Developed Countries

Executive Summary Bond investors can’t seem to decide whether the US economy is in the midst of an inflationary boom or hurtling toward recession. Our sense is that, while US economic growth is clearly slowing, we don’t see the unemployment rate rising enough for the Fed to abandon its tightening cycle any time soon. The 5-year US Treasury yield has tightened relative to the rest of the curve in recent weeks, and the 2-year maturity now looks like the most attractive spot for investors. TIPS breakeven inflation rates have also declined markedly in recent weeks, and TIPS no longer look expensive on our models. TIPS Are No Longer Expensive

TIPS Are No Longer Expensive

TIPS Are No Longer Expensive

Bottom Line: US bond investors should keep portfolio duration close to benchmark. They should also shift Treasury curve allocations from the 5-year maturity to the 2-year maturity and upgrade TIPS from underweight to neutral. Whipsaw Inflationary boom or recession? US bond investors can’t seem to decide and yields are swinging back and forth depending on the latest economic data. Just in the past month we’ve seen the 10-year US Treasury yield peak at 3.49%, fall to 2.82% and then finally move back above 3% following last week’s strong employment report. Not surprisingly, implied interest rate volatility is the highest it’s been since the Global Financial Crisis (Chart 1). Our sense is that, while US economic growth is clearly slowing, we don’t see the unemployment rate rising enough for the Fed to abandon its tightening cycle any time soon. This is especially true because the Fed will tolerate a significant rise in the unemployment rate as long as inflation stays above target.1 Turning to the evidence, decelerating US economic activity is apparent in the manufacturing and non-manufacturing PMIs, which are both falling rapidly from high levels (Chart 2). Though both indexes remain firmly above the 50 boom/bust line, trends in financial conditions suggest that they could dip below 50 within the next few months. Chart 1A Highly Volatile Rates Market

A Highly Volatile Rates Market

A Highly Volatile Rates Market

Chart 2US Growth Is Slowing

US Growth Is Slowing

US Growth Is Slowing

The employment components of both indexes are already in contractionary territory (Chart 2, bottom panel), but this is due to concerns about labor supply, not demand. For example, last week’s ISM non-manufacturing PMI release included three representative quotes from respondents about labor market conditions.2 All three quotes reference concerns about labor supply: Unable to fill positions with qualified applicants. Extremely hard to find truck drivers. Demand for talent is higher, but availability of candidates to fill open roles continues to keep employment levels from increasing. This doesn’t sound like an economy that is on the cusp of surging unemployment, and this is exactly what the Fed is counting on. The Fed’s hope is that slower demand will bring down the large number of job openings without leading to a significant increase in layoffs or a significant rise in the unemployment rate. In that regard, it is notable that job openings ticked down in May, both in absolute terms and relative to the number of unemployed. Meanwhile, the rates of hiring and layoffs held steady (Chart 3). Chart 3Some Hope For A Soft Landing

Some Hope For A Soft Landing

Some Hope For A Soft Landing

Investment Implications Our investment strategy hinges on two key economic views related to the labor market and inflation. First, while a surge doesn’t seem imminent, slowing economic activity means that the unemployment rate is more likely to edge higher between now and the end of the year than it is to fall. Second, as we’ve written in previous reports, US inflation has a relatively easy path back to its underlying trend of approximately 4%.3 After that, it will be more difficult for policymakers to bring inflation from 4% back down to 2%, and we could see the Fed push rates above 4% next year to accomplish this task. Taken together, these two views suggest that growth will be slowing and inflation falling between now and the end of the year. This combination could easily push bond yields lower, especially if recession worries flare up again. High frequency bond yield indicators such as the CRB Raw Industrials / Gold ratio and the relative performance of cyclical versus defensive equities also suggest that bond yields have room to fall (Chart 4). That said, the market is currently priced for the fed funds rate to peak at 3.74% in May 2023 and to fall back to 3.19% by the end of 2023. We see strong odds that inflation will be sticky enough (and the labor market resilient enough) for the Fed to push rates above those levels next year. This leaves us with an ‘at benchmark’ stance on portfolio duration for the time being, with an inclination to turn more bearish on bonds later this year if our base case forecast pans out. More specifically, we would likely reduce portfolio duration if the 10-year Treasury yield falls back to 2.5% or if inflation reverts to its 4% underlying trend. Conversely, we will turn more bullish on bonds if we see signs in the labor market data that point to a Fed pause (or Fed rate cuts) being necessary. For now, growth in nonfarm employment and aggregate weekly payrolls (wages x hours x employment) suggest we aren’t close to this outcome (Chart 5). Chart 4High-Frequency Bond Yield Indicators

High-Frequency Bond Yield Indicators

High-Frequency Bond Yield Indicators

Chart 5The US Labor Market Is Strong

The US Labor Market Is Strong

The US Labor Market Is Strong

Sliding Down The Yield Curve Since early April we’ve been recommending that investors position long the 5-year Treasury note and short a duration-matched barbell consisting of the 2-year and 10-year notes to take advantage of a US yield curve that was quite steep out to the 5-year maturity point and quite flat beyond that. That trade is now played out. The 5 over 2/10 butterfly spread has tightened back to zero and the 2-year note is now the most attractively priced security on the US Treasury curve. Chart 6 shows that the spread between the 2-year note and a duration-matched barbell consisting of cash and the 5-year note offers an extraordinary yield advantage of 92 bps. What’s more, Table 1 shows that, with the exception of the unloved 20-year bond, the 2-year note offers the most attractive 12-month carry on the curve, largely a result of the 18 bps of rolldown attributable to the still-steep slope between the 1-year and 2-year maturity points. Chart 6Shift Into 2s

Shift Into 2s

Shift Into 2s

Table 112-Month Carry Across The US Treasury Curve

A Low Conviction US Bond Market

A Low Conviction US Bond Market

This large shift in relative pricing compels us to close our prior position (long 5-year bullet versus 2/10 barbell) and open a new position: long the 2-year note and short a duration-matched cash/5 barbell. This new position (long 2yr over cash/5) offers attractive 12-month carry, but given the current volatile interest rate environment, it should mainly be expected to profit in the event of a steepening of the 2/5 Treasury slope. With that in mind, it’s notable that the 2/5 slope recently inverted. Inversions of the 2/5 slope are historically rare. They tend to occur near the end of Fed tightening cycles and, with the exception of the early-1980s, they tend to not last that long (Chart 7). Chart 72/5 Inversions Are Rare And Fleeting

