Developed Countries

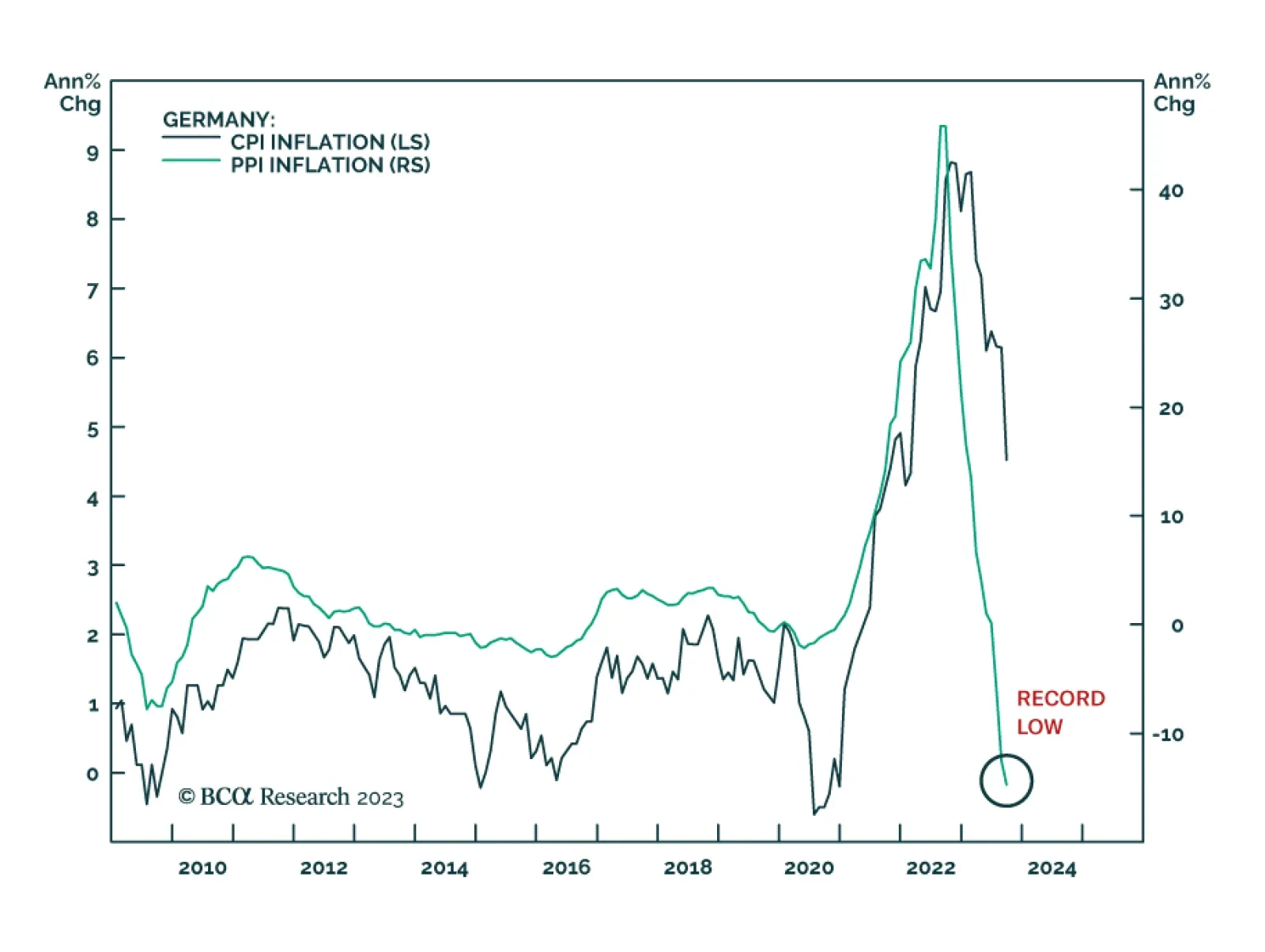

German producer prices declined by a new record 14.7% y/y in September, broadly in line with expectations of -14.1% y/y and a steeper pace of contraction than August's -12.6% y/y. Meanwhile, the monthly rate of change returned to contraction (-0.2% m/m)…

