Developed Countries

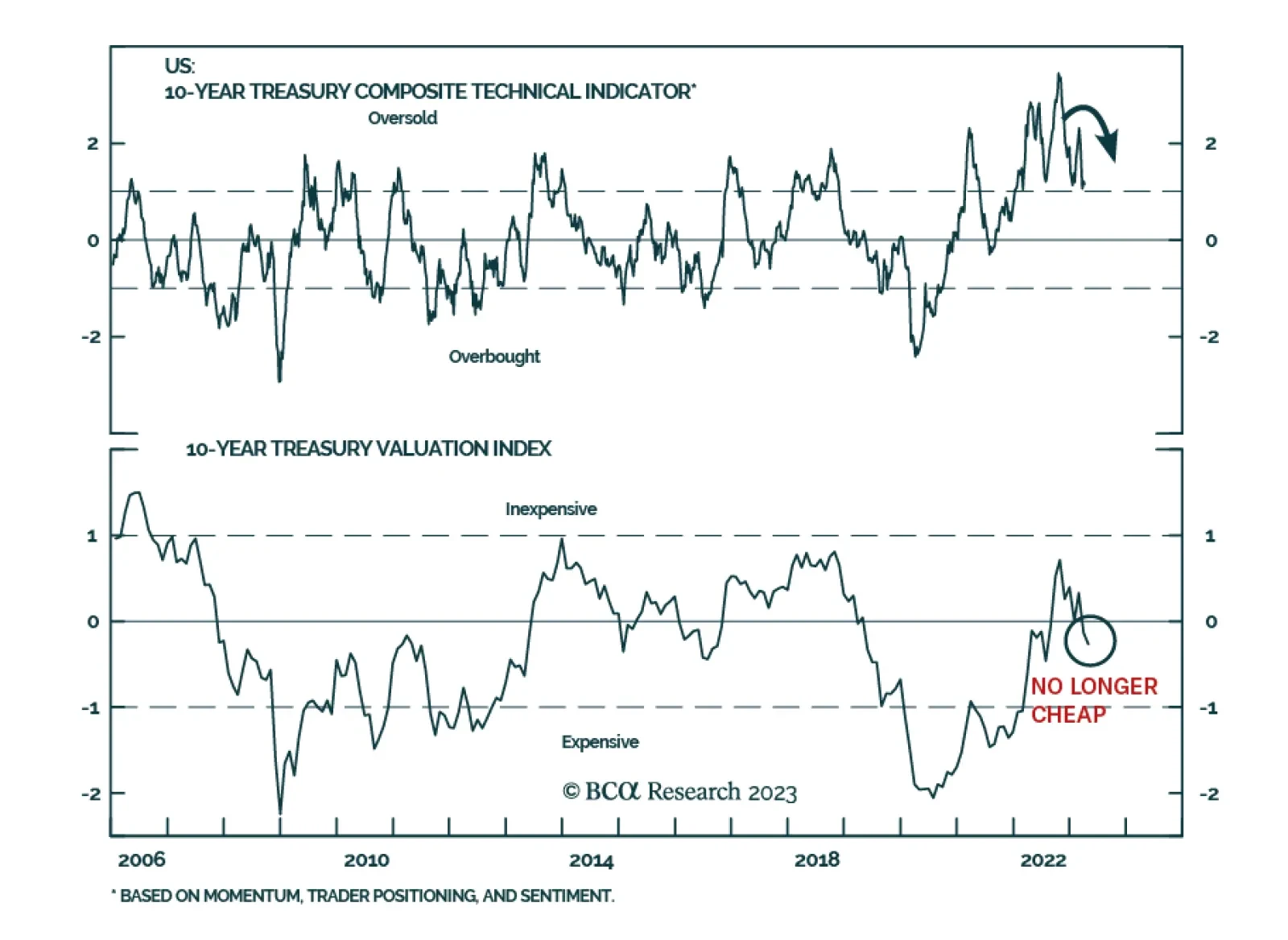

Today’s releases of the March CPI and March FOMC minutes do not change our view that the Fed will deliver one more 25 basis point rate increase before going on hold.