2/5 Inversions Are Rare And Fleeting

2/5 Inversions Are Rare And Fleeting

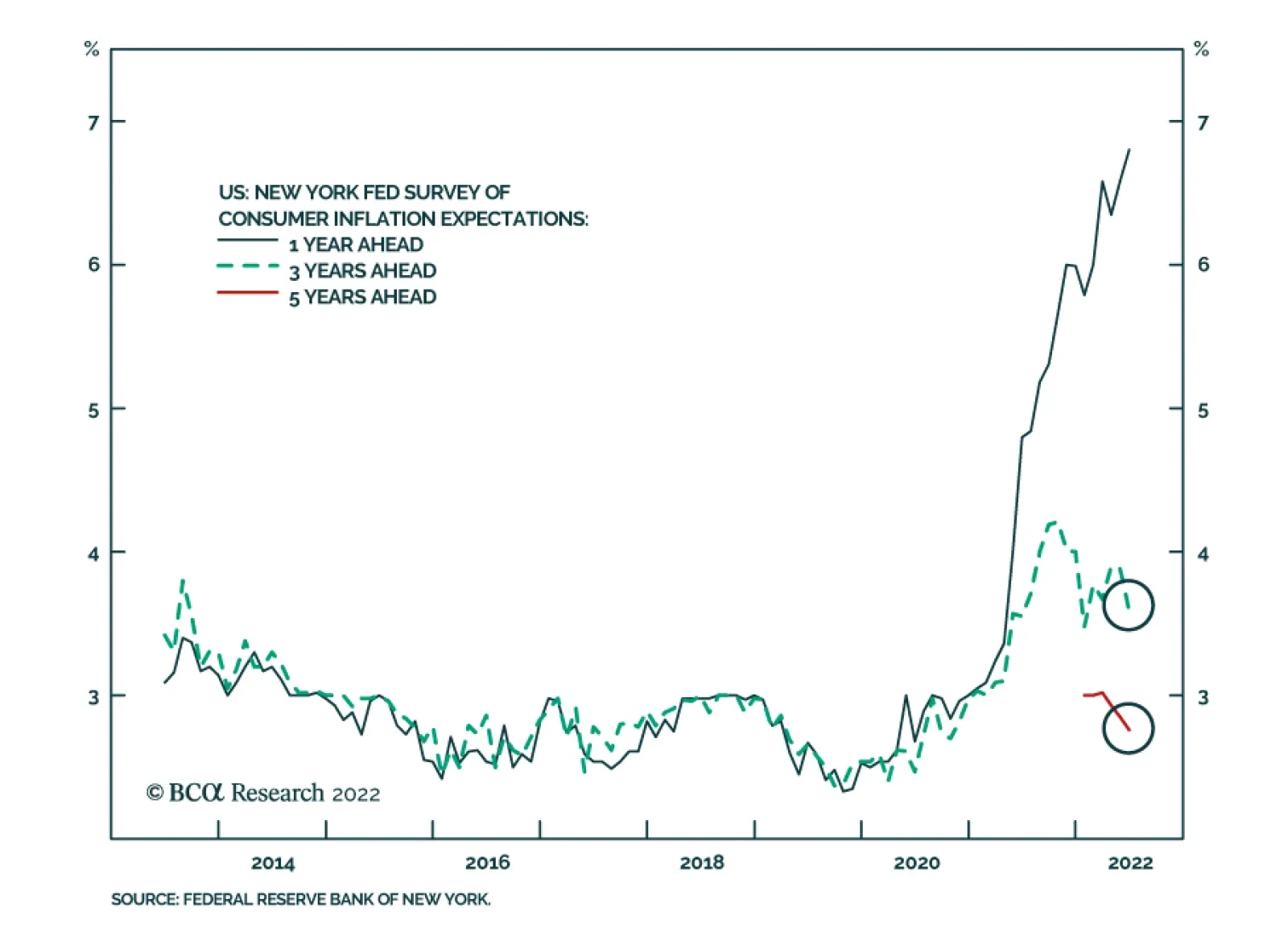

Going forward, we see three plausible scenarios for the 2/5 slope during the next 6-12 months. First, the Fed achieves something close to the soft landing it is aiming for. Inflation starts to fall and the unemployment rate edges higher. However, unemployment never reaches levels that necessitate a complete reversal of Fed tightening. The 2/5 Treasury slope bear-steepens in this scenario as the market discounts that the Fed will have to push rates above 4% to hit its inflation target. Second, a deep recession and complete reversal of Fed tightening occur much more quickly than we anticipate. The 2/5 Treasury slope would bull-steepen in this scenario as the front-end of the curve is pulled down by the Fed’s pivot. Third, inflation shows no signs of reversing course. Long-dated inflation expectations jump and the Fed determines that it has no choice but to follow the example of Paul Volcker and tighten, even if the economy falls into a deep recession. As was the case in the early-1980s, the 2/5 Treasury slope could become deeply inverted in this scenario. Our sense is that the first two scenarios are much more likely than the third. We have written in prior reports about how the current spate of inflation is much different than what was seen in the early 1980s.4 This makes us willing to bet against a prolonged deep inversion of the 2/5 slope. Bottom Line: US Treasury curve investors should exit their positions long the 5-year bullet versus a duration-matched 2/10 barbell. They should initiate a position long the 2-year bullet versus a duration-matched cash/5 barbell. Upgrade US TIPS To Neutral Finally, we note that TIPS breakeven inflation rates have declined markedly during the past month. The 10-year TIPS breakeven inflation rate is currently 2.38%, near the lower-end of the Fed’s 2.3%-2.5% target range, and the 5-year/5-year forward TIPS breakeven inflation rate is a mere 2.12%, well below target (Chart 8). We also note that the 5-year/5-year forward TIPS breakeven inflation rate is back below survey estimates of what inflation will be 5-10 years in the future (Chart 8, bottom panel). Chart 8TIPS Breakevens

TIPS Breakevens

TIPS Breakevens

We have been recommending an underweight position in TIPS versus nominal US Treasuries since early April, but the recent valuation shift means it’s time to add some exposure. Critically, our TIPS Breakeven Valuation Indicator has also increased to +0.6, moving into “TIPS cheap” territory (Chart 9). Historically, the 10-year TIPS breakeven inflation rate has averaged an increase of 28 bps in the 12 months following a reading between +0.5 and +1.0 from our Indicator (Table 2). Chart 9TIPS Are No Longer Expensive

TIPS Are No Longer Expensive

TIPS Are No Longer Expensive

Table 2TIPS Breakeven Valuation Indicator Track Record

A Low Conviction US Bond Market

A Low Conviction US Bond Market

The drop in TIPS breakeven inflation rates has been most prominent at the front-end of the curve. The 2-year TIPS breakeven inflation rate is down to 3.22% from a peak of 4.93%. The high correlation between short-maturity TIPS breakevens and realized CPI inflation means that short-dated breakevens can fall further as inflation continues to trend down, but already we see that 3.22% looks like a much more reasonable estimate of average inflation for the next two years than did the 4.93% peak. While we advise investors to upgrade TIPS from underweight to neutral relative to nominal US Treasuries, we continue to recommend an outright short position in 2-year TIPS. The 2-year TIPS yield has risen sharply since its 2021 low (Chart 10), but recent comments from Fed officials imply that the Fed would like to see positive real yields across the entire curve before it declares monetary policy sufficiently restrictive.5 This means that there is still some room for the 2-year TIPS yield to increase, from its current level of -0.10% back into positive territory. Such a move should also lead to more flattening of the 2/10 TIPS curve, and we continue to recommend holding that position as well (Chart 10, bottom panel). Chart 10Stay Short 2-Year TIPS

Stay Short 2-Year TIPS

Stay Short 2-Year TIPS

Bottom Line: Investors should upgrade TIPS from underweight to neutral relative to nominal US Treasuries but maintain outright short positions in 2-year TIPS. 2/10 TIPS curve flatteners and 2/10 inflation curve steepeners also continue to make sense. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 For more details on how to think about the tradeoff between the Fed’s inflation and employment goals please see US Bond Strategy Weekly Report, “When The Dual Mandates Clash”, dated June 28, 2022. 2 https://www.ismworld.org/supply-management-news-and-reports/reports/ism-report-on-business/services/june/ 3 Please see US Bond Strategy / Global Fixed Income Strategy Weekly Report, “No End In Sight For Fed Tightening”, dated June 21, 2022. 4 Please see US Bond Strategy Weekly Report, “No Relief From High Inflation”, dated June 14, 2022. 5 Please see US Bond Strategy Weekly Report, “When The Dual Mandates Clash”, dated June 28, 2022. Recommended Portfolio Specification Other Recommendations Treasury Index Returns Spread Product Returns

Stronger-than-expected job gains in June increase the odds that the Fed will lift interest rates by another 75bps when it meets again in two weeks. Data released this week will either cement the case for another mega hike, or instead provide support for a…

The Atlanta Fed’s GDPNow model is sending an extremely pessimistic signal about the US economy. Since mid-May, its estimates of Q2 GDP growth have been consistently deteriorating. Although June’s robust non-farm payroll release led to an upward revision, the…

According to BCA Research’s European Investment Strategy service, while EUR/USD possesses ample upside over the coming 12 months, there is roughly a 1/3 chance that it will plunge to 0.9 by the winter. The euro benefits from important tailwinds that…

Executive Summary Don’t Try Catching Falling Euros

Don"t Try Catching Falling Euros

Don"t Try Catching Falling Euros

The euro is inexorably moving toward parity. However, many positives could still save EUR/USD, a cheap currency that will benefit if the fears of a global recession recede and if European inflation peaks by the fall. Nonetheless, many fundamental risks still weigh on the euro, including the dollar’s momentum and the continuing ructions in the European energy market. Moreover, technical vulnerabilities are likely to amplify the potential weakness in the euro. There is greater than a 30% chance that EUR/USD will fall to 0.9 or below. As a result, it is preferable to stay on the sidelines and opt for a neutral stance on the EUR/USD. Selling EUR/JPY offers a more attractive reward-to-risk ratio than EUR/USD. The GBP remains under threat. Bottom Line: Don’t be a hero. At this juncture, the EUR/USD outlook remains particularly uncertain. While EUR/USD possesses ample upside over the coming 12 months, there is roughly a 1/3 chance that it will plunge to 0.9 by the winter. Investors should sell EUR/JPY instead. The euro’s race toward parity continues. From May 12 to July 1, EUR/USD attempted to form a triple bottom at 1.0375 that could have marked the end of this year’s decline. Alas, the euro did not hold that floor and now traders are inexorably pushing the common currency lower. The outlook for the euro is complex. At current levels, it is inexpensive and discounts many negative developments affecting both the global and European economies. However, the EUR/USD’s weakness is also a story of dollar strength, and the deteriorating global economic momentum remains the Greenback’s best friend, to the euro’s detriment. For now, we stick to our mantra of the past few months: don’t be a hero. The euro may soon bottom, but enough risks lie ahead that a move below 0.9 against the dollar should not be discarded. The risk-reward from bottom fishing is therefore poor. Instead, investors should sell EUR/JPY, for which downside remains ample. What We Like About The Euro… Despite the pervasive negativity engulfing the euro, there are plenty of positives that will soon help EUR/USD form a bottom. First, the euro is cheap on most metrics. The Purchasing Power Parity (PPP) model developed by BCA’s Foreign Exchange Strategists adjust for the different consumption baskets in the Eurozone and the US. It currently shows that EUR/USD trades 25% below fair value, its deepest discount since 2001. This degree of undervaluation is associated with a high probability of strong long-term returns for the euro (Chart 1). Based on interest rate parity and risk aversion, the euro also trades well below its fair value. Steep discounts are often followed by an imminent rebound in the currency (Chart 2). However, the euro hit a similar discount in January, but failed to rally because of the problems in the energy markets prompted by Russia’s invasion of Ukraine. Chart 1Strong Long-Term Returns based on PPP

Strong Long-Term Returns based on PPP

Strong Long-Term Returns based on PPP

Chart 2Oversold on Many Metrics

Oversold on Many Metrics

Oversold on Many Metrics

Second, the euro is oversold. Both BCA’s Intermediate-Term Technical Indicator and the Citi FX Euro PAIN Index are very depressed, which indicates pervasive negative sentiment toward the euro (Chart 2, bottom two panels). This kind of extremes in momentum are often followed by a euro rally. Chart 3Global Recession Fears Hurt EUR/USD

Global Recession Fears Hurt EUR/USD

Global Recession Fears Hurt EUR/USD

Third, global economic pessimism is widespread. EUR/USD is a pro-cyclical pair, which mostly reflects the counter-cyclicality of the dollar and the great liquidity of the euro. It is therefore not surprising that spikes in global recession concerns are associated with a weakening EUR/USD (Chart 3). The recent wave of depreciation happened contemporaneously with a spike in Google searches for the word “recession.” If these fears, which reached extreme levels, subside further in the months ahead, the euro may benefit greatly. Fourth, pessimism toward China may ease, which would lift the euro in the process. Last week, it was announced that Beijing is considering allowing local governments to sell RMB1.5 trillion of special government bonds in the second half of the year to fund infrastructure spending. The news caused a rebound in the AUD, Brazilian assets, and copper. Europe too would benefit from greater activity in China. Chart 4Chinese Salvation?