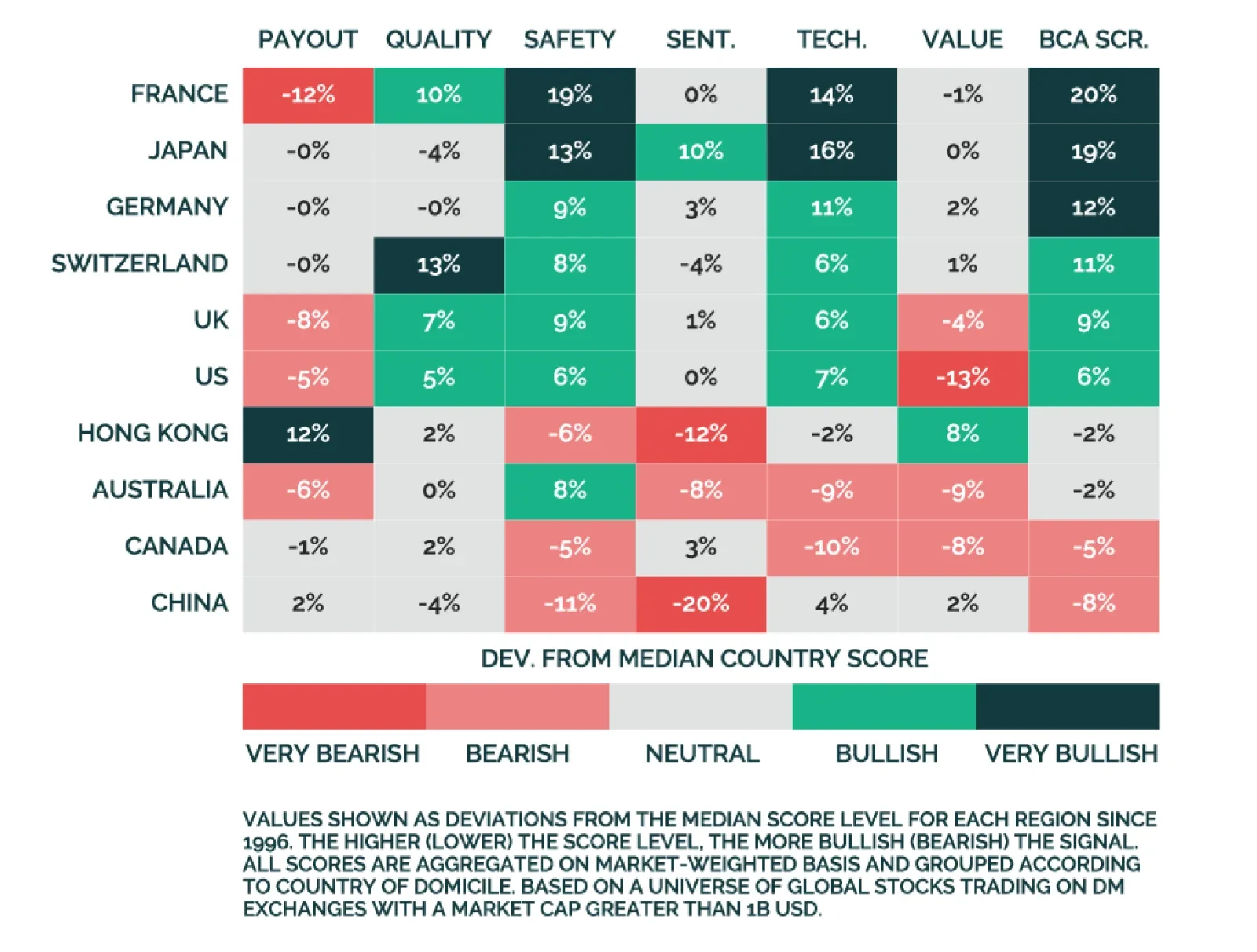

A powerful feature of the Equity Analyzer platform is its breadth of coverage: roughly 13 thousand stocks trading on MSCI Developed Market exchanges. Since we have a cross-section of the same stock level data across multiple regions, we can aggregate this…