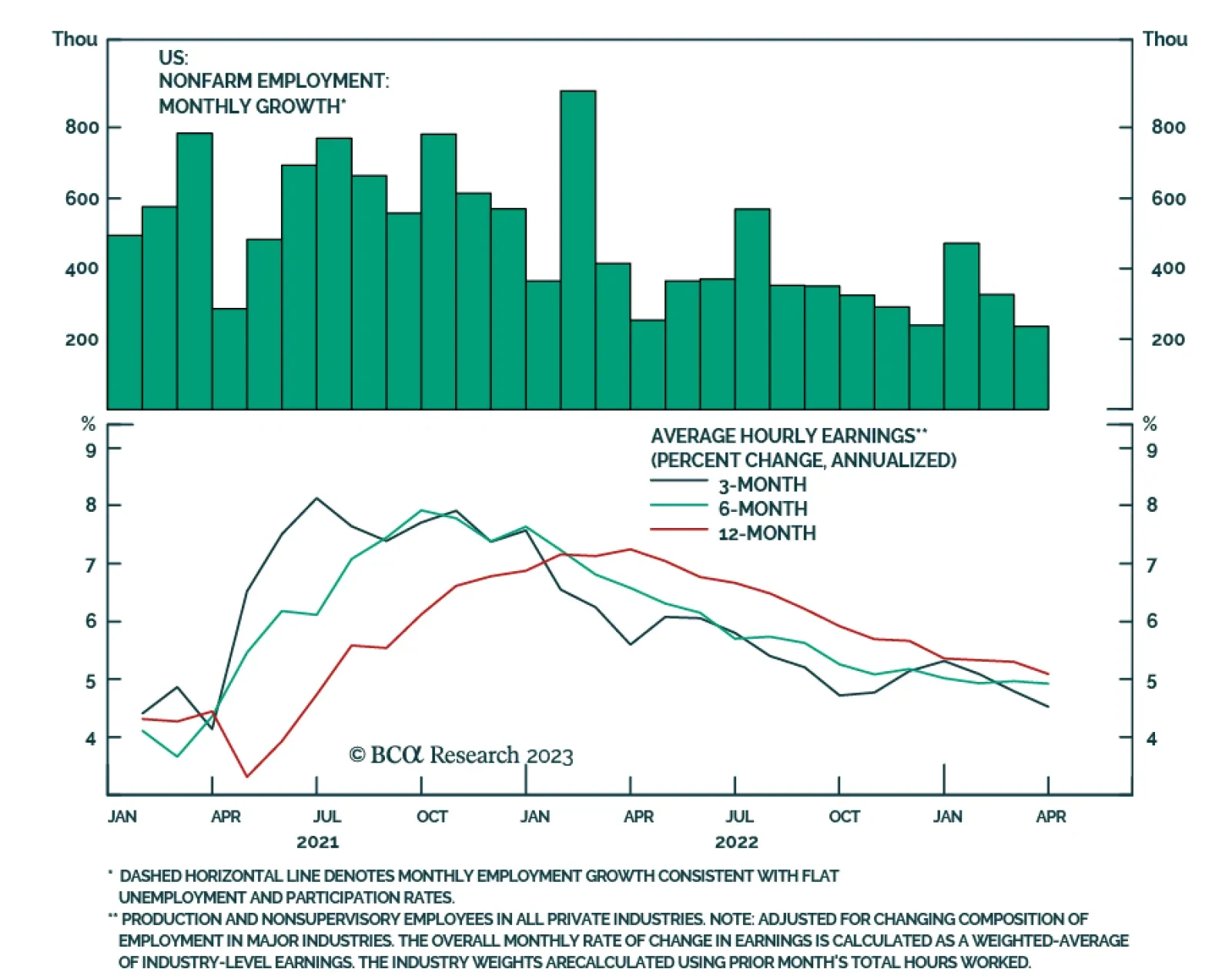

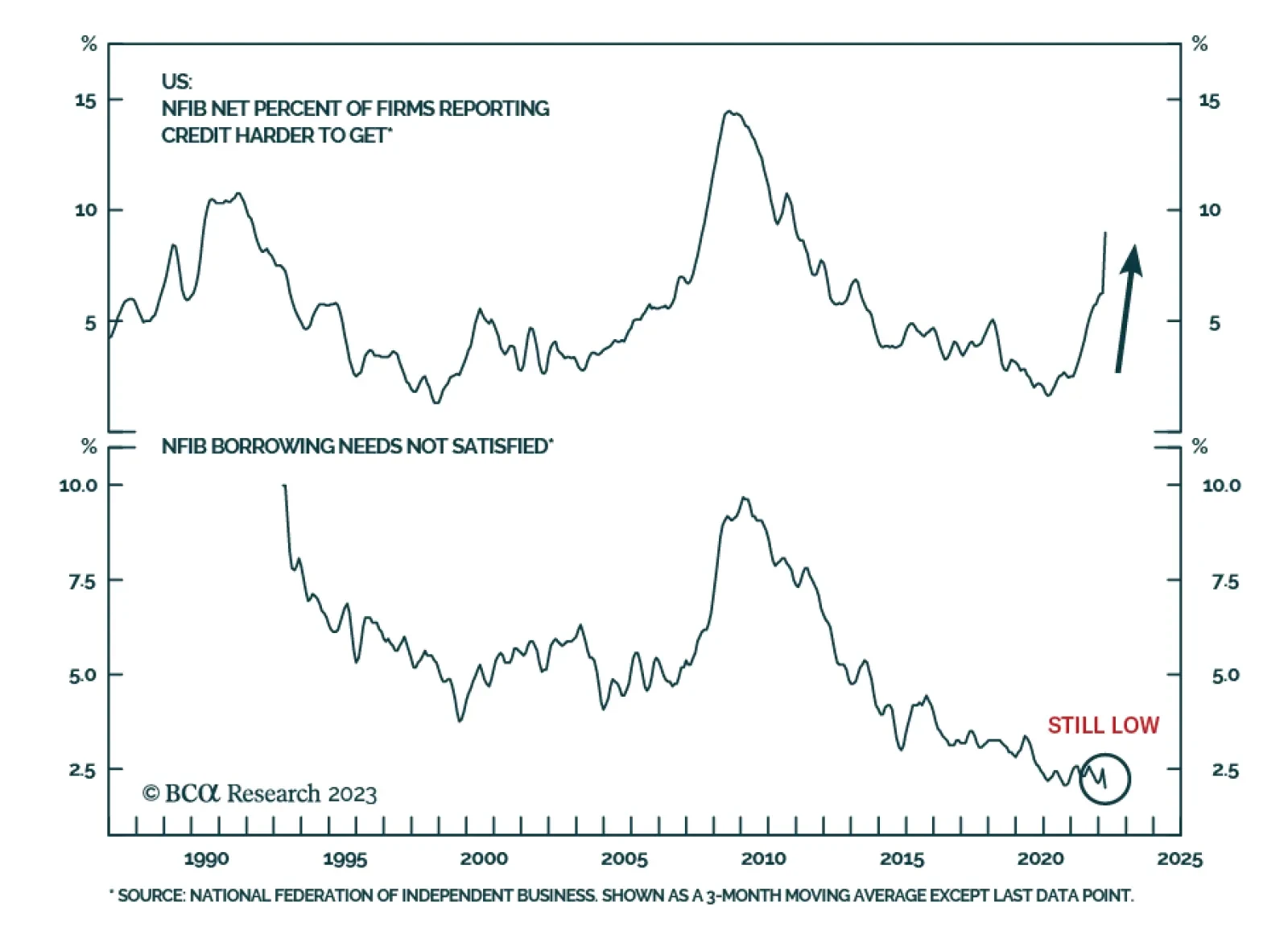

Through February and March, the number of US ‘job losers’ surged by almost half a million. Constituting the largest two-month increase in Americans who have lost their job since the depth of the pandemic. Unless we see a big drop in the number of job losers in the coming months, the correct investment strategy is still to position for a US recession that starts in 2023.

