Developed Countries

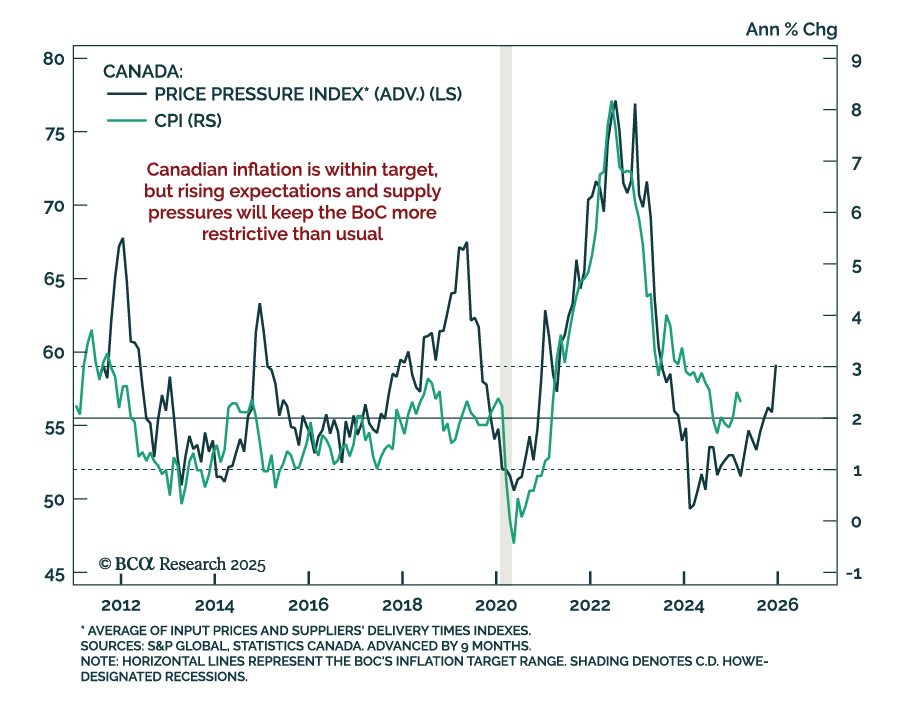

Cooler inflation will not shift the BoC’s stance, as stagflation limits potential easing, keeping us neutral on Canadian bonds. In March, headline CPI slowed more than expected to 2.3% y/y from 2.6%. However, lower energy prices drove much of the downside…