Chinese Salvation?

Chinese Salvation?

Chinese monetary conditions are also easing, which historically supports industrial activity in Europe relative to the US (Chart 4, top panel). The change in approach in the implementation of the zero-COVID policy is helping Chinese PMIs rebound, which will eventually translate into higher European shipments to China. Moreover, the rate of change of the performance of real estate stocks relative to the broad market has turned the corner, which may facilitate a stabilization of Chinese real estate transactions (Chart 4, second panel). Ultimately, the expanding excess reserves in the Chinese banking system point toward a stabilization of the performance of EUR/USD later this year (Chart 4, bottom panel). Fifth, our expectation that European inflation will peak by the autumn will prove the greatest help to the euro. The EUR/USD’s weakness over the past twelve months has coincided with a surge in European inflation surprises (Chart 5, top panel). This relationship reflects the negative impact on European real rates of both stronger realized and expected inflation (Chart 5, second panel). Investors understand that Europe’s inflation crisis is driven by a relative price shock in the energy market that greatly hurts economic activity in the Eurozone. Hence, even if they expect the ECB to increase interest rates, they believe policy rates will lag inflation because of Europe’s poor growth outlook. This is particularly true when compared to the US Fed. As a result, European real rates continue to lag far behind US ones and the European yield curve is steeper than that of the US, because traders foresee easier policy on the Eastern shores of the Atlantic (Chart 5, panel three and four). Chart 5Inflation Hurts the Euro

Inflation Hurts the Euro

Inflation Hurts the Euro

Chart 6Declining Inflation Expectations? Declining Inflation Expectations?

Declining Inflation Expectations? Declining Inflation Expectations?

Declining Inflation Expectations? Declining Inflation Expectations?

This situation is fluid and inflation expectations have begun to decrease. The recent easing in energy prices has contributed to a decline in long-term inflation expectations (Chart 6). We argued last week that the energy inflation is arithmetically set to decrease over the coming twelve months, which suggests further downside in inflation expectations is likely. Moreover, four of the five largest weights in the Eurozone HICP are running hot, but all are linked to commodity inflation, which confirms our bias that European inflation will soon peak (Chart 7). A top in both headline and core inflation will drag short- and long-term inflation expectations lower, which will help European real rates (Chart 8). Meanwhile, lower imported energy inflation will limit the damage to European economic activity, allowing the ECB to increase rates anyway. Chart 7Key HICP Components

Key HICP Components

Key HICP Components

Chart 8A durable Decline In Expected Inflation Depends On Realized Inflation

A durable Decline In Expected Inflation Depends On Realized Inflation

A durable Decline In Expected Inflation Depends On Realized Inflation

Chart 9Balance Of Payment Support

Balance Of Payment Support

Balance Of Payment Support

Bottom Line: The euro benefits from important tailwinds that suggest EUR/USD will be higher 12 to 18 months from now. It is cheap and oversold and the pervasive gloom among investors about the state of the global economy indicates that many negatives are already embedded in its pricing. Moreover, the Chinese economy could stabilize in the second half of 2022 and into 2023, which will hurt the dollar and boost the euro. Crucially, a peak in European inflation will allow European real rates to recover and curtail the handicap keeping EUR/USD under pressure, especially as the basic balance of payment remains in the euro’s favor (Chart 9). … And What We Don’t EUR/USD may benefit from some important tailwinds, but it is still burdened by massive handicaps. The first problem that will place downward pressure on the euro is that its weakness is not unique and that it reflects broad-based dollar strength (Chart 10). This is a problem for the euro because the dollar (and the yen) is the foremost momentum currency in the G10. Its strength begets further strength, and the momentum signal from moving average crossovers remains dollar-bullish. This headwind for the euro could even intensify in the coming months. JP Morgan EM FX Index is breaking down to new lows, which points to further tightening in EM financial conditions. Historically, tighter EM FCIs translate in both weaker Eurozone stock prices and a weaker EUR/USD, which reflects the closer link between the Euro Area and EM economies than between the US and EM (Chart 11). Chart 10The Dollar's Strength Is Broad-Based

The Dollar's Strength Is Broad-Based

The Dollar's Strength Is Broad-Based

Chart 11More Trouble In Store

More Trouble In Store

More Trouble In Store

This phenomenon is exacerbated by the underlying weakness in global economic activity. Arthur Budaghyan, BCA’s EM Chief Strategist, often reminds us that Asian exports remain soft. Additionally, the deterioration in US economic activity is likely to continue, as suggested by the weakness in the ISM new orders-to-inventories ratio and by the poor readings from the Regional Fed Surveys. Slowing US growth will generate a further decline in the business-sales-to-inventory ratio, which often coincides in a strong dollar and a weak euro. Chart 12Past Chinese Weaknesses Linger

Past Chinese Weaknesses Linger

Past Chinese Weaknesses Linger

The second problem for EUR/USD is that China’s economic outlook may be improving in the future, but, for now, the impact of the recent Chinese slowdown continues to hamper Europe. More specifically, the recent decline in Chinese import volumes is consistent with a euro-bearish backdrop for the remainder of this year (Chart 12, top panel). In fact, even if the CNY remains stable against the USD, this does not guarantee a positive outcome for the euro as the past weakness in Chinese import volumes is also consistent with a depreciating EUR/CNY (Chart 12, bottom panel) The third euro-negative force is the natural gas market. As we showed last week, Dutch natural gas prices must settle between EUR500-600/MWh this upcoming winter to have the same inflationary impact as they did over the past 18 months. This is unlikely to happen, even according to the direst forecasts of BCA’s Commodity and Energy strategists. However, there is a greater than 30% chance that Europe must ration electricity this winter, which would cause a violent output contraction. As a result, any fluctuation in natural gas flows in Europe will cause the market-based odds of a European recession to swing widely. Consequently, the negative correlation between EUR/USD and TTF prices observed over the past twelve months is likely to remain intact (Chart 13). Related Report European Investment StrategyQuestions From The Road The fourth issue hurting the euro is the US’s comparative isolation from the energy market’s travails. The US is a haven of relative economic stability today. Yes, its growth will slow further, but it is nonetheless set to outperform the Eurozone. The US is not under threat of rationing energy this winter. Moreover, the US terms of trades benefit from rising energy prices, unlike Europe (Chart 14). Furthermore, the US output gap is closing faster than that of in the Eurozone (Chart 14, bottom panel). As a result, the odds of dovish surprises by the ECB are much greater than those by the Fed. Chart 13Neutral Gas Is Still A Drag

Neutral Gas Is Still A Drag

Neutral Gas Is Still A Drag

Chart 14The US As A Haven Of Stability

The US As A Haven Of Stability

The US As A Haven Of Stability

The US’s relative resilience might also impact equity flows over the next few months in a euro-bearish fashion. US EPS have been stable relative to Euro Area ones, even in local currency terms. Interestingly, because relative EPS reflect broader economic forces, EUR/USD follows them (Chart 15). Thus, if the European economic outlook deteriorates further relative to that of the US, chances are high that Eurozone EPS estimates will be revised down relative to the US, which will coincide with a lower EUR/USD. In fact, the recent underperformance of Eurozone small-cap stocks (which are domestically focused) relative to European large-cap equities (which derive a greater proportion of their sales abroad) and US small-cap shares also confirms the worsening relative economic outlook between Europe and the US, and thus portend significant near-term risks to EUR/USD (Chart 16). Chart 15Follow Earnings Estimates

Follow Earnings Estimates

Follow Earnings Estimates

Chart 16Small Caps Indicate More EUR Selling

Small Caps Indicate More EUR Selling

Small Caps Indicate More EUR Selling

Chart 17An ECB Bungle Would Burden The Euro

An ECB Bungle Would Burden The Euro

An ECB Bungle Would Burden The Euro

The last major fundamental risk weighing on EUR/USD is the significant probability that the ECB will disappoint markets with respect to its anti-fragmentation tool to be announced in July. Investor expectations are lofty. However, internal divisions within the ECB Governing Council remain, and, most importantly, the ECB is hamstrung by previous ECJ and German Constitutional Court rulings on bond purchases. Thus, our base case remains that the development of an appropriate bond purchase program will be an iterative process resulting from a back-and-forth between market tensions and ECB responses. As a result, there are risks of further widening in Italian spreads as well as European corporate bond spreads. These developments would further hurt the euro (Chart 17). Chart 18Much Selling To Be Unleashed Sentiment Could Get More Negative

