Developed Countries

Our reaction to today’s FOMC meeting and the Treasury’s Quarterly Refunding Announcement.

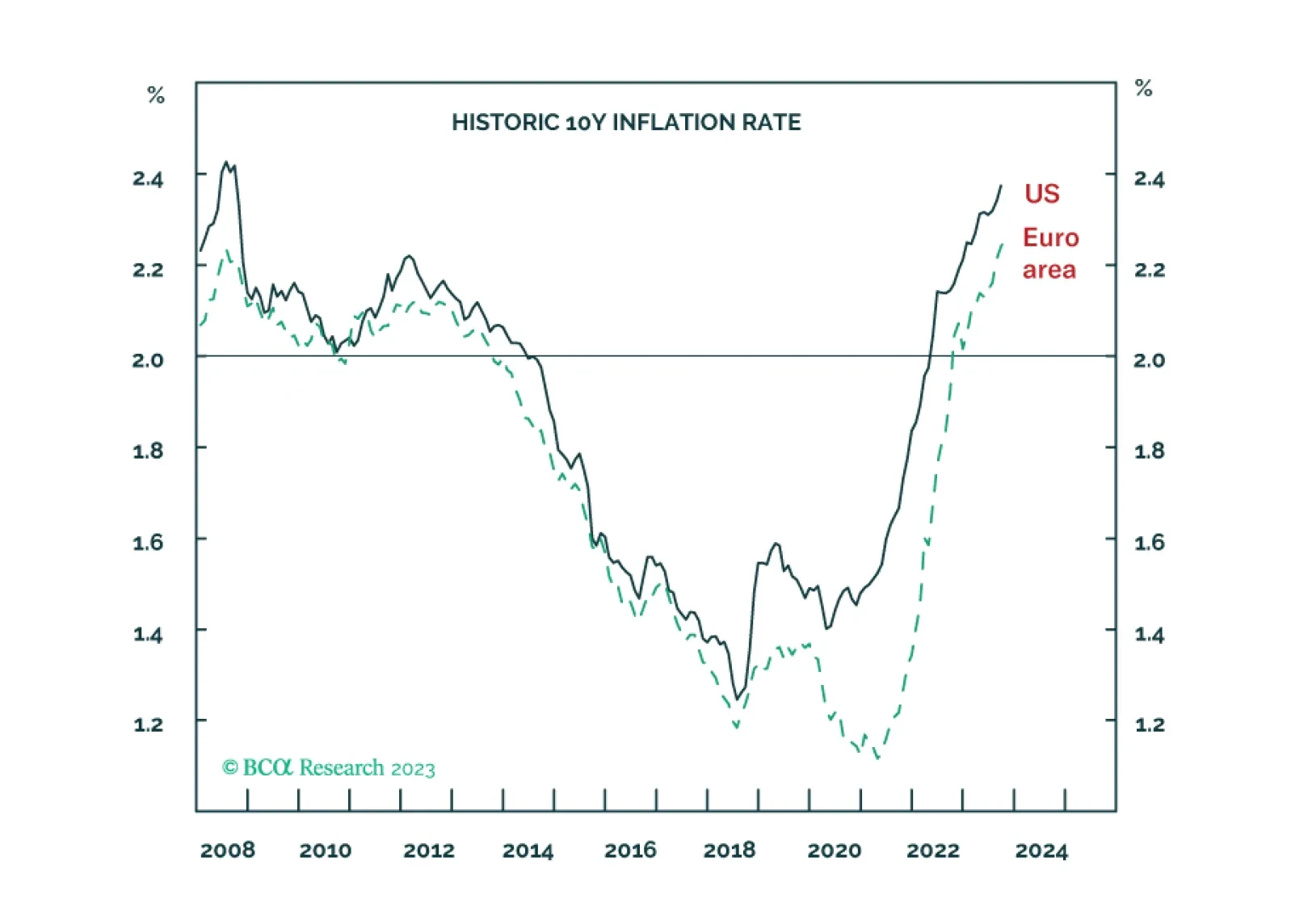

The fundamental component of long-term inflation expectations has climbed to its highest level since 2008 in both the US and the euro area. This means that both the Fed and the ECB will need to engineer inflation to undershoot 2 percent for an extended period if they are to maintain their 2 percent inflation targets. We explain what this means for investment strategy over the coming 6-12 months. Plus, we pinpoint what to focus on in this Friday’s US jobs report. And we identify food and beverages (PBJ) and the Indonesian rupiah (IDR/USD) as excellent rebound candidates.

