Corporate Bonds

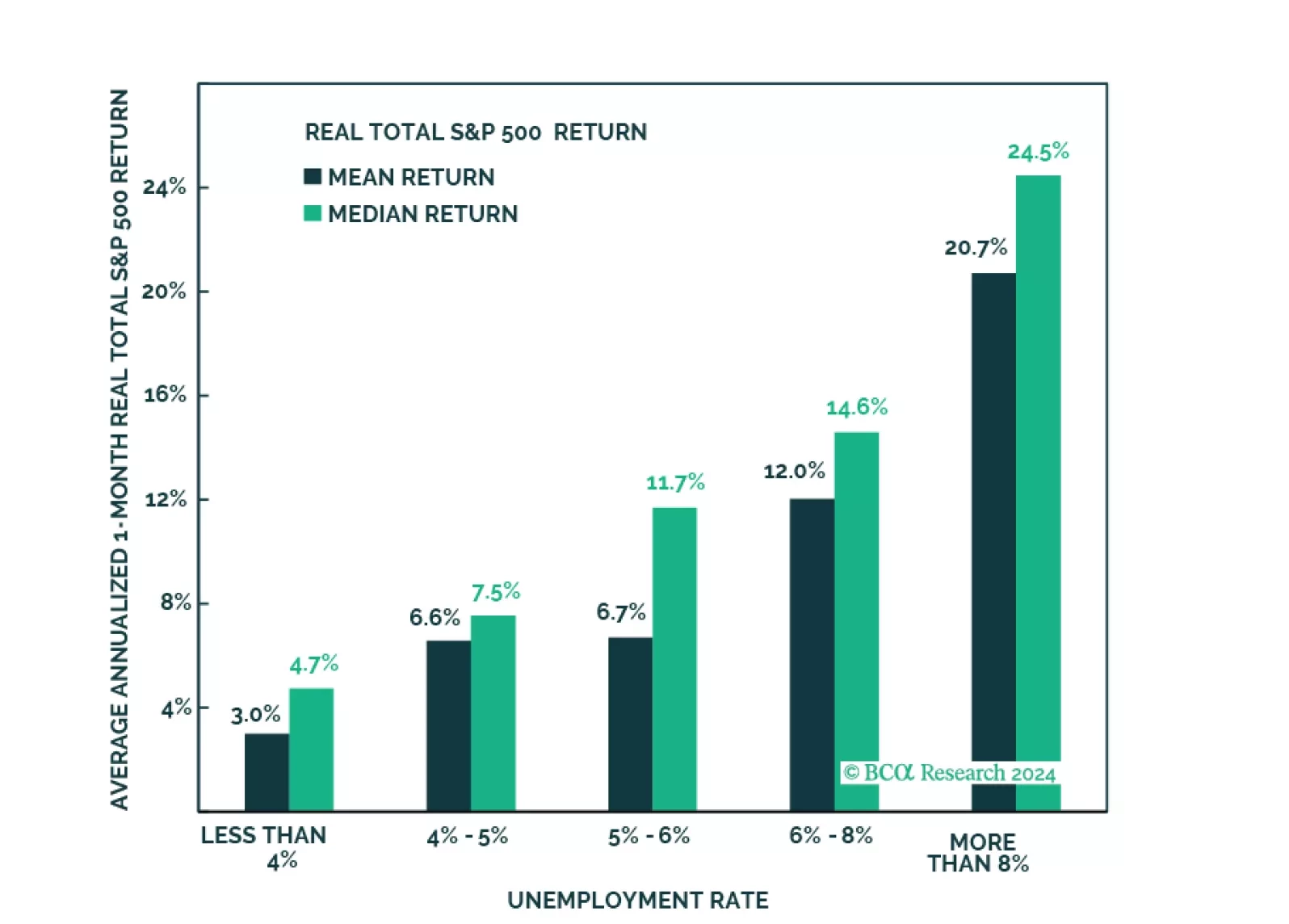

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.

