Business Cycles

Brent prices climbed to an over six-year high on Tuesday, nearly touching $80/bbl. Current prices are above our Commodity & Energy strategists’ expectation that prices will average $70.50/bbl in Q4 and $75/bbl in 2022. The team views oil markets as facing…

BCA Research’s Global Fixed Income Strategy service recommends investors underweight government bonds where markets are discounting a path for future policy rates over the next two years that is too flat: the US, UK, Canada, and Norway Last week…

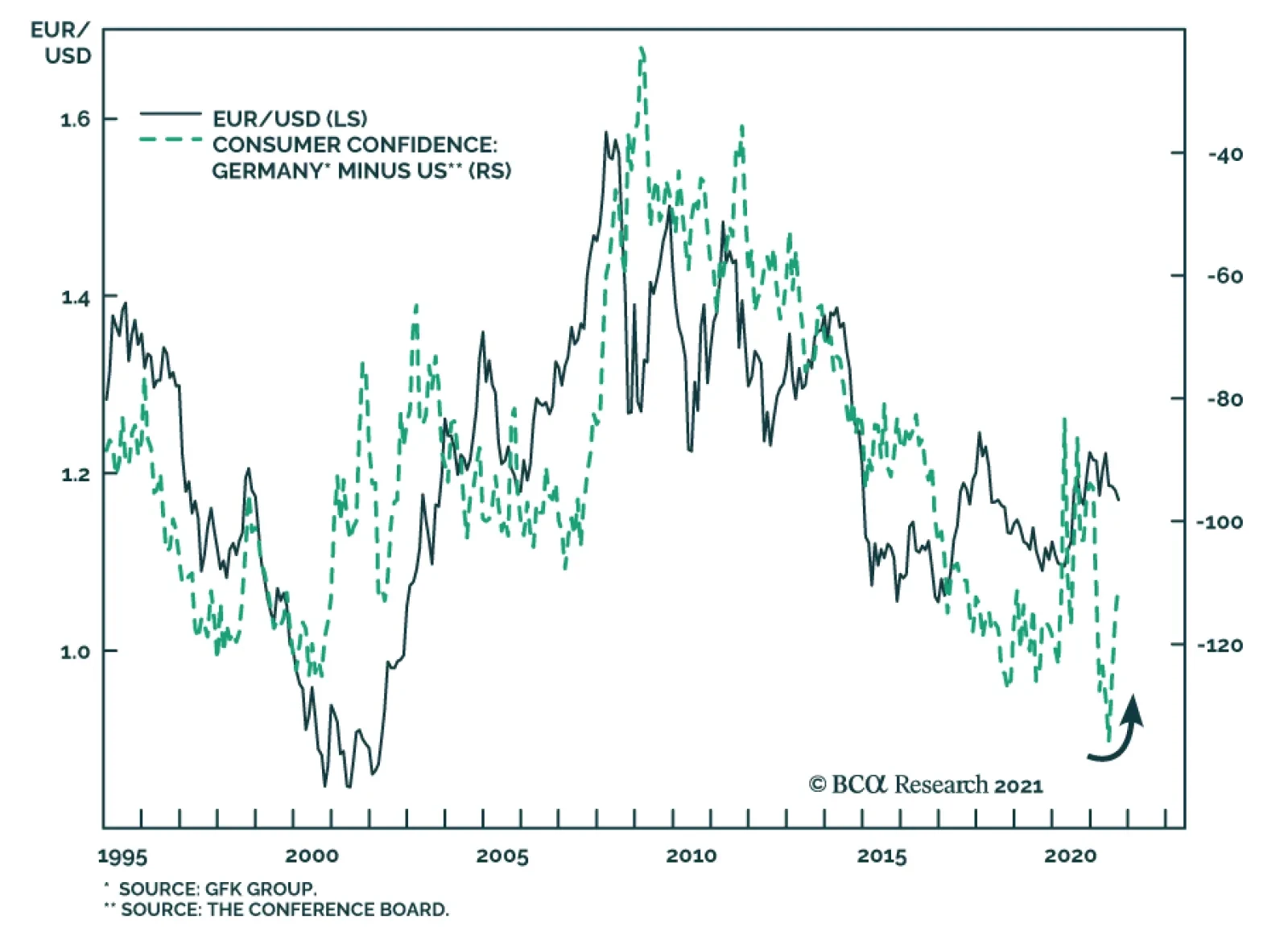

US and Euro Area measures of consumer confidence are diverging. According to the Conference Board survey, US consumer sentiment declined for the third consecutive month to a seven-month low of 109.3 in September. The nearly six-point drop is well below…

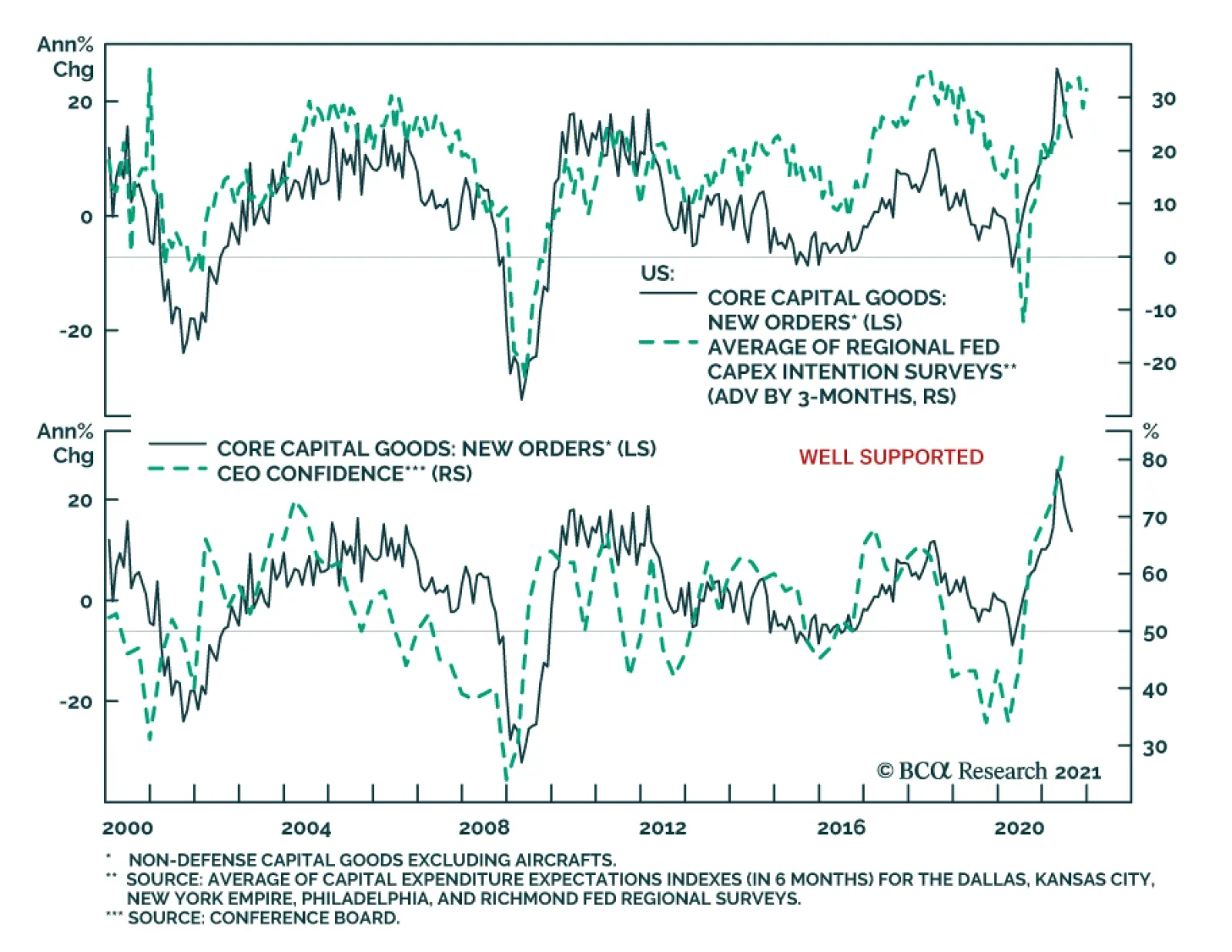

New orders for US durable goods grew 1.8% month-on-month to a record $263.5 billion in August. The increase follows an upwardly revised 0.5% and is more than double expectations of a 0.7% rise. However, a 5.5% month-on-month surge in transportation equipment…