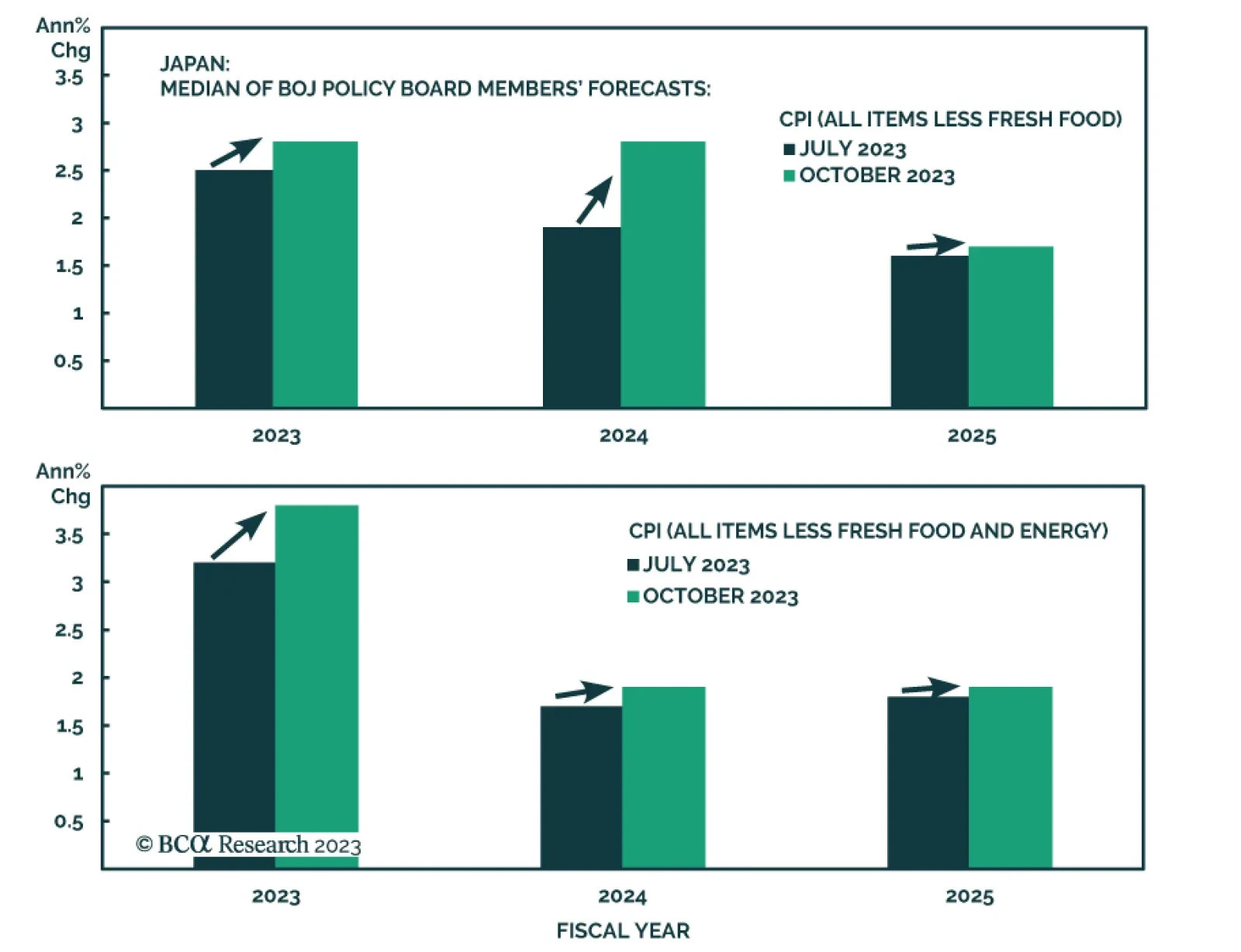

The Bank of Japan adjusted the language of its Monetary Policy Statement on Tuesday to indicate that it will allow greater flexibility it its yield curve control policy (YCC). It indicated that although the target level of 10-year JGB yields remains unchanged…

