Commodities & Energy Sector

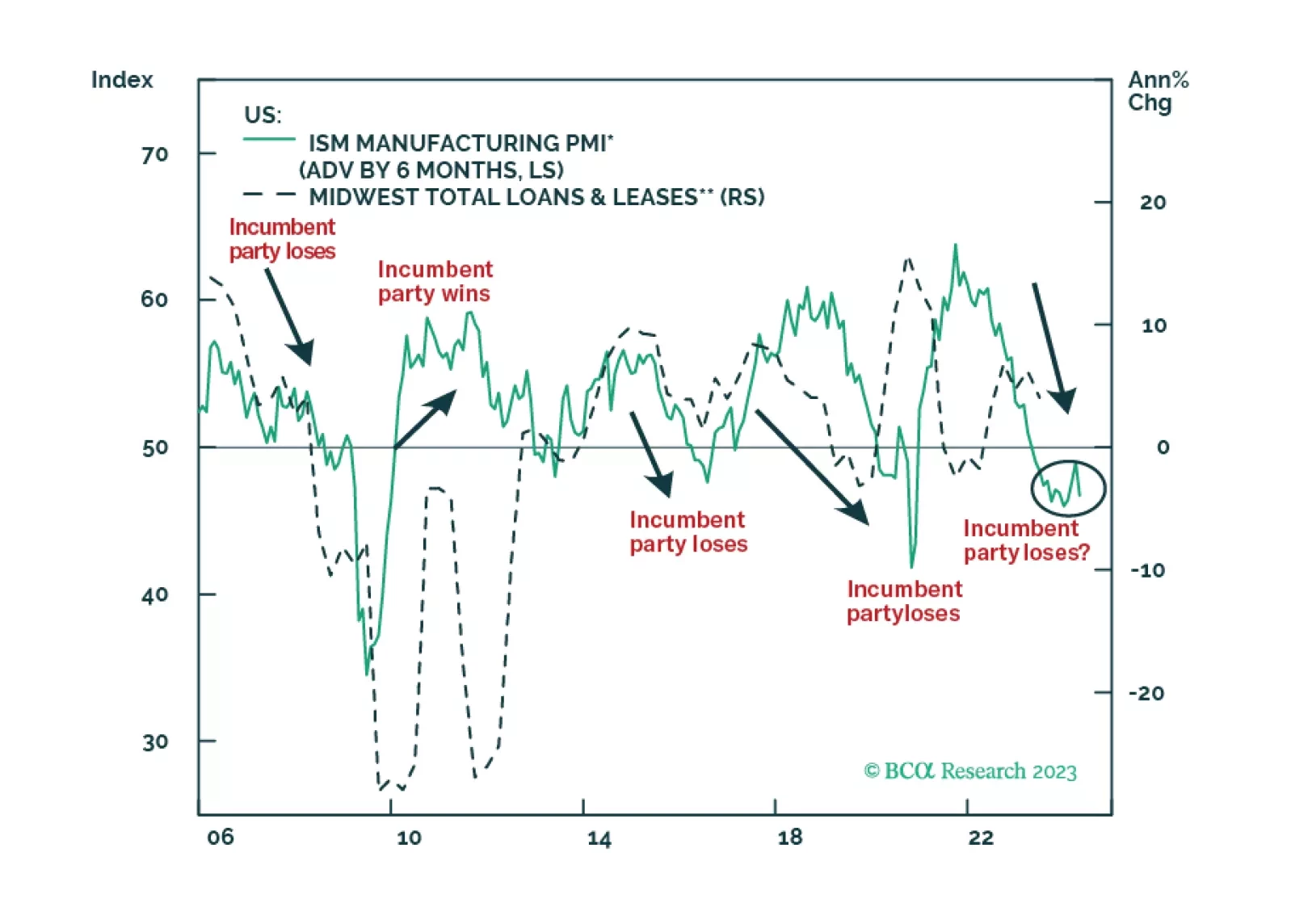

President Biden is facing foreign challenges on three fronts and these challenges are coalescing around the critical states of the Midwest. Take risks off the table and stay defensive in 2024.

