An Uneven Inflation Shock

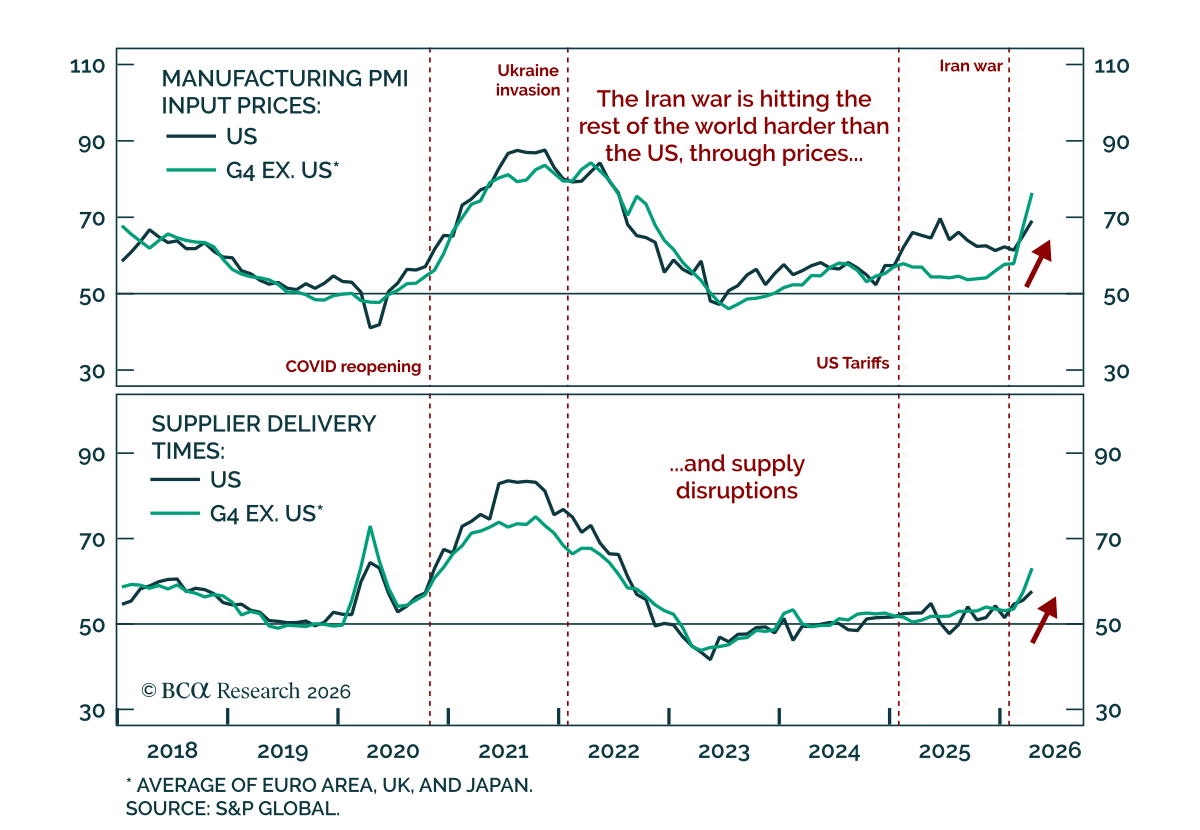

The April flash PMIs show that the global energy shock is feeding through unevenly, with sharper price pressures outside the US. Longer delivery times were widespread across developed markets, and input prices rose. One of our most timely tools for tracking inflation is our price pressure index, which combines the input prices and supplier delivery times components of PMIs. By combining those two and excluding output prices, the index aims to capture pipeline inflation pressures, which tend to lead consumer inflation. The price pressure indexes also tend to be closely correlated with goods inflation across countries and regions.

Price pressures are more widespread in Europe and Japan, reflecting their greater dependence on Hormuz for energy and petrochemical supply. Yet this shock differs from 2022: The global economy is much weaker than it was then. Second-round effects, where stronger growth lifts wage growth, are unlikely at this stage. The Iran war is already the fourth inflationary shock of the 2020s, after the COVID reopening, Russia’s invasion of Ukraine, and the 2025 US tariffs. Central banks can do little against a supply-side inflation shock and are likely to hike meaningfully only if long-term inflation expectations become unanchored. Long-term expectations remain anchored for now, but repeated supply shocks have made them more fragile.

We therefore expect most major central banks to stay on hold until more clarity emerges on the impact of the shock. Fed Governor Waller had been a leading dove until recently, but has since shifted and signaled that staying put is now the appropriate stance. A sidelined Fed means it is too early to put on curve steepeners to bet on a dovish pivot, but also that low rates volatility should remain a tailwind for risk assets.