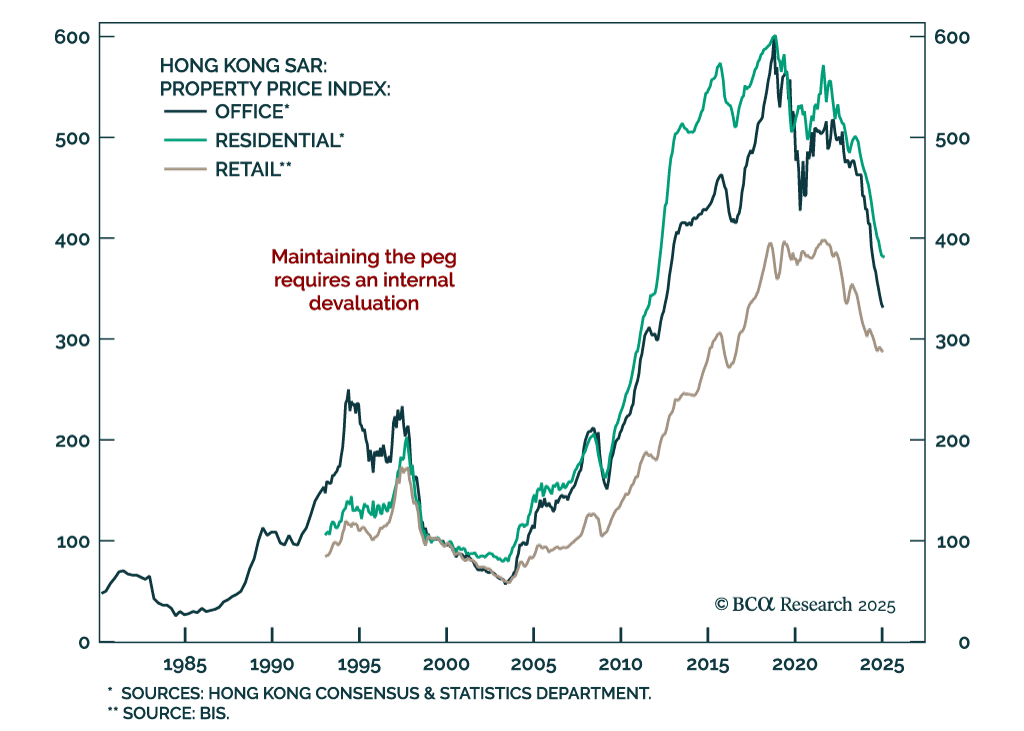

Our FX strategists expect the HKD peg to hold, but at the cost of prolonged economic weakness and debt deflation in Hong Kong. Interest rates remain too high for the local economy, yet monetary easing is off-limits due to the peg.The currency’s…

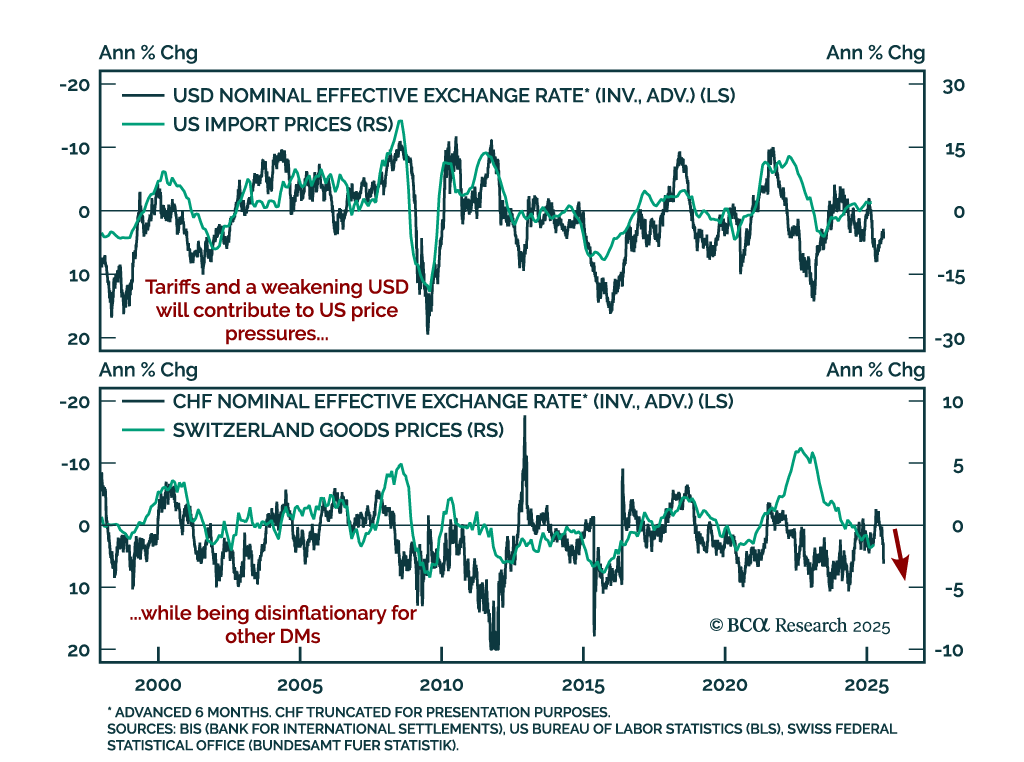

Tariff-driven inflation is diverging across economies, with the US facing mounting pressures while disinflation persists elsewhere. In theory, US tariffs should strengthen the dollar and weaken targeted currencies. In practice, the opposite has occurred: The…

