allocation close to the benchmark. We still favor defensives over cyclicals.

US PPI grew by 0.8% m/m (10.8% y/y) in May, from 0.4% m/m (10.9%y/y) in April. The core measure firmed 0.5% m/m (8.3% y/y) from 0.2% m/m (8.6% y/y). Unlike the hotter-than-expected May CPI report, the PPI release was broadly in line with – and in some…

The 7% drop in the S&P 500 following Friday’s CPI release has pushed US equities into bear market territory. The index is now down 22% from its all-time high on January 3, raising the question of the potential sources of upside surprises for equity…