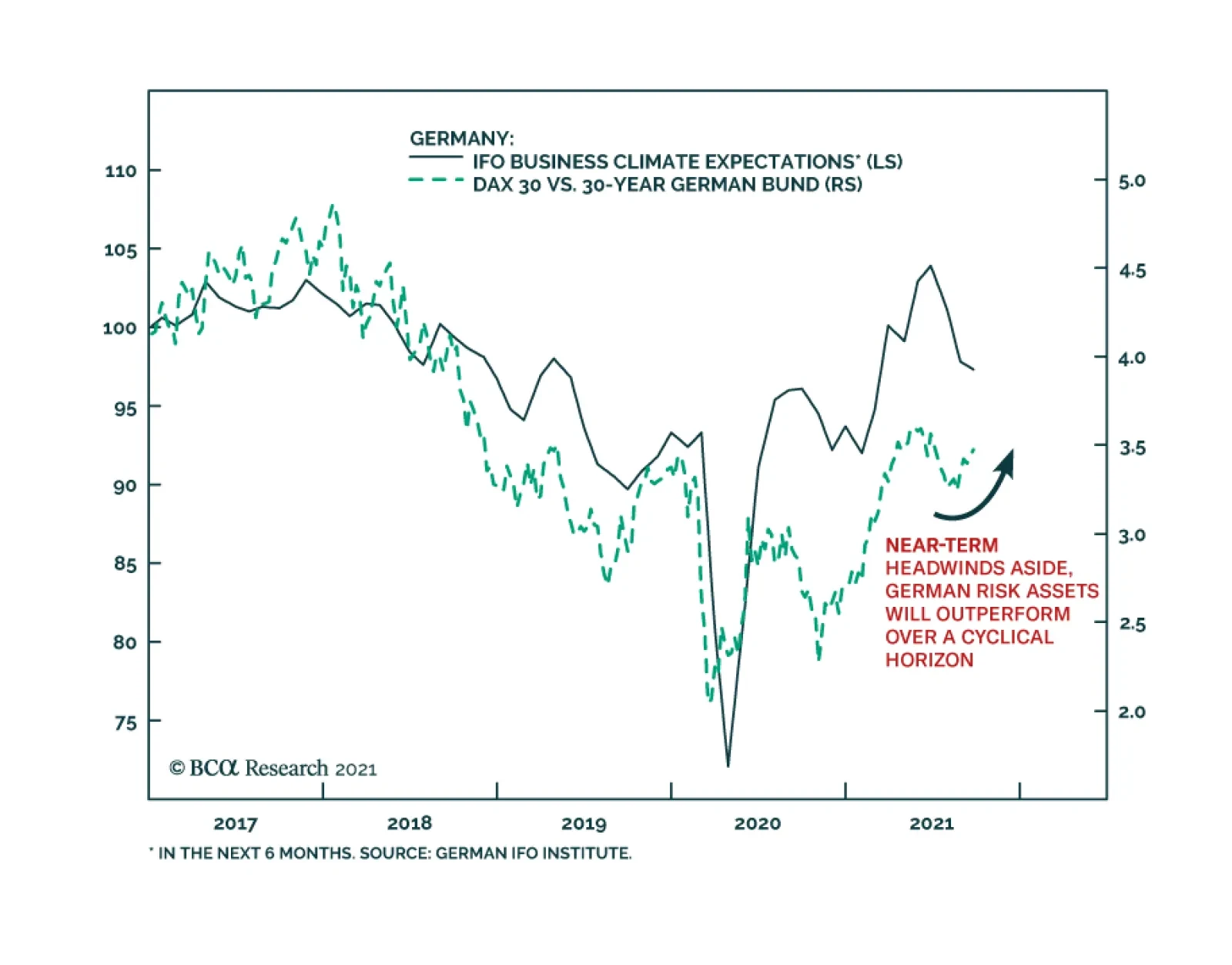

The German IFO’s Business Climate Index softened for the third consecutive month in September, falling to 98.8 from 99.6. The weakness was led by the Current Assessment number which lost 1-point versus expectations of a minor improvement. Meanwhile, the…