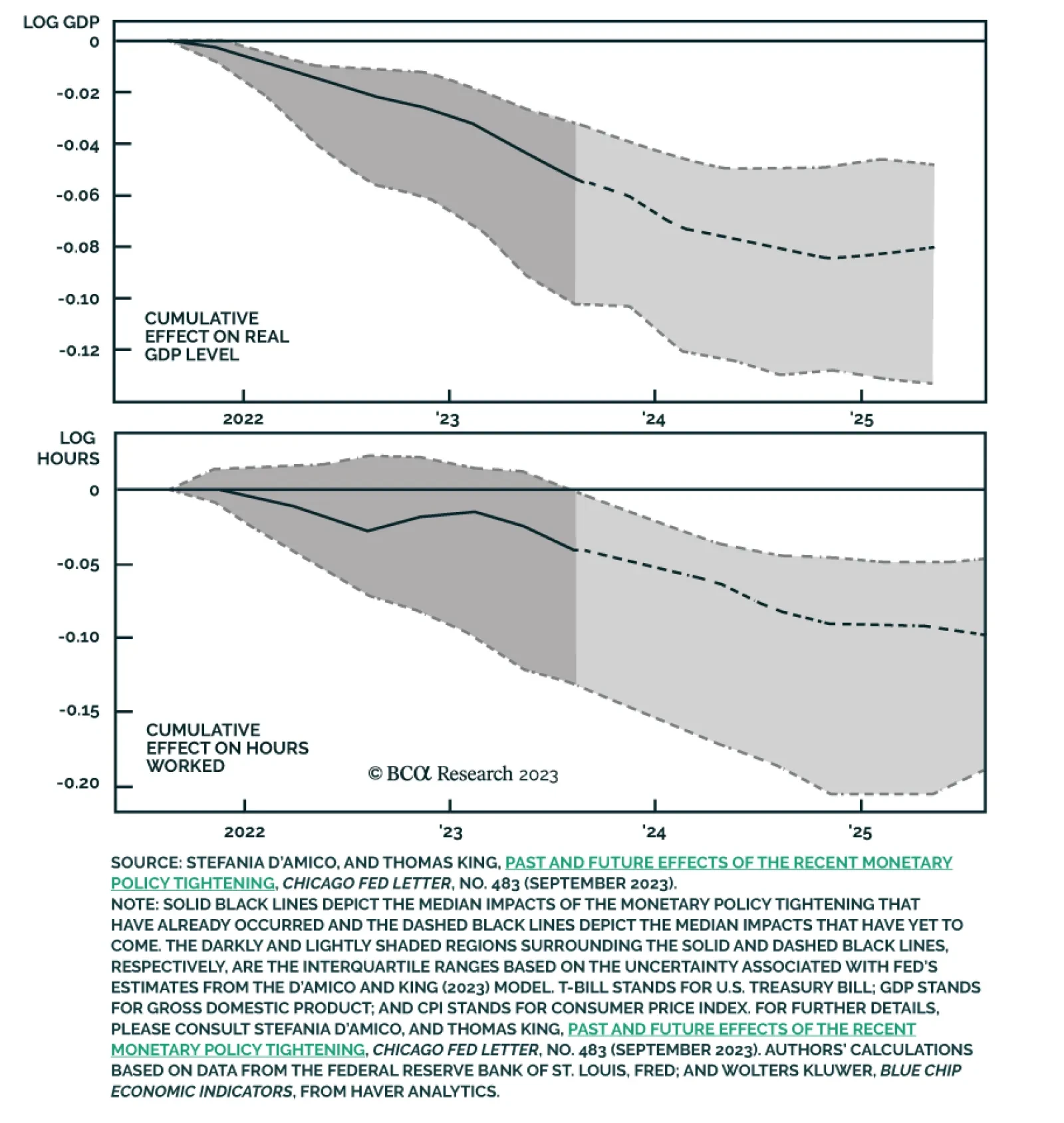

According to BCA Research's Global Investment Strategy service, the global economy will stay buoyant over the next few quarters but will then sour as the lagged effects of higher interest rates and tighter bank lending standards work their way through the…