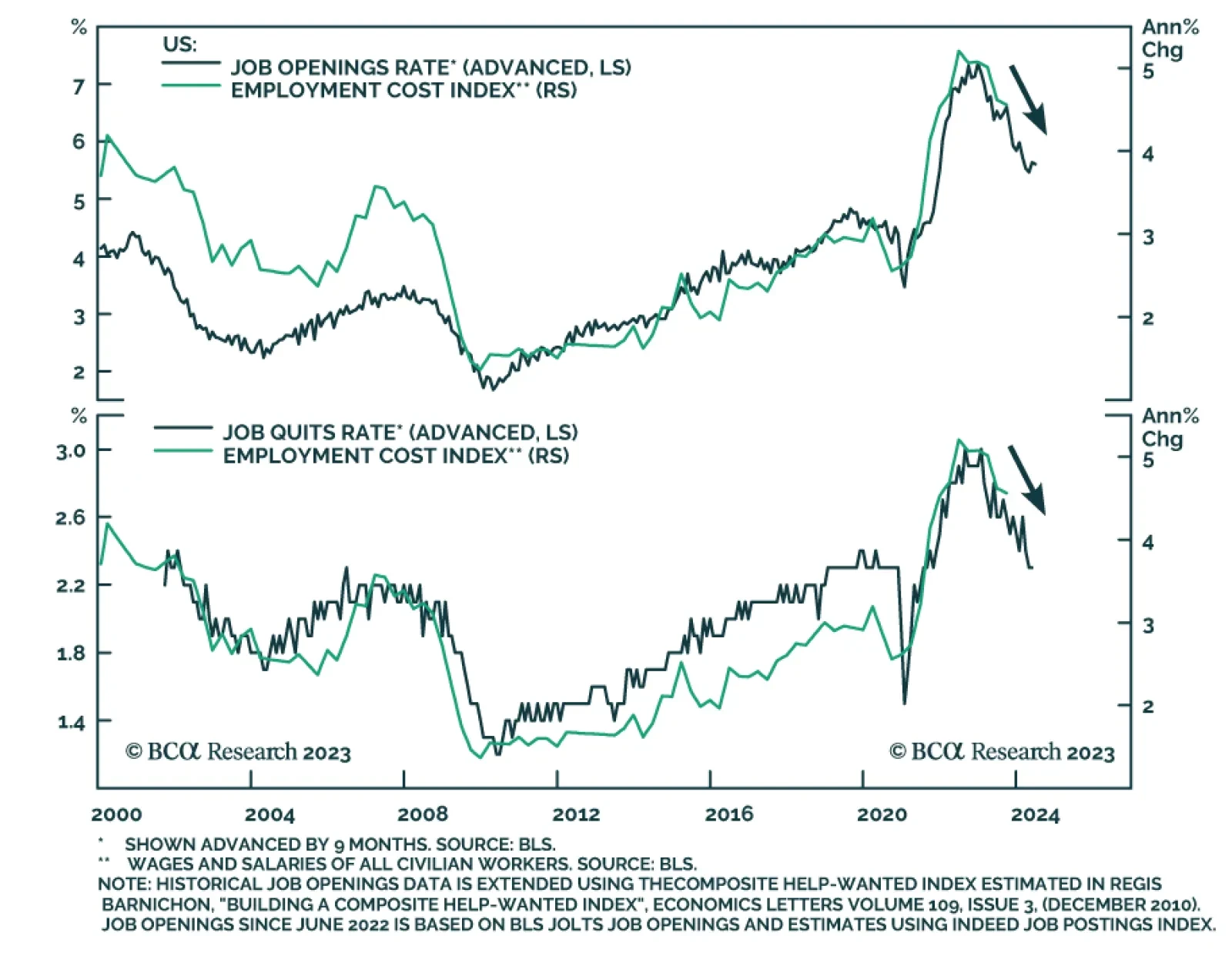

The US Employment Cost Index (ECI) unexpectedly accelerated in Q3, rising by 1.1% q/q versus anticipations the pace of increase would remain unchanged at 1.0% q/q. A pickup in wages and salaries drove the increase. On an annual basis, the ECI slowed from 4.5%…