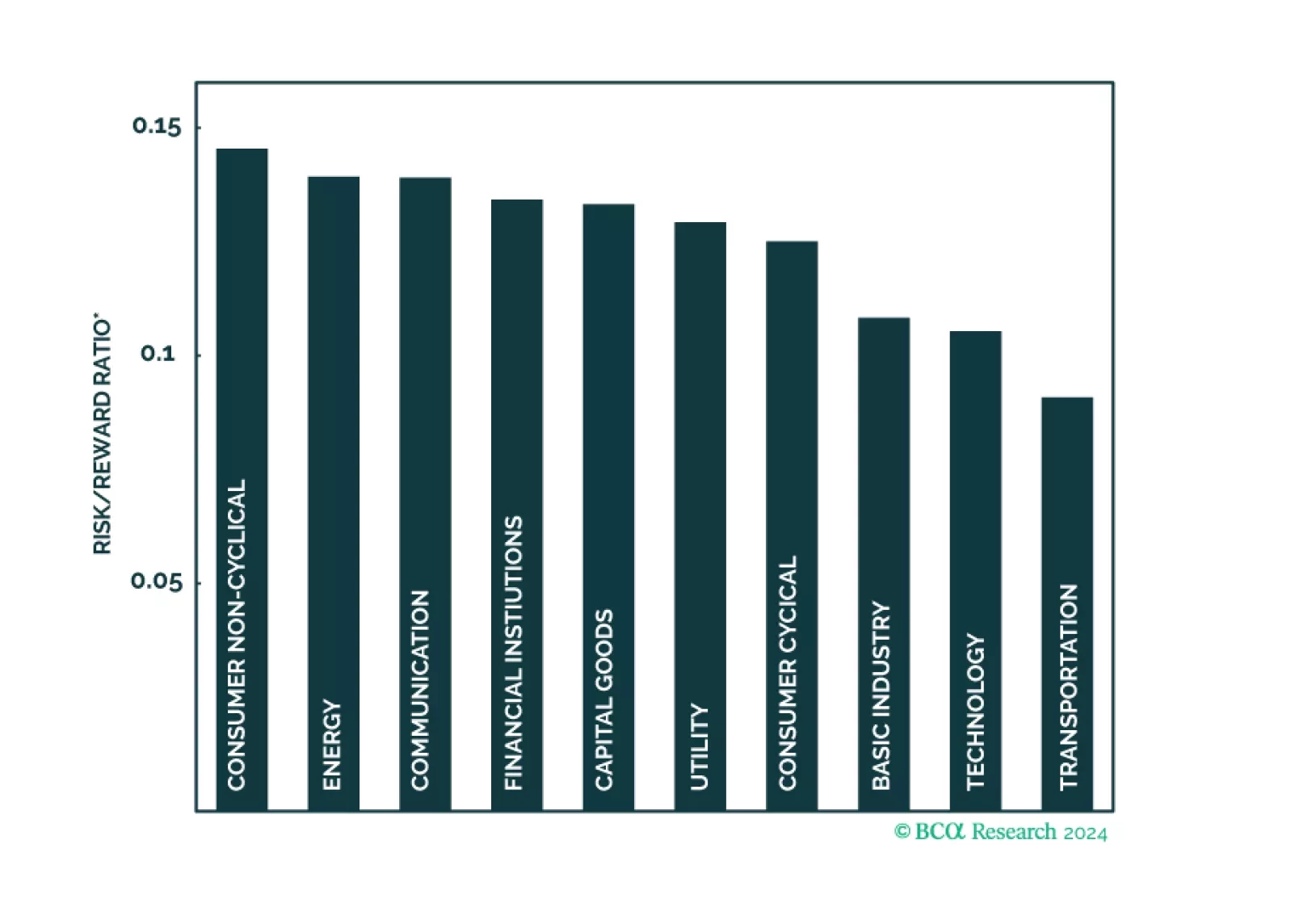

A risk/reward ranking of the 10 major US investment grade corporate bond sectors.

Our Portfolio Allocation Summary for March 2024.