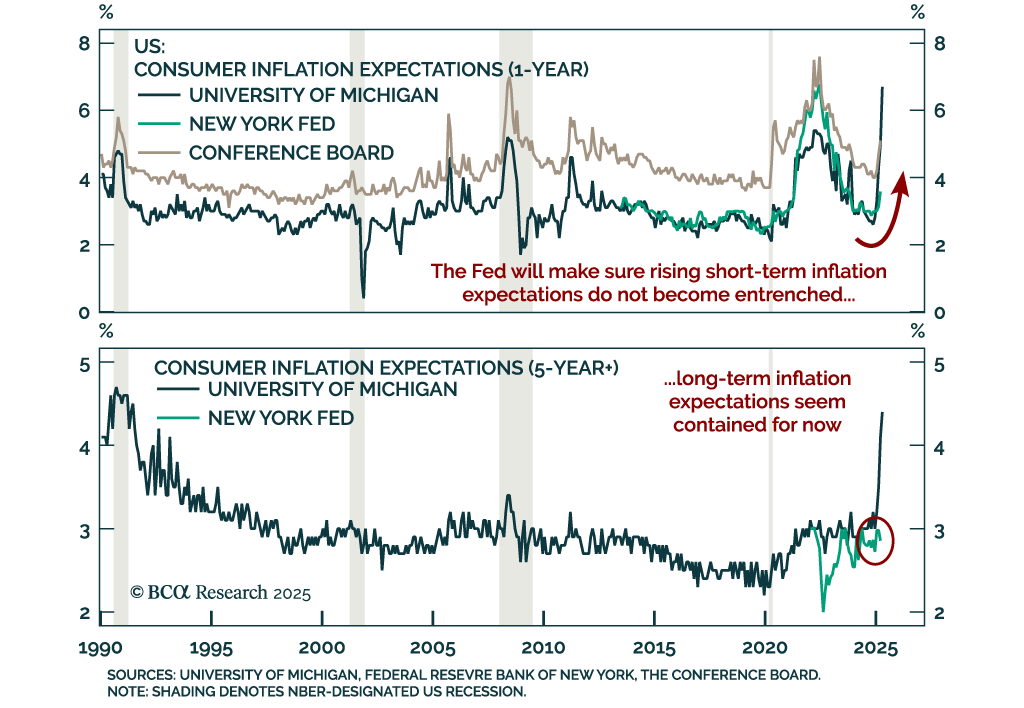

The latest NY Fed Survey of Consumer Expectations reinforces our defensive stance, with growth concerns deepening even as long-term inflation expectations remain anchored. The survey is a useful cross-check against broader sentiment and inflation indicators,…