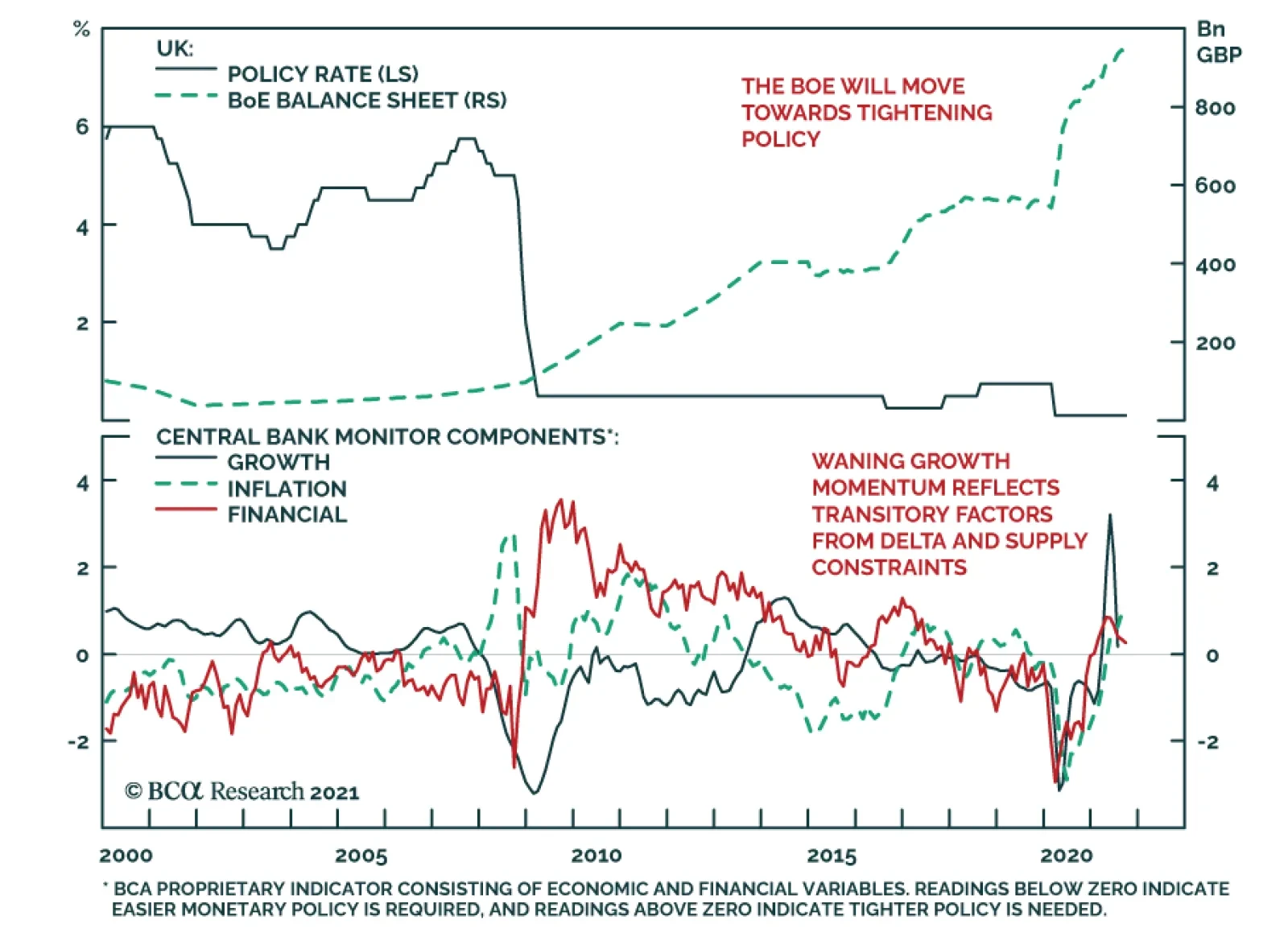

The Bank of England kept policy unchanged at its meeting on Thursday. Instead, it revised down its Q3 growth outlook to 2.1% from last month’s 2.9%. However, it highlighted that this revision largely reflects the dampening effect of supply constraints on…

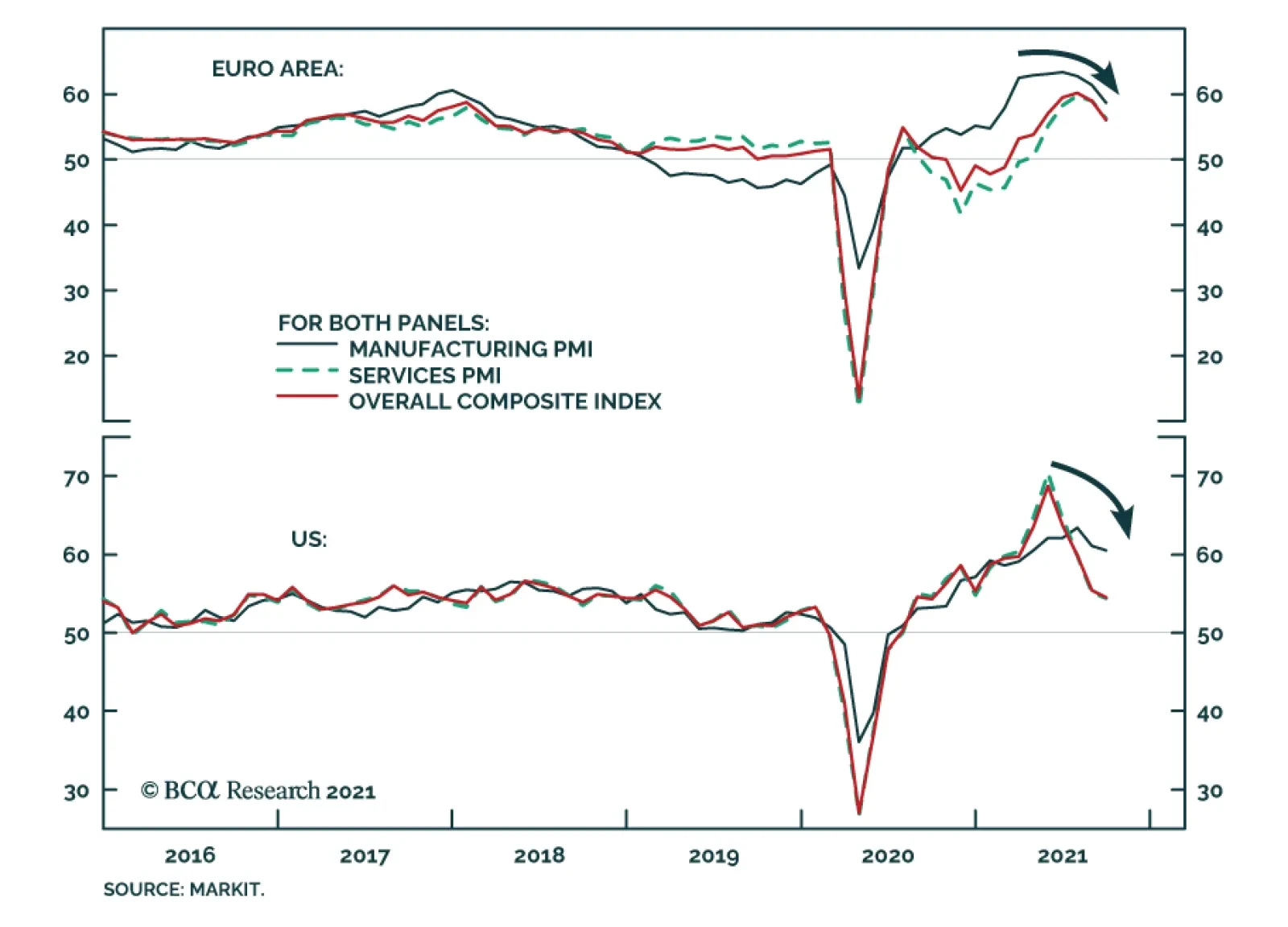

Manufacturing and service flash PMIs for September were weaker than expected. In the US, both service and manufacturing PMIs fell below expectations, bringing down the composite PMI by 0.9 points to 54.5. This dynamic was even more pronounced in the Euro…