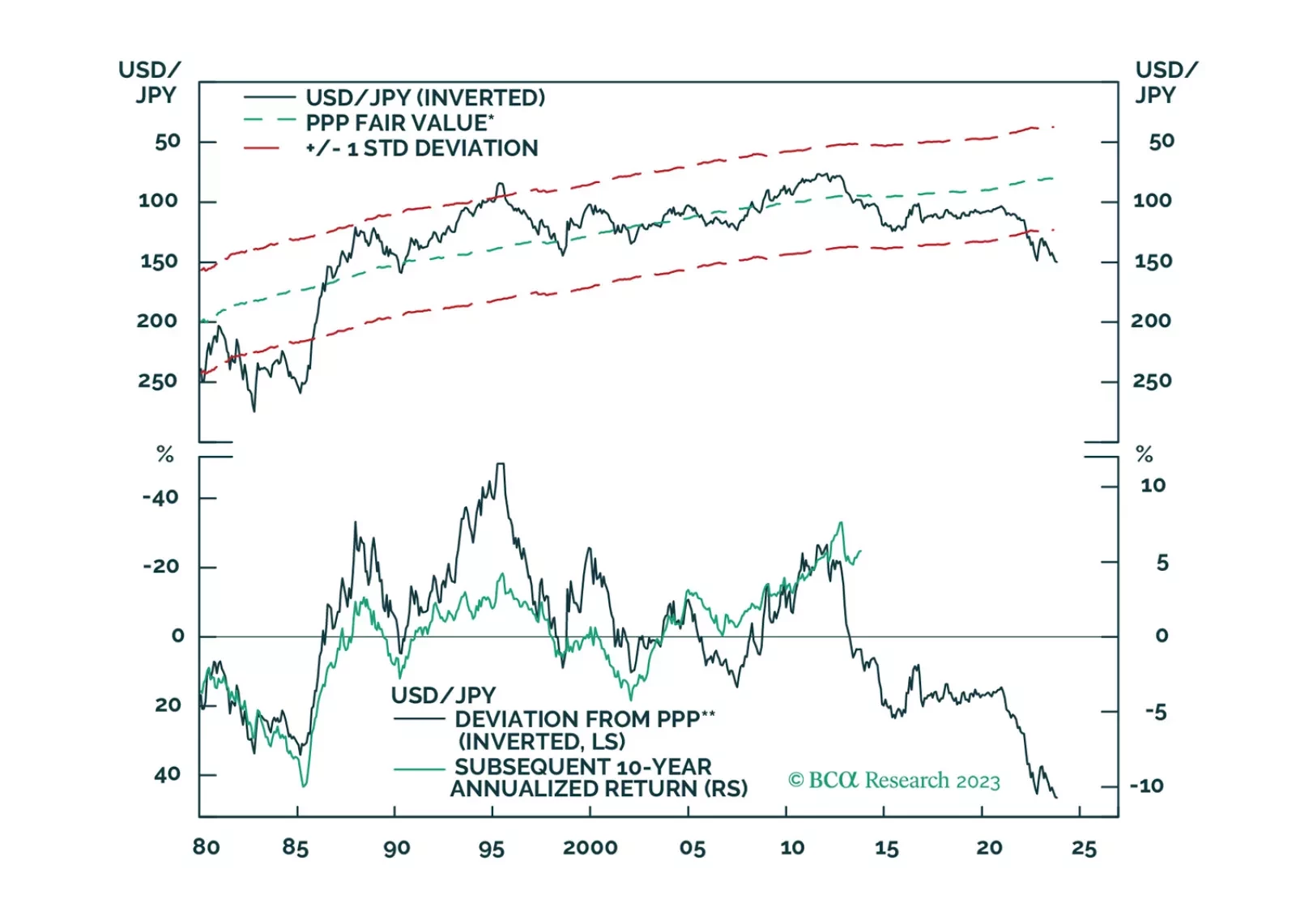

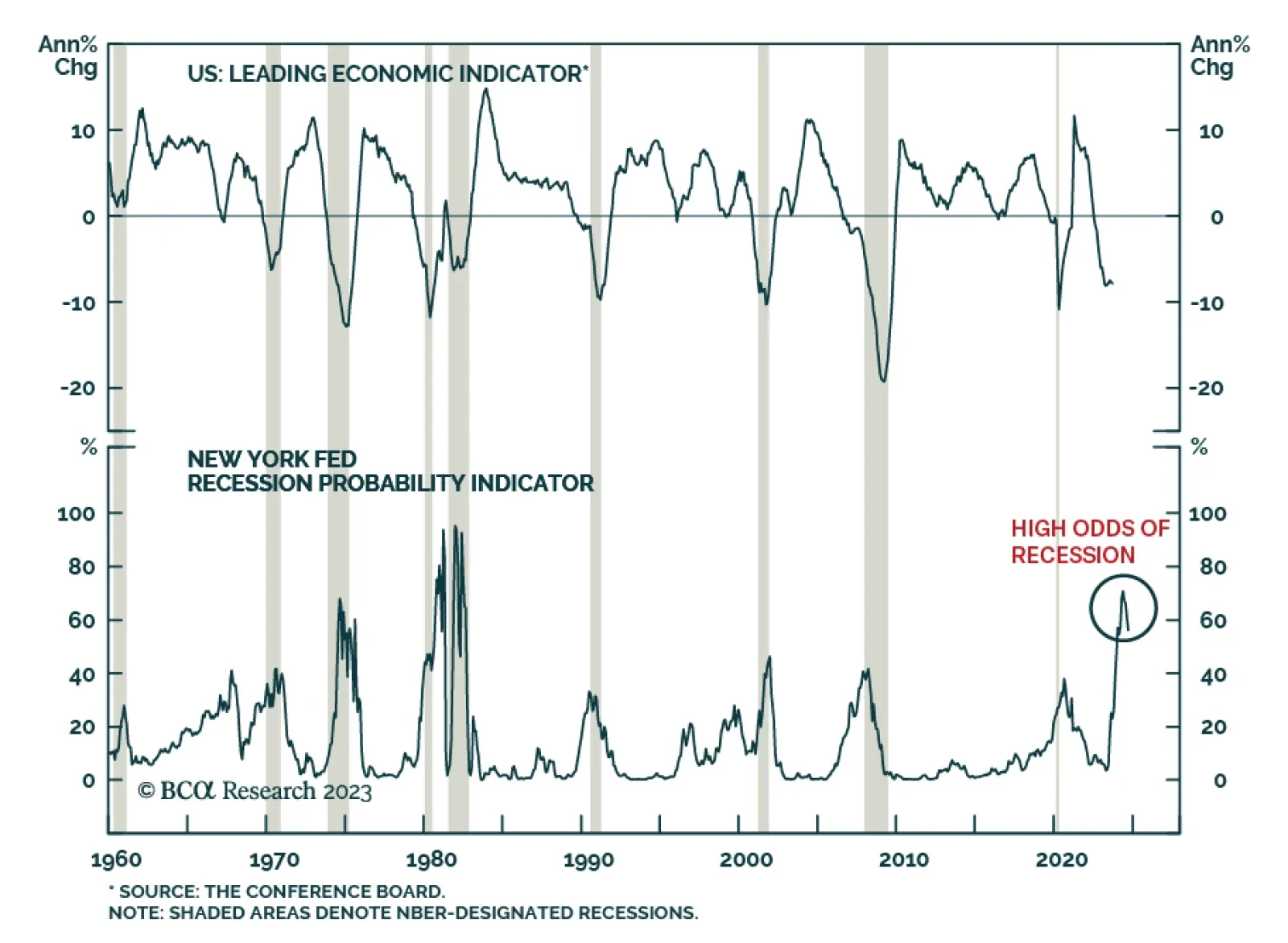

There is a high probability that the global economy will tip into recession in the second half of 2024. A long yen position is an excellent hedge against that risk.