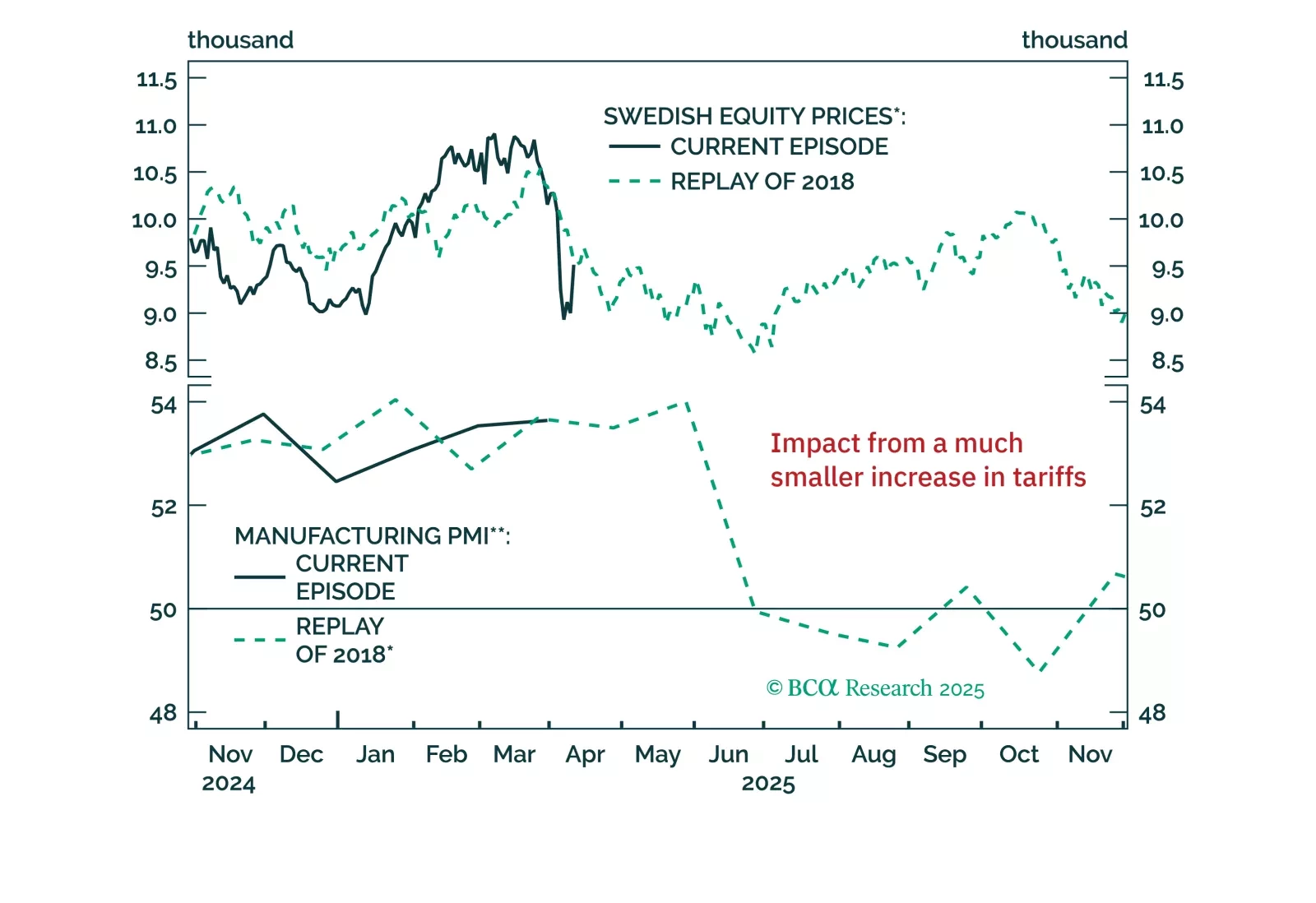

Europe’s near-term outlook remains clouded by uncertainty, even after the tariff reprieve. Our latest update breaks down why the risks to growth, profits, and financial conditions are still skewed to the downside — with Sweden standing out as a key bellwether.

The sharp drop in consumer sentiment and rise in inflation expectations reinforce our defensive positioning and preference for long-duration bonds. The preliminary April University of Michigan Consumer Sentiment Index fell to 50.8 from 57.0 in March, missing…

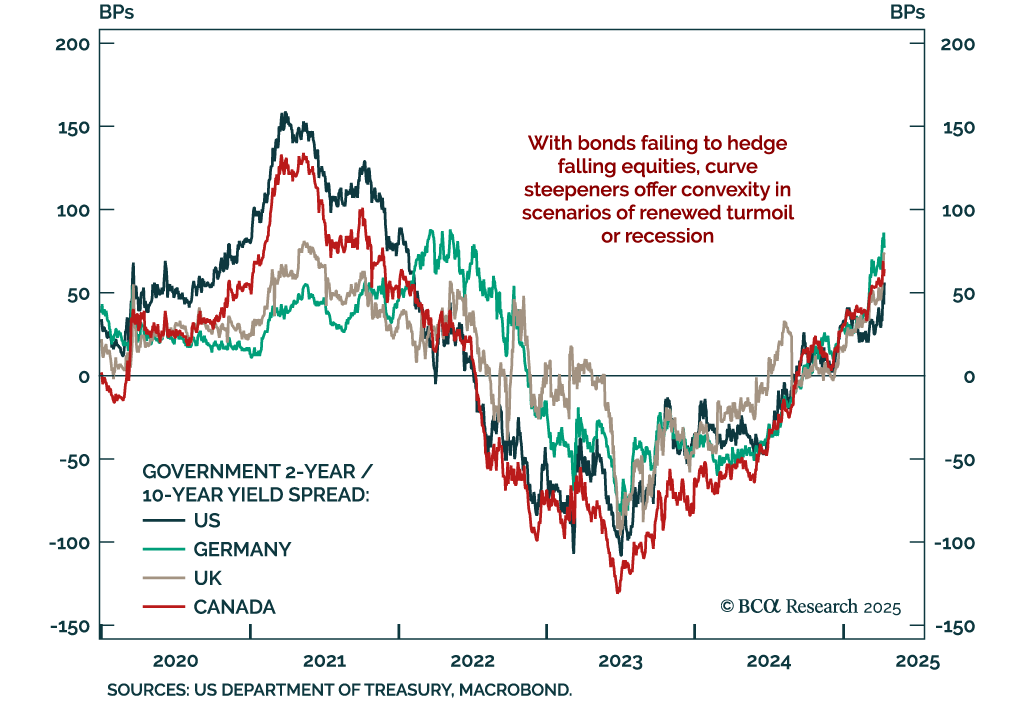

Bonds are failing to deliver defensive convexity; asset allocators should look to tactical curve steepeners for protection. Despite rising growth fears, Treasury yields have risen sharply at the long end. This is a clear break from the typical recession…

