Asset Allocation

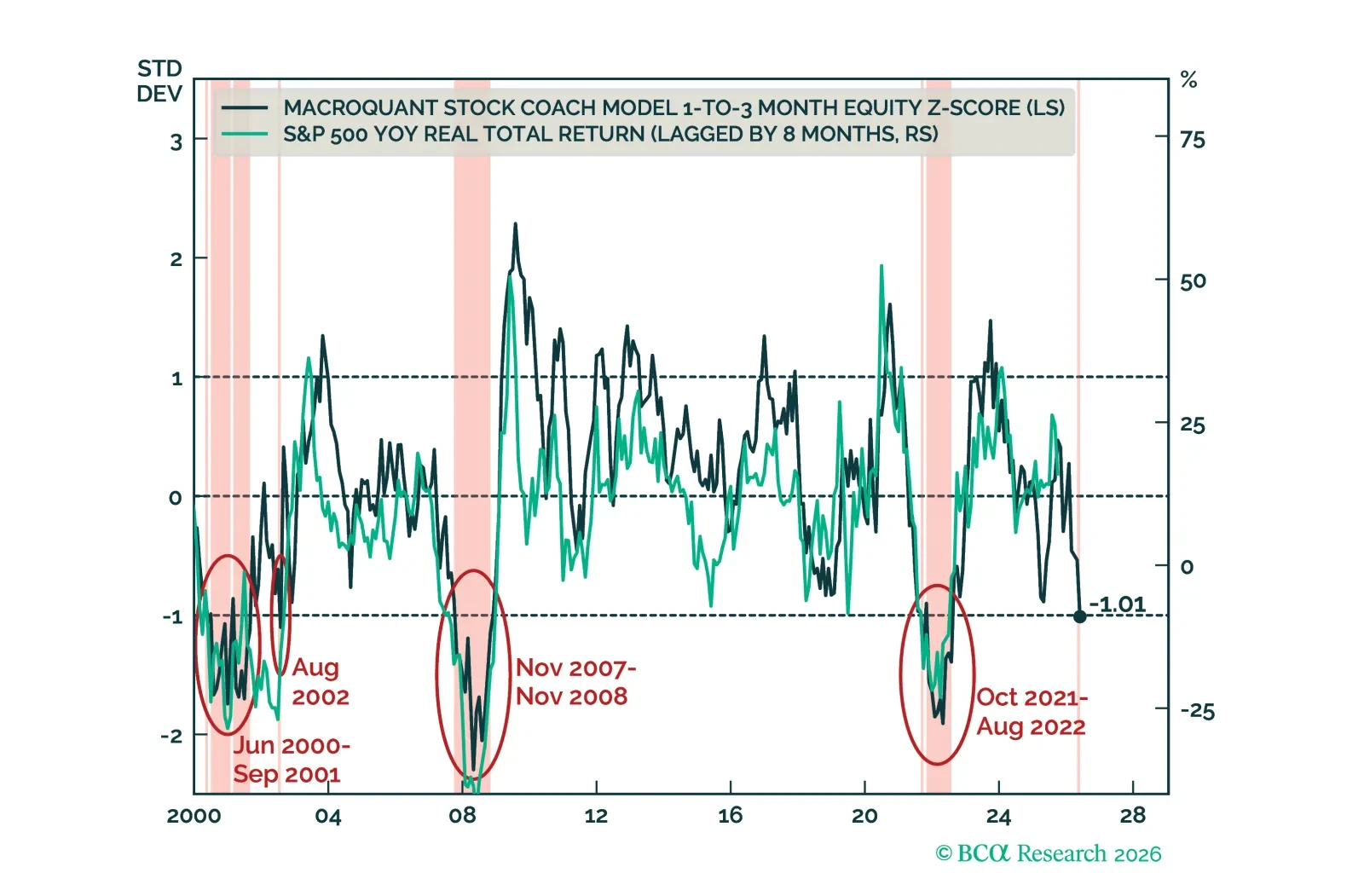

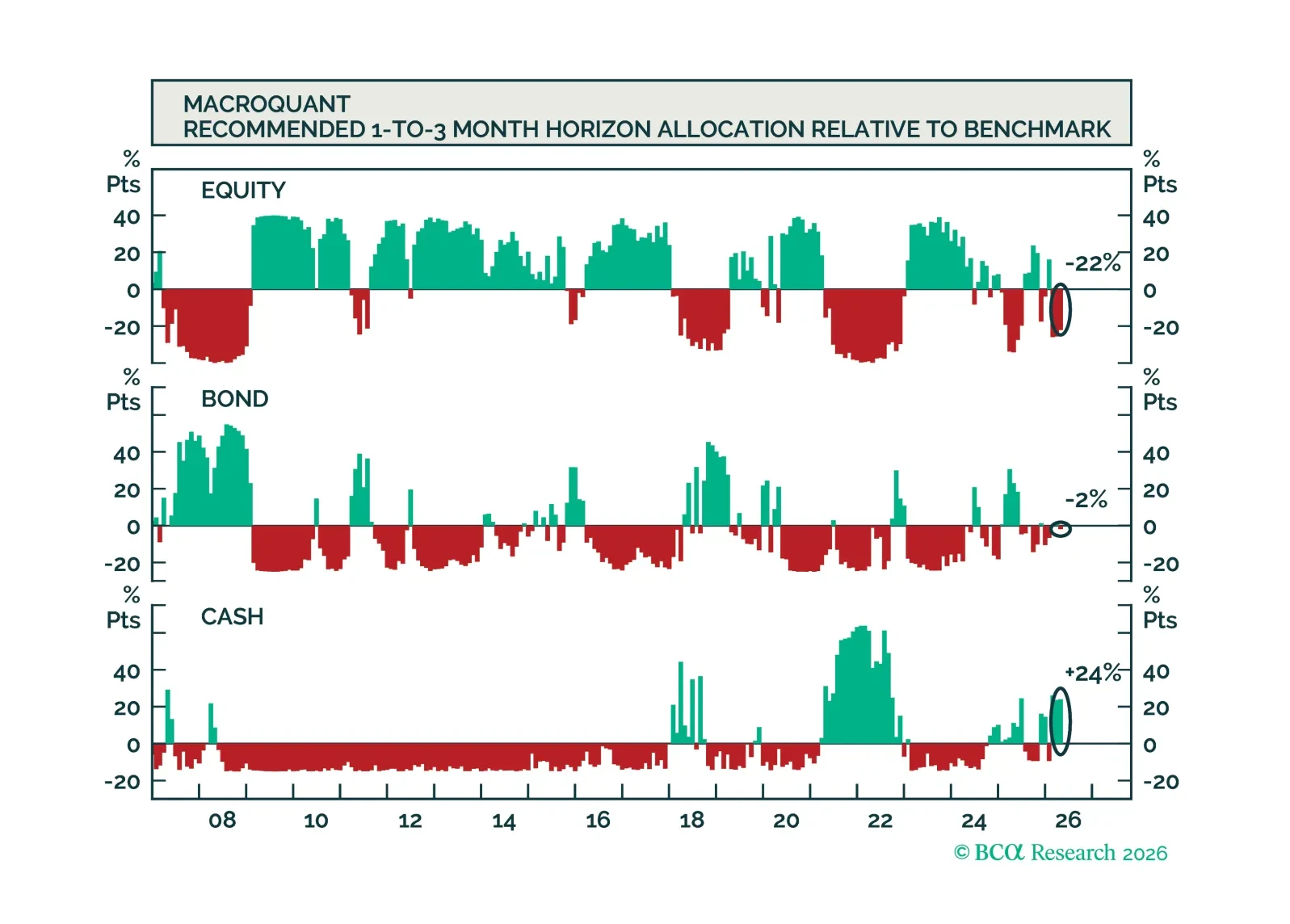

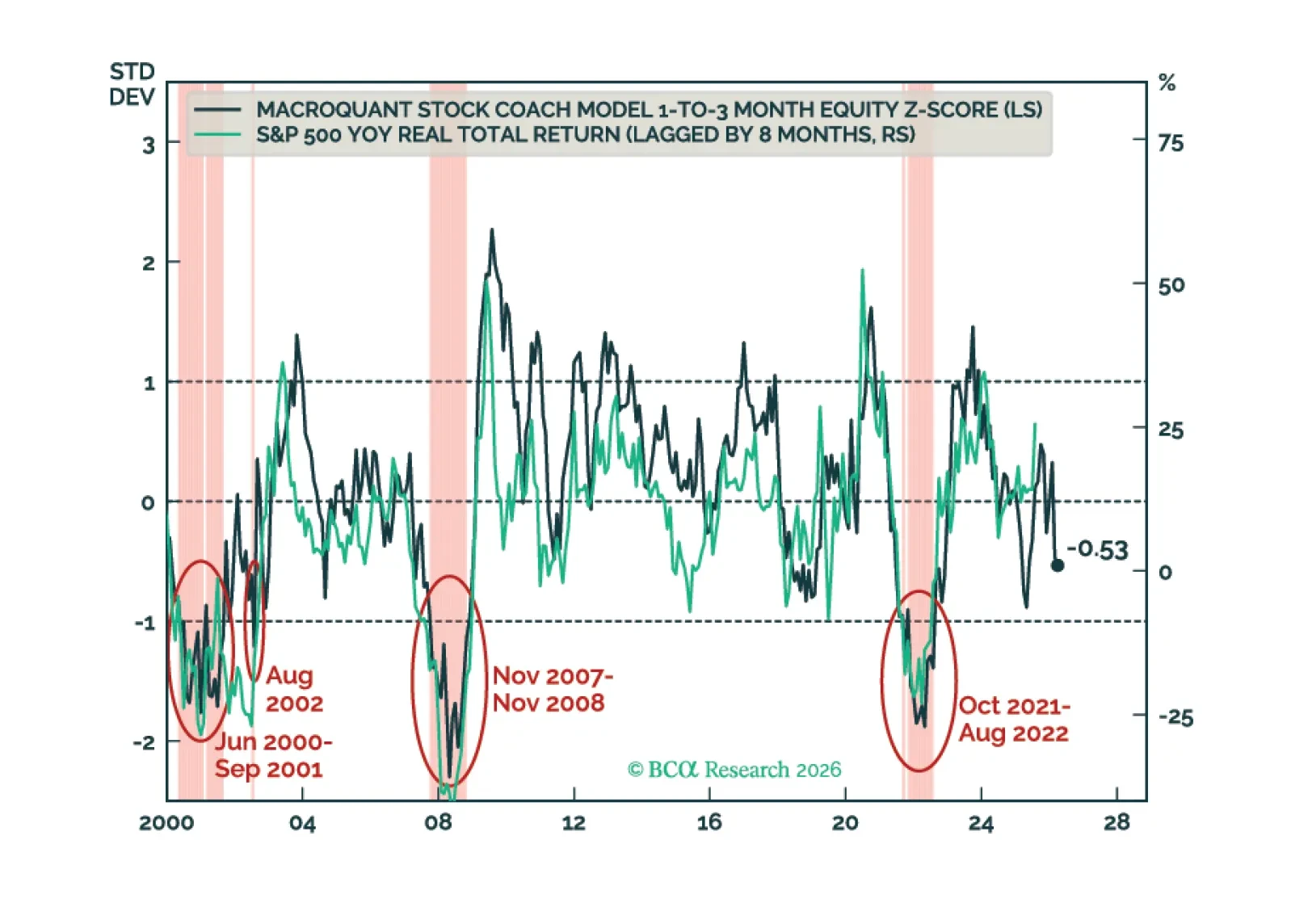

On Friday, the MacroQuant equity z-score fell to -1.01, below the critical -1 threshold that often coincided with bear markets in the past. With that in mind, today, I am downgrading stocks to a slight underweight on both a 3-month and a 12-month horizon.

So far most of the value in the AI supply chain has been captured by hardware companies. However, as model providers shift to usage-based pricing, value will begin to accrue to models and applications. Communications Services and Software should benefit from this shift. This broadening of the AI story, along with solid economic momentum should keep the rally going for the rest of the year. Remain overweight equities. Downgrade Energy to Neutral. Buy Software.

