Developed Countries

The message from the latest Beige Book release is confirming that US demand is showing signs of slowing down. Of the 12 Federal Reserve districts, 2 reported modest economic growth, 8 reported economic activity was slightly up, and 2 indicated flat economic…

The Conference Board’s measure of consumer confidence surprised to the upside on Tuesday. The headline index improved to 102 from 97.5, upending expectations of a continued moderation to 96. The rebound follows 3 consecutive months of decline. The…

Recent US housing market data has been uninspiring. The FHFA house price index decelerated in March from 1.2% m/m to 0.1% m/m, disappointing expectations of 0.5% m/m, and the S&P CoreLogic 20-City index growth rate declined from 0.55% m/m to…

At BCA Research, fundamentals drive our analysis and we use indicators and quantitative metrics as guides to inform our views further. It is our fundamental assessment of the US labor market that underpins our view that softer labor demand and decelerating…

Our Global Investment strategists highlighted back in November 2022 that structural deflationary forces in Japan were weakening, thus setting the stage for inflation to make a historic comeback in Japan. About a year later, they highlighted that 2024…

According to BCA Research’s European Investment Strategy service, the money sloshing around the financial system from pandemic-era stimulus measures disconnects near-term prospects for growth from risk asset prices. As a result, we are witnessing an odd…

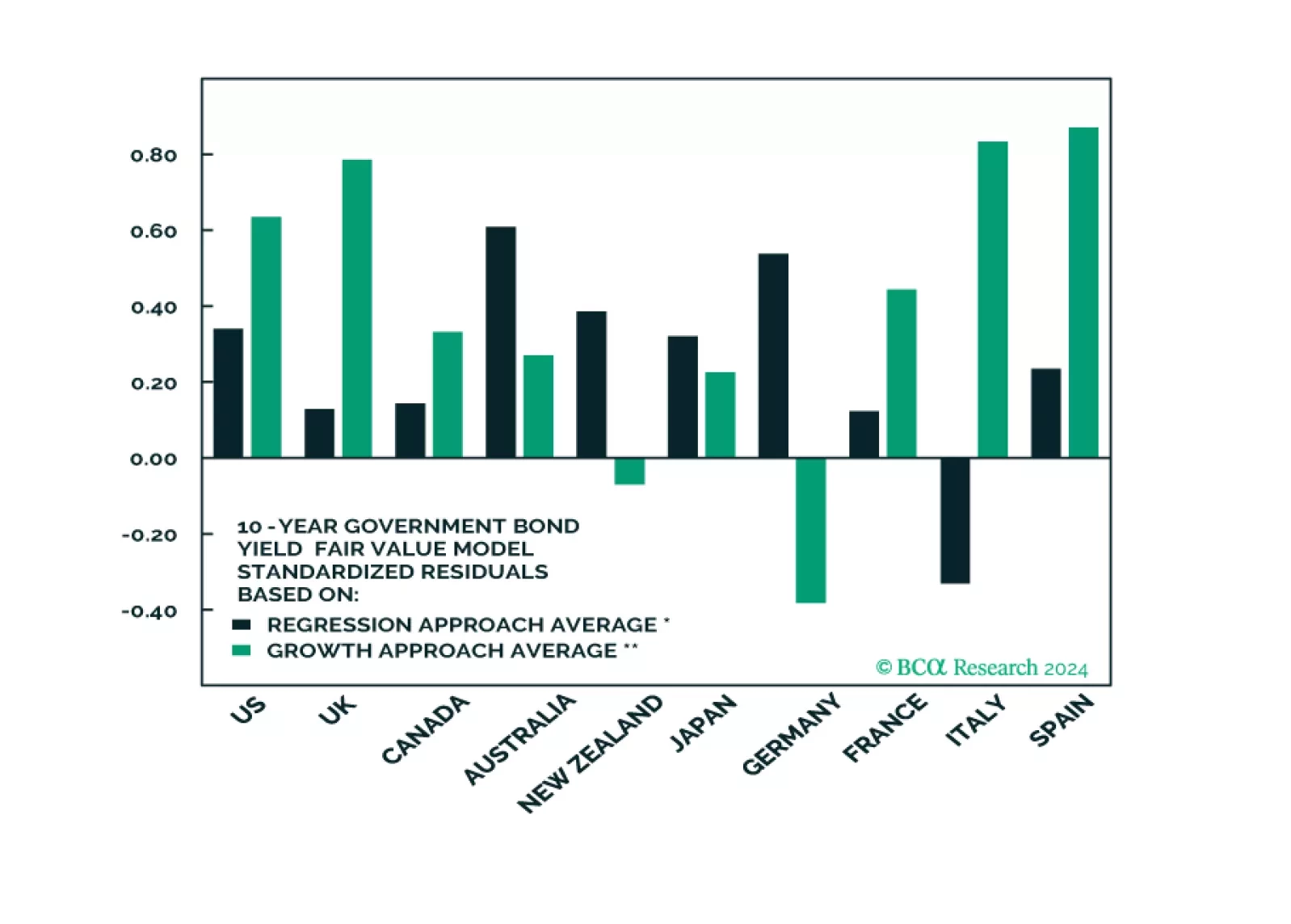

In this Special Report we assess the absolute and relative attractiveness of developed market government bonds using several fair value models. Longer-term investors who are focused on value should overweight US long-maturity bonds, and favor Spanish, Australian, and potentially UK government bonds within a DM ex-US allocation.