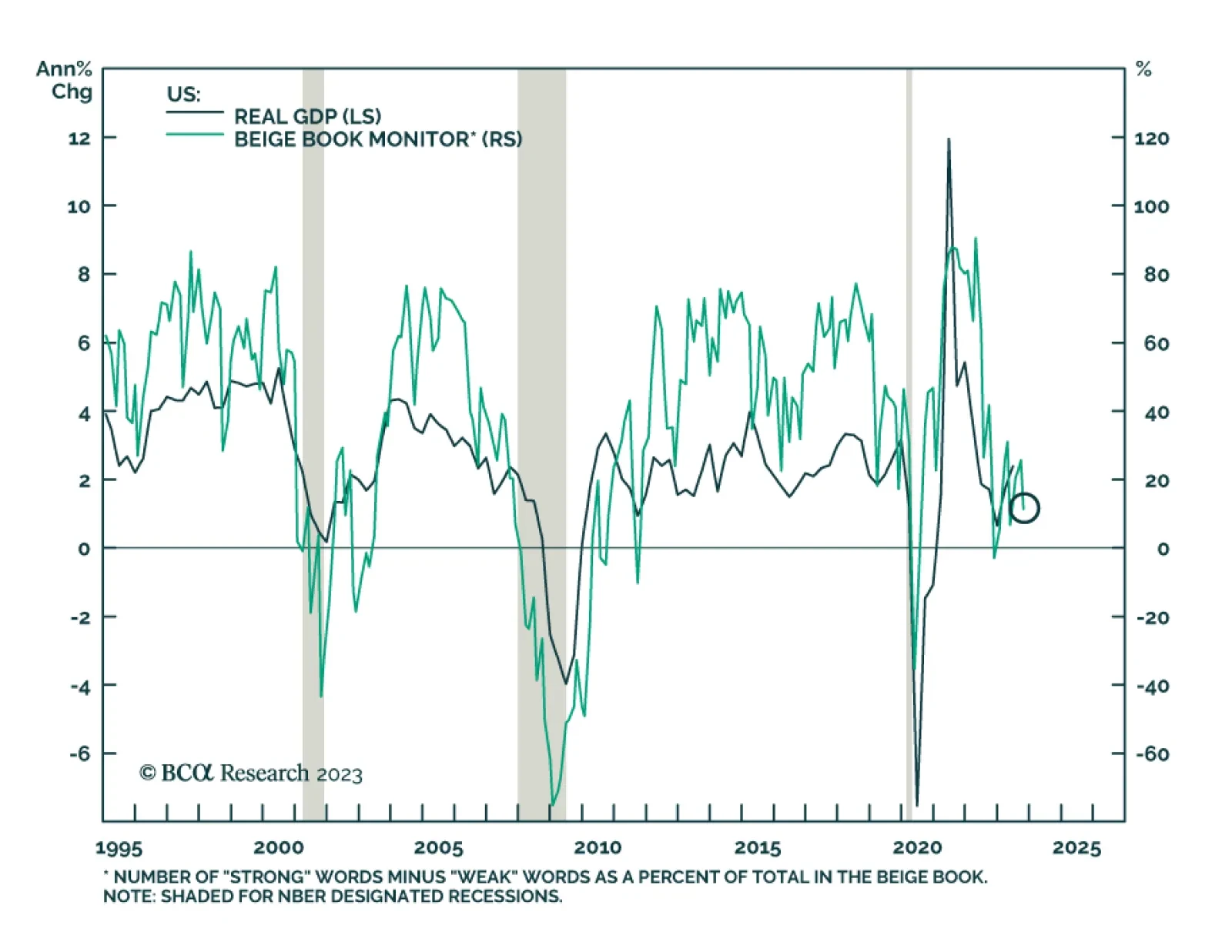

The Conference Board's Leading Economic Index's 0.7% m/m decline in September sent a weaker-than-anticipated signal about the outlook for the US economy. It fell below anticipations that the pace of decline would remain unchanged at -0.4% m/m and marks the…

