AI

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

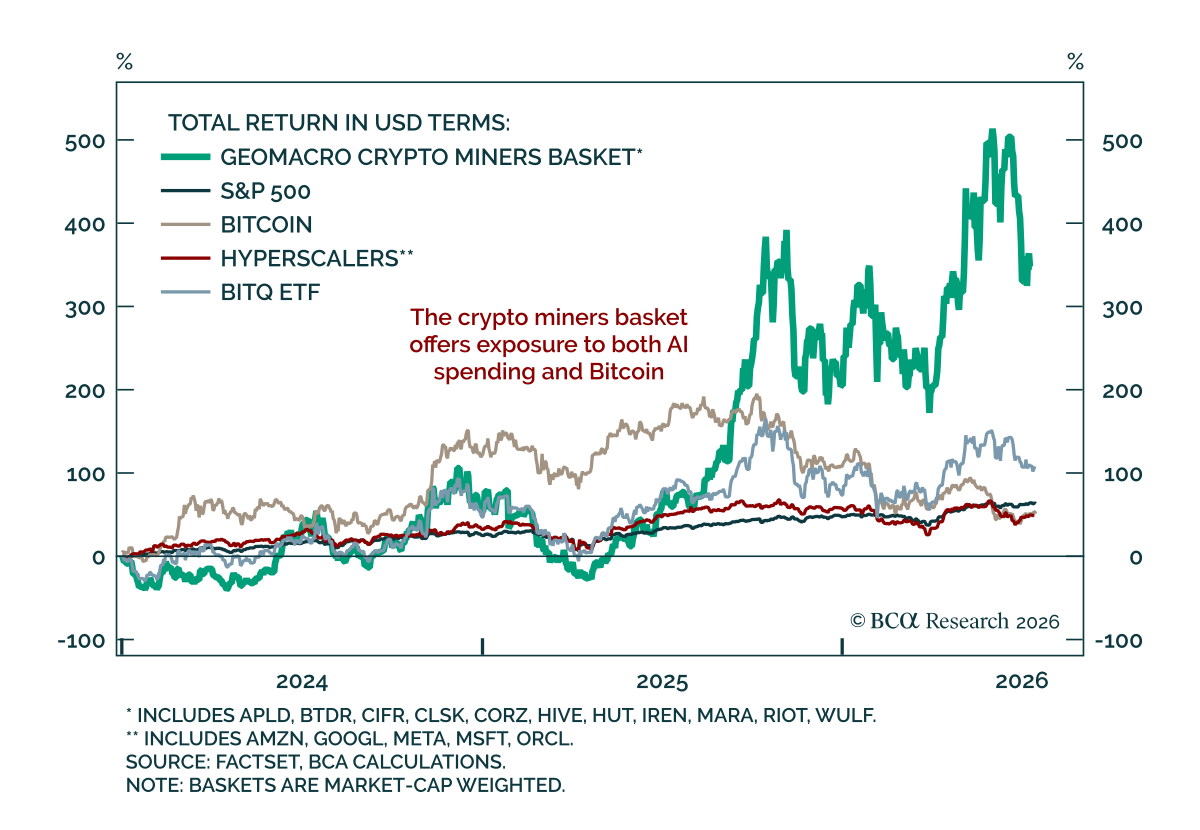

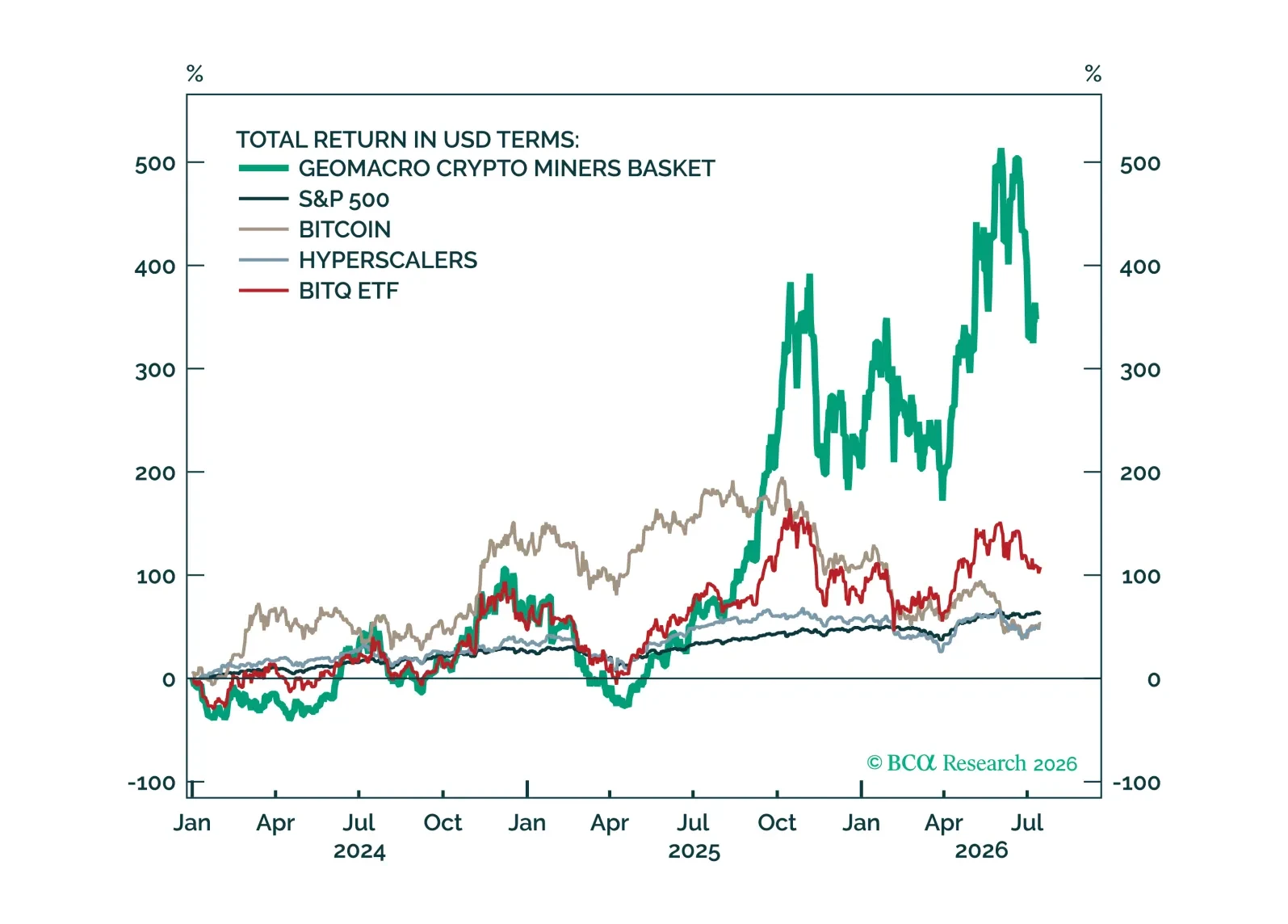

Bitcoin miners are transitioning from a pure crypto play to AI infrastructure landlords, offering investors exposure to both a crypto recovery and the surge in secular power demand driven by the AI capex buildout.