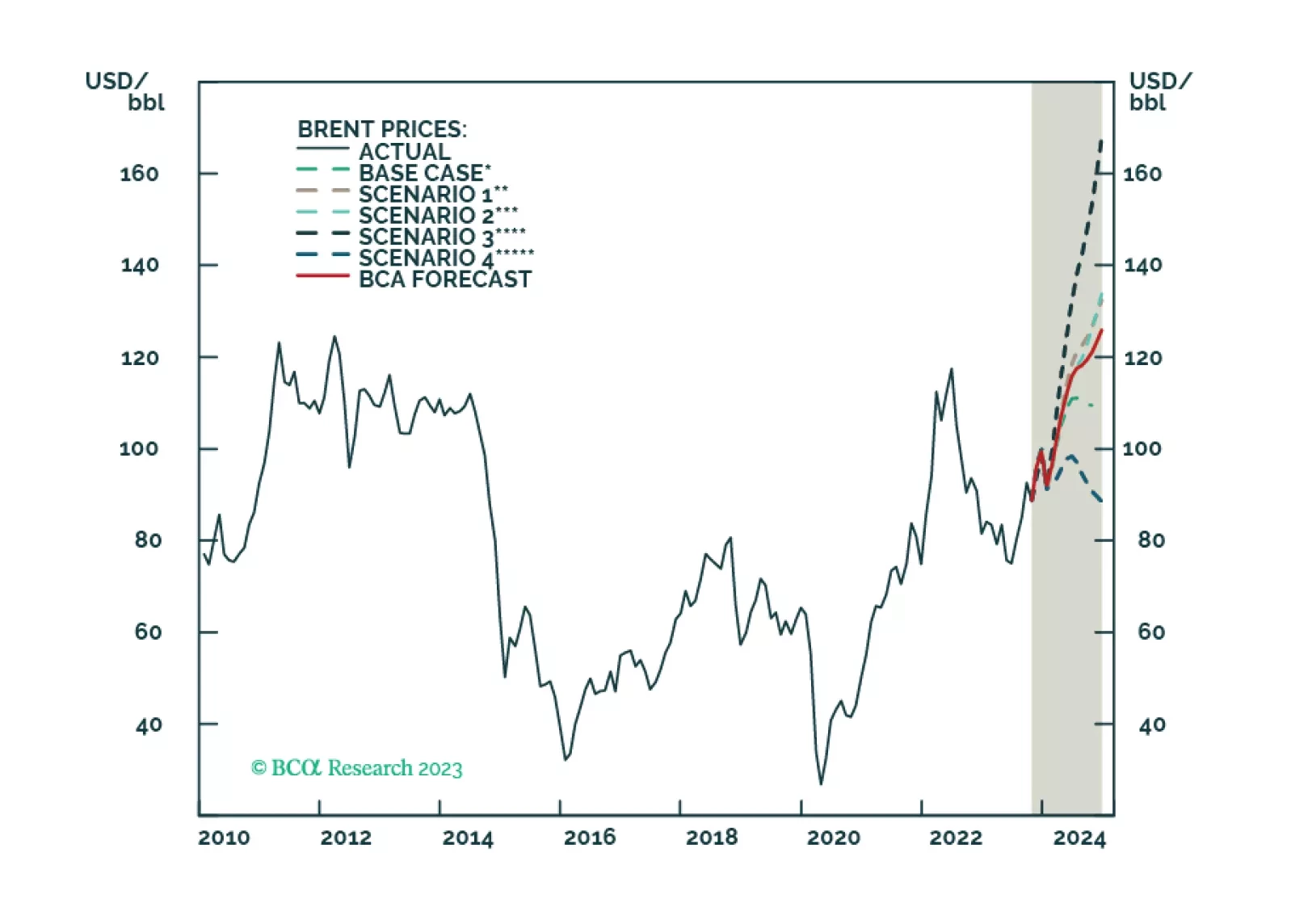

US and Chinese oil-demand strength will offset EU weakness next year. Incremental supply growth from non-OPEC 2.0 producers, coupled with a lower risk of the US enforcing its sanctions on Iranian oil exports, reduces our 2024 Brent price forecast by $6/bbl, and takes it to $112/bbl.