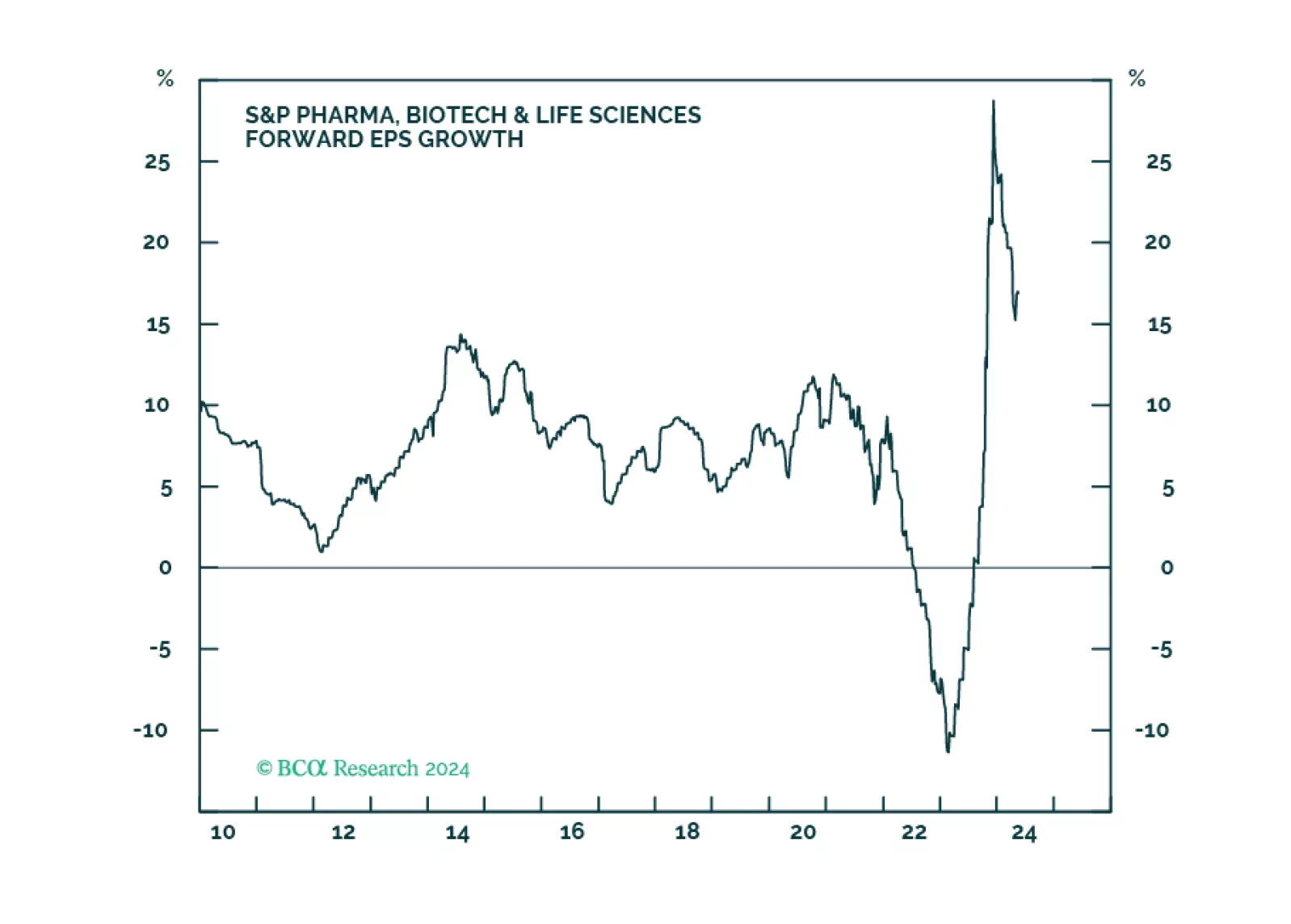

We recommend overweight in Pharma over a tactical and strategic investment horizon, as challenges, that have recently hampered the industry group’s performance, are dissipating. Likely election outcomes are positive for the industry, while major trends like generative AI applied to drug development and an aging population are long-term tailwinds.

Sentiment among German companies stalled in May, after having firmed for 3 consecutive months. The IFO Business Climate came in at 89.3, unchanged from April, disappointing expectations of further strengthening to 90.4. Although respondents’ assessment of…

The US manufacturing cycle has followed a surprisingly stable pattern for over seven decades. History suggests that this cycle tends to last for about 36 months, with a down leg spanning 18 months, followed by an up leg approximately spanning another 18…