Developed Countries

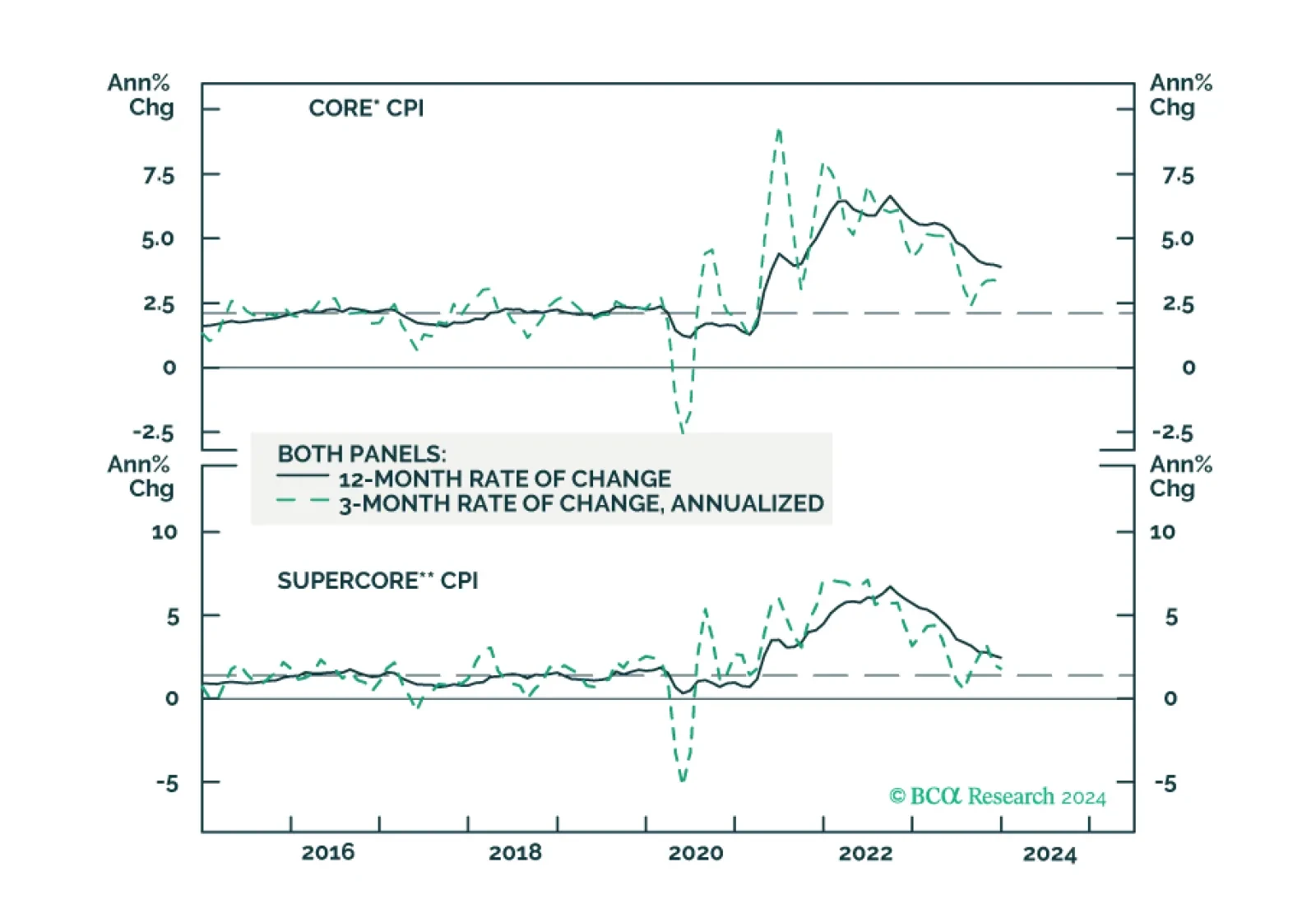

We update our inflation forecast following this morning’s CPI report.