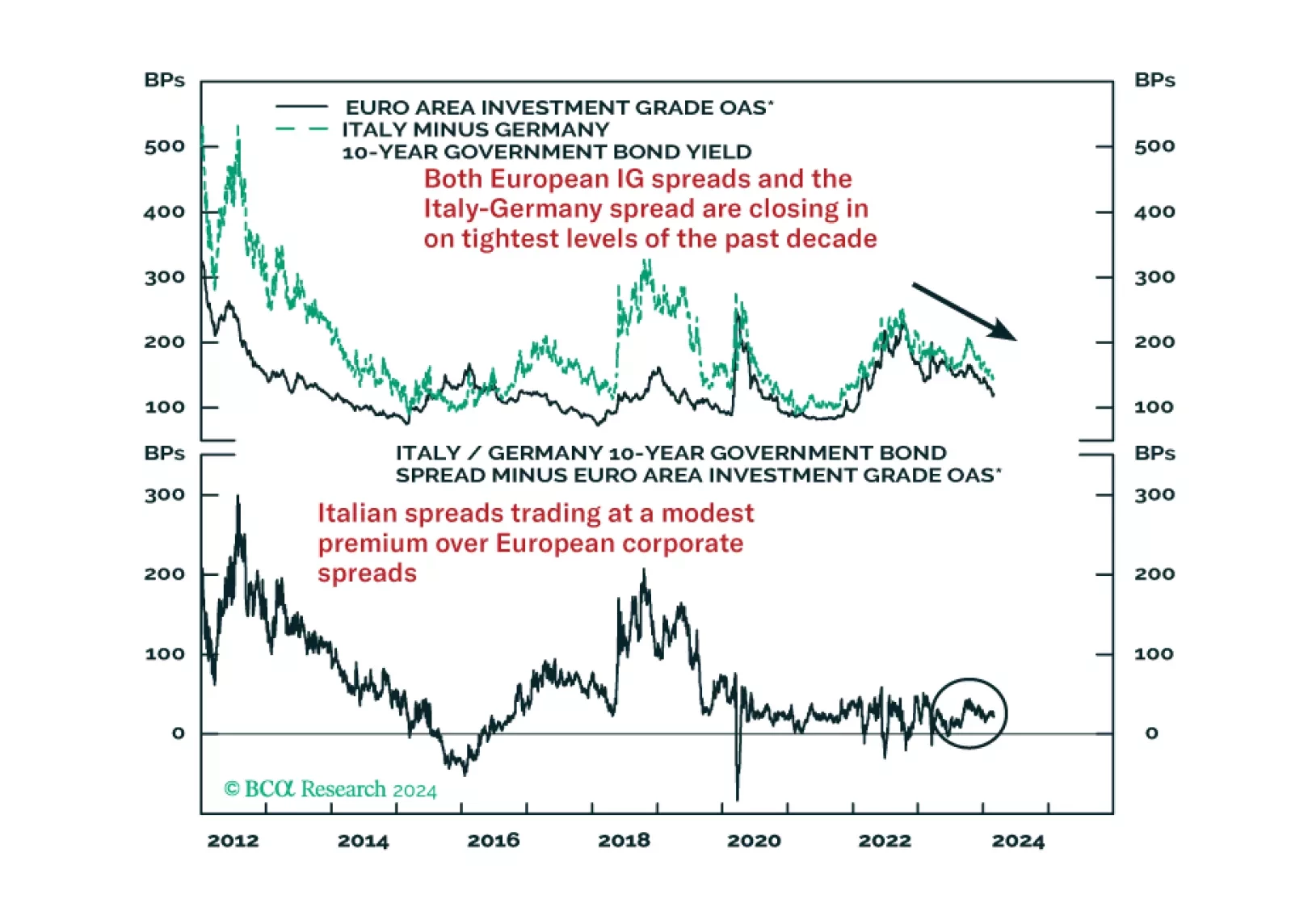

In this Strategy Insight, we take a comparative look at two of the largest spread product sectors in Europe – Italian government bonds and investment grade corporates. We make the case for favoring Italy over investment grade in the event of a downturn in European economic sentiment.

We rank the US spread sectors in terms of risk versus reward.