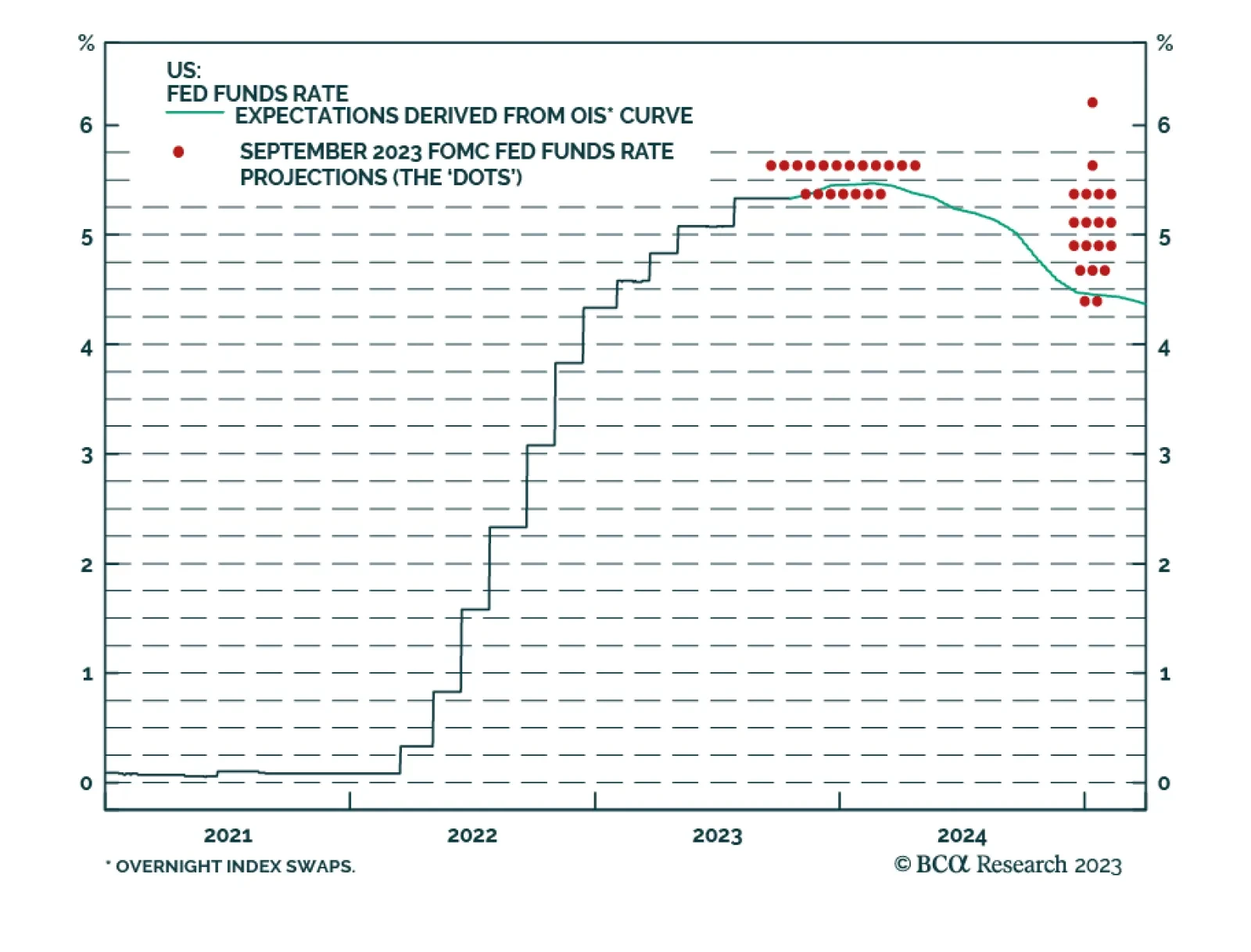

Fed Chair Jay Powell's speech at the Economic Club of New York on Thursday corroborates the signal from other recent Fedspeak that policymakers may not need to hike rates again. He highlighted that although inflation is still too high, price pressures are…