MacroQuant recommends a slight underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is very positive on the US dollar, downgrades gold to underweight, upgrades copper to overweight, and remains very bullish on oil.

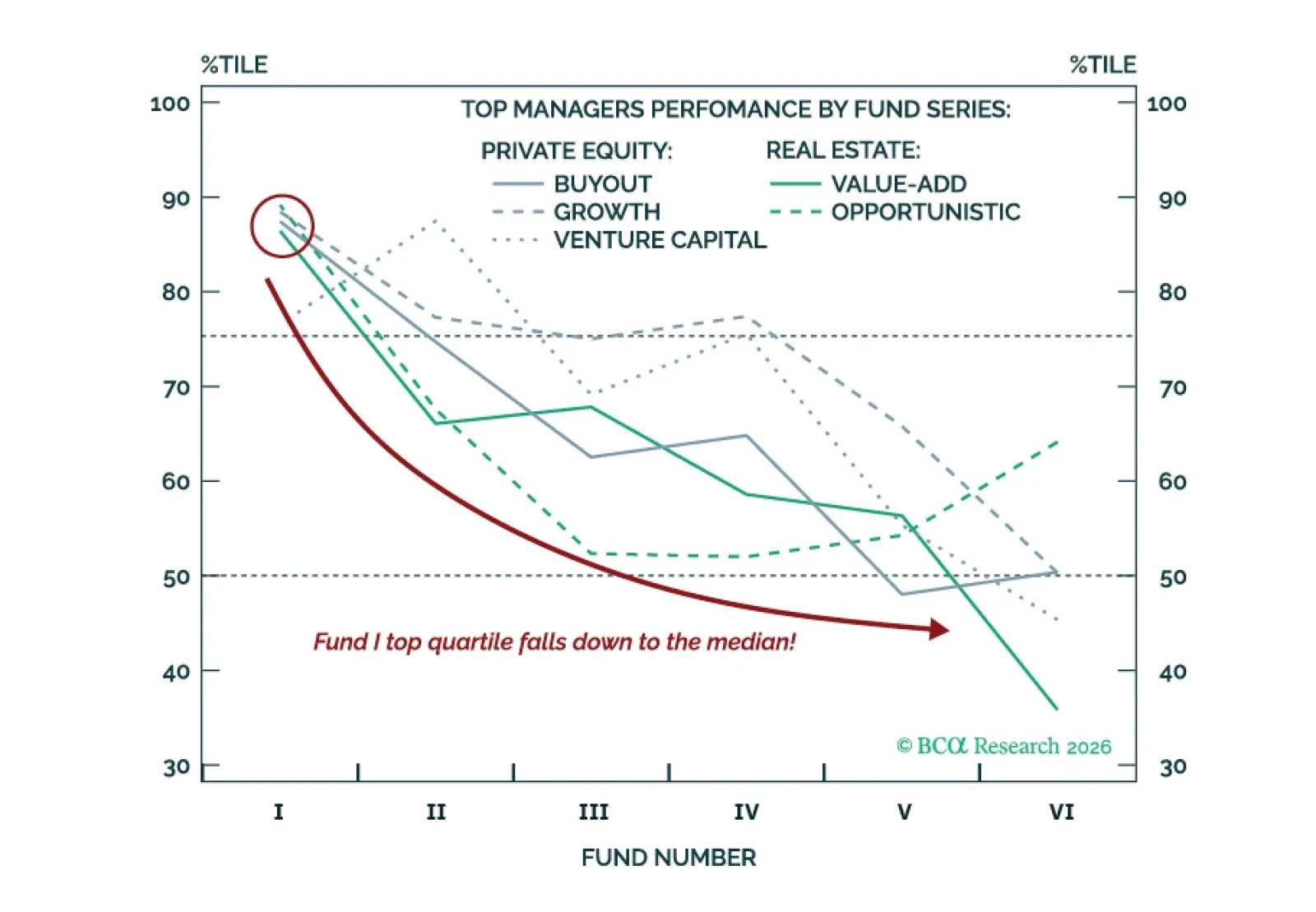

In Private Markets, yesterday’s winners often see outperformance fade. Top-quartile managers often regress toward the median as fund series mature. For investors evaluating the next Real Estate or Private Equity manager: Bias toward underweighting Funds V and beyond.