Much Selling To Be Unleashed Sentiment Could Get More Negative

Much Selling To Be Unleashed Sentiment Could Get More Negative

These fundamental problems with EUR/USD do not guarantee that the euro will punch below parity. After all, there are also plenty of positives with this currency. However, the risk of a violent selloff is elevated, at around 30%, because of underlying technical vulnerabilities. Global market liquidity has deteriorated in recent years, and this phenomenon is also impacting FX markets, resulting in sudden jumps being more frequent. Most crucially, the odds are high that automatic selling will be triggered if the euro tests parity, which would result in a cascading decline for a euro entering territory that has not been charted for the past 20 years. Specifically, speculators are marginally short the euro (Chart 18, top panel) and 1-month and 3-month risk reversals in the option markets are not yet at a capitulation point (Chart 18, bottom panel). Thus, if panic sets in, the euro could easily fall below 0.9, where the strongest supports lie. In essence, we worry that a sudden crash in the euro is becoming a growing threat. Bottom Line: The combination of the dollar’s momentum, the lagging impact of China’s economic woes, the risks to Europe’s energy supplies, the relative stability of the US economy, and the heightened chance that the ECB underdelivers with respect to its anti-fragmentation tool later next week all point to significant risks to the euro in the coming months. Moreover, the technical vulnerabilities present in the FX market suggest that, if further downside takes place, it will not only be large but also rapid. Investment Conclusions The dilemma between views and strategy is greatest with the euro today. There are many positives highlighted in this report that suggest that the euro has upside on a 12-month basis. However, the risks are abundant, and the potential downside in the coming six months not only carries a large probability, it is also likely to be pronounced if it takes place. As a result of this configuration, we fall back to the strategy we had adopted for European equities earlier this year: don’t be a hero. Even if the euro bottoms tomorrow, the risks are such that capital preservation remains paramount. Consequently, we recommend that investors stay on the sideline and maintain a neutral stance on EUR/USD. It is just as risky to try to bottom fish this pair as it is to chase it lower from current levels. Chart 19Sell EUR/JPY

Sell EUR/JPY

Sell EUR/JPY

Instead, we follow BCA’s Foreign Exchange Strategists recommendation to go short EUR/JPY as a bet with a lower risk-reward ratio. Global recession worries and weakening commodity inflation are likely to allow for greater downside in global yields, which often results in a lower EUR/JPY (Chart 19). Additionally, investors do not expect much out of the BoJ this year, but if recession risks intensify in Europe because of energy rationing this winter, there is room to curtail the interest rate pricing for the ECB embedded in the €STR curve. Furthermore, the JPY is the cheapest currency in the G10. Finally, investors wanting to build greater exposure to European currencies should do so via the Swiss franc. We argued three weeks ago that the CHF enjoys significant structural tailwinds because of the Swiss economy’s strong productivity. Additionally, the SNB is no longer intervening to limit the CHF upside, as demonstrated by the decline in its current deposits. Instead, a stronger Swiss franc is the most potent weapon in the SNB’s arsenal to combat inflation. Moreover, the CHF offers a hedge against both recession risks in the Eurozone and further widening in European spreads. Bottom Line: Don’t be a hero. EUR/USD’s outlook is uniquely uncertain now. While many factors point to positive returns on a 12-to-18 month basis, if the euro hits parity in response to the many clouds still hanging over Europe, technical factors could plunge this currency to EUR/USD 0.9 into a steep decline. Instead, the clearer call is to sell EUR/JPY. Investors who want to assume a European FX exposure today should do so through the Swiss franc, not the euro. A Few Words On The UK Last week, Prime Minister Boris Johnson resigned. The initial response of the pound was to rebound. This reaction should fade. BCA Geopolitical strategists argue that, even though the person sitting at 10 Downing Street is about to change, the fundamental problems with the UK remain the same. The Labour Party is ascending, but it will still have to deal with the Brexit aftermath, rising populism, and popular discontent across the country. The economy is still fragile and engulfed in an inflationary spiral. Meanwhile, the risks created by a looming Scottish independence referendum are much more significant than was the case in 2014. As a result, the pound is likely to remain under stress over the coming quarters. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Tactical Recommendations Cyclical Recommendations Structural Recommendations

Dear client, In lieu of July 18 publication, I will be hosting our quarterly webcast that I invite you to join. Our regular weekly publication will resume Monday, July 25. Kind Regards, Irene Tunkel Chief Strategist, US Equity Strategy Deploy Fresh Capital Into Growth At The Expense Of Value In early June, we closed our Growth/Value underweight by moving the ratio to benchmark allocation and crystallizing just under 9% in gains. At the time, we also wrote that we would upgrade Growth and downgrade Value once uncertainty about inflation and the Fed’s action recedes. Today, we believe that the time is ripe for making a move: We are upgrading Growth to overweight, and downgrade Value to underweight. The following are the reasons for a change in positioning: Chart 1Deploy Fresh Capital Into Growth At The Expense Of Value

Deploy Fresh Capital Into Growth At The Expense Of Value

Deploy Fresh Capital Into Growth At The Expense Of Value

Inflationary pressures will ease: There are early signs that inflation is about to turn - prices of energy and commodities are down 20% and 13% off their peaks respectively. A turn in inflation heralds a change in market leadership from Value to Quality and Growth (Chart 1). Chart 2

Deploy Fresh Capital Into Growth At The Expense Of Value

Deploy Fresh Capital Into Growth At The Expense Of Value

Economic growth is slowing: The market focus has shifted away from inflation and has turned towards worries about growth as is evident in the falling 10-year Treasury yield, which decreased from its peak at 3.5% to 3.0% over the past couple of weeks. The environment of slowing growth and falling rates is a tailwind for growth stocks. In a world where growth is becoming scarcer, companies that can deliver growth will shine. These are “growth” companies, i.e., large, stable companies with strong balance sheets that are able to generate positive cash flow and churn out strong earnings even under economic duress. Quality growth outperforms during slowdowns (Chart 2). Earnings Growth Expectations: Analysts expect earnings of Value to grow by over 10% over the next twelve months and Growth by 8.0%. While earnings growth expectations for value stocks appear more attractive, we believe that they will be downgraded. Value stocks are dominated by cyclicals (Chart 3), and as we wrote in the Tuesday's publication, this is the area of the market in which analysts have the least certainty in their estimates and downgrades are imminent. Growth is oversold relative to Value: The Growth/Value ratio is extremely oversold sitting at a level exceeded only during the dot-com crash and on par with the 1970-1980 inflationary era (Chart 4). Chart 3

Deploy Fresh Capital Into Growth At The Expense Of Value

Deploy Fresh Capital Into Growth At The Expense Of Value

Chart 4

Deploy Fresh Capital Into Growth At The Expense Of Value

Deploy Fresh Capital Into Growth At The Expense Of Value

Bottom Line: Slowing growth, impending turn in inflation, and attractive technicals are key reasons for our upgrade of Growth to overweight at the expense of Value.

Executive Summary The Dollar And Volatility

The Dollar And Volatility

The Dollar And Volatility

The dollar continues to be bid, as volatility rises. The MOVE volatility index is making fresh cycle highs and has pushed the DXY index above our stop level of 107 (Feature Chart). The move in the dollar suggests that we are experiencing a classic breakout pattern. Historically, this means that flows into the USD will continue, until it becomes clear that drivers of USD strength have abated. These include inflation peaking and global growth bottoming. We are moving our recommended stance on USD to neutral. It is becoming clear that the market sees the risk of a nasty recession in Europe to be high. The euro could break below parity, as speculators short the currency en masse. The yen is becoming a winner in the current context. We are reopening our short EUR/JPY trade this week, in addition to our short CHF/JPY position initiated last week. Our long AUD/USD position was stopped out at 68 cents this week. Given our shift to a neutral view on the dollar, we recommend investors stand aside for now. Bottom Line: We were stopped out of our short DXY position at 107, for a loss of 2.34%. We are moving to a neutral stance on the greenback. While valuation and sentiment are at contrarian extremes, the current environment dictates that further gains in the greenback are likely in the near term. Feature The DXY index has staged a classic breakout and the next technical level is closer to the 2002 highs near 120. Year-to-date, the DXY has been one of the best performing currencies (Chart 1). In last week’s report, we presented a framework for managing currencies, suggesting that while the path of least resistance for the dollar was up, significant headwinds were also building. One of the closest correlations we have seen in recent trading days is with volatility. As Chart 2 shows, the dollar and the MOVE index have been the same line. As markets increasingly price in the probability of a recession, especially in Europe, the dollar will be bought. This puts central banks in a quandary: focusing on growth or inflation? As such bond volatility is shooting up and the dollar is commanding a hefty safety premium. In the next few sections, we go over the important data releases from our universe of G10 countries, and implications for currency strategy. Chart 1The Dollar Remains King

Month In Review: The Euro At Parity, What Next?

Month In Review: The Euro At Parity, What Next?