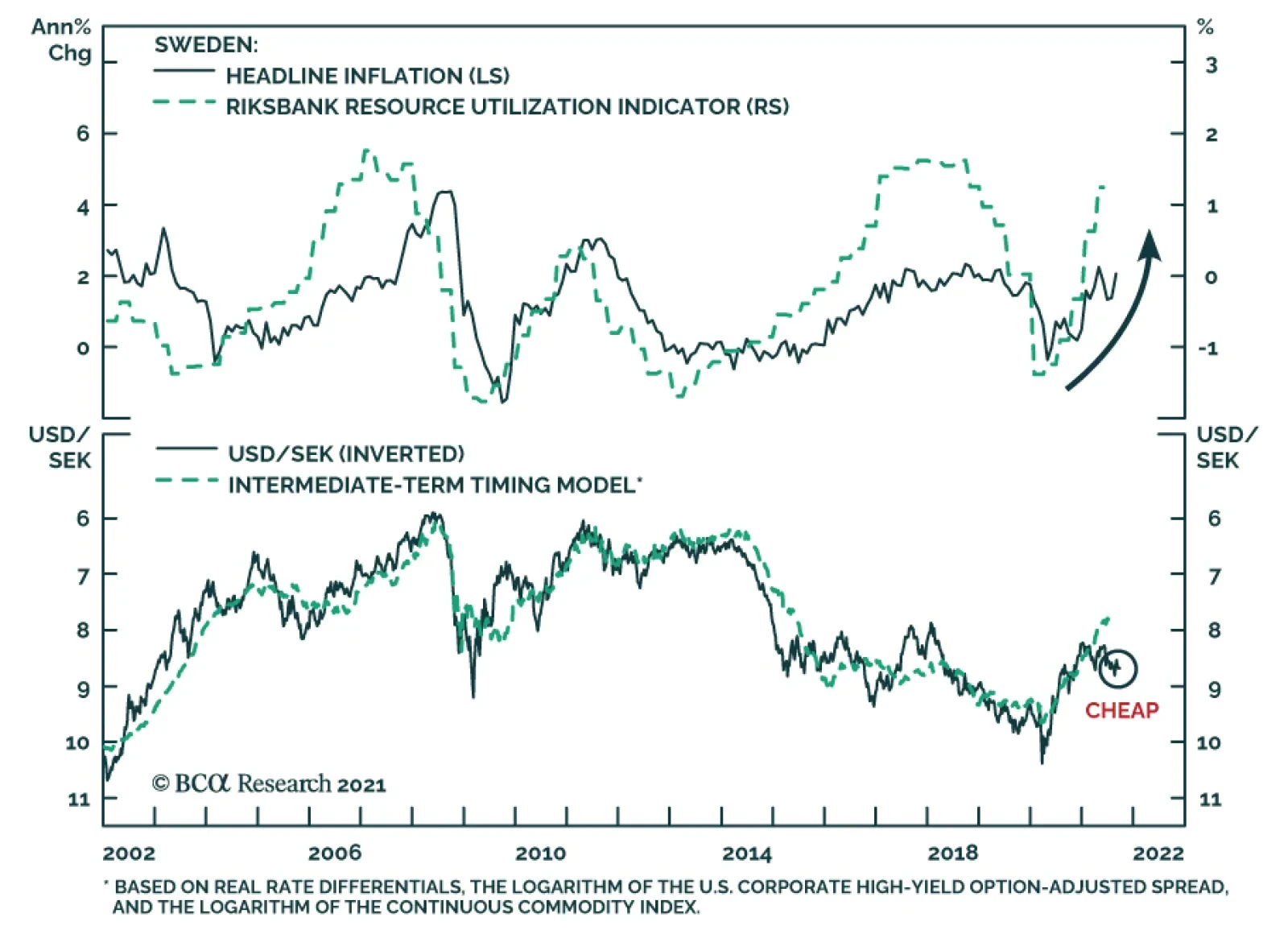

As expected, Sweden’s central bank maintained a dovish tone and kept policy unchanged following its meeting on Tuesday. The Riksbank acknowledged that Swedish inflation surprised to the upside relative to its July forecast. As anticipated by our European…

Highlights Stocks tend to perform worse when unemployment is low. Since 1950, the S&P 500 has risen at an annualized pace of 12% when the unemployment rate was above its historic average compared to 6% when the unemployment rate was below its average. Three reasons help explain this relationship: 1) The unemployment rate has historically been mean-reverting; 2) Low unemployment often leads to monetary tightening; and 3) Valuations are usually more stretched when unemployment is low. In the spring of 2020, stocks benefited from what turned out to be a very auspicious environment: A steady decline in the unemployment rate from very high levels, assisted by a massive dose of monetary and fiscal stimulus. Today, the situation is less clear-cut. The labor market has improved dramatically, while both monetary and fiscal policy are turning less accommodative. Nevertheless, the Fed is unlikely to hike rates for at least 12 months, and it will take much longer than that for monetary policy to turn restrictive. This suggests that we are still in the middle-to-late stages of a business cycle expansion that began following the Great Recession (and was only briefly interrupted by the pandemic). Historically, cyclical stocks have done well during this phase of the business cycle. To the extent that cyclicals are overrepresented in overseas indices, investors should favor non-US stock markets. Non-US stocks also trade at a substantial valuation discount to their US peers. A Surprising Relationship One of the best pieces of advice I received when I was starting my research career was to get to the punchline as soon as possible. As a strategist, you are not writing a detective novel where the answers are shrouded in mystery until the very end. You are providing conclusions to readers with supporting evidence. Chart 1Stocks Do Best When Unemployment Is High

Is Low Unemployment Good Or Bad For Stocks?

Is Low Unemployment Good Or Bad For Stocks?

With that in mind, let me answer the question posed in the title of this report: Is low unemployment good or bad for stocks? As Chart 1 shows, the answer is bad. The interesting issues are why it is bad and what this may mean for investors today. There are three key reasons why low unemployment has typically corresponded with paltry equity returns: The unemployment rate has historically been mean-reverting: Low unemployment is often followed by high unemployment. And, when the unemployment rate starts rising, it keeps rising. There has never been a case in the post-war era where the unemployment rate has risen by more than one-third of a percentage point without a recession occurring (Chart 2). Chart 2When Unemployment Starts Rising, It Usually Keeps Rising

When Unemployment Starts Rising, It Usually Keeps Rising

When Unemployment Starts Rising, It Usually Keeps Rising

Low unemployment often leads to monetary tightening: An economy can only grow at an above-trend pace if there is labor market slack. Once the slack runs out, growth is liable to weaken as supply-side constraints kick in. Worse yet, labor market overheating has historically prompted central banks to raise rates (Chart 3). Higher rates in the context of slowing growth is toxic for stocks. Valuations are usually more stretched when unemployment is low: During the post-war period, the S&P 500 has traded at an average Shiller P/E ratio of 22.5 when the unemployment rate was below its historic average compared to 16.3 when the unemployment rate was above its average. Implications For The Present Day Stocks fare best when unemployment is high but falling. In contrast, stocks fare the worst when unemployment is low and rising (Chart 4). My colleague Doug Peta, BCA’s Chief US Investment Strategist, reached a similar conclusion in his August report entitled Level Or Direction? Chart 3Low Unemployment Often Leads To Monetary Tightening

Low Unemployment Often Leads To Monetary Tightening

Low Unemployment Often Leads To Monetary Tightening

Chart 4Stocks Do Best When Unemployment Is Falling From High Levels

Is Low Unemployment Good Or Bad For Stocks?

Is Low Unemployment Good Or Bad For Stocks?

In the spring of 2020, stocks benefited from what turned out to be a very auspicious environment: A steady decline in the unemployment rate from very high levels, assisted by a massive dose of monetary and fiscal stimulus. Controversially at the time, this led us to argue that the pandemic could lead to much higher stock prices. Chart 5There Is Still Slack

There Is Still Slack

There Is Still Slack

Today, the situation is less clear-cut. On the one hand, the unemployment rate has fallen dramatically, while monetary and fiscal policy are turning less accommodative. This week, the ECB reduced the pace of net asset purchases under the PEPP. The Fed will start paring back asset purchases by the end of this year. Governments are also withdrawing fiscal policy support. In the US, emergency federal unemployment benefits expired, somewhat ironically, on Labor Day. On the other hand, the unemployment rate in most economies is still above pre-pandemic levels. In the US, the unemployment rate for prime-age workers is 1.7 percentage points higher than in February 2020, while the employment-to-population ratio is 2.4 points lower (Chart 5). The presence of labor market slack ensures that policy support will be withdrawn only gradually. Granted, core CPI inflation in the US is running above 4%. Standard Taylor Rule equations suggest that the Fed funds rate should be well above zero (Chart 6). That said, these equations use realized inflation, which may be misleading given that both market participants and Fed officials expect inflation to fall rapidly (Chart 7). Indeed, the widely followed 5-year/5-year forward TIPS breakeven rate is below the Fed’s comfort zone (Chart 8).1 With long-term inflation expectations still subdued, there is no urgency for the Fed to sound more hawkish. Chart 6What Rate Does The Taylor Rule Prescribe?

Is Low Unemployment Good Or Bad For Stocks?

Is Low Unemployment Good Or Bad For Stocks?

Chart 7Investors Expect Inflation To Fall Rapidly From Current Levels

Is Low Unemployment Good Or Bad For Stocks?

Is Low Unemployment Good Or Bad For Stocks?