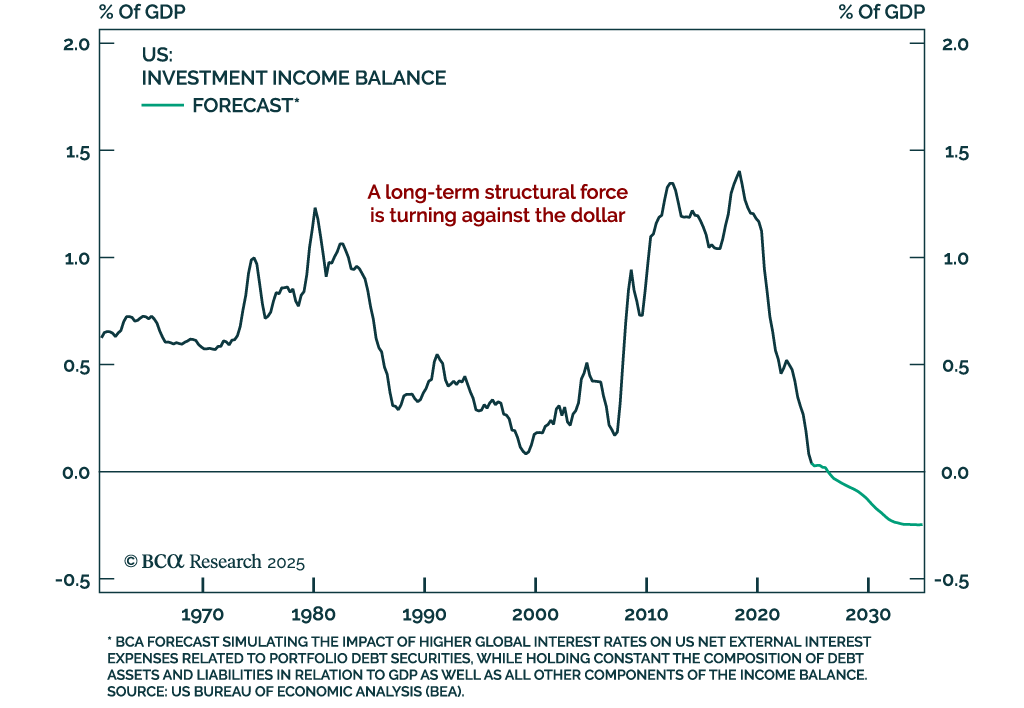

The US dollar’s reserve status is not done, but its foundations are starting to crack. Our Chart Of The Week comes from Juan Correa, Chief Global Asset Allocation Strategist. Most defensive currencies, like the yen and the Swiss franc, benefit from a positive…