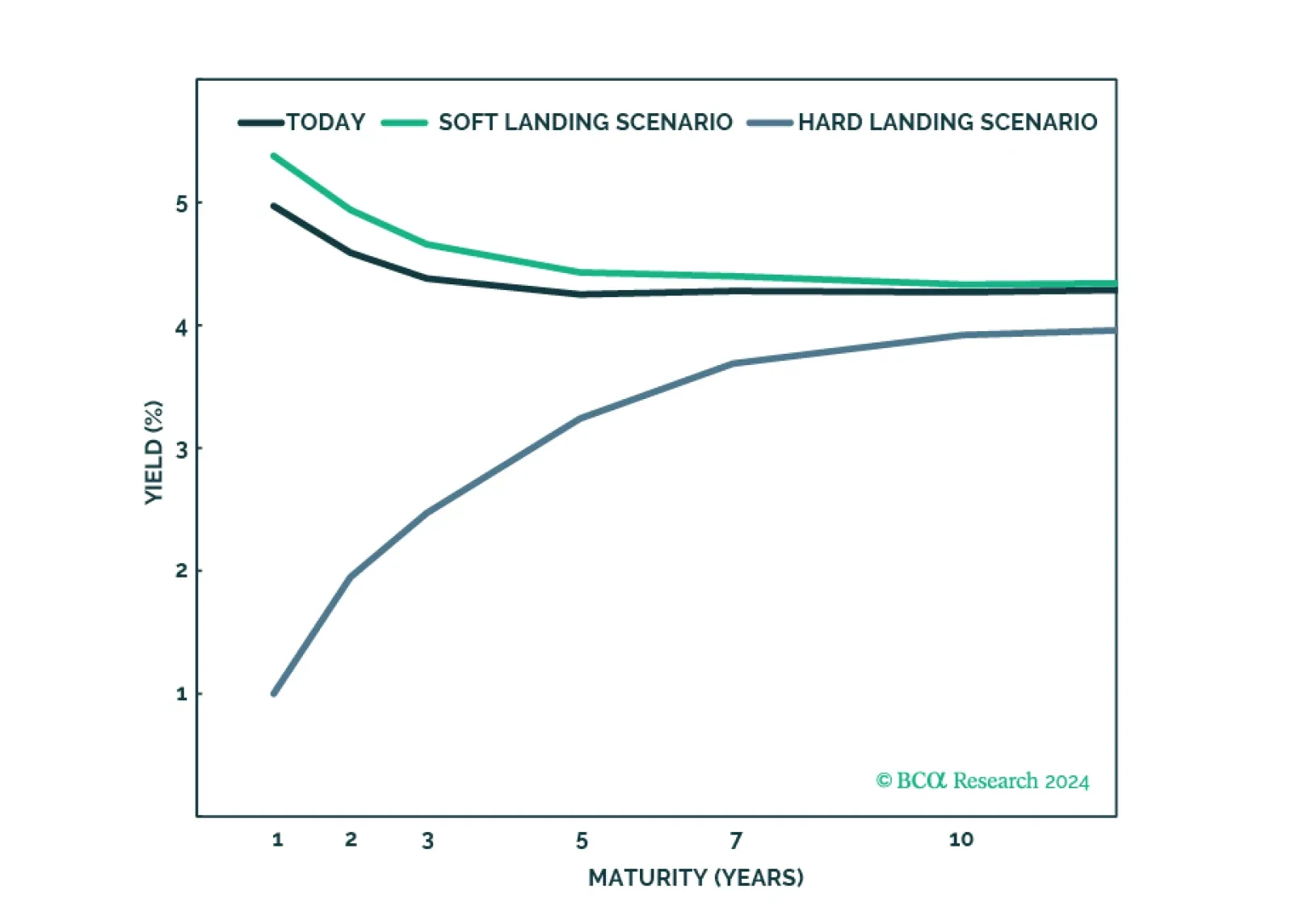

Easier financial conditions, rising home prices, rebounding consumer sentiment, and a stabilization in manufacturing activity all augur well for near-term US growth prospects. An unsustainably low savings rate is a key risk to the US economic outlook. Our revised forecast is centered on a recession starting in late 2024 or early 2025.

Our Portfolio Allocation Summary for February 2024.

When will the US also buckle under high rates? We expect a US recession to begin around mid-year. Stay defensive.