Chart 8Long-Term Inflation Expectations Are Muted

Long-Term Inflation Expectations Are Muted

Long-Term Inflation Expectations Are Muted

Cyclical Stocks Usually Do Best In The Latter Innings Of The Business Cycle Expansion Monetary policy is unlikely to become restrictive in any major economy during the next 18 months, which should allow global growth to remain at an above-trend pace. Hence, it is too early to turn bearish on stocks. Nevertheless, given that the unemployment rate in most countries is closer to a trough than to a peak, it is reasonable to conclude that we are somewhere in the middle-to-late stages of a business cycle expansion that began following the Great Recession (and was only briefly interrupted by the pandemic). As Chart 9 shows, cyclical equity sectors, such as industrials, energy, and materials, typically do best in the latter innings of business cycle expansions. Such was the environment that prevailed in 2005-08, and such will be the environment that prevails over the coming quarters as the unemployment rate falls further, capital spending increases, and commodity prices rise further. Chart 9The Business Cycle And Equity Sectors

Is Low Unemployment Good Or Bad For Stocks?

Is Low Unemployment Good Or Bad For Stocks?

Increased government infrastructure spending should help cyclical sectors. The US Congress is set to pass a 10-year $500 billion package. The EU’s €750 billion Next Generation fund is finally up and running. Chinese local government infrastructure spending is poised to accelerate over the remainder of the year. Chart 10The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Chart 11Past Another Covid Wave

Is Low Unemployment Good Or Bad For Stocks?

Is Low Unemployment Good Or Bad For Stocks?

A weaker US dollar should also buoy cyclical stocks (Chart 10). As a countercyclical currency, the greenback usually weakens when global growth is strong. A cresting in the Delta variant wave should help jumpstart global growth over the coming months (Chart 11). Meanwhile, interest rate differentials have moved sharply against the US dollar, while the US trade deficit has widened noticeably (Charts 12A & B). Chart 12AInterest Rate Differentials Have Moved Against The Dollar

Interest Rate Differentials Have Moved Against The Dollar

Interest Rate Differentials Have Moved Against The Dollar

Chart 12BThe US Trade Deficit Has Widened Noticeably

The US Trade Deficit Has Widened Noticeably

The US Trade Deficit Has Widened Noticeably

Cyclical sectors are overrepresented outside the US (Table 1). Although not a classically cyclical sector, financials are also overrepresented in overseas indices. BCA’s global fixed-income strategists recommend a moderately underweight duration stance. As bond yields rise, bank shares should outperform (Chart 13). In contrast, tech stocks often lag in a rising yield environment. Table 1Cyclicals Are Overrepresented Outside The US

Is Low Unemployment Good Or Bad For Stocks?

Is Low Unemployment Good Or Bad For Stocks?

Chart 13Higher Rates: A Boon For Banks And A Bane For Tech

Higher Rates: A Boon For Banks And A Bane For Tech

Higher Rates: A Boon For Banks And A Bane For Tech

How Expensive Are Stocks? A high Shiller P/E predicts low future returns (Chart 14). Today, the Shiller P/E stands at 37 in the US. This is consistent with an expected 10-year total real return of close to zero for the S&P 500. Thus, the long-term outlook for US stocks is poor. We stress the words “long term.” As the bottom panel of Chart 14 shows, no matter what the starting point of valuations is, the average return over short-term horizons is very low relative to realized volatility. This is another way of saying that valuations provide a great deal of information about the long-term outlook for stocks, but little information about their near-term direction. Over horizons of about 12 months, the business cycle drives the stock market, as a simple comparison between purchasing manager indices and stock returns illustrates (Chart 15). Chart 14Valuation Is The Single Best Predictor Of Long-Term Equity Returns

Is Low Unemployment Good Or Bad For Stocks?

Is Low Unemployment Good Or Bad For Stocks?

Chart 15AThe Business Cycle Drives Cyclical Swings In Stocks

The Business Cycle Drives Cyclical Swings In Stocks

The Business Cycle Drives Cyclical Swings In Stocks

Chart 15BThe Business Cycle Drives Cyclical Swings In Stocks

The Business Cycle Drives Cyclical Swings In Stocks

The Business Cycle Drives Cyclical Swings In Stocks

Outside the US, the Shiller P/E stands at 20. In emerging markets, it is only 16 (Chart 16). This is significantly below US levels, implying that the long-term prospect for equities is much more attractive abroad. Thus, both medium-term cyclical factors and long-term valuation considerations favor non-US stocks. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Chart 16US Stocks Are Pricey

US Stocks Are Pricey

US Stocks Are Pricey

Footnotes 1 The Federal Reserve targets an average inflation rate of 2% for the personal consumption expenditures (PCE) index. The TIPS breakeven is based on the CPI index. Due to compositional differences between the two indices, CPI inflation has historically averaged 30-to-50 basis points higher than PCE inflation. This is why the Fed effectively targets a CPI inflation rate of about 2.3%-to-2.5%. Global Investment Strategy View Matrix

Is Low Unemployment Good Or Bad For Stocks?

Is Low Unemployment Good Or Bad For Stocks?

Special Trade Recommendations

Is Low Unemployment Good Or Bad For Stocks?

Is Low Unemployment Good Or Bad For Stocks?

Current MacroQuant Model Scores

Is Low Unemployment Good Or Bad For Stocks?

Is Low Unemployment Good Or Bad For Stocks?

Highlights Globalization is recovering to its pre-pandemic trajectory. But it will fail to live up to potential, as the “hyper-globalization” trends of the 1990s are long gone. China was the biggest winner of hyper-globalization. It now faces unprecedented risks in the context of hypo-globalization. Global investors woke up to China’s domestic political risks this year, which include arbitrary regulatory crackdowns on tech and private business. While Chinese officials will ease policy to soothe markets, the cyclical and structural outlook is still negative for this economy. Growth and stimulus have peaked. Political risk will stay high through the national party congress in fall 2022. US-China relations have not stabilized. India, the clearest EM alternative for global investors, is high-priced relative to China and faces troubles of its own. It is too soon to call a bottom for EM relative to DM. Feature Global investors woke up to China’s domestic political risk over the past week, as Beijing extended its regulatory crackdown to private education companies. Our GeoRisk Indicator shows Chinese political risk reaching late 2017 levels while the broad Chinese stock market continued this year’s slide against emerging market peers (Chart 1). Chart 1China: Domestic Political Risk Takes Investors By Surprise

Hypo-Globalization (A GeoRisk Update)

Hypo-Globalization (A GeoRisk Update)

A technical bounce in Chinese tech stocks will very likely occur but we would not recommend playing it. The first of our three key views for 2021 is the confluence of internal and external headwinds for China. True, today’s regulatory blitz will pass over like previous ones and the fast money will snap up Chinese tech firms on the cheap. The Communist Party is making a show of force, not destroying its crown jewels in the tech sector. However, the negative factors weighing on China are both cyclical and structural. Until Chinese President Xi Jinping adjusts his strategy and US-China relations stabilize, investors do not have a solid foundation for putting more capital at risk in China. Globalization is in retreat and this is negative for China, the big winner of the past 40 years. Hypo-Globalization Globalization in the truest sense has expanded over millenia. It will only reverse amid civilizational disasters. But the post-Cold War era of “hyper-globalization” is long gone.1 The 2010s saw the emergence of de-globalization. In the wake of COVID-19, global trade is recovering to its post-2008 trend but it is nowhere near recovering the post-1990 trend (Chart 2). Trade exposure has even fallen within the major free trade blocs, like the EU and USMCA (Chart 3). Chart 2Hypo-Globalization