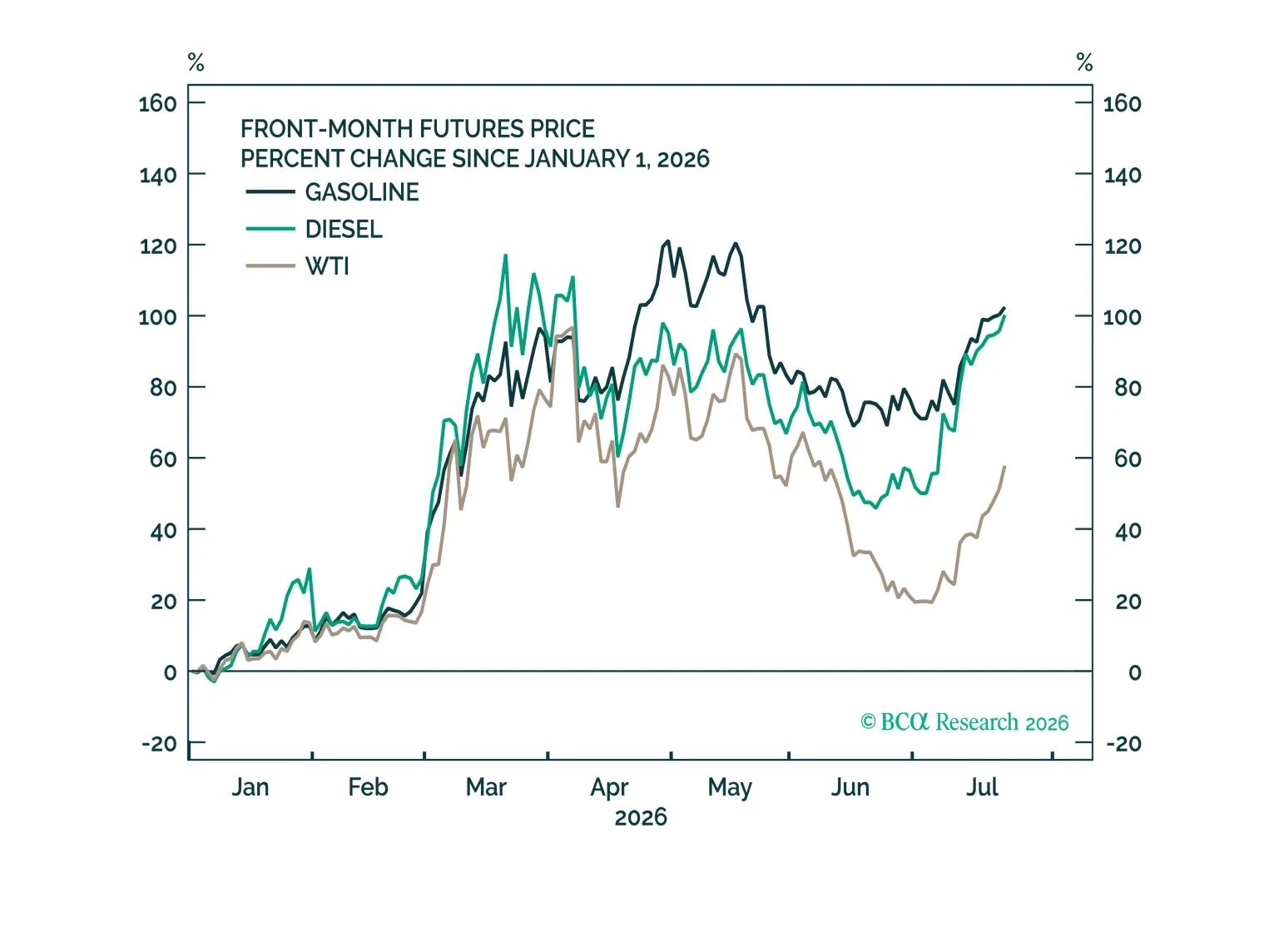

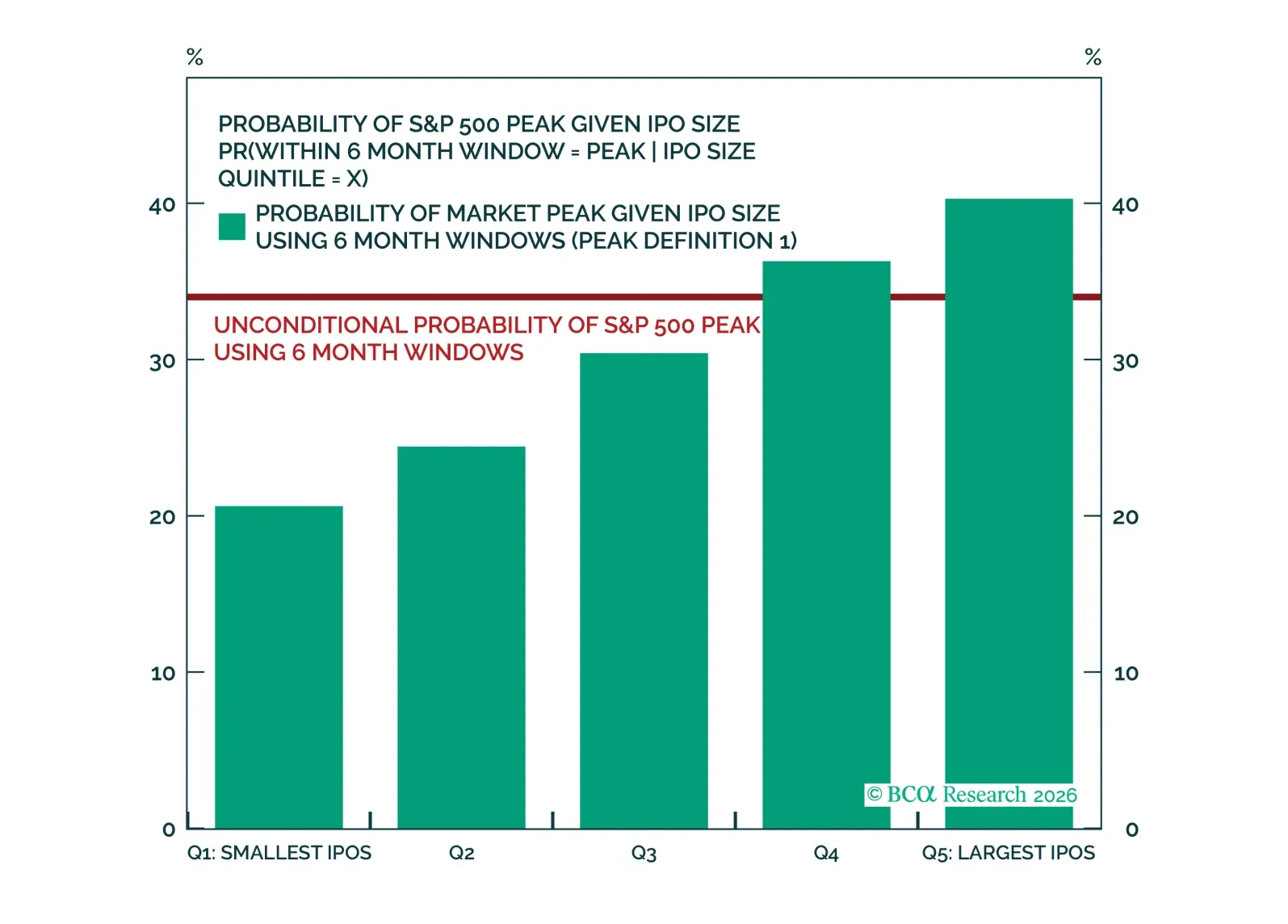

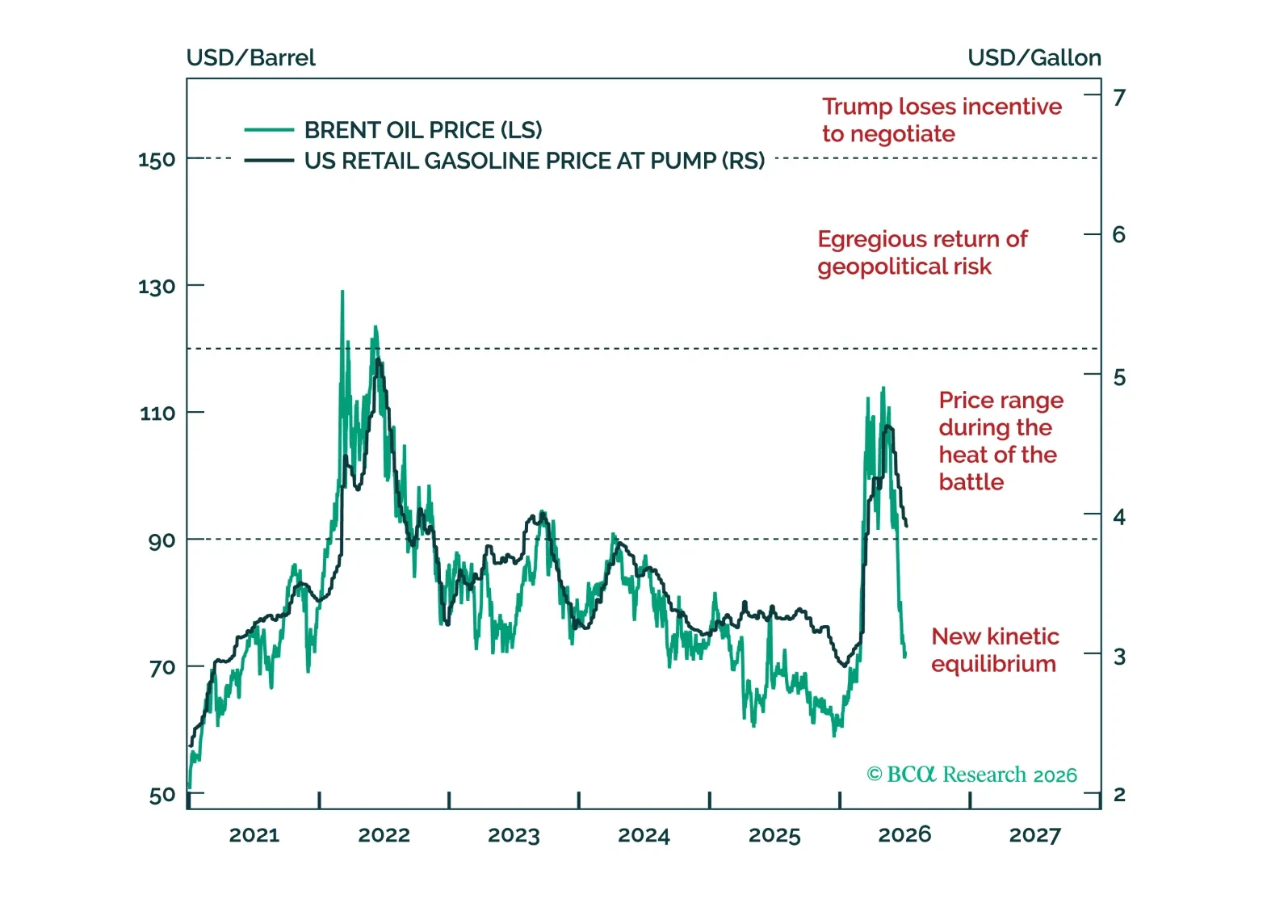

We stick to the view that geopolitical risk has peaked. The US and Iran tensions will increase oil prices, but below a level that will matter for the market. With global liquidity ample, private sector leverage low, and inflation peaking, bears are holding onto an epic collapse of the AI capex to short stocks. Eventually, the capex cycle will end in tears. That much history teaches us. But not yet.