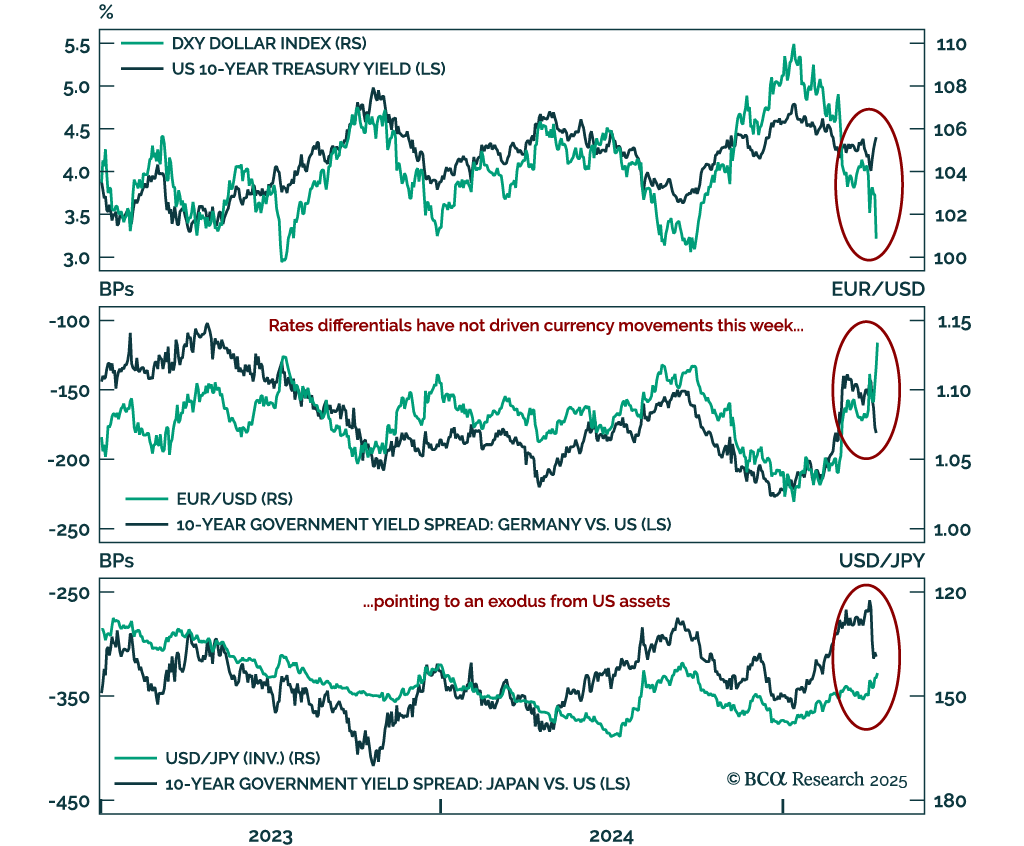

The recent breakdown in cross-asset correlations highlights mounting risk premia on US assets. Last week, the long-standing correlations underpinning our understanding of global markets violently broke down. The Treasury market turmoil had already broken the…

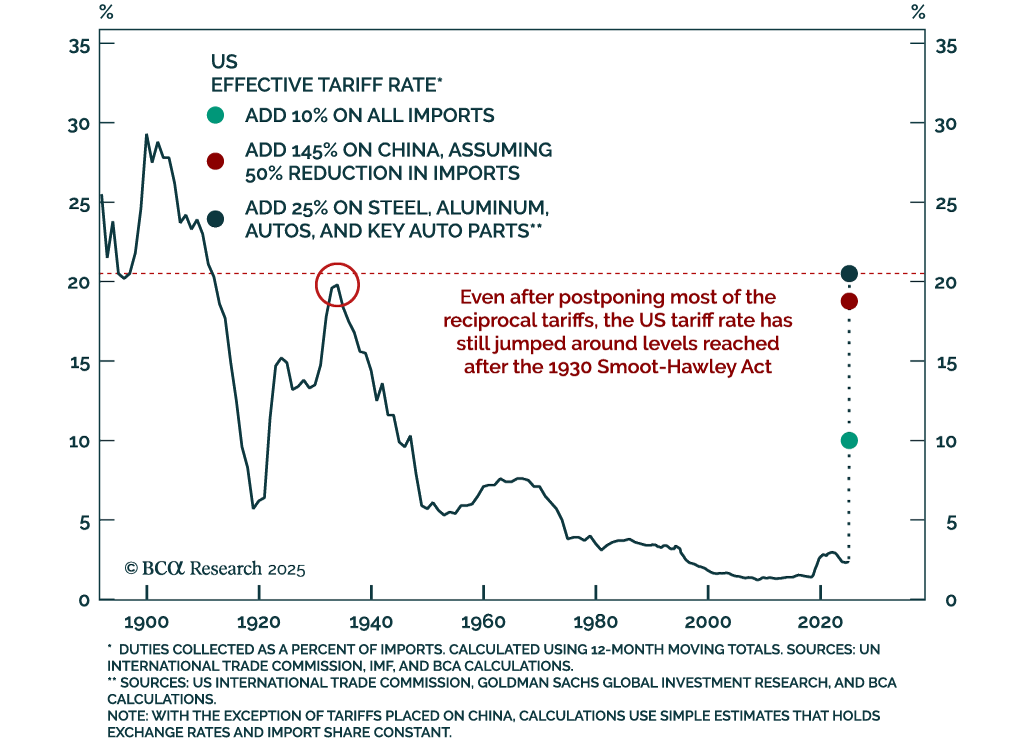

Our Global Investment Strategists remain defensive, expecting a global recession in the coming months unless the trade war de-escalates meaningfully. They maintain a year-end S&P 500 target of 4450, with downside risk to 4200.While reciprocal tariffs were…