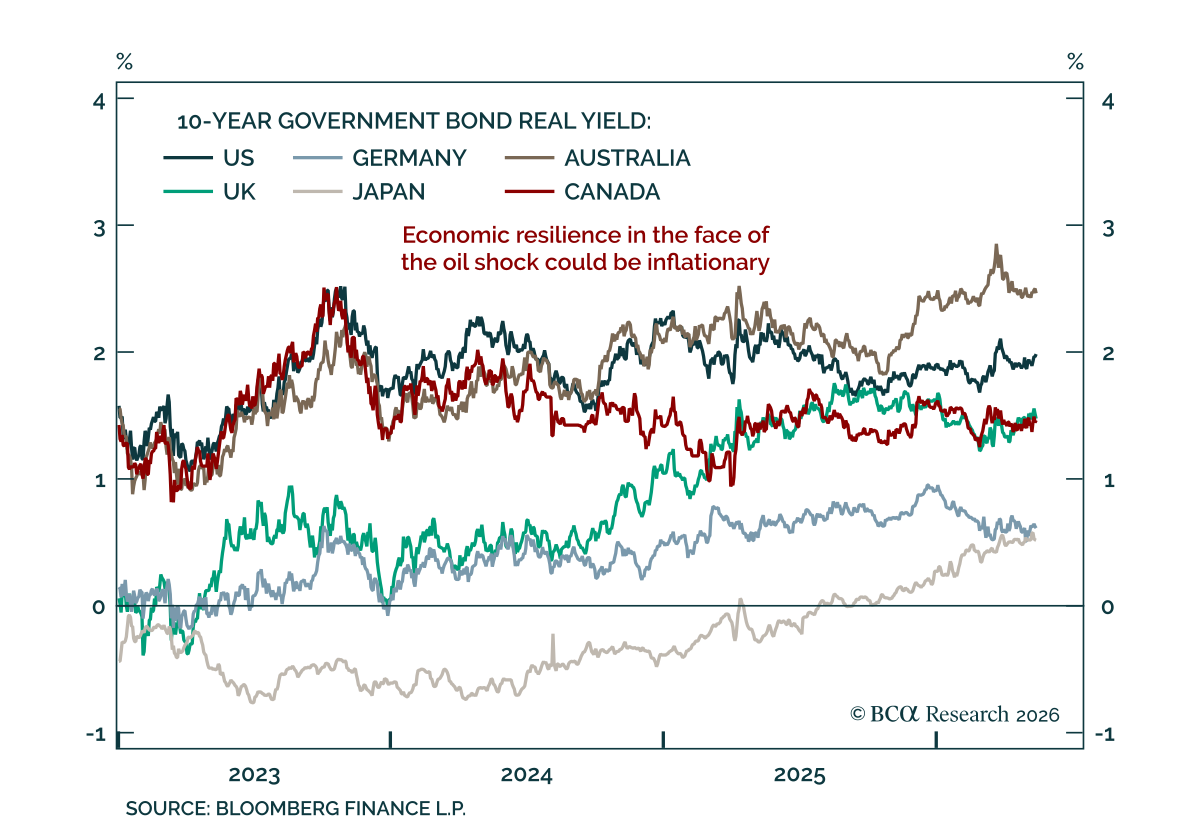

The Strait of Hormuz remains closed. Even if the Strait were to open tomorrow, global consumers will be squeezed for the rest of the year. However, AI capex is accelerating, and signs of ROI are emerging. This capex boom will keep the world from an economic downturn. Upgrade equities to overweight and downgrade cash to underweight. Upgrade the US and downgrade Europe and Australia. Upgrade Communication Services.

MacroQuant recommends an underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is neutral-to-slightly positive on the US dollar, remains neutral on gold, upgrades copper to neutral, and is very bullish on oil.