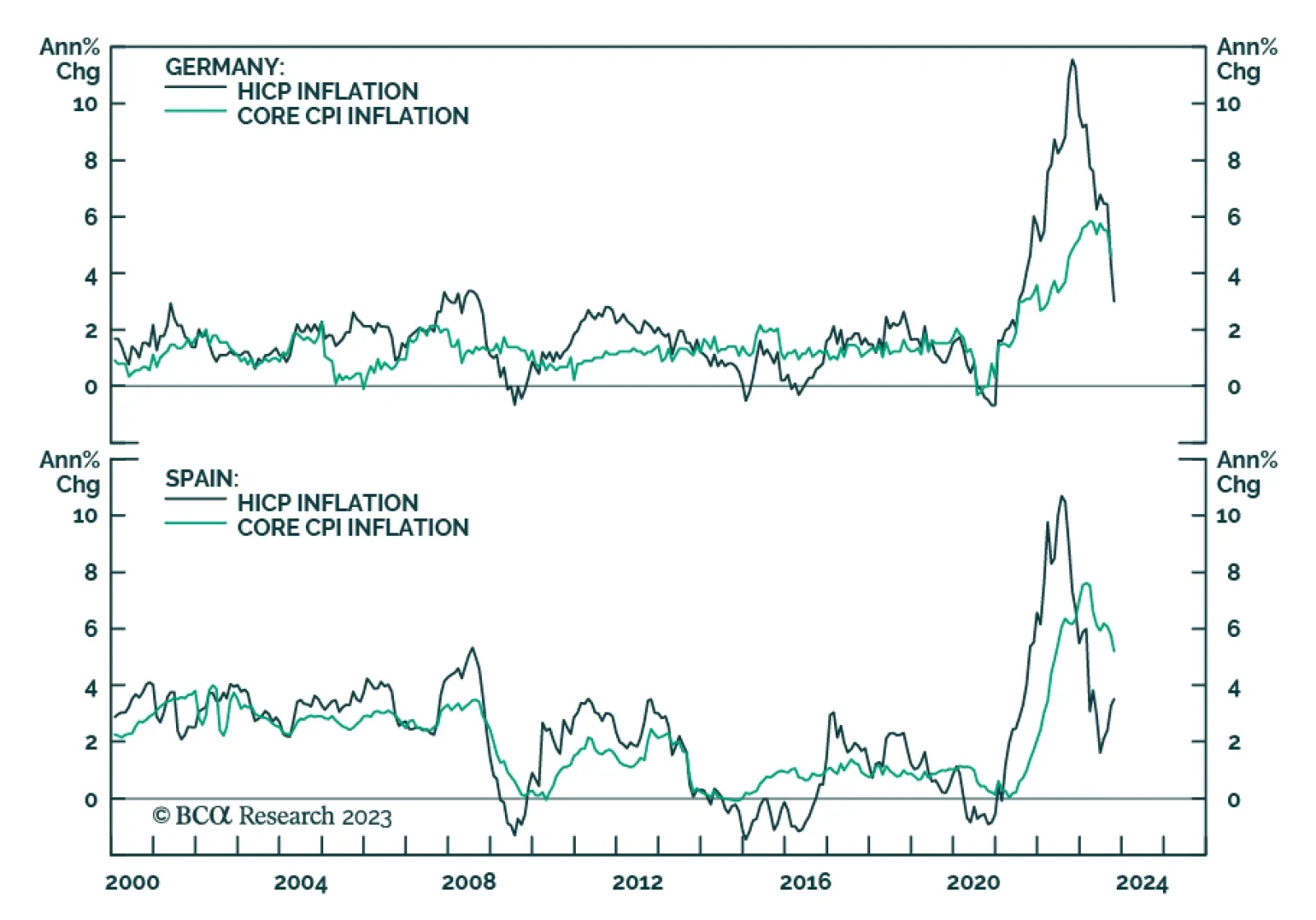

The Eurozone's October inflation release confirmed the signal from the German and Spanish reports that price pressures are moderating. CPI inflation softened from 4.3% y/y to 2.9% y/y (below expectations of 3.1% y/y) while the monthly rate of change eased to…