Chart 2The Dollar And Volatility

The Dollar And Volatility

The Dollar And Volatility

US Dollar: A Classic Breakout Chart 3A Clean Breakout In The DXY

A Clean Breakout In The DXY

A Clean Breakout In The DXY

The dollar DXY index is up 11.3% year-to-date. Over the last month, the DXY index is up 4.7%. Technical forces are still in favor of the greenback as a momentum currency, given the classic breakout pattern. Looking at incoming data from the US, the case for dollar strength remains in place in the near term. The May CPI print came in well above expectations, at 8.6% for headline, versus 8.3% expected. A few days later, the PPI print was also strong at 10.8% year on year. This is happening at a time when consumer confidence is rolling over. The University of Michigan current conditions index fell from 63.3 to 53.8 in May. The expectations component dropped from 55.2 to 47.5. The conference board measure fell from 103.2 to 98.7 in June. After this print, the Fed met on June 15 and increased interest rates by 75bps, a surprise to the market. The current account deficit widened to $291.4bn US, a record low since the end of the Bretton Woods system . Retail sales disappointed in May. Excluding automobile and gasoline, sales were up 0.1% month on month, versus a consensus expectation of a 0.4% rise. It was also flat for the control group, suggesting basket changes were not responsible for the deterioration. The numbers are on a nominal basis, which suggests that retail sales volumes are contracting meaningfully. The rise in interest rates is filtering into the housing market. Mortgage applications fell 5.4% during the week of July 1. Housing starts declined from 1,810K to 1,724K in May, a 14.4% drop. Building permits also fell 7% month on month, in line with the 3.4% drop in existing home sales. The ISM manufacturing index fell from 56.1 to 53 in June. US economic data is softening, which raises the odds that the US joins Europe and China in a classic slowdown. In such a configuration, the market is pricing in that the dollar will ultimately be the haven asset, as has been the case in recent history. We went short the DXY index at 104.8, with a stop-loss at 107, that was triggered overnight. We are moving to a neutral stance today and will revisit this position once global economic uncertainty subsides. The Euro: A European Hard Landing Chart 4The Euro Is Pricing In A Deep Recession

The Euro Is Pricing In A Deep Recession

The Euro Is Pricing In A Deep Recession

The euro is down 10.5% year-to-date. Over the last month, the euro is down 4.7%, and recent trading suggests we will probably breach parity versus the dollar in the coming weeks. Recent data from the eurozone continues to suggest it is trapped in stagflation. The preliminary CPI print for June came in at 8.6%, well above the previous 8.1% print. PPI in the euro area is at 36.3%. Meanwhile, consumer confidence (the European Commission’s measure) is approaching a record low. The Sentix investor confidence index peaked in July last year and has been falling ever since. With a mandate of bringing down inflation, the ECB may have no choice but to knock the eurozone economy to its knees. The proximate expression of this view has been via shorting the euro. Most of the incoming data for the euro area have been deteriorating. For example, on a seasonally adjusted basis, the trade deficit widened to -€31.7bn. This is a record since the creation of the euro. This has completely wiped the eurozone current account, meaning the euro is now becoming a borrower nation. The critical question for Europe lies in the adjustment mechanism towards a possible shut-off in natural gas supplies for the winter. European natural gas prices are soaring anew, though well below the peak this year. A cut-off of Russian supplies is becoming a very real possibility. The question then becomes how deep of a European recession the euro is pricing in. Back in 2020, the euro bottomed at 1.06. At the time, quarterly real GDP in the euro area fell 11.9% in the second quarter. That was worse than both during the global financial crisis, and anytime since the creation of the euro. This means that fundamentally, the euro has already priced in a nasty recession in Europe. If it occurs, the euro could undershoot but if it does not, the potential for a coiled spring rebound is immense. A hedged bet on the euro is to sell the EUR/JPY cross. In a risk-off environment, EUR/JPY will collapse. In a Goldilocks scenario, the yen has sold off much more that the euro, that the cross could move sideways. The Japanese Yen: Now A Safe Haven Chart 5The Yen Is Becoming An Attractive Safe Haven

The Yen Is Becoming An Attractive Safe Haven

The Yen Is Becoming An Attractive Safe Haven

The Japanese yen is down 15.4% year-to-date, the worst performing G10 currency. Over the last month, the yen is down 2.4%. Incoming data in Japan has been mixed with the domestic economy still showing some signs of weakness, while the external sector is faring relatively better. The Bank of Japan kept monetary policy on hold last month, despite a widely held view in markets that it would pivot, following the surprise hike by the Swiss National Bank. Inflation in Japan has been modest, with nationwide CPI at 2.5% in May. The Tokyo CPI release for June showed that inflation remains sticky around this level. Yet the BoJ views a large chunk of inflation in Japan to be transitory, due to rising energy costs, and base effects from the sharp drop in mobile phone prices last year. For inflation to pick up, ultimately wages need to rise. Labor cash earnings for May came in at 1%. For Japan, this is a healthy print compared to recent history, but still pins real cash earnings at -1.8%, suggesting little risk of a wage inflation spiral. The Tankan survey for the second quarter provided a glimmer of hope. While large manufacturers (mainly exporters) sensed a deterioration in the outlook, domestic concerns were more upbeat. The large non-manufacturing index improved from 9 to 13 in the second quarter. The small non-manufacturing index improved from -6 to -1. Notably, capex intentions rose 18.6%, the highest level since the late 80s. The drivers of the yen remain clear and absolute. First, rising global interest rates put selling pressure on the yen and vice versa. Second, energy prices sap the trade balance, which is also negative. Should these factors abate (as they are currently), the yen will benefit. This week, we are reopening our short EUR/JPY trade, in addition to being short CHF/JPY. From a contrarian perspective, the yen is the cheapest G10 currency according to our PPP models. It also happens to be one of the most heavily shorted currencies, according to CFTC data. British Pound: Sterling Breaks Below 1.20 Chart 6Politics Will Keep Cable Volatile

Politics Will Keep Cable Volatile

Politics Will Keep Cable Volatile

The pound is down 11.1% year-to-date. Over the last month, the pound is down by 4.5% as a combination of economic and political headwinds hit sterling. Politically, the resignation of Prime Minister Boris Johnson is fueling sterling volatility. According to our geopolitical strategists, investors’ focus should be on whether UK national policy will change. This will require an election that replaces the Conservative Party-led government, or at least removes its single-party majority. Boris Johnson’s approval rating had been collapsing in recent days on the back of a series of scandals, so a less unloved leader under the same party will at least assuage public opinion, while keeping existing policies largely the same. The next milestones to watch for are an early election (unlikely since the Conservative Party still has an interest in prolonging until 2025) and a Scottish referendum for independence next year. Labor will also continue to benefit from a tailwind of high inflation and the mishandling of the pandemic by the Tories that has left voters largely frustrated. Economically, data in the UK continues its whiff of stagflation. CPI came out at 9.1% in May, the RPI accelerated to 11.7%, and nationwide housing prices came in at 10.7% in June, while retail sales are tanking, falling 4.7% year on year in June, excluding auto and fuel costs. The GFK Consumer confidence indicator hit a record low of -41 in June. Our report on sterling suggested that headwinds remain likely in the near term, but the pound is becoming more and more attractive for longer-term investors. We are currently long EUR/GBP. This cross still heavily underprices the risks to the UK economy in the near term. However, if recession fears ease, our suspicion is that cable is poised for a coiled-spring rebound. Canadian Dollar: The BoC Will Stay Hawkish Chart 7The CAD Has Decoupled From Oil Prices

The CAD Has Decoupled From Oil Prices

The CAD Has Decoupled From Oil Prices

The CAD is down 2.5% year-to-date. Over the last month, it is down 3.4%. Incoming data continues to suggest there is little reason for the BoC to change course in tightening monetary policy. The employment market remains strong. In May, 40K new jobs were added, and the details below the surface were notable. 135K full time jobs were swapped for 96K part time roles. Hourly wages rose 4.5% and the unemployment rate dipped to 5.1%. This sort of data is carte blanche for the BoC to keep hiking, since it signals a soft landing in the economy. Housing has been a point of contention for higher rates in Canada (given indebted households), but the Teranet national house price index shows that home prices are still rising 18.3% year-on-year in Canada as of May. This is occurring within the context of widespread price gains. Headline CPI came in at 7.7% in May, with all measures of the BoC’s trimmed estimates (core-common, core-median, core-trim), well above target and expectations. It will be interesting to watch how the BoC calibrates monetary policy given that the closely watched Business Outlook Survey showed a large deterioration in participants’ outlook for the future. In a world where USD strength persists, CAD will trade on the weaker side, but we remain buyers of the CAD once recession fears ebb. Australian Dollar: A Contrarian Play Chart 8A Jumbo Hike By The RBA