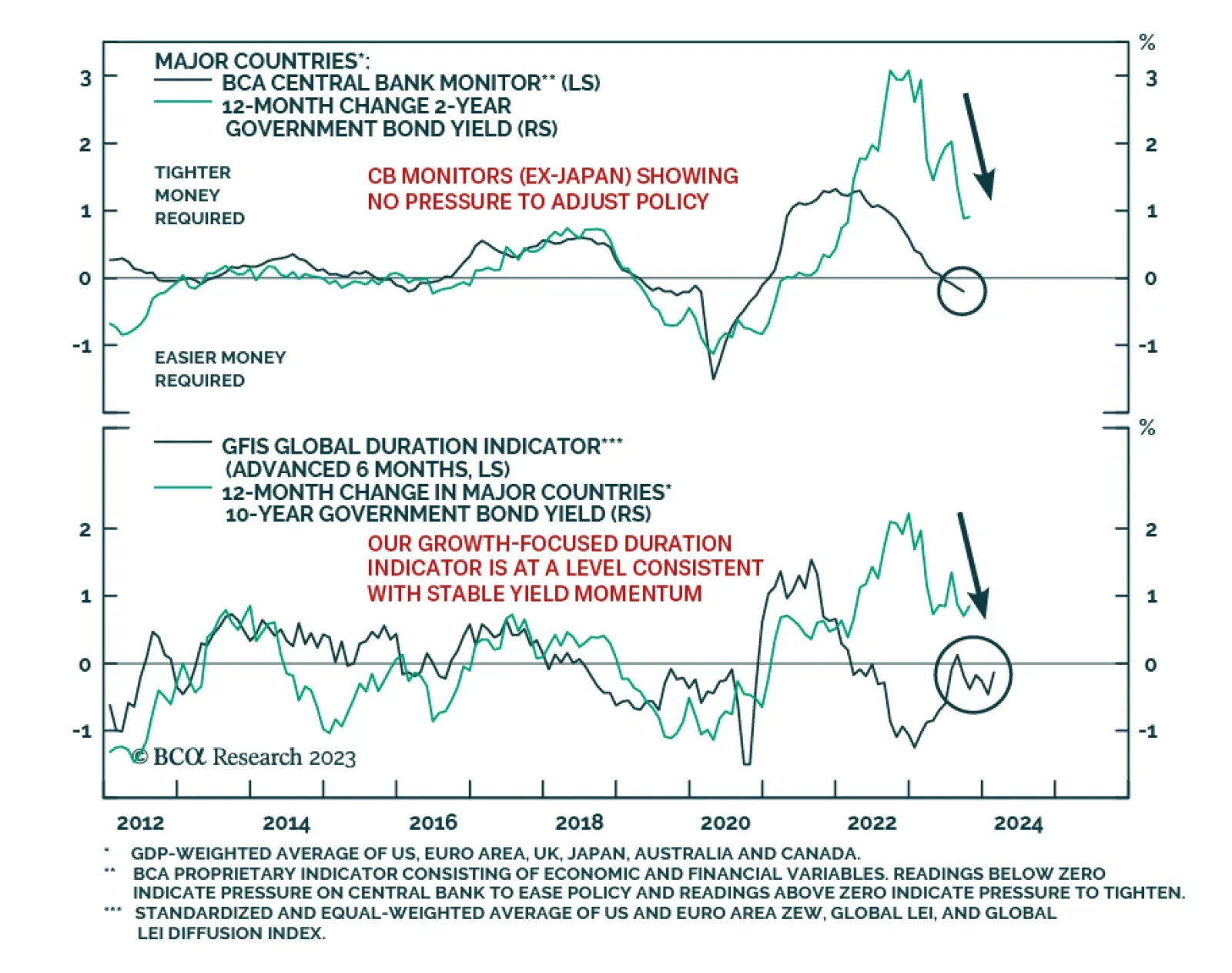

BCA Research’s Global Fixed Income Strategy service is maintaining a tactical neutral duration stance to begin Q4. The team believes the risk/reward on US Treasuries has improved substantially after latest backup in yields, with the market now discounting…