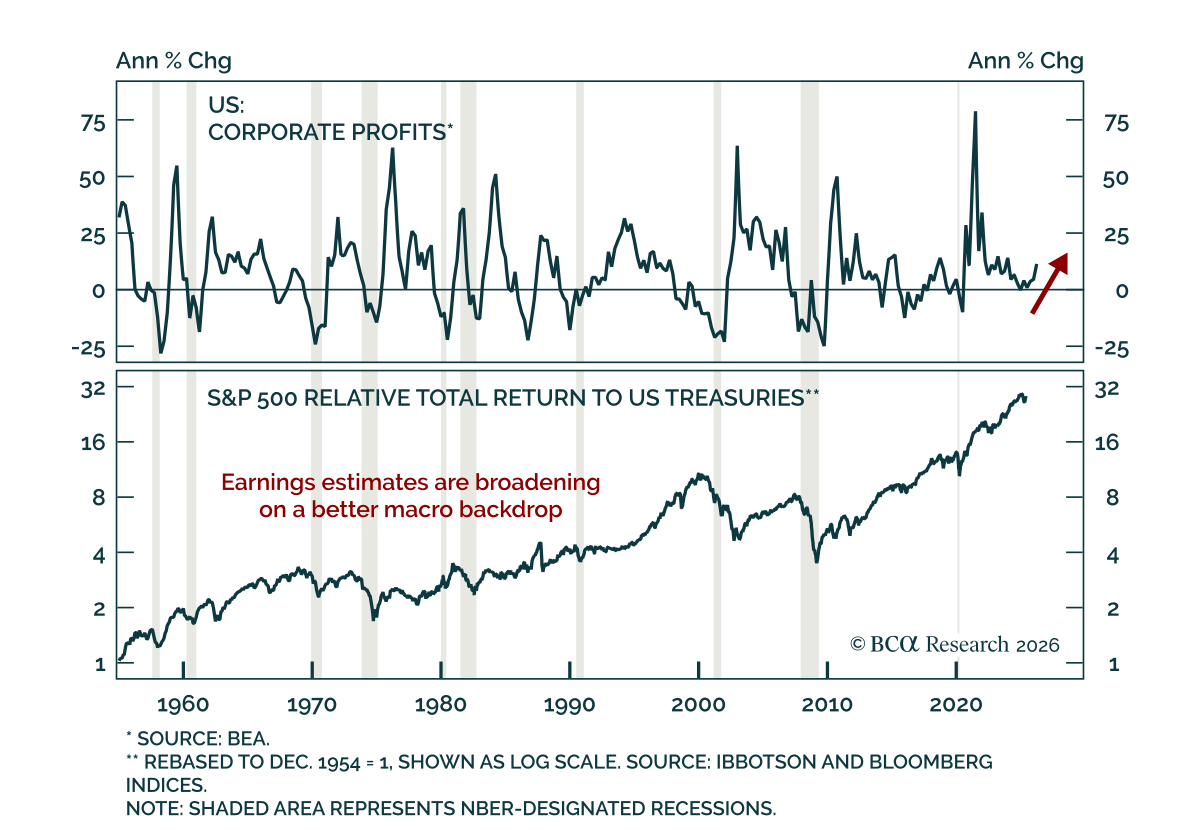

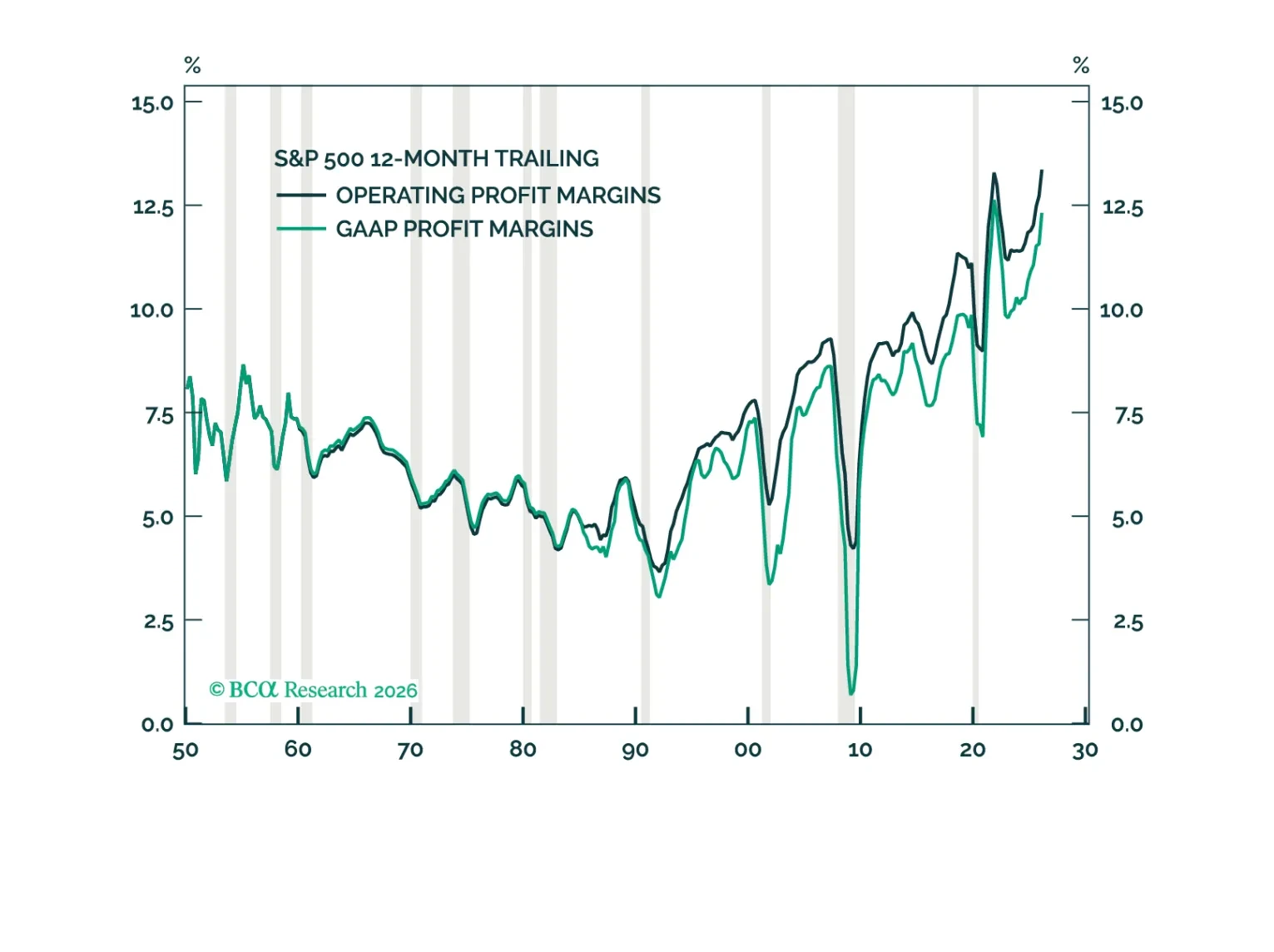

The Goldilocks environment for US profit margins should start to sour next year. Contrary to conventional wisdom, AI could end up eroding margins for both producers and consumers of artificial intelligence.

We remain bullish on risk assets given that the Hormuz war has resolved itself and oil prices have declined by even more than we expected. In addition, the macro fundamentals are not flashing any red signs. That said, we remain skeptical that the AI revolution will continue without any hiccups. In fact, a price war may ensue once all the players realize they’re in the commodity – not tech – space.