A Jumbo Hike By The RBA

A Jumbo Hike By The RBA

The Australian dollar is down 5.8% year- to-date. Over the last month, the AUD is down 5.3% as the price of iron ore declined by over 10% and the Chinese economy remained on lockdown. The RBA raised its interest rate by 50bps for a second month in a row this week. This aggressively shifted market expectations for further rate increases, with pricing in the OIS curve one year out rising from 3.35 to 3.51% today. While the RBA admitted global supply chain issues have contributed to inflation, capacity constraints in certain sectors and a tight labor market are also helping fuel domestic inflation. Particularly, the May employment report was robust, with 69.4K full-time jobs added, and a healthy jump in the participation rate to 66.7%. Job vacancies continued to grow at 13.8%. Rising rates in Australia are having the desired effect. Home price inflation is cooling, especially in places like Sydney. Demand for housing and construction remains robust, suggesting the RBA is achieving a soft landing in the economy. For example, home loan values are growing 1.7% and building approvals are growing by 9.9%. Demand also appears strong as manufacturing PMI came out at 56.2 in June. We are bullish the AUD against the dollar; however, short-term headwinds from Chinese lockdowns do not currently make us buyers of the currency. We are exiting our long AUD/USD position after being stopped out at 0.68 for a loss of -5.67%. New Zealand Dollar: Least Preferred G10 Currency Chart 9Terms Of Trade Are Waning For NZD

Terms Of Trade Are Waning For NZD

Terms Of Trade Are Waning For NZD

The NZD is down 9.7% this year. Over the last month, it is down 4.7%. New Zealand has the highest policy rate in the G10, and that is beginning to take a toll on interest-rate sensitive parts of the economy. REINZ house sales fell 28.4% year on year in May. House price inflation is also rapidly cooling. In June, the ANZ consumer confidence index fell from 82.3 to 80.5. Business confidence deteriorated from -55.6 to -62.6. The external sector is no longer a tailwind for the NZ economy, as grain and meat prices cool off. The price of dairy, approximately 20% of New Zealand’s exports, continues to decline with a 10% drop in June. The 12-month trailing trade balance continues to plummet, hitting -9.5bn NZD in May. The current account for May came in at -6.14 billion NZD versus a consensus -5.5 billion NZD. China is an important economic partner for New Zealand, with circa 27% of Kiwi exports China bound. Restrictions seem to be easing as the latest non-manufacturing PMI from China data came in at 54.7 against a previous 48.4 reading. The number of days required to quarantine on arrival also dropped to 10 days from 21 days in June. If this trend continues, it will be positive for the NZD; however, China does not appear to have an exit strategy for their zero-case COVID-19 policy. Within the G10 currency space, many other currencies appear more attractive than the kiwi, though our view is that NZD will benefit when US dollar momentum rolls over. Swiss Franc: A Safe Haven Chart 10A U-Turn From The SNB

A U-Turn From The SNB

A U-Turn From The SNB

CHF is down 6.4% year-to-date and flat over the past month versus the dollar. Against the euro, the franc is up 4.7% year-to-date and 5.2% over the past month. Our special report on the franc was timely, given the surprise rate hike announcement from the SNB last month. Amidst currency market volatility, EUR/CHF broke below parity. The SNB views currency strength as a virtue in today’s paradigm. As such, it has halted currency interventions, evident through the decline in sight deposits. Markets are pricing in another 50bps hike in September. Inflation continued to accelerate above projections in June. Headline and core CPI were up 3.4% and 1.9% year on year respectively, lower than other G10 countries but high enough to keep the SNB on alert. Inflation remains largely driven by the prices of imported goods which strengthens the case for a strong franc. The labor market is also tight, with unemployment at 2.2% in May. The outlook for the Swiss economy remains positive for the rest of the year, albeit with some signs of slowing activity emerging. The manufacturing PMI at 59.1 and the KOF leading indicator at 96.8 were both down to multi-month lows in June. The trade surplus in May was down to CHF 2bn. The franc is undervalued against the dollar and can serve as a good hedge for spikes in global volatility. Norwegian Krone: Improving The Current Account Chart 11NOK Has Decoupled From Oil Prices

NOK Has Decoupled From Oil Prices

NOK Has Decoupled From Oil Prices

The NOK is down 13.2% YTD and down 6.2% over the last month. Against the euro, the NOK is down 2.4% YTD and 1.3% in over the past month. In June, the Norges Bank raised the policy rate from 0.75% to 1.25%, 25bps higher than broadly anticipated. The rate path was also revised sharply higher and now corresponds to a 25bps hike at each meeting until the rate steadies at around 3% next summer. Governor Ida Wolden Bache left the door open for more half-point hikes but also highlighted the potential risk of overtightening, suggesting a balanced approach. Inflation in Norway is surprising to the upside. In May, CPI came in at 5.7% and 3.4% for core, signaling that price increases are becoming more broad-based. The labor market remains tight. The unemployment rate dipped to 1.7% in June, the lowest reading since 2008. Wages are projected to grow 3.9% this year. Together with a positive output gap, and a weak currency, both domestic and imported inflation could remain sticky for a while. Economic activity remains healthy in Norway. The manufacturing PMI went up to 56.4 in June, private consumption is robust, and business investment is expected to increase around 8% this year. Petroleum investments are also expected to pick up markedly in the years ahead, spurred by elevated energy prices and tax incentives. Recent natural gas production hikes, approved by the government, will further contribute to the healthy trade surplus. The strike started by union workers this week threatened to halt a significant portion of Norway’s oil and natural gas output. However, a resolution was found rather quickly. Despite record energy prices, the krone is one of the worst-performing majors this year. Pronounced global risk-off sentiment in the first half weighed on the currency. Despite potential challenges in the near term, Norway’s trade balance will remain a major tailwind this year. Shorting EUR/NOK on rallies looks attractive. Swedish Krona: Tracking The Euro Lower Chart 12The SEK Is At Capitulation Lows

The SEK Is At Capitulation Lows

The SEK Is At Capitulation Lows

The SEK is down 14.2% year-to-date and 7.1% over the last month. Inflation is becoming a problem in Sweden. In May, the CPIF increased 7.2% year on year, while the core measure was up 5.4%. In response, the Riksbank raised the policy rate by 50bps to 0.75% at its June meeting. The Riksbank sees the policy rate at around 1.75% by year-end, implying 50bps hikes at the remaining two meetings this year. The bank also announced a faster run-off in its balance sheet. We had anticipated the hawkish pivot by the Riksbank in early June, but that has not helped the Swedish krona much. Like Europe, the Swedish economy is being held hostage by external shocks, the global slowdown and an energy crisis. Signs of economic slowdown are becoming more pronounced. The Riksbank’s GDP forecast for 2022 was revised down by 1% to 1.8% and cut in half to 0.7% for 2023. Industrial production and new order data also point to a cooling in economic activity. Manufacturing and services PMIs remain expansionary zone but are falling rapidly. Notably, export orders have been hovering around the 50 boom/bust line over the last few months. Housing market is also vulnerable, with the Riksbank projecting a more-than-10% decline in prices by next year. That said, the SEK is below the 2020 lows suggesting these risks are well priced in. We are buyers of SEK on weakness. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Artem Sakhbiev Research Associate artem.sakhbiev@bcaresearch.com Thierry Matin Research Associate thierry.matin@bcaresearch.com Trades & Forecasts Strategic View Cyclical Holdings (6-18 months) Tactical Holdings (0-6 months) Limit Orders Forecast Summary

While BCA Research’s Emerging Markets Strategy service is not entirely convinced that US tech stocks are a bubble waiting to burst, they view the odds of this happening as nontrivial. There are a lot of similarities between dynamics prevailing in US tech…

Executive Summary Global risk assets are oversold, and investor sentiment is downbeat. In this context, a technical equity rebound cannot be ruled out. However, we do not think it will be the beginning of a major cyclical rally. The Fed and the stock market remain on a collision course. An equity rally and easing financial conditions would make the Fed even more resolute to continue hiking interest rates. There are many similarities between dynamics that prevailed in US tech stocks and in previous bubbles. While it is not our baseline view, the odds of a protracted bear market are nontrivial. Resource prices and commodity plays have more downside. The History Of Financial Bubbles: Is This Time Different?

On A Bull Case, Bubbles And Commodity Prices

On A Bull Case, Bubbles And Commodity Prices

Bottom Line: The decline in commodity prices and the relentless US dollar rally will ensure that EM currencies, bonds and stocks continue to sell off even if the US equity market rebounds in the near term. Feature Among the most frequently discussed topics in recent client calls are the upside and downside risks to our baseline view. We elaborate on these risks in this report. To recap, our baseline view is as follows: EM and DM stocks have another 15% downside in USD terms, the US dollar will continue overshooting and commodity prices will fall. Global yields are topping out, and the US yield curve will soon invert. Hence, defensive positioning for absolute-return investors is still warranted, and global equity and fixed-income portfolios should continue to underweight EM. The rationale is that US and EU demand for goods ex-autos, and hence global trade, is about to contract while the Fed is straightjacketed by high and broad-based inflation. China’s economy will be struggling to recover. In EM ex-China, domestic demand will relapse. Chart 1Will The S&P 500's Technical Support Hold?

Will The S&P 500's Technical Support Hold?

Will The S&P 500's Technical Support Hold?