Hypo-Globalization

Hypo-Globalization

Chart 3Trade Intensity Slows Even Within Trade Blocs

Trade Intensity Slows Even Within Trade Blocs

Trade Intensity Slows Even Within Trade Blocs

Of course, with vaccines and stimulus, global trade will recover in the coming decade. We coined the term “hypo-globalization” to capture this predicament, in which globalization is set to rebound but not to its previous trajectory.2 We now inhabit a world that is under-globalized and under-globalizing, i.e. not as open and free as it could be. A major factor is the US-China economic divorce, which is proceeding apace. China’s latest state actions – in diplomacy, finance, and business – underscore its ongoing disengagement from the US-led global architecture. The US, for its part, is now on its third presidency with protectionist leanings. American and European fiscal stimulus are increasingly protectionist in nature, including rising climate protectionism. Bottom Line: The stimulus-fueled recovery from the global pandemic is not leading to re-globalization so much as hypo-globalization. A cyclical reboot of cross-border trade and investment is occurring but will fall short of global potential due to a darkening geopolitical backdrop. Still No Stabilization In US-China Relations Chart 4Do Nations Prefer Growth? Or Security?

Hypo-Globalization (A GeoRisk Update)

Hypo-Globalization (A GeoRisk Update)

A giant window of opportunity is closing for China and Russia – they will look back fondly on the days when the US was bogged down in the Middle East. The US current withdrawal from “forever wars” incentivizes Beijing and Moscow to act aggressively now, whether at home or abroad. Investors tend to overrate the Chinese people’s desire for economic prosperity relative to their fear of insecurity and domination by foreign powers. China today is more desirous of strong national defense than faster economic growth (Chart 4). The rise of Chinese nationalism is pronounced since the Great Recession. President Xi Jinping confirmed this trend in his speech for the Communist Party’s first centenary on July 1, 2021. Xi was notably more concerned with foreign threats than his predecessors in 2001 and 2011 (Chart 5).3 China has arrived as a Great Power on the global stage and will resist being foisted into a subsidiary role by western nations. Chart 5Xi Jinping’s Centenary Speech Signaled Nationalist Turn

Hypo-Globalization (A GeoRisk Update)

Hypo-Globalization (A GeoRisk Update)

Meanwhile US-China relations have not stabilized. The latest negotiations did not produce agreed upon terms for managing tensions in the relationship. A bilateral summit between Presidents Biden and Xi Jinping has not been agreed to or scheduled, though it could still come together by the end of October. Foreign Minister Wang Yi produced a set of three major demands: that the US not subvert “socialism with Chinese characteristics,” obstruct China’s development, or infringe on China’s sovereignty and territorial integrity (Table 1). The US’s opposition to China’s state-backed economic model, export controls on advanced technology, and attempts to negotiate a trade deal with the province of Taiwan all violate these demands.4 Table 1China’s Three Demands From The United States (July 2021)

Hypo-Globalization (A GeoRisk Update)

Hypo-Globalization (A GeoRisk Update)

The removal of US support for China’s economic, development – recently confirmed by the Biden administration – will take a substantial toll on sentiment within China and among global investors. US President Joe Biden and four executive departments have explicitly warned investors not to invest in Hong Kong or in companies with ties to China’s military-industrial complex and human rights abuses. The US now formally accuses China of genocide in the Xinjiang region.5 Bottom Line: There is no stabilization in US-China relations yet. This will keep the risk premium in Chinese currency and equities elevated. The Sino-American divorce is a major driver of hypo-globalization. China’s Regulatory Crackdown President Xi Jinping’s strategy is consistent. He does not want last year’s stimulus splurge to create destabilizing asset bubbles and he wants to continue converting American antagonism into domestic power consolidation, particularly over the private economy. Now China’s sweeping “anti-trust” regulatory crackdown on tech, education, and other sectors is driving a major rethink among investors, ranging from Ark-founder Cathie Wood to perma-bulls like Stephen Roach. The driver of the latest regulatory crackdown is the administration’s reassertion of central party control. The Chinese economy’s potential growth is slowing, putting pressure on the legitimacy of single-party rule. The Communist Party is responding by trying to improve quality of life while promoting nationalism and “socialism with Chinese characteristics,” i.e. strong central government control and guidance over a market economy. Beijing is also using state power and industrial policy to attempt a great leap forward in science and technology in a bid to secure a place in the sun. Fintech, social media, and other innovative platforms have the potential to create networks of information, wealth, and power beyond the party’s control. Their rise can generate social upheaval at home and increase vulnerability to capital markets abroad. They may even divert resources from core technologies that would do more to increase China’s military-industrial capabilities. Beijing’s goal is to guide economic development, break up the concentration of power outside of the party, prevent systemic risks, and increase popular support in an era of falling income growth. Sociopolitical Risks: Social media has demonstrably exacerbated factionalism and social unrest in the United States, while silencing a sitting president. This extent of corporate power is intolerable for China. Economic And Financial Risks: Innovative fintech companies like Ant Group, via platforms like Alipay, were threatening to disrupt one of the Communist Party’s most important levers of power: the banking and financial system. The People’s Bank of China and other regulators insisted that Ant be treated more like a bank if it were to dabble in lending and wealth management. Hence the PBoC imposed capital adequacy and credit reporting requirements.6 Data Security Risks: Didi Chuxing, the ride-sharing company partly owned by Uber, whose business model it copied and elaborated on, defied authorities by attempting to conduct its initial public offering in the United States in June. The Communist Party cracked down on the company after the IPO to show who was in charge. Even more, Beijing wanted to protect its national data and prevent the US from gaining insights into its future technologies such as electric and autonomous vehicles. Foreign Policy Risks: Beijing is also preempting the American financial authorities, who will likely take action to kick Chinese companies that do not conform to common accounting and transparency standards off US stock exchanges. Better to inflict the first blow (and drive Chinese companies to Hong Kong and Shanghai for IPOs) than to allow free-wheeling capitalism to continue, giving Americans both data and leverage. Thus Beijing is continuing the “self-sufficiency” drive, divorcing itself from the US economy and capital markets, while curbing high-flying tech entrepreneurs and companies. The party’s muscle-flexing will culminate in Xi Jinping’s consolidation of power over the Politburo and Central Committee at the twentieth national party congress in fall 2022, where he is expected to take the title of “Chairman” that only Mao Zedong has held before him. The implication is that the regulatory crackdown can easily last for another six-to-12 more months. True, investors will become desensitized to the tech crackdown. But health care and medical technology are said to be in the Chinese government’s sights. So are various mergers and acquisitions. Both regulatory and political risk premia in different sectors can persist. The current administration has waged several sweeping regulatory campaigns against monopolies, corruption, pollution, overcapacity, leverage, and non-governmental organizations. The time between the initial launch of one of these campaigns and their peak intensity ranges from two to five years (Chart 6). Often, but not always, central policy campaigns have an express, three-year plan associated with them. Chart 6ABeijing Cracked Down On Monopolies, Corruption, Pollution...

Beijing Cracked Down On Monopolies, Corruption, Pollution...

Beijing Cracked Down On Monopolies, Corruption, Pollution...