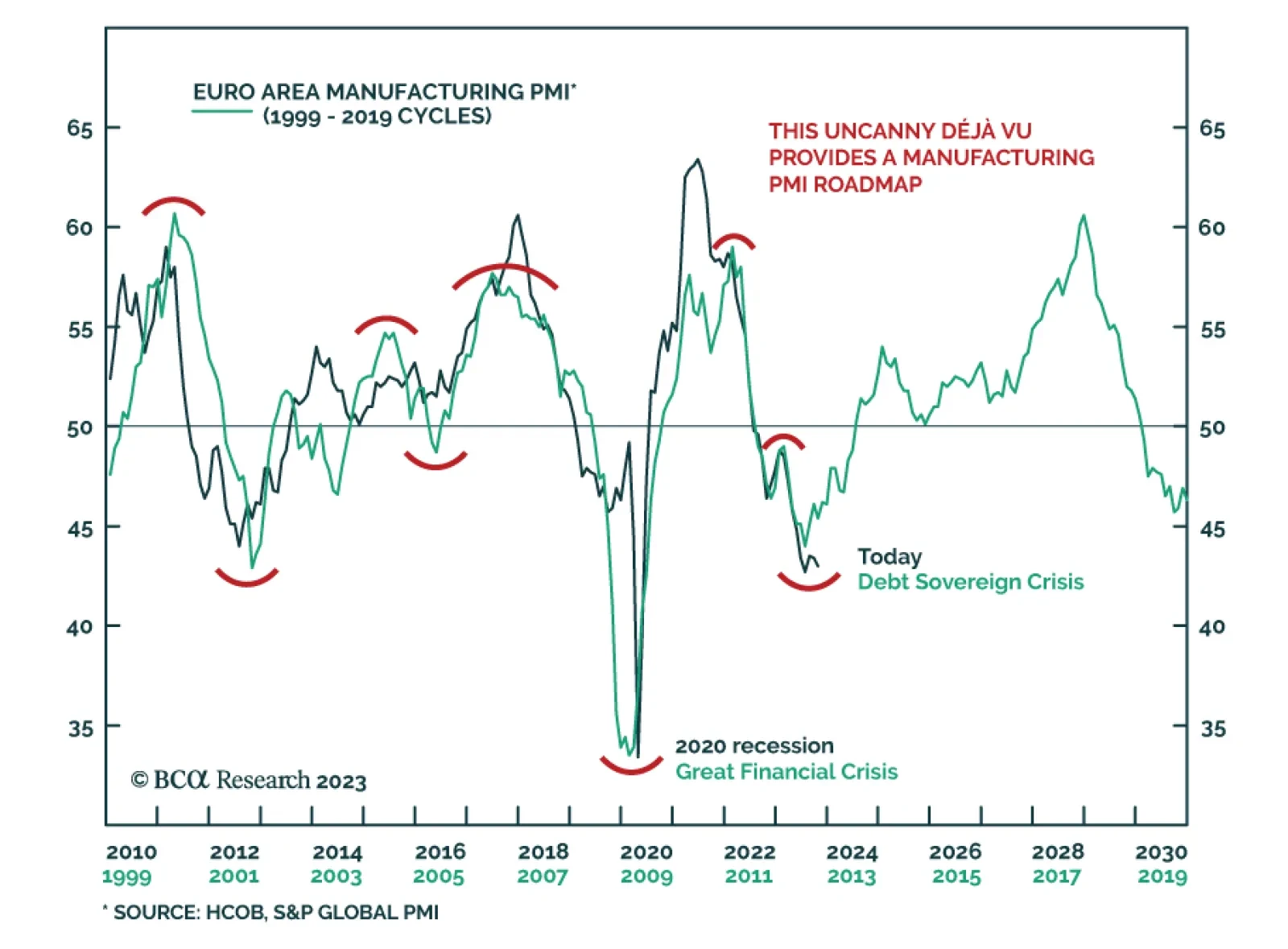

According to BCA Research’s European Investment Strategy service, 2012 provides a tentative roadmap of the next Eurozone manufacturing cycle. The resemblance between today and 2012 is uncanny. The overlap matches the current cycle down to a couple of…

Eurozone economic data sent a positive signal on Monday. Preliminary CPI releases from Germany and Spain show price pressures continue to moderate. In Germany, the harmonized index declined by 0.2% m/m while the annual rate of change eased from 4.3% y/y to…

