Developed Countries

Although our take has not changed yet, the immediate emergence of a second wave of banking system stresses poses a new threat to our constructive near-term economic and market views and will have to be monitored carefully.

The initial phase of the EU’s ambitious CBAM will launch 1 October and will begin collecting a carbon tax in 2026. Between now and then, it will be challenged as it attempts to put a price tag on CO2 emissions as imports cross the EU border. The CBAM will impart an inflationary bias in EU commodity and goods markets as 2026 draws near and importers have to secure EU ETS credits, the number of which, by design, will contract over time.

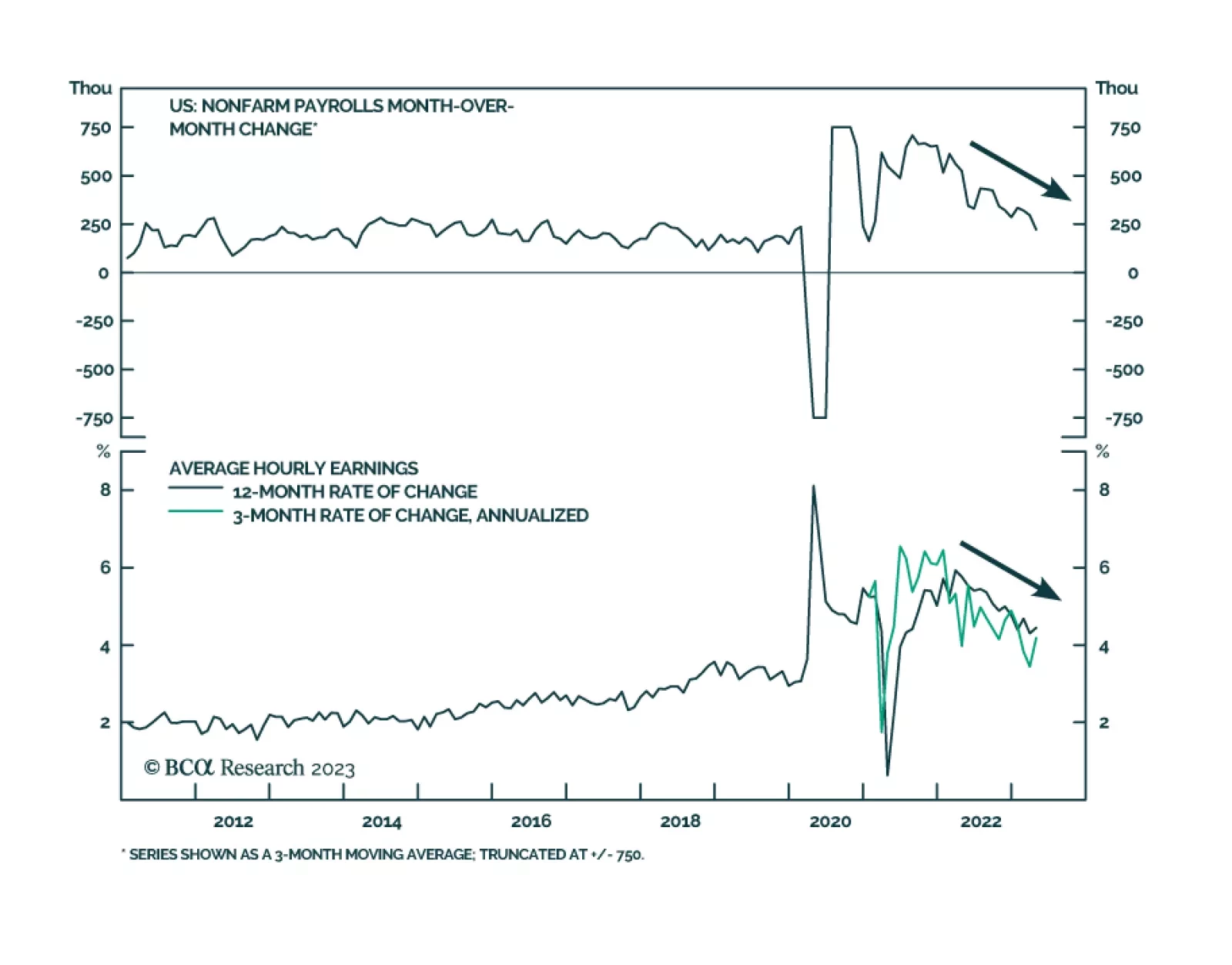

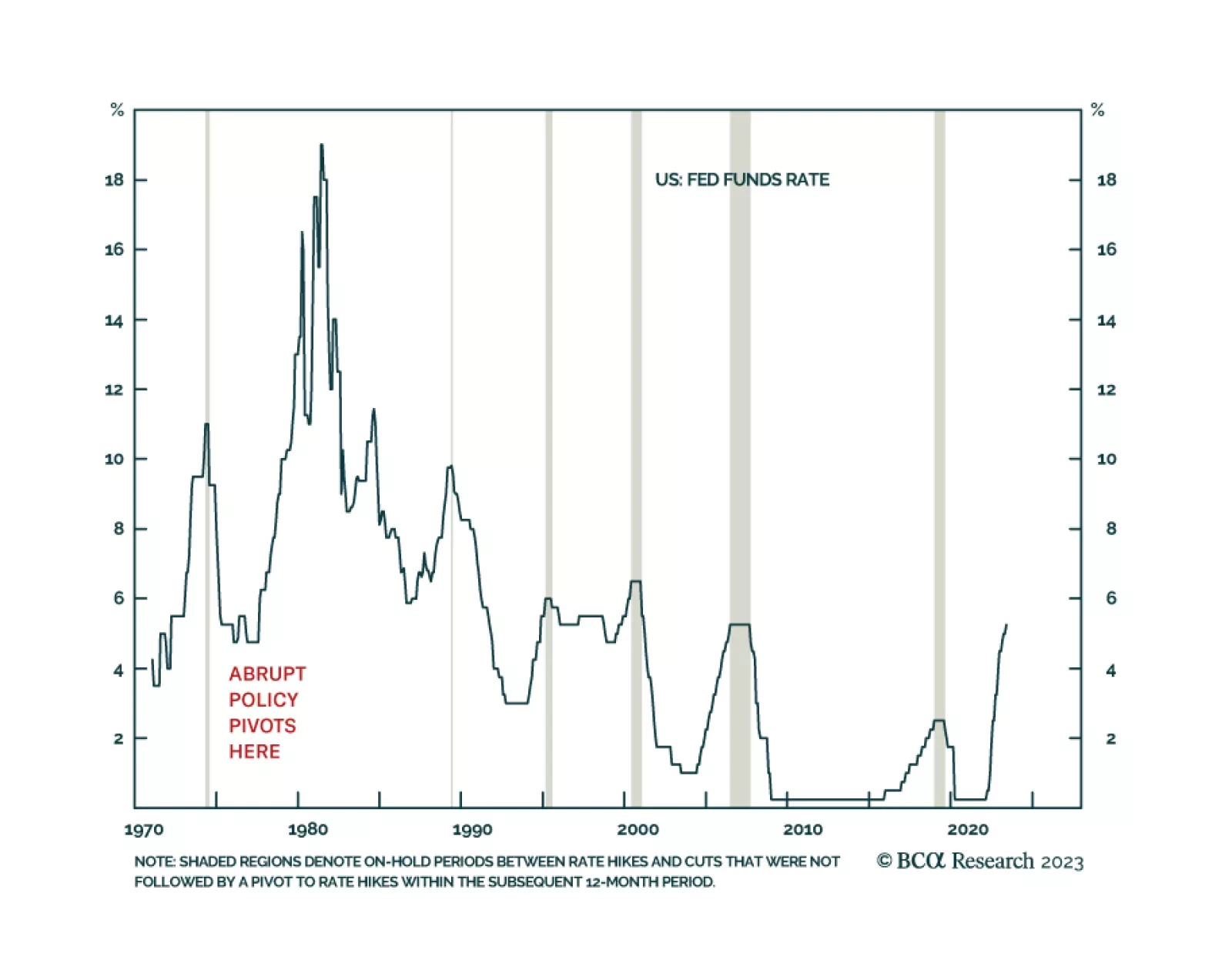

The Fed hiked 25 basis points at yesterday’s FOMC meeting while also signaling that the tightening cycle is now on hold. We discuss the short-run and long-run implications for Treasury yields.