Chart 6B...NGOs, Overcapacity, And Leverage

...NGOs, Overcapacity, And Leverage

...NGOs, Overcapacity, And Leverage

Chart 7China Tech: Buyer Beware

China Tech: Buyer Beware

China Tech: Buyer Beware

The first and second year mark the peak impact. The negative profile of Chinese tech stocks relative to their global peers suggests that the current crackdown is stretched, although there is little sign of bottom formation yet (Chart 7). The crackdown began with Alibaba founder Jack Ma, and Alibaba stocks have yet to arrest their fall either in absolute terms or relative to the Hang Seng tech index. Bottom Line: A technical bounce is highly likely for Chinese stocks, especially tech, but we would not recommend playing it because of the negative structural factors. For instance, we fully expect the US to delist Chinese companies that do not meet accounting standards. The Chinese Government’s Pain Threshold? The government is not all-powerful – it faces financial and economic constraints, even if political checks and balances are missing. Beijing does not have an interest in destroying its most innovative companies and sectors. Its goal is to maintain the regime’s survival and power. China’s crackdown on private companies goes against its strategic interest of promoting innovation and therefore it cannot continue indefinitely. The hurried meeting of the China Securities Regulatory Commission with top bankers on July 28 suggests policymakers are already feeling the heat.7 In the case of Ant Group, the company ultimately paid a roughly $3 billion fine (which is 18% of its annual revenues) and was forced to restructure. Ant learned that if it wants to behave more like a bank athen it will be regulated more like a bank. Yet investors will still have to wrestle with the long-term implications of China’s arbitrary use of state power to crack down on various companies and IPOs. This is negative for entrepreneurship and innovation, regardless of the government’s intentions. Chart 8China's Pain Threshold = Property Sector

China's Pain Threshold = Property Sector

China's Pain Threshold = Property Sector

Ultimately the property sector is the critical bellwether: it is a prime target of the government’s measures against speculative asset bubbles. It is also an area where authorities hope to ease the cost of living for Chinese households, whose birth rates and fertility rates are collapsing. While there is no risk of China’s entire economy crumbling because of a crackdown on ride-hailing apps or tutoring services, there is a risk of the economy crumbling if over-zealous regulators crush animal spirits in the $52 trillion property sector, as estimated by Goldman Sachs in 2019. Property is the primary store of wealth for Chinese households and businesses and falling property prices could well lead to an unsustainable rise in debt burdens, a nationwide debt-deflation spiral, and a Japanese-style liquidity trap. Judging by residential floor space started, China is rapidly approaching its overall economic pain threshold, meaning that property sector restrictions should ease, while monetary and credit policy should get easier as necessary to preserve the economic recovery (Chart 8). The economy should improve just in time for the party congress in late 2022. Bottom Line: China will be forced to maintain relatively easy monetary and fiscal policy and avoid pricking the property bubble, which should lend some support to the global recovery and emerging markets economies over the cyclical (12-month) time frame. China’s Regulation And Demographic Pressures Is the Chinese government not acting in the public interest by tamping down financial excesses, discouraging anti-competitive corporate practices, and combating social ills? Yes, there is truth to this. But arbitrary administrative controls will not increase the birth rate, corporate productivity, or potential GDP growth. First, it is true that Chinese households cite high prices for education, housing, and medicine as reasons not to have children (Chart 9). However, price caps do not attack the root causes of these problems. The lack of financial security and investment options has long fueled high house prices. The rabid desire to get ahead in life and the exam-oriented education system have long fueled high education prices. Monetary and fiscal authorities are forced to maintain an accommodative environment to maintain minimum levels of economic growth amid high indebtedness – and yet easy money policies fuel asset price inflation. In Japan, fertility rates began falling with economic development, the entrance of women in the work force, and the rise of consumer society. The fertility rate kept falling even when the country slipped into deflation. It perked up when prices started rising again! But it relapsed after the Great Recession and Fukushima nuclear crisis (Chart 10, top panel). Chart 9China: Concerns About Having Children

Hypo-Globalization (A GeoRisk Update)

Hypo-Globalization (A GeoRisk Update)

China’s fertility rate bottomed in the 1990s and has gradually recovered despite the historic surge in property prices (Chart 10, second panel), though it is still well below the replacement rate needed to reverse China’s demographic decline in the absence of immigration. A lower cost of living and a higher quality of life will be positive for fertility but will require deeper reforms.8 Chart 10Fertility Fell In Japan Despite Falling Prices

Fertility Fell In Japan Despite Falling Prices

Fertility Fell In Japan Despite Falling Prices

At the same time, arbitrary regulatory crackdowns that punish entrepreneurs are not likely to boost productivity. Anti-trust actions could increase competition, which would be positive for productivity, but China’s anti-trust actions are not conducted according to rule of law, or due process, so they increase uncertainty rather than providing a more stable investment environment. China’s tech crackdown is also aimed at limiting vulnerability to foreign (American) authorities. Yet disengagement with the global economy will reduce competition, innovation, and productivity in China. Bottom Line: China’s demographic decline will require larger structural changes. It will not be reversed by an arbitrary game of whack-a-mole against the prices of housing, education, and health. India And South Asia Chart 11China Will Ease Policy... Or India Will Break Out

China Will Ease Policy... Or India Will Break Out

China Will Ease Policy... Or India Will Break Out

Global investors have turned to Indian equities over the course of the year and they are now reaching a major technical top relative to Chinese stocks (Chart 11). Assuming that China pulls back on its policy tightening, this relationship should revert to mean. India faces tactical geopolitical and macroeconomic headwinds that will hit her sails and slow her down. In other words, there is no great option for emerging markets at the moment. Over the long run, India benefits if China falters. Following the peak of the second COVID-19 wave in May 2021, some high frequency indicators have showed an improvement in India’s economy. However, activity levels appear weaker than of other emerging markets (Chart 12). Given the stringency levels of India’s first lockdown last spring, year-on-year growth will look faster than it really is. As the base effect wanes, underlying weak demand will become evident. Moreover India is still vulnerable to COVID-19. Only 25% of the population has received one or more vaccine shots which is lower than the global level of 28%. The result will be a larger than expected budget deficit. India refrained from administering a large dose of government spending in 2020 (Chart 13). With key state elections due from early 2022 onwards, the government could opt for larger stimulus. This could assume the form of excise duty cuts on petroleum products or an increase in revenue expenditure. These kinds of measures will not enhance India’s productivity but will add to its fiscal deficit. Chart 12Weak Post-COVID Rebound In India – And Losing Steam

Hypo-Globalization (A GeoRisk Update)

Hypo-Globalization (A GeoRisk Update)

Chart 13India Likely To Expand Fiscal Spending Soon

Hypo-Globalization (A GeoRisk Update)

Hypo-Globalization (A GeoRisk Update)

Such an unexpected increase in India’s fiscal deficit could be viewed adversely by markets. India’s fiscal discipline tends to be poorer than that of peers (see Chart 13 above). Meanwhile India’s north views Pakistan unfavorably and key state elections are due in this region. Consequently, Indian policy makers may be forced to adopt a far more aggressive foreign policy response to any terrorist strikes from Pakistan or territorial incursions by China over August 2021. The US withdrawal from Afghanistan poses risks for India as it has revived the Taliban’s influence. India has a long history of being targeted by Afghani terrorist groups. And its diplomatic footprint in Afghanistan has been diminishing. Earlier in July, India decided temporarily to close its consulate in Kandahar and evacuated about 50 diplomats and security personnel. As August marks the last month of formal US presence in Afghanistan, negative surprises emanating from Afghanistan should be expected. Bottom Line: Pare exposure to Indian assets on a tactical basis. Our Emerging Markets Strategy takes a more optimistic view but geopolitical changes could act as a negative catalyst in the short term. We urge clients to stay short Indian banks. Investment Takeaways US stimulus contrasts with China’s turmoil. The US Biden administration and congressional negotiators of both parties have tentatively agreed on a $1 trillion infrastructure deal over eight years. Even if this bipartisan deal falls through, Democrats alone can and will pass another $1.3-$2.5 trillion in net deficit spending by the end of the year. Stay short the renminbi. Prefer a balance of investments in the dollar and the euro, given the cross-currents of global recovery yet mounting risks to the reflation trade. A technical bounce in Chinese stocks and tech stocks is nigh. China’s policymakers are starting to respond to immediate financial pressures. However, growth has peaked and structural factors are still negative. The geopolitical outlook is still gloomy and China’s domestic political clock is a headwind for at least 12 more months. Prefer developed market equities over emerging markets (Chart 14). Emerging markets failed to outperform in the first half of the year, contrary to our expectation that the global reflation trade would lift them. China/EM will benefit when Beijing eases policy and growth rebounds. Chart 14Emerging Markets: Not Out Of The Woods Yet

