The US Consumer Is Not Flinching Yet

The April Conference Board survey beat estimates, with both current conditions and expectations improving. Consumer confidence rose to 92.8 from 92.2, when consensus expected a pullback. Consumers’ assessment of their present situation was mostly flat after positive revisions to the prior month, while expectations improved. The labor differential, measuring jobs as “plentiful” versus “hard to get” also improved, suggesting geopolitical uncertainty has not affected perceived labor-market strength.

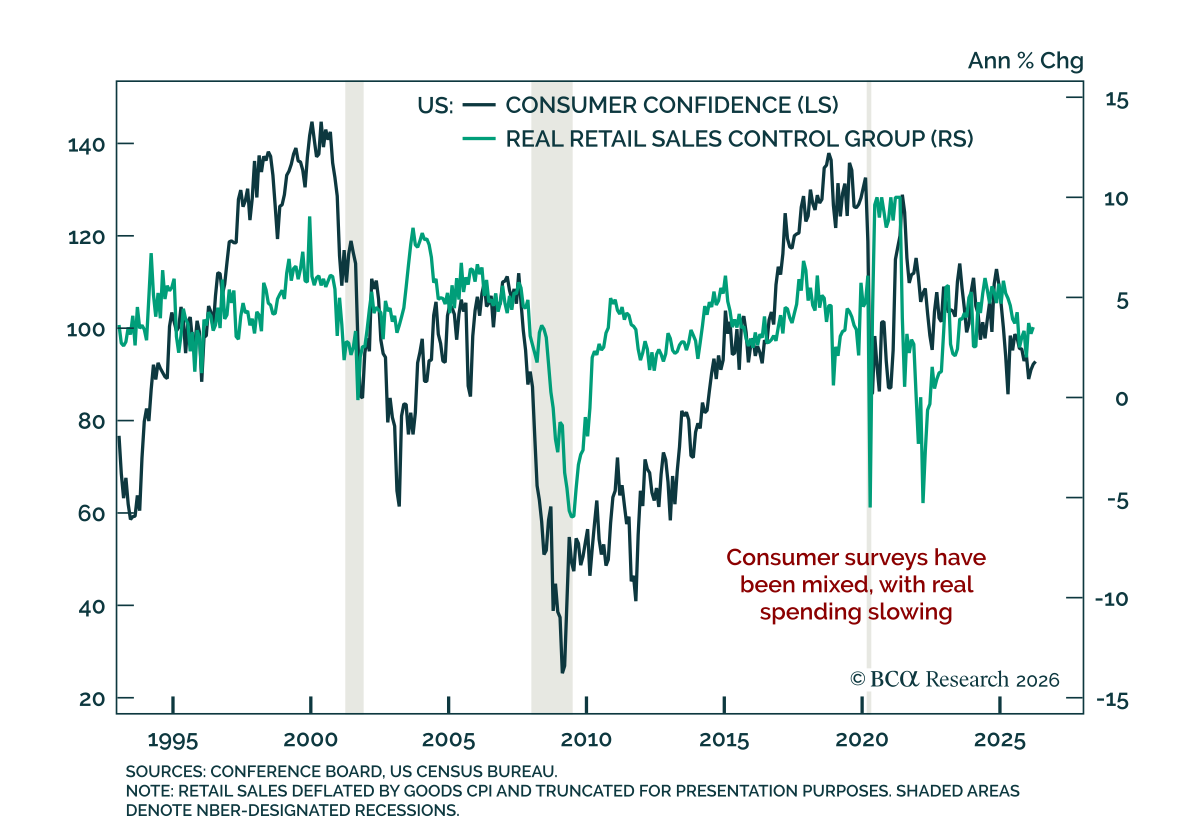

Consumer surveys are sending mixed signals. While the Conference Board measure improved, the University of Michigan survey deteriorated. The difference reflects each survey’s focus: The Conference Board has historically been more sensitive to the labor market, while the Michigan survey tends to be more sensitive to inflation. The latest consumption data were mixed as well. March retail sales were likely boosted by inflation and pointed to stalling real spending.

While not recessionary yet, this combination points to moderation. Outright contraction in nominal spending rarely occurs outside recessions. A reaccelerating labor market would support spending, but it remains too early to make that call. We have recently considered moving to a tactical overweight on risk assets, but the lack of progress on Hormuz is keeping us patient.