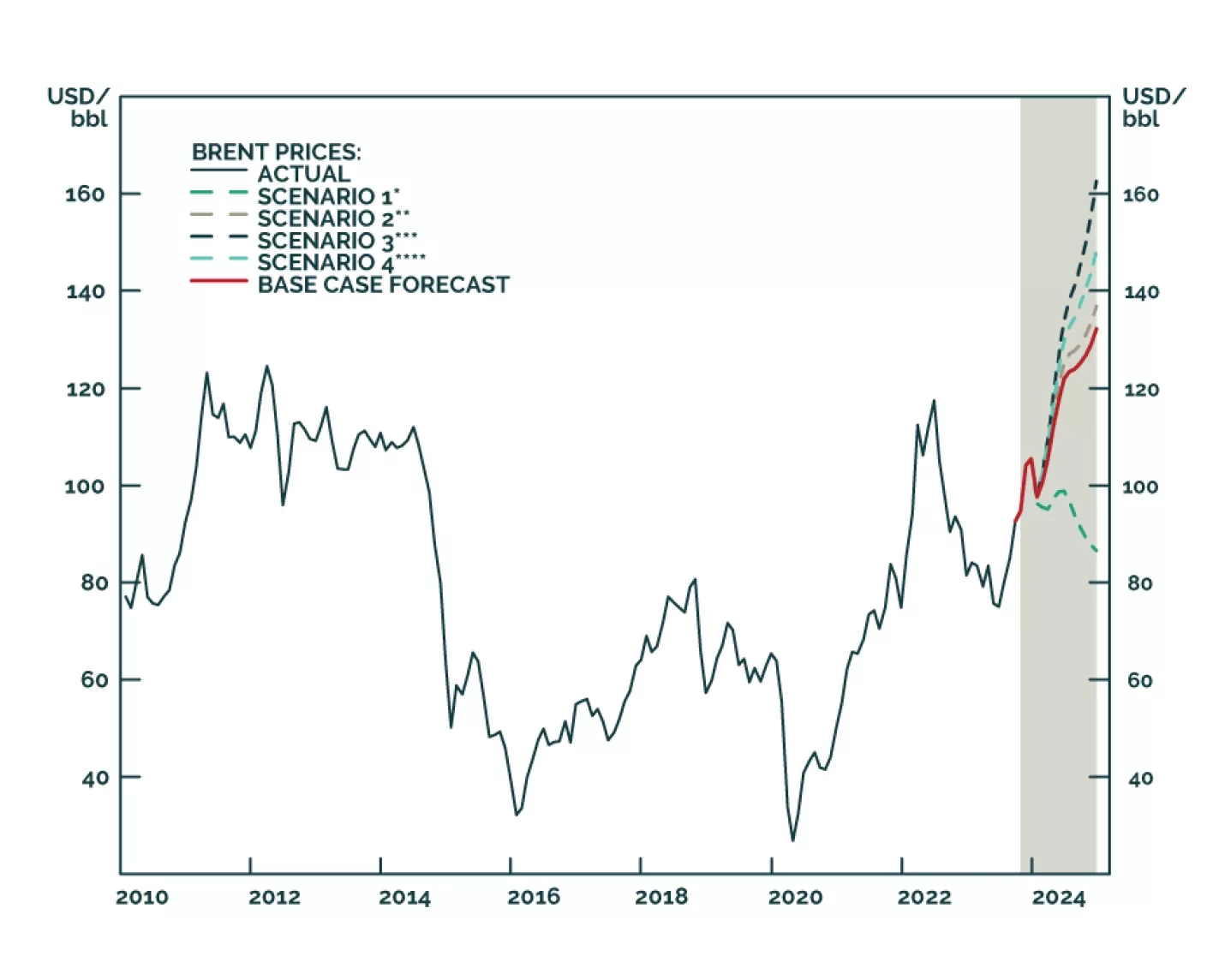

Despite higher uncertainty, our Brent price forecasts remain unchanged at just over $101/bbl for 4Q23 and $118/bbl for next year. We remain long equity exposure to oil and gas producers via the XOP ETF, and commodity exposure via the COMT ETF. We also remain long $100 Dec24 Brent calls and long 1Q24 Brent futures vs. short 1Q25 Brent futures in anticipation of stronger backwardation.

Stronger-than-anticipated retail sales and nonfarm payroll employment in September indicate that conditions are still favorable for US consumers. Similarly, the latest reading from the Atlanta Fed's GDPNow model stands at 5.4% for Q3 – well above estimates of…

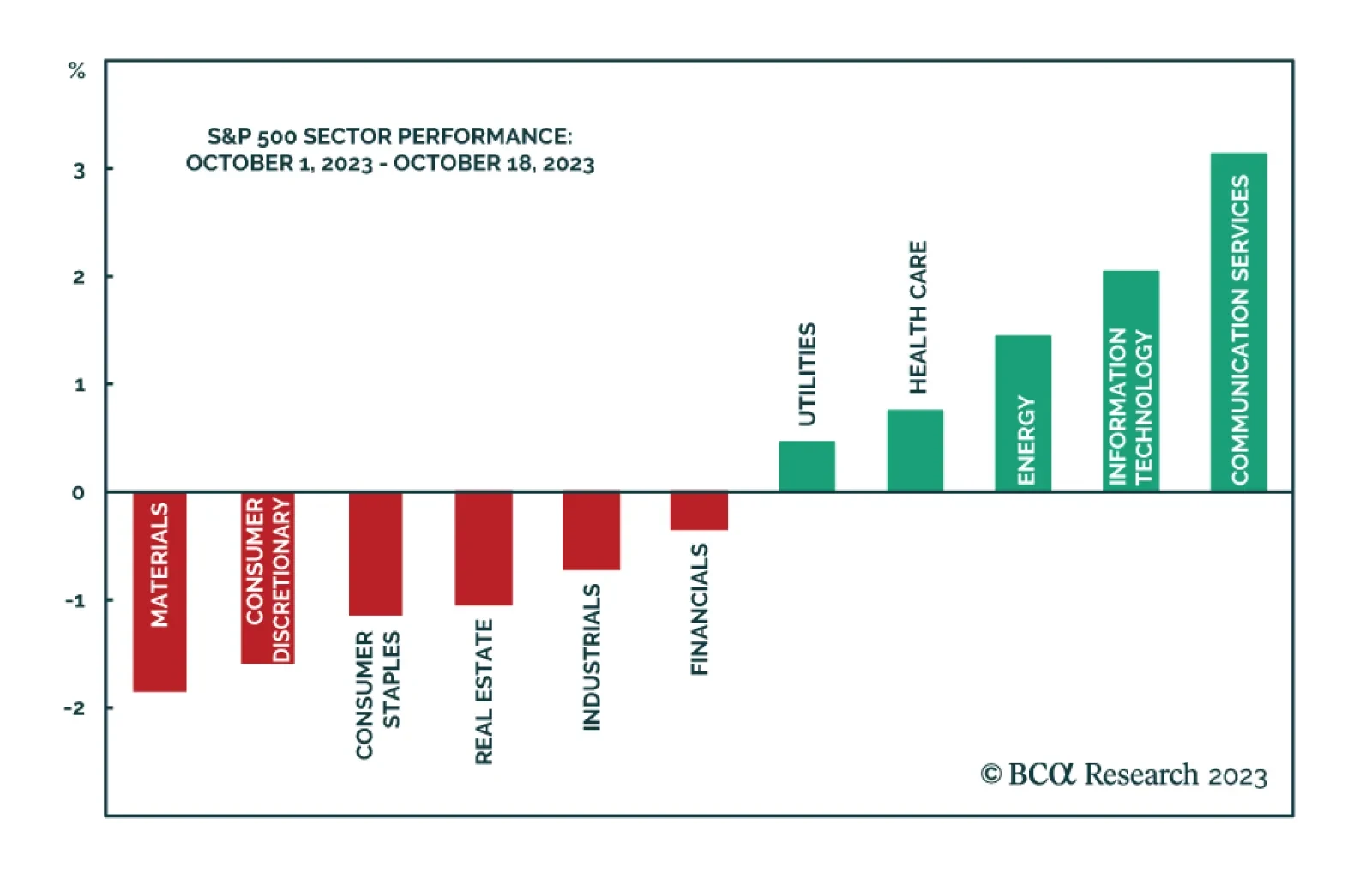

S&P 500: A Look Under The Hood

…