Emerging Markets: Not Out Of The Woods Yet

Emerging Markets: Not Out Of The Woods Yet

Stay short Indian banks and strongman EM currencies, including the Turkish lira, the Brazilian real, and the Philippine peso. The biggest driver of EM underperformance this year is the divergence between the US and China. But until China’s policy corrects, the rest of EM faces downside risks. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Ritika Mankar, CFA Editor/Strategist ritika.mankar@bcaresearch.com Footnotes 1 Dani Rodrik, The Globalization Paradox: Democracy and the Future of the World Economy (New York: Norton, 2011). 2 See my "Nationalism And Globalization After COVID-19," Investments & Wealth Monitor (Jan/Feb 2021), pp13-21, investmentsandwealth.org. 3 Our study of Xi’s speech is not limited to this quantitative, word-count analysis. A fuller comparison of his speech with that of his predecessors on the same occasion reveals that Xi was fundamentally more favorable toward Marx, less favorable toward Deng Xiaoping and the pro-market Third Plenum, utterly silent on notions of political reform or liberal reform, more harsh in his rhetoric toward the outside world, and hawkish about the mission of reunifying with Taiwan. 4 The Chinese side also insisted that the US stop revoking visas, punishing companies and institutes, treating the press as foreign agents, and detaining executives. It warned that cooperation – which the US seeks on the environment, Iran, North Korea, and other areas – cannot be achieved while the US imposes punitive measures. 5 See US Department of State, "Xinjiang Supply Chain Business Advisory," July 13, 2021, and "Risks and Considerations for Businesses Operating in Hong Kong," July 16, 2021, state.gov. 6 Top business executives are also subject to these displays of state power. For example, Alibaba founder Jack Ma caricatured China’s traditional banks as “pawn shops” and criticized regulators for stifling innovation. He is now lying low and has taken to painting! 7 See Emily Tan and Evelyn Cheng, "China will still allow IPOs in the United States, securities regulator tells brokerages," CNBC, July 28, 2021, cnbc.com. Officials are sensitive to the market blowback but the fact remains that IPOs in the US have been discouraged and arbitrary regulatory crackdowns are possible at any time. 8 Increasing social spending also requires local governments to raise more revenue but the central government had been cracking down on the major source of revenues for local government: land sales and local government financing vehicles. With the threat of punishment for local excesses and lack of revenue source, local governments have no choice but to cut social services, pushing affluent residents towards private services, while leaving the less fortunate with fewer services. As with financial regulations, the central government may backpedal from too tough regulation of local governments, but more economic and financial pain will be required to make it happen. The Geopolitics Of The Olympics The 2020 Summer Olympics are currently underway in Tokyo, even though it is 2021. The arenas are mostly empty given the global pandemic and economic slowdown. Every four years the Summer Olympics create a golden opportunity for the host nation to showcase its achievements, infrastructure, culture, and beauty. But the Olympics also have a long history of geopolitical significance: terrorist acts, war protests, social demonstrations, and boycotts. In 1906 an Irish athlete climbed a flag pole to wave the Irish flag in protest of his selection to the British team instead of the Irish one. In 1968 two African American athletes raised their fists as an act of protest against racial discrimination in the US after the assassination of Martin Luther King Jr. In 1972, the Palestinian terrorist group Black September massacred eleven Israeli Olympians in Munich, Germany. In 1980 the US led the western bloc to boycott the Moscow Olympics while the Soviet Union and its allies retaliated by boycotting the 1984 Los Angeles Olympics. In 2008, Russia used the Olympics as a convenient distraction from its invasion of Georgia, a major step in its geopolitical resurgence. So far, thankfully, the Tokyo Olympics have gone without incident. However, looking forward, geopolitics is already looming over the upcoming 2022 Winter Olympics in Beijing.

Hypo-Globalization (A GeoRisk Update)

Hypo-Globalization (A GeoRisk Update)

How the world has changed. The 2008 Summer Olympics marked China’s global coming-of-age celebration. The breathtaking opening ceremony featured 15,000 performers and cost $100 million. The $350 million Bird’s Nest Stadium showcased to the world China’s long history, economic prowess, and various other triumphs. All of this took place while the western democratic capitalist economies grappled with what would become the worst financial and economic crisis since the Great Depression. In 2008, global elites spoke of China as a “responsible stakeholder” that was conducting a “peaceful rise” in international affairs. The world welcomed its roughly $600 billion stimulus. Now elites speak of China as primarily a threat and a competitor, a “revisionist” state challenging the liberal world order. China is blamed for a lack of transparency (if not virological malfeasance) in handling the COVID-19 pandemic. It is blamed for breaking governance promises and violating human rights in Hong Kong, for alleged genocide in Xinjiang, and for a list of other wrongdoings, including tough “Wolf Warrior” diplomacy, cyber-crime and cyber-sabotage, and revanchist maritime-territorial claims. Even aside from these accusations it is clear that China is suffering greater financial volatility as a result of its conflicting economic goals. Talk of a diplomatic or even full boycott of Beijing’s winter games is already brewing. Sponsors are also second-guessing their involvement. More than half of Canadians support boycotting the winter games. Germany is another bellwether to watch. In 2014, Germany’s president (not chancellor) boycotted the Sochi Olympics; in 2021, the EU and China are witnessing a major deterioration of relations. Parliamentarians in the UK, Italy, Sweden, Switzerland, and Norway have asked their governments to outline their official stance on the winter games. In the age of “woke capitalism,” a sponsorship boycott of the games is a possibility. This is especially true given the recent Chinese backlash against European multinational corporations for violating China’s own rules of political correctness. A boycott which includes any members of the US, Norway, Canada, Sweden, Germany, or the Netherlands would be substantial as these are the top performers in the Winter Olympics. Even if there is no boycott, there is bound to be some political protests and social demonstrations, and China will not be able to censor anything said by Western broadcasters televising the events. Athletes usually suffer backlash at home if they make critical statements about their country, but they run very little risk of a backlash for criticizing China. If anything, protests against China’s handling of human rights will be tacitly encouraged. Beijing, for its part, will likely overreact, as these days it not only controls the message at home but also attempts more actively to export censorship. This is precisely what the western governments are now trying to counteract, for their own political purposes. The bottom line is that the 2008 Beijing Olympics reflected China’s strengths in stark contrast with the failures of democratic capitalism, while the 2022 Olympics are likely to highlight the opposite: China’s weaknesses, even as the liberal democracies attempt a revival of their global leadership. Jesse Anak Kuri Associate Editor Jesse.Kuri@bcaresearch.com Section II: GeoRisk Indicator China

China: GeoRisk Indicator

China: GeoRisk Indicator

Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

United Kingdom

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Canada

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Taiwan

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Australia

Australia: GeoRisk Indicator

Australia: GeoRisk Indicator

Section III: Geopolitical Calendar