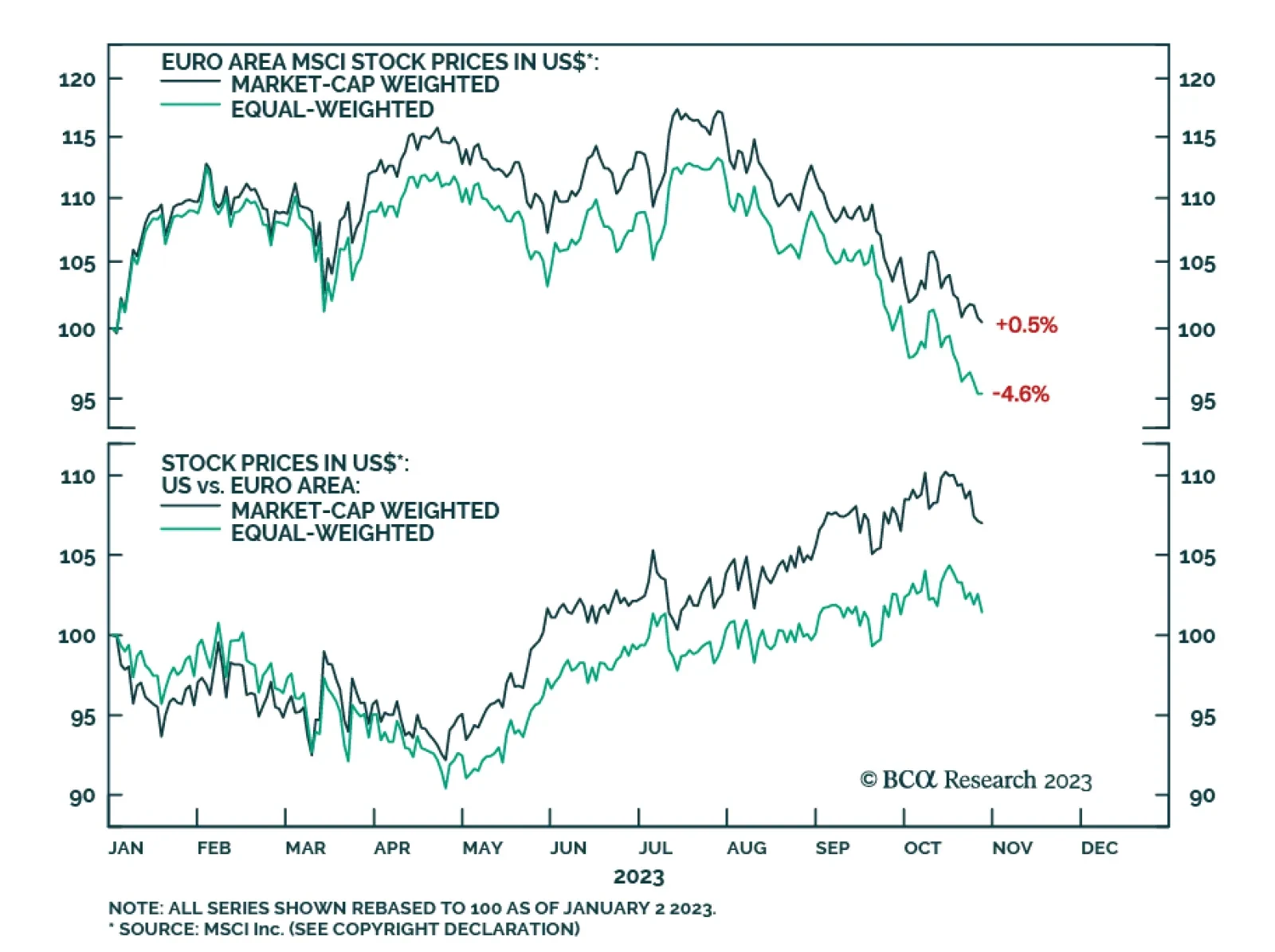

In a recent Insight we highlighted that the S&P 500's year-to-date rally is narrow in breadth and that the equal weighted index has erased all its year-to-date gains. This is also true in the case of the Euro Area where the MSCI price index is still up by…