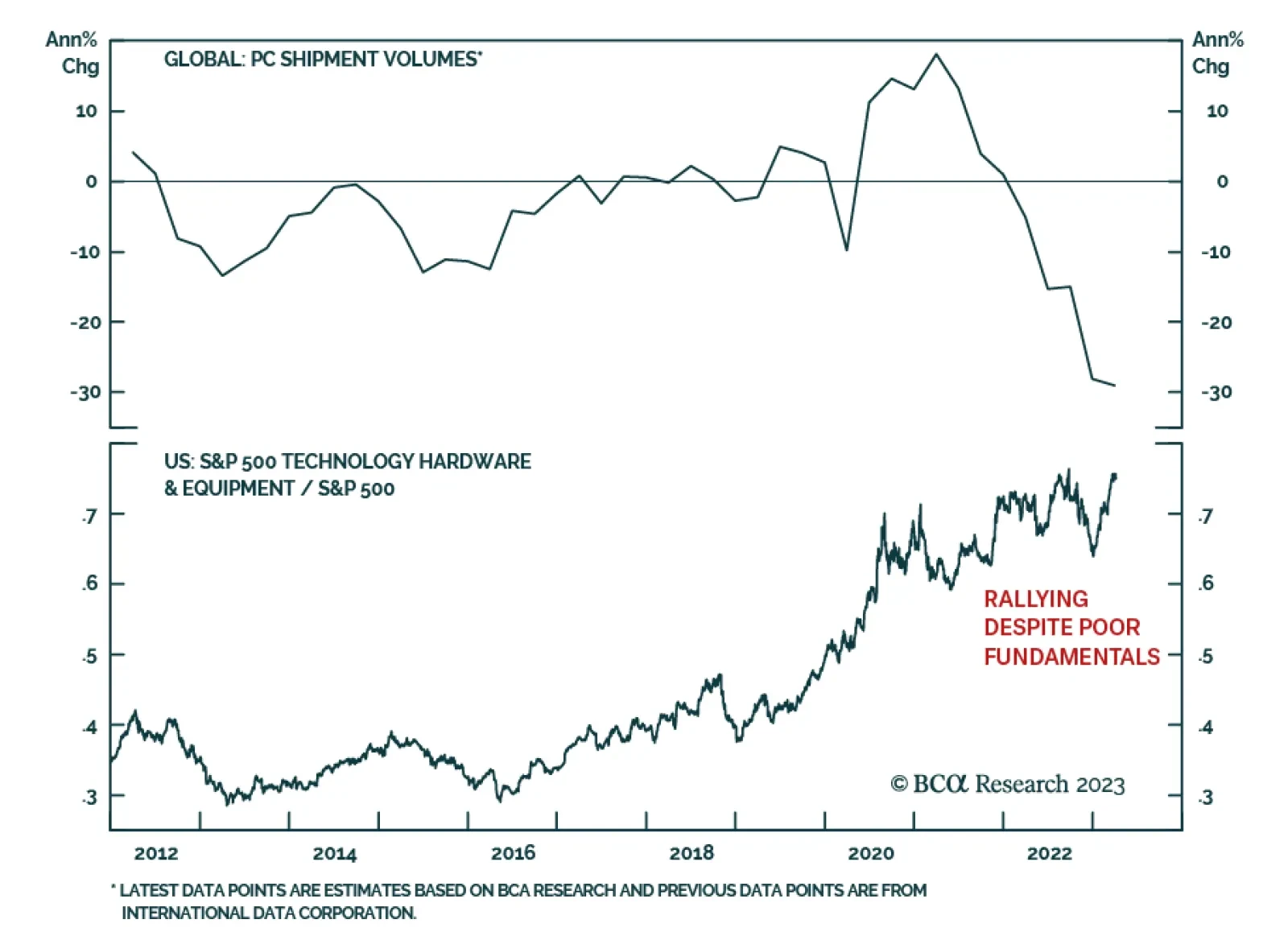

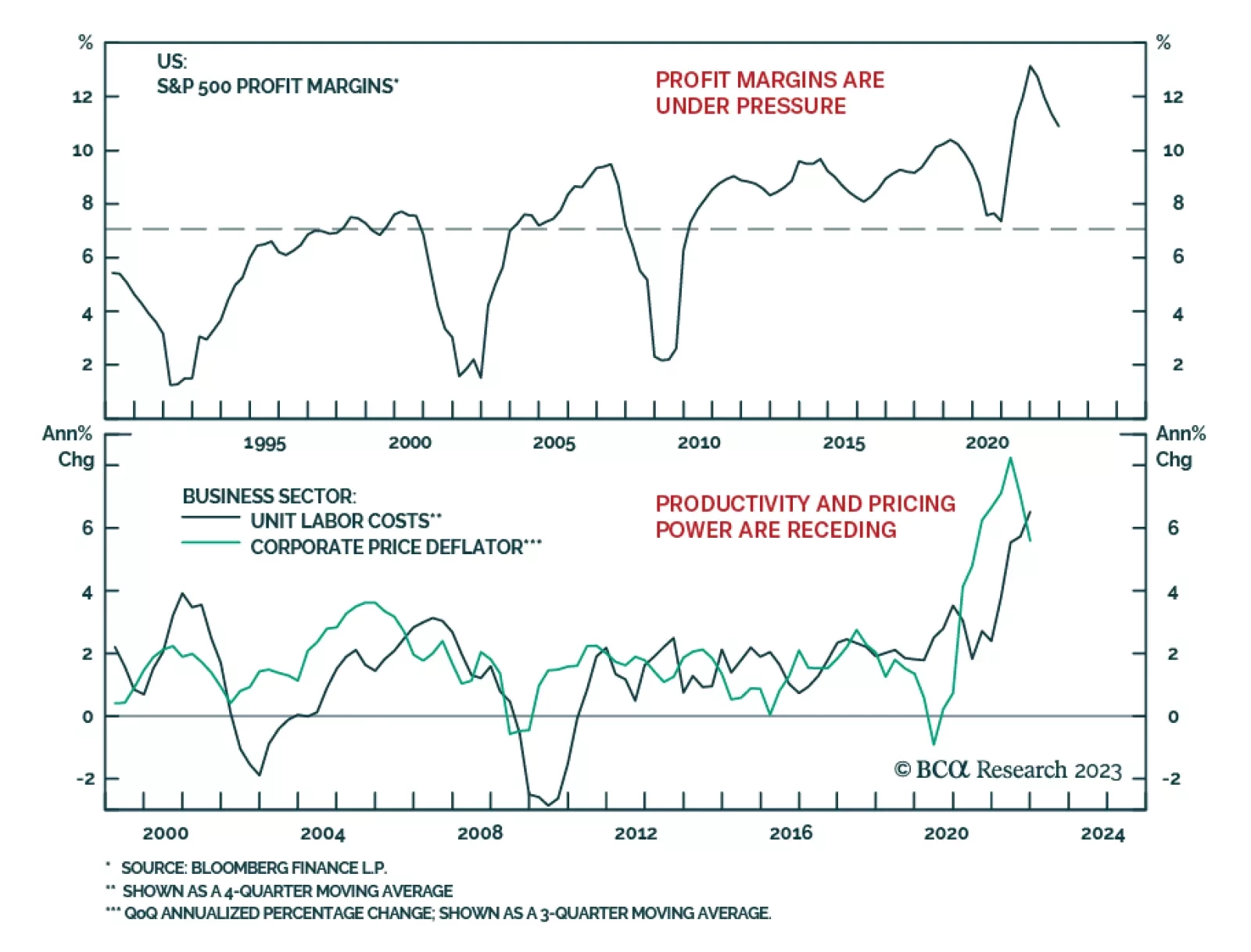

Several signs have emerged that the “bad news is good news” rally has run its course. Despite deteriorating economic data, the Fed is expected to maintain its “higher for longer” stance, disappointing the market. A rate cut is likely is only in case of a severe downturn, but that will not offer support to equities, until earnings growth bottoms. We recommend shifting a portfolio toward a defensive stance, and away from cyclicals at this juncture. We downgrade Auto to an underweight, and Capital Goods and Energy Equipment and Services to an equal weight.