If one believes that the US equity bull market that began in 2009 is still alive (i.e. the March 2020 selloff is a short-lived red herring), odds are that the S&P 500 drawdown is over. The reasoning is that the S&P 500 is already down 23% from its 2021 peak, on par with the selloffs that occurred in 2011, 2015-16 and 2018 (Chart 1). However, if one believes that the structural bull market is over, the magnitude of the current equity selloff is likely to exceed the ones in 2011, 2015-16 and 2018. Hence, a bearish stance is still warranted. As we argue below, after a 12-year bull run, the excesses in the US equity market in general, and US tech stocks in particular, have become extreme. There are many signs of a bubble, or at least of a major top. Even though we risk overstaying in our negative view, our bias is that the global equity market rout is not yet over. A Bullish Scenario A (hypothetical) bullish case would look something like this: Weakening global and US growth and falling commodity prices bring down US inflation and Treasury yields. As US bond yields drop further, the S&P 500 rallies given their negative correlation of the past 18 months or so. As US inflation declines rapidly, the Fed makes a dovish pivot, reinforcing the risk asset rally and reversing the US dollar’s uptrend. Finally, Chinese stimulus produces a robust business cycle recovery in China that propels commodity prices higher and lifts the rest of EM out of the abyss. Chart 2Keep An Eye On Rising US Trimmed-Mean Inflation

Keep An Eye On Rising US Trimmed-Mean Inflation

Keep An Eye On Rising US Trimmed-Mean Inflation

In our opinion, this scenario has no more than a 25% chance of playing out. Even if there are apparent signs of a US/global slowdown, elevated US core inflation and accelerating wages and unit labor costs would keep the Fed from dialing down its hawkishness Critically, even though US core PCE inflation has rolled over and will likely decline further, its trimmed-mean PCE inflation is rising (Chart 2). The latter means that inflation is broadening even as some volatile items like food, energy and used-auto prices deflate. As we have written extensively, wages and inflation are lagging variables. Despite the ongoing slowdown in the US economy, it will take many months before the underlying core inflation rate drops below 3%. We maintain that the Fed and the stock market remain on a collision course. An equity rally and easing financial conditions would make the Fed even more resolute to hike interest rates. The basis is that even if core inflation falls in the coming months, it would still be well above the Fed’s target of 2%. Notably, the Fed has recently communicated that its commitment to bring down inflation to 2% is unconditional. Chart 3The Anatomy Of The US Equity Bear Market In 2000-2002

The Anatomy Of The US Equity Bear Market In 2000-2002

The Anatomy Of The US Equity Bear Market In 2000-2002

This policy stance represents a major departure from the past several decades when the Fed was very sensitive to any tightening in financial conditions and often eased preemptively. In short, with inflation still well above its target, the Fed will, for now, err on the side of hawkishness if financial conditions ease. Importantly, US corporate profits will likely contract even if US real GDP does not shrink. As US corporate top-line growth slows and unit labor costs accelerate, profit margins will shrink. For example, the 2001-2002 recession was very mild – consumer spending did not contract at all, and housing boomed (Chart 3, top two panels). Yet, the S&P 500 operating earnings dropped by 30%, and the S&P 500 fell by 50% (Chart 3, bottom two panels). In brief, a devastating bear market does not necessarily require a hard landing. Concerning China, the recovery will likely be U-shaped rather than V-shaped with risks skewed to the downside. Finally, contracting global trade and falling commodity prices will continue, which are negative for EM currencies and assets. Notably, industry data from Taiwan’s manufacturing PMI suggest that the slowdown in the Asian and global economies is widespread. Taiwan’s substantial trade linkages with mainland China signify that the slowdown is not limited to the US and the EU but includes China too. Taiwanese PMI export orders of both semiconductor and basic material producers have plunged to 40 and 30, respectively (Chart 4). Barring a quick turnaround, global semiconductor and basic materials stocks have more downside. Even as US Treasury yields drop, the dollar will continue firming versus EM currencies, including those of Emerging Asian countries. In such a scenario, EM stocks and bonds will weaken further (Chart 5). Chart 4A Broad-Based Contraction In Global Trade Is In The Cards

A Broad-Based Contraction In Global Trade Is In The Cards

A Broad-Based Contraction In Global Trade Is In The Cards

Chart 5A Free Fall In EM Ex-China Stocks And Currencies

A Free Fall In EM Ex-China Stocks And Currencies

A Free Fall In EM Ex-China Stocks And Currencies

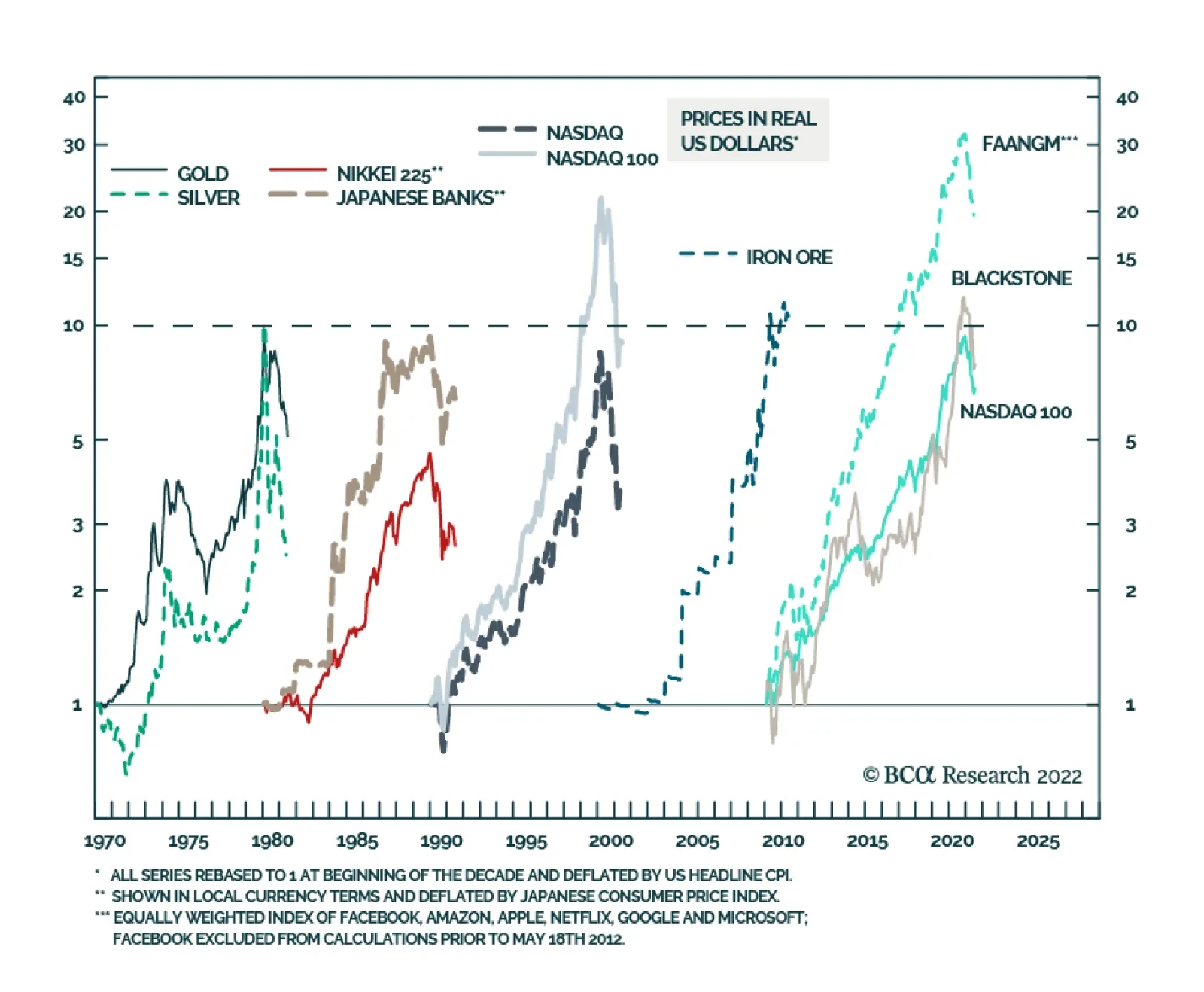

Bottom Line: The S&P 500 is oversold, and investor sentiment is downbeat. In this context, a technical equity rebound can occur at any moment. However, we do not think it will be the beginning of a major cyclical rally. A Bearish Case: Are US TMT Stocks A Bubble? What is a more bearish scenario than our baseline case? The bursting of bubbles or the unwinding of excesses would entail a more protracted and devastating bear market than the 15% drop in global share prices we currently expect. We can identify two major excesses in the global economy and financial system: In US TMT (Technology, Media & Entertainment and Internet & Catalog Retail) stocks and private equity In Chinese real estate. We have written extensively about property market excesses in China. Below we discuss the recent sharp selloff in commodities, which is partially linked to Chinese property construction. We also present the case for major excesses in US stocks. Chart 6 illustrates the history of bubbles of the past several decades: The Nifty-fifty (involving the 50 US large-cap stocks) bubble occurred in the 1960s and burst in the 1970s (not shown in the chart). The commodity bubble took place in the 1970s and burst in the 1980s. Japanese equity and property prices rose exponentially in the 1980s and deflated in the 1990s. The Nasdaq bubble occurred in the 1990s and was shattered in the early 2000s. Commodities/EM/China were the leaders of the 2000s, and they were devastated in the 2010s. We use iron ore in this chart because its price surged the most in the 2000s. FAANGM stocks, the Nasdaq 100 index and private equity were by far the biggest beneficiaries of the 2010s. No one can be certain about bubbles in real time because there are always superior fundamentals or persuasive stories that justify exponential price appreciation. That said, there are a lot of similarities between dynamics prevailing in US tech and private equity and in previous bubbles: In the past decade, FAANGM stocks, the Nasdaq 100 index and private equity companies registered gains comparable to the bubbles of the previous 60 years. Furthermore, as Chart 6 illustrates, the equal-weighted FAANGM index in inflation-adjusted terms rose 30-fold, much more than the bubbles of the previous decades. The Nasdaq 100 index and share prices of Blackstone, the largest private equity company, have risen by nearly 10-fold in real (inflation-adjusted terms) between 2010 and the end of 2021. Chart 6The History Of Financial Bubbles: Is This Time Different?