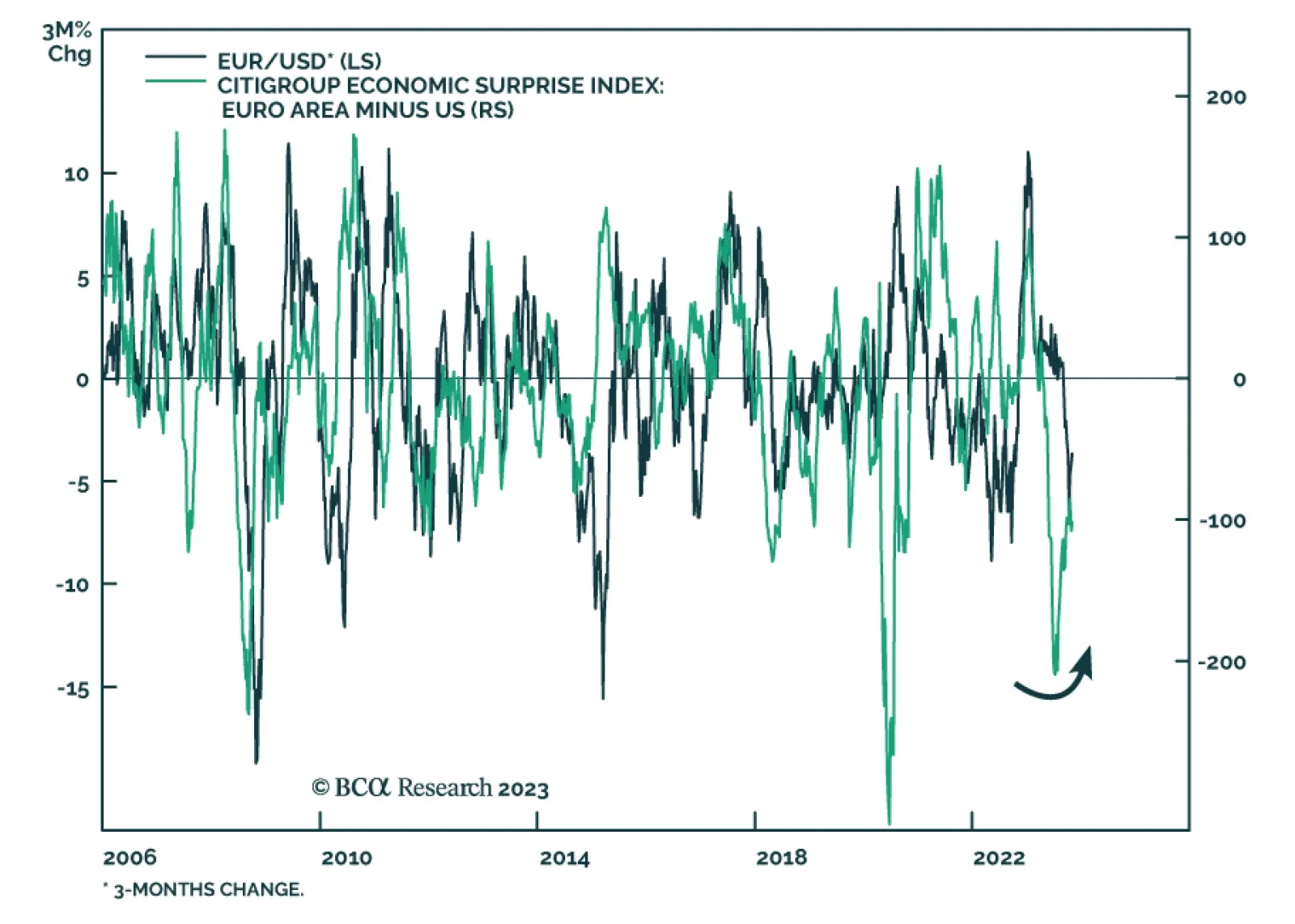

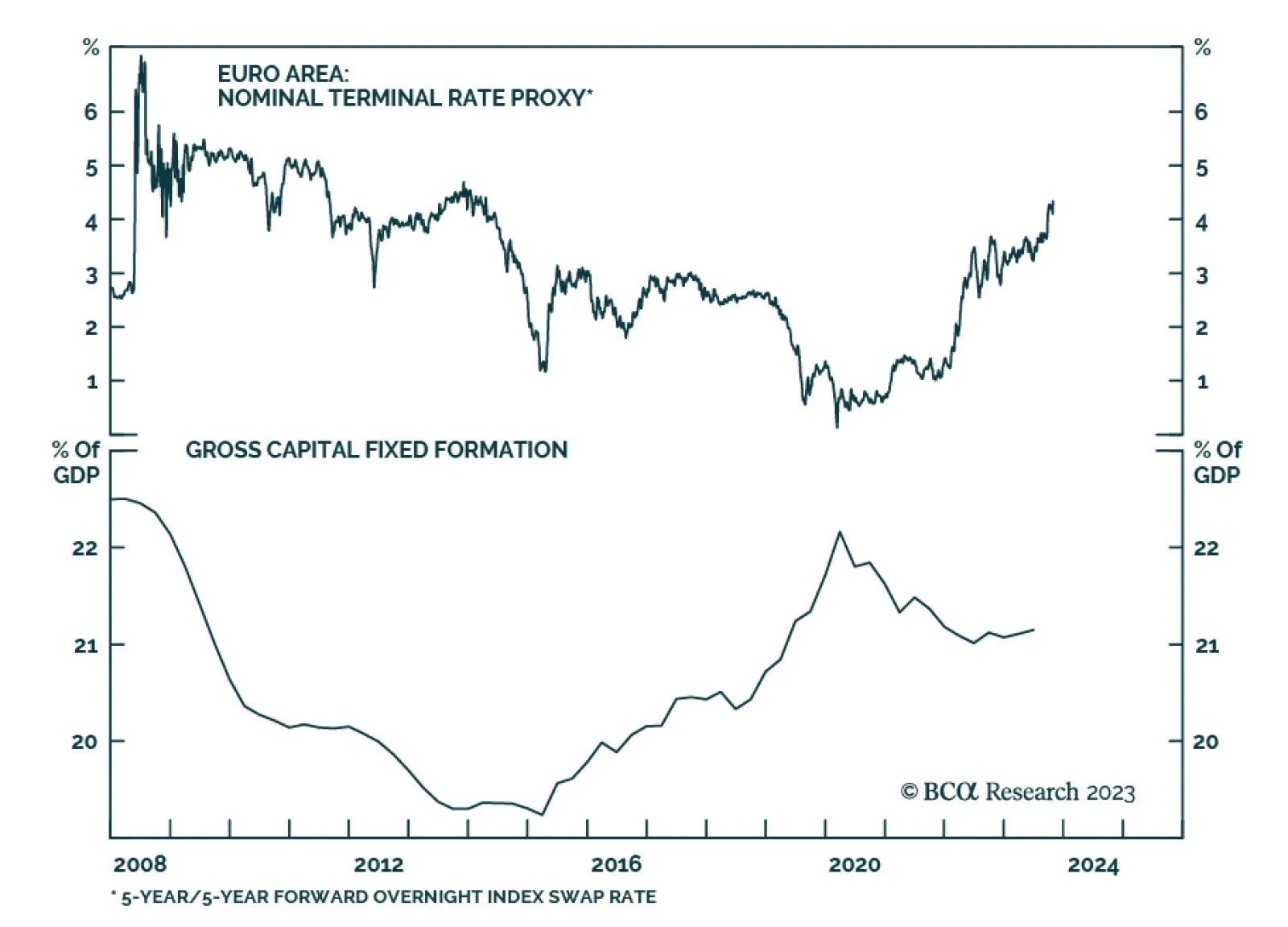

The European money market curve anticipates three rate cuts by October 2024. This pricing is appropriate considering the outlook for European growth next year. BCA’s Europe strategist expect a recession in the second half of the year, which will force the ECB…