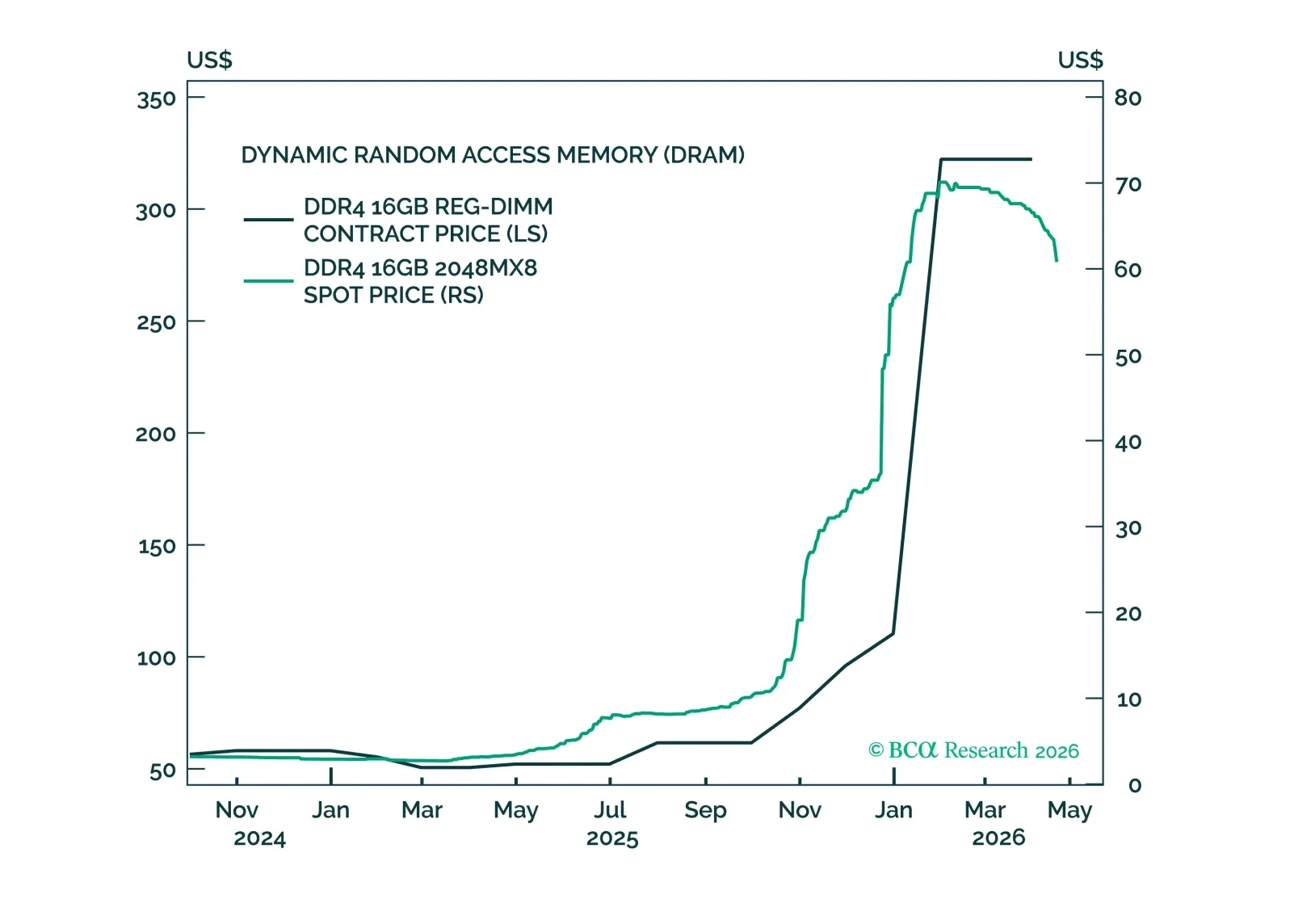

Most of the increase in S&P 500 earnings estimates this year has stemmed from shortages. The oil shortage, which has pushed up estimates for energy companies, will fade once the military conflict is resolved. However, the shortage of semiconductors and other AI paraphernalia could persist for a while longer. As such, we are moving our recommended 12-month equity allocation from a slight underweight to neutral. We are already neutral on a 3-month horizon.