On A Bull Case, Bubbles And Commodity Prices

On A Bull Case, Bubbles And Commodity Prices

The final phase of bubbles is often characterized by growing retail investor participation. This is exactly what happened with US tech/new economy stocks. Chart 7US TMT Stocks: Exponential Growth Rarely Ends Well

US TMT Stocks: Exponential Growth Rarely Ends Well

US TMT Stocks: Exponential Growth Rarely Ends Well

Toward the end of the decade, not only retail but also institutional capital stampedes into the winners of the decade. This played out with US large-cap tech stocks as well as in private equity and private debt spaces. Inflows into private equity and private debt have been enormous. As a result of these inflows into US large-cap stocks, the market cap share of US TMT stocks as a percentage of total US market cap has surpassed 40%, its peak in 2000 (Chart 7). Bubbles often thrive during periods of low interest rates and crash when the cost of capital rises. This is exactly what has been happening in global financial markets since early 2019. The parameters of the overall US equity market were also excessive prior to this bear market. As of last year, the S&P 500 stock prices in real (inflation-adjusted) terms became as elevated relative to their long-term time trend as they were in the late 1960s and the late 1990s − the peaks of previous secular bull markets (Chart 8, top panel). Chart 8The S&P 500 and Operating Profits: A Long-Term Perspective

The S&P 500 and Operating Profits: A Long-Term Perspective

The S&P 500 and Operating Profits: A Long-Term Perspective

Chart 9Equity Issuance Marks Market Tops

Equity Issuance Marks Market Tops

Equity Issuance Marks Market Tops

The S&P 500’s operating earnings in real terms have surpassed two standard deviations above its time trend (Chart 8, bottom panel). Some sort of mean reversion to its long-term trend is in the cards. US corporate profits have benefited from fiscal/monetary stimulus, low labor costs and pricing power. All of these are now working against profits. Finally, new share issuance in the US mushroomed in 2021, another sign of a major top (Chart 9). Bottom Line: We are not entirely convinced that US TMT stocks are a bubble waiting to burst. Yet, the odds of this happening are nontrivial. This time might not be different. A Word On Commodities The selloff in the commodity space has been broad-based. Odds are that it will continue for the following reasons: A global business cycle downtrend is always bearish for commodity prices. In fact, oil prices are often lagging and are typically the last shoe to drop during global slowdowns. US sales of gasoline have started to contract. Besides, Saudi Arabia will likely increase its oil output and shipments following President Biden’s visit to the Kingdom next week. Chart 10Investors Have Been Long Commodity Futures

Investors Have Been Long Commodity Futures

Investors Have Been Long Commodity Futures

As we have argued in recent months, China’s demand for commodities was contracting and, in our opinion, the rally in resource prices over the past 12 months was supported by investment demand for commodities, i.e., financial inflows into the commodity space. Many portfolios have bought commodities as an inflation hedge. When a hedge becomes a consensus trade and crowded, it stops being a hedge. Chart 10 demonstrates that net long positions in 17 commodities have been very elevated. The speed at which liquidation is taking place corroborates our thesis that it is investors not producers or consumers who have been caught being long commodities. China’s business cycle recovery will be U-shaped at best. Domestic orders point to weaker import volumes in the months ahead (Chart 11, top panel). Corporate loan demand has plunged suggesting that liquidity provisions by the PBoC might fail to produce a meaningful recovery in credit growth (Chart 11, bottom panel). Finally, technicals bode ill for commodity prices. As Chart 12 illustrates, copper prices and global material stocks have probably formed medium-term tops, and risks are skewed to the downside. Chart 11China: The Economy Is Struggling To Gain Traction

China: The Economy Is Struggling To Gain Traction

China: The Economy Is Struggling To Gain Traction

Chart 12A Major Top In Commodity Prices?

A Major Top In Commodity Prices?

A Major Top In Commodity Prices?

Bottom Line: Commodity prices and their plays have more downside. Investment Strategy The decline in commodity prices and the relentless US dollar rally will ensure that EM currencies, bonds and stocks continue to sell off even if the US equity market rebounds in the near term driven by lower Treasury yields. Global equity and fixed-income portfolios should continue underweighting EM. We also continue to short the following currencies versus the USD: ZAR, COP, PEN, PLN, PHP and IDR; as well as HUF vs. CZK, and KRW vs. JPY. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Strategic Themes (18 Months And Beyond) Equities Cyclical Recommendations (6-18 Months) Cyclical Recommendations (6-18 Months)

Executive Summary Caught In Risk-Off Selling

Copper Testing Support

Copper Testing Support

Weak Chinese and European economies are suppressing copper demand and helping to temper prices in a market that remains fundamentally tight. Weaker US GDP growth could put the three largest economies in the world in or close to recession in 2H22/1H23, which would contribute to demand-side weakness in copper markets. The odds manufacturing and base-metals refining will be curtailed in Europe are rising. Although a strike in Norway has been averted by government intervention, maintenance on Russia’s Nord Stream 1 pipeline scheduled to begin next week likely will serve as a pretext for longer and deeper natgas supply cuts to the EU. Bottom Line: Despite fundamental tightness in global copper markets, prices are being restrained by fears weaker Chinese and European economic performance will lead to a global recession. Early reads of US GDP pointing to negative growth in 2Q22 stoke these fears. Heightened economic policy uncertainty globally exacerbates them. We remain fundamentally bullish copper and will re-establish our long SPDR S&P Metals & Mining ETF (XME) – down ~ 40% from its highs in April – at tonight’s close. In addition, we went long the XOP oil and gas ETF at Tuesday’s close, after prompt Brent breached the buy-trigger we set last week of $105/bbl during this week’s crude-oil sell-off. Feature Lower GDP growth expectations in China and the EU – along with a wobbly US economy being flagged by an Atlanta Fed GDPNow forecast pointing to negative growth in 2Q22 – are stoking fears of a global manufacturing and industrial recession. This prompted a rout in industrial commodities – base metals and oil – this week, which still has markets on edge. This slow-down in the world’s three largest economies – accounting for almost 50% of global GDP expressed in purchasing-power terms – is the only thing keeping the level of global copper demand close to supply at present (Chart 1).1 At least for the time being, this is keeping the threat of sharply higher copper prices, which would be more in line with the low levels of supplies and inventories globally, at bay (Chart 2). As of the week ended May 27th, global copper stocks stood at just above 562k tons, which is ~ 31% lower y/y. Chart 1World’s Biggest Economies Slowing

Copper Prices Decouple From Fundamentals

Copper Prices Decouple From Fundamentals

Chart 2Copper Prices Disconnect From Fundamentals

Copper Prices Disconnect From Fundamentals

Copper Prices Disconnect From Fundamentals

Uncertainty Weakens Copper Prices Energy and metals markets remain extremely tight on a fundamental supply-demand basis.2 The sharp sell-off this week in oil and metals prices is, in our view, evidence industrial-commodity prices have decoupled from fundamentals. This makes traders – hedgers and speculators – extremely risk-averse, which reduces liquidity and increases volatility. On the back of these concerns, markets exhibit the sort of volatility associated with economic collapse, despite still-strong underlying fundamentals. Chart 3Rising Global Policy Uncertainty

Copper Prices Decouple From Fundamentals

Copper Prices Decouple From Fundamentals

Volatility is on the rise due to increasing economic uncertainty in these markets. This makes it extremely difficult to assign probabilities to different price outcomes (i.e., true uncertainty). The BBD Global Economic Policy Uncertainty is approaching levels seen during the early pandemic (Chart 3). We put this rising uncertainty down to poor policy and communication from central banks and governments; a pig’s breakfast of energy policy globally that increasingly adds nothing but confusion to markets; and a muddled public-health policy in China, which produces random shut-downs in global supply chains as covid infections randomly crop up in important port cities. Lastly, the East and West are moving toward a new Cold War, which already is having profound effects on all markets, trade flows and capital availability in the short- and medium-term. This keeps markets on edge and forces them to parse every geopolitical development that hits the tape.3 Re-forging supply chains, re-building basic industrial infrastructure as the West moves away from outsourcing to China and other EM states will be costly and volatile, especially as embargoes and sanctions increase between these blocs. This political and economic evolution will require increased investment in base metals production and exploration, along with similar commitments to oil and gas. Low and volatile prices will not support this, as they disincentivize investment, and set markets up for continued shortage and scarcity going forward. In the metals markets, years of underinvestment by major mining companies will keep copper supplies and inventories tight going forward (Chart 4). This will hinder and delay the global renewable-energy transition, which cannot be realized without higher base-metals supplies. Chart 4Structural Underinvestment In Mining Fundamentally Bullish Copper

Copper Prices Decouple From Fundamentals

Copper Prices Decouple From Fundamentals