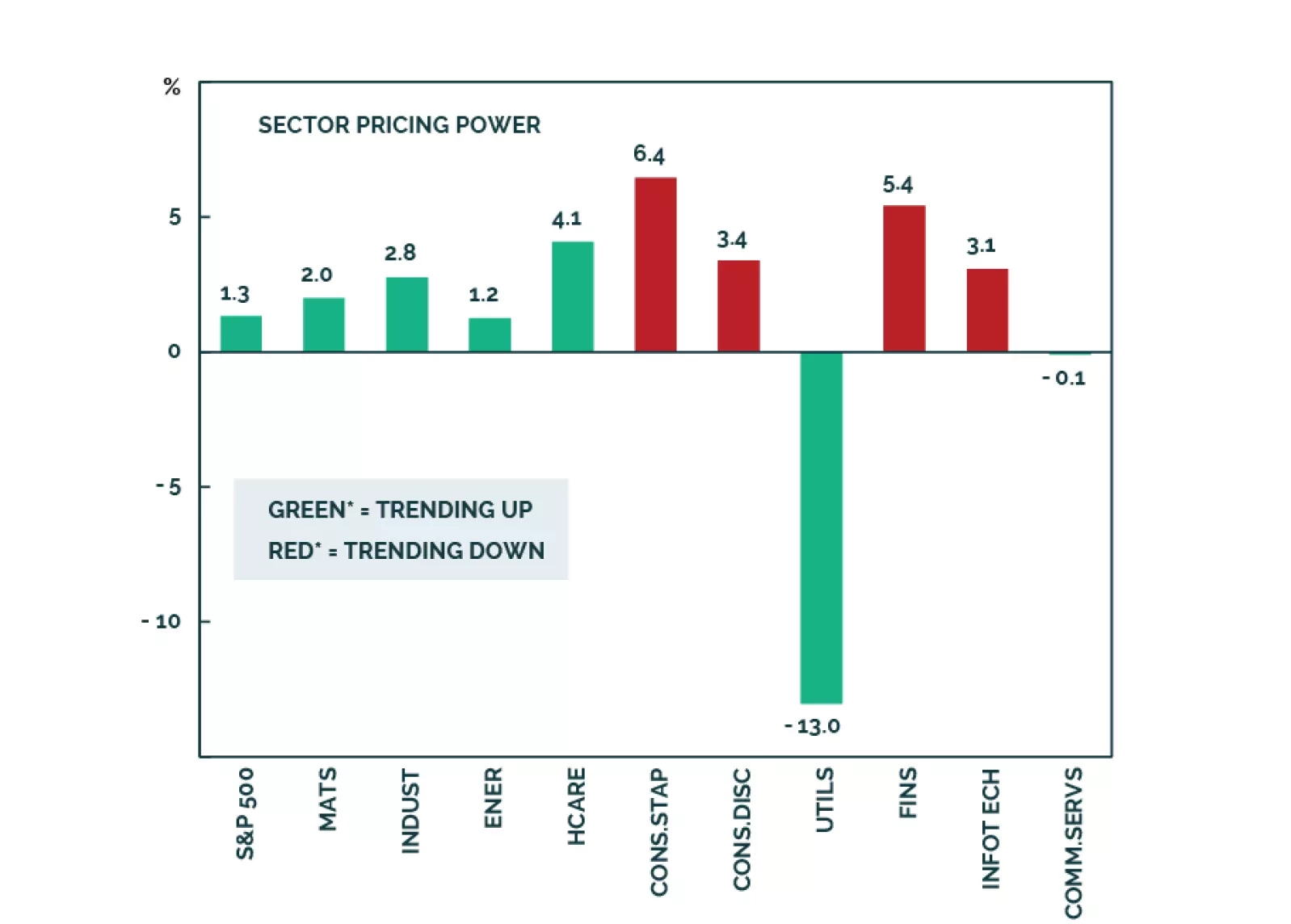

Q3 earnings commentary has been broadly positive, despite intensifying macro headwinds. Going forward, a negative growth outlook and geopolitical risks, are a threat to buoyant earnings expectations. We project that earnings growth for 2024 will move lower than currently projected - a negative for equities. This Santa Claus rally is unlikely to be the start of a new bull market.