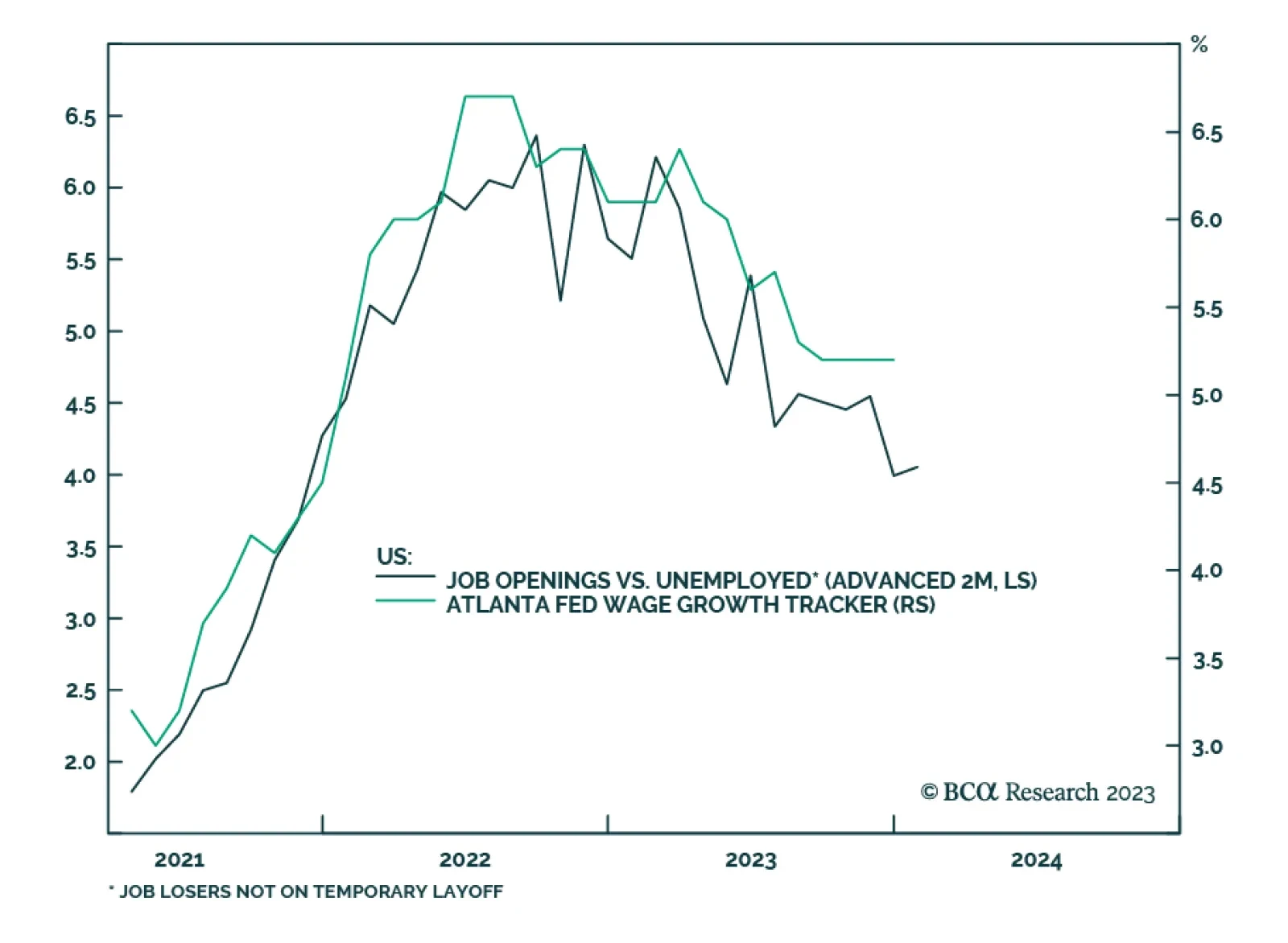

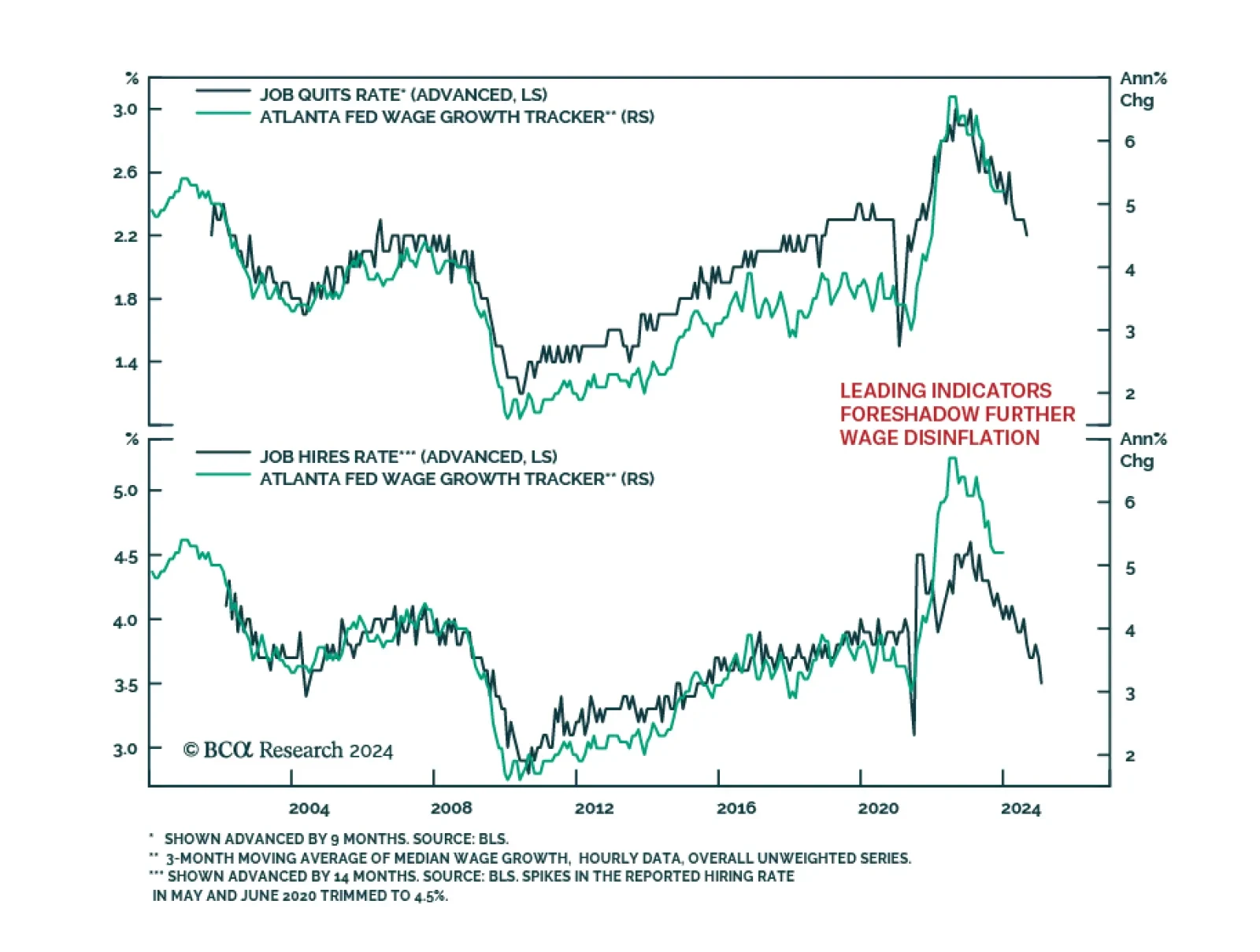

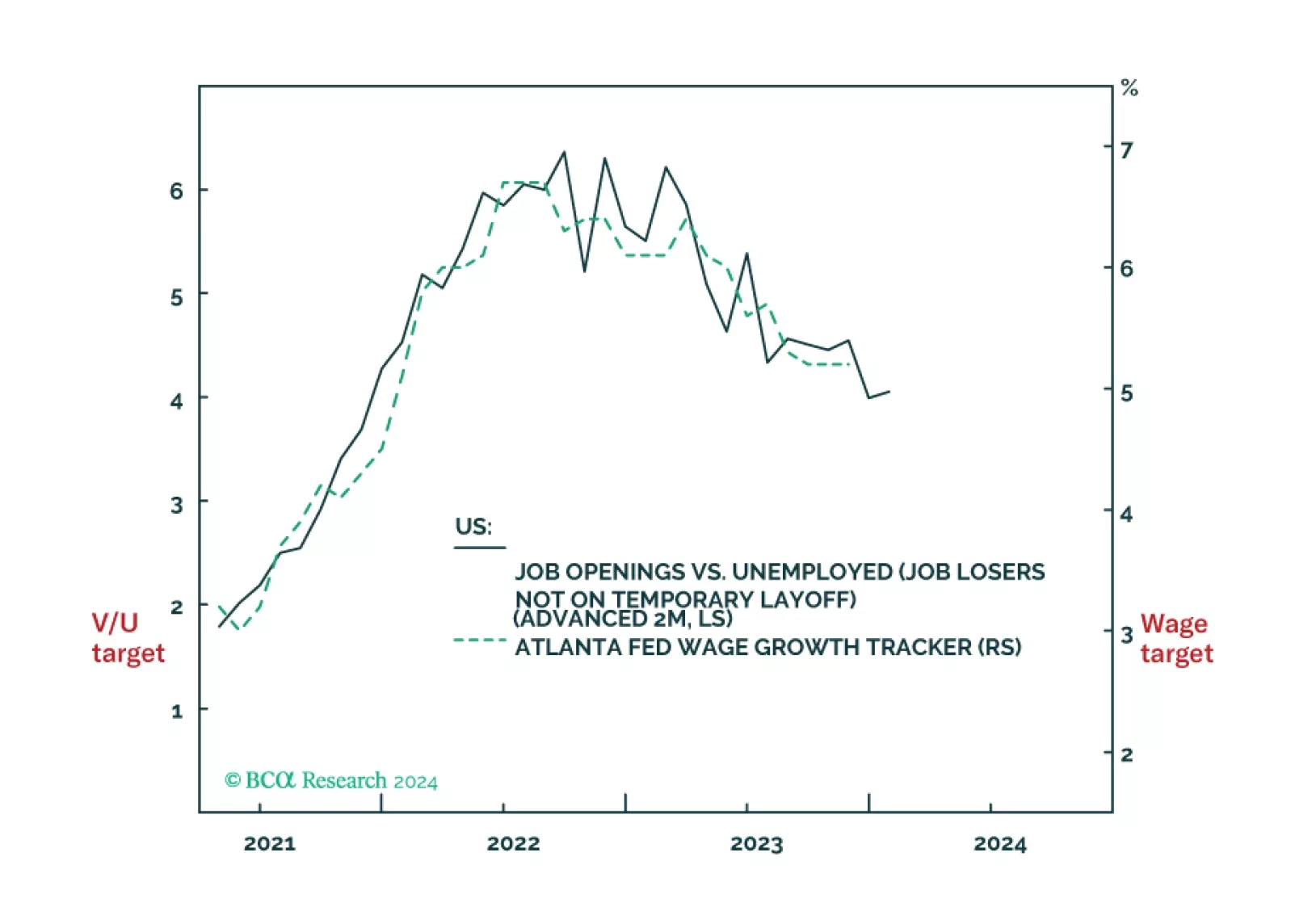

The Fed faces a dilemma. Cut rates early to avoid a recession, but at the risk of not slaying wage inflation. Or, not cut rates early to ensure that wage inflation is slayed, but at the risk of a downturn. Faced with such a dilemma, the lesser evil is to slay wage inflation even at the risk of a downturn. Meaning that the market has overpriced early rate cuts. We discuss some other investment implications, and identify two rebound candidates.

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.