Sentiment Snaps In Europe

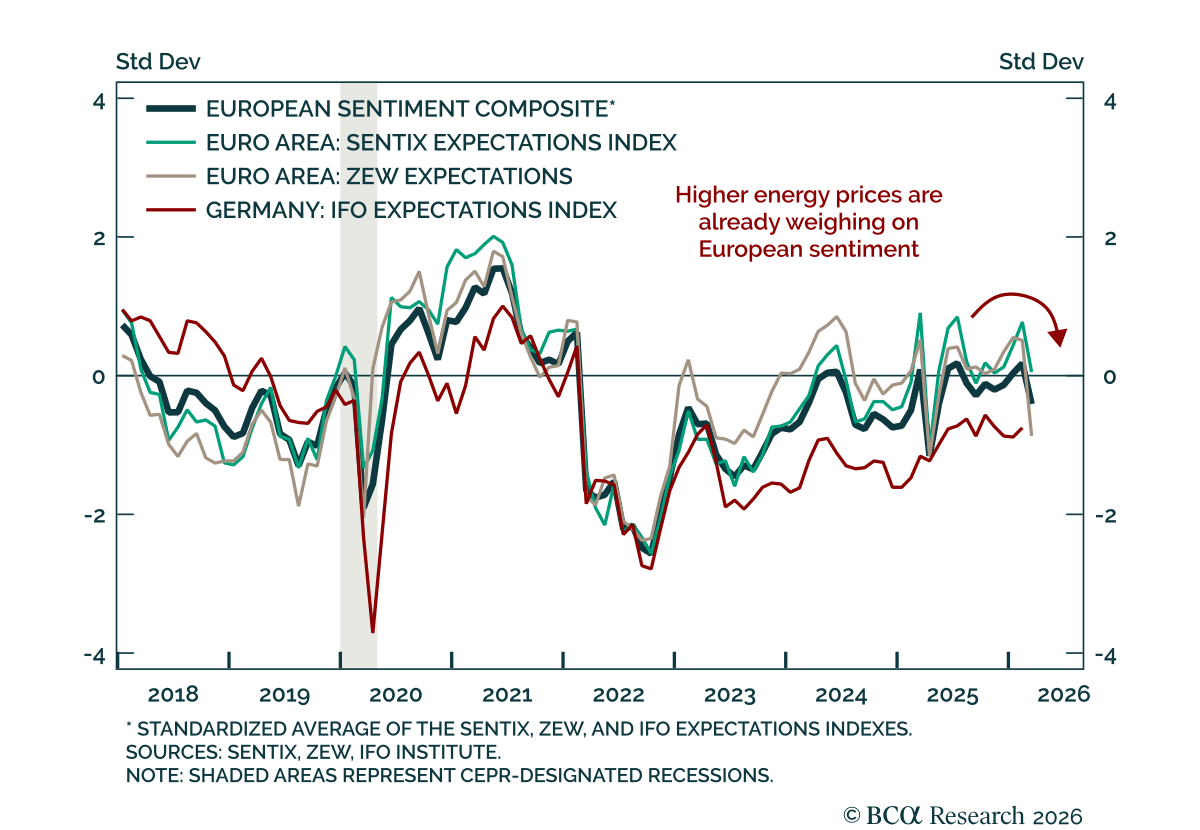

European sentiment plunged in March, reflecting vulnerability to higher energy prices. The ZEW expectations index fell sharply to -8.5 from 39.4 at the Euro Area level and to -0.5 from 58.3 in Germany. German current conditions were better than estimates but remain deeply pessimistic at -62.9. The decline is consistent with the March Sentix release, which showed a similar deterioration in sentiment.

The alignment across sentiment indicators is notable, as these measures had been dispersed prior to the Iran conflict and showed no clear momentum. While still early, there is already evidence of a sharp deterioration in European sentiment in response to higher energy prices. This pattern is also consistent with early March data in the US, where manufacturing activity has remained relatively unchanged but sentiment has weakened amid geopolitical uncertainty.

Europe remains more vulnerable than the US to a prolonged energy shock due to its reliance on imported energy. The European economy is anchored by the Rhine industrial cluster fed by energy infrastructure in the West, with natural gas as a key input. Recent cross-asset price action has been driven largely by oil, with European equities underperforming. Sector composition helps explain the divergence, as European benchmarks have a higher share of industrial companies sensitive to energy costs, while the US market is more heavily weighted toward technology. Given weaker pre-Iran momentum and higher energy vulnerability, near-term conditions continue to favor US assets over Europe’s, including equities and currency.