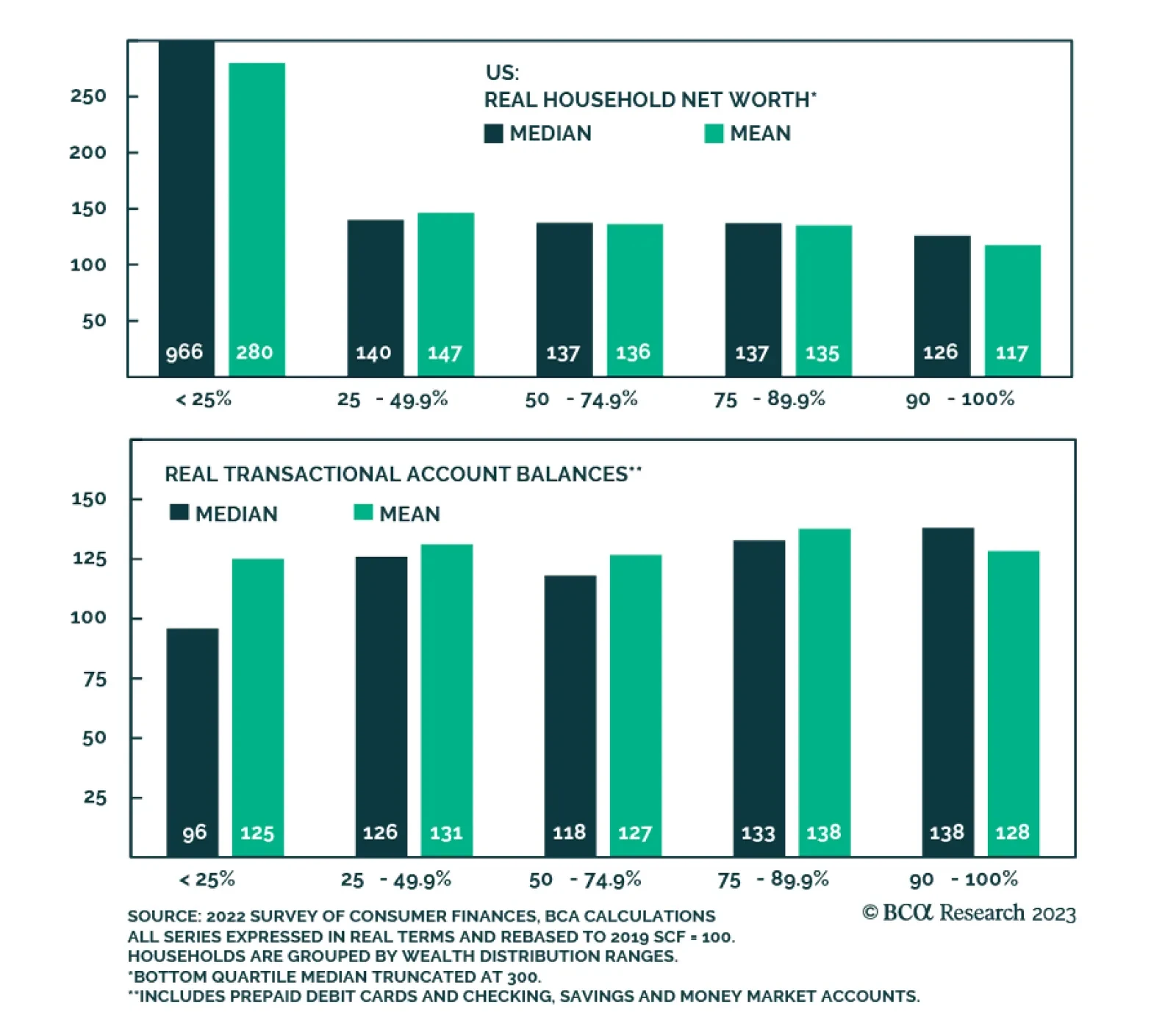

The Fed’s latest triennial Survey of Consumer Finances (SCF), spanning the period from 2019 to 2022, was released on October 18th. It augments the Distributional Financial Accounts' (DFA) depiction of